IN THIS ISSUE:

1. The US Economy Tanked in the 1Q, But Why?

2. 2Q Growth to Quicken but Still Another Slow Year

3. Will Fed Alter “Taper” Due to Weak GDP Report?

4. Lots of New Faces on Fed Open Market Committee

5. The Beginning of the End of the Stock Bull Market

Overview

Today we take a closer look at last week’s very ugly 1Q GDP report and see if we can discern why it was so much worse than anyone expected (hint: it was more than the severe winter weather). Fortunately, it continues to look like 2Q growth will come in at +3.0% or better. But even if GDP for the rest of the year comes in strong, the devastating 1Q will ensure yet another slow growth year.

The stunning 1Q GDP report immediately raised the question of what the Fed will do in response. Will the Fed slow down its methodical reduction of QE bond purchases? Will it put the so-called “taper” on hold? Or will it continue to taper as planned and end the program in the fall? I’ll share my thoughts as we go along today.

Finally, one well-known financial writer – Mark Hulbert – believes that the recent decline in corporate profits spells the beginning of the end of the bull market in stocks. I have reprinted his latest article below, and I suggest you read it and give it some serious thought.

The US Economy Tanked in the 1Q, But Why?

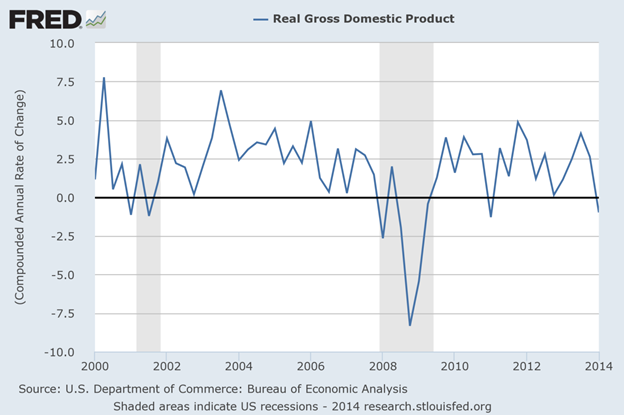

By now the whole world knows that the US economy plunged much worse than expected in the first three months of this year. Last Wednesday, the Commerce Department reported that 1Q GDP shrank at an annual rate of -2.9% in its third and final estimate. That was much worse than the pre-report consensus of -1.8% and was the worst reading in five years.

In the second estimate in May, the government reported that 1Q GDP was -1.0%. The difference between the second and third estimates was the largest on record going back to 1976, the Commerce Department said. Growth has now been revised down by a total of 3.0 percentage points since the government’s initial estimate was published in April, which had the economy expanding by a modest 0.1%.

The economy’s woes in the 1Q have been largely blamed on the unusually cold winter. However, most economists agree that the cold weather only slashed 1.0-1.5 percentage points from GDP growth in the 1Q. (The government does not report statistics on the economic impact of the weather.)

The magnitude of the latest downward revisions confirms that other factors were at play beyond the weather, as I have suggested for several months. So what were those other negative factors?

Recent data have confirmed that healthcare spending was much weaker than expected in the 1Q, which I discussed in some detail last week. Actual health spending came in substantially lower than expected based on Obamacare enrollments and Medicaid data, declining at a 1.4% annualized pace in the 1Q, compared with the May estimate of a 9.1% increase. That’s a huge revision! Yet with all of the uncertainty surrounding Obamacare, this should not have been such a big surprise.

Consumer spending, which accounts for more than two-thirds of US economic activity, was reported to have increased by 3.1% (annual rate) in the May estimate; however, in the latest report, this key reading was revised down to only 1.0%. That was very disappointing.

Trade was also a bigger drag on the economy than previously thought. Exports declined by 8.9%, instead of 6.0% estimated in May, resulting in a trade deficit that further reduced GDP growth.

Businesses accumulated fewer inventories than estimated in May. A measure of domestic demand that strips out exports and inventories expanded at a 0.3% rate, rather than a 1.6% rate estimated in May. Both residential and non-residential fixed investment were revised lower as well.

For all the reasons cited above, the final 1Q GDP number was the worst since the 1Q of 2009.

2Q Growth to Quicken but Still Another Slow Year

As I discussed last week, most forecasters believe that 2Q GDP will come in much stronger. Several are revising their estimates higher, despite the terrible 1Q report. Last week, consulting firm Macroeconomic Advisers increased its forecast for 2Q growth to 3.5% from 3.3%.

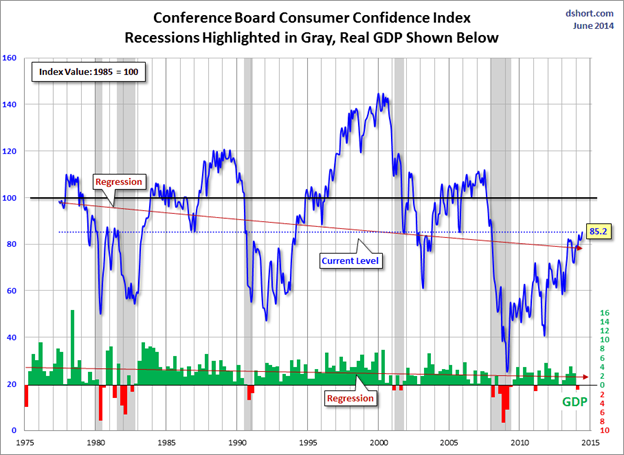

Consumer confidence is at the highest level today since January 2008 (for more on that, see my blog last Thursday). Since consumer spending makes up over two-thirds of GDP, that explains why some forecasters now believe that GDP could be up as much as 4% for the April–June quarter that ended yesterday.

As the chart above illustrates, consumer confidence is still well below pre-recession levels, and we should keep in mind that consumer confidence can change quickly. Let’s hope not this time.

Let’s be generous and say that the economy grew by 4% in the 2Q and continues to do so for the rest of the year – a level only attained twice in the last five years – the overall growth rate for 2014 would still work out to only a tepid 2.2%.

The first estimate of 2Q GDP will be released on Wednesday, July 30 at 8:30 AM Eastern.

Will Fed Alter “Taper” Due to Weak GDP Report?

Not long after the GDP report came out last Thursday, analysts quickly turned to the question of how the bad news might affect the Fed. Might it influence the Fed to put its bond-buying taper on hold for a while? Since late last year, the Fed has been reducing its purchases of Treasury and mortgage bonds by $10 billion at each FOMC policy meeting.

The last policy meeting was on June 17-18 at which time the FOMC reduced bond purchases by another $10 billion, to $35 billion per month, down from the high of $85 billion late last year. The next policy meeting will be on July 29-30 when the Fed is expected to reduce purchases to $25 billion a month.

After that, the next FOMC meeting will be on September 16-17 when purchases would likely be cut to $15 billion, followed by the next meeting on October 28-29 when some analysts believe the Fed will vote to stop all QE purchases.

But does last week’s dreadful GDP report suggest that the Fed will alter its taper course? While the Fed is intent on reducing bond purchases as described above, it has always left its taper options open with the following qualifier:

If incoming information broadly supports the Committee's expectation of ongoing improvement in labor market conditions and inflation moving back toward its longer-run objective, the Committee will likely reduce the pace of asset purchases in further measured steps at future meetings. However, asset purchases are not on a preset course, and the Committee's decisions about their pace will remain contingent on the Committee's outlook for the labor market and inflation…

Former Fed Chairman Ben Bernanke often reassured markets and the media that if the economy faltered, the Fed would not hesitate to stop the taper – and even increase bond purchases – if need be. It is widely assumed that New Fed Chair Janet Yellen, widely seen as the most “dovish” member of the FOMC, feels the same way.

In any event, the Fed clearly believes that the economy has improved significantly in the 2Q. The FOMC’s June 18 policy statement opened as follows regarding economic conditions:

Information received since the Federal Open Market Committee met in April indicates thatgrowth in economic activity has rebounded in recent months. Labor market indicators generally showed further improvement… Household spending appears to be rising moderately and business fixed investment resumed its advance, while the recovery in the housing sector remained slow. [Emphasis added.]

So anything could happen at the policy meeting at the end of July. My bet is that the FOMC will take the position that the events of the 1Q are in the past, that it was largely (but not entirely) the result of the bitter winter and move to cautiously continue the taper.

Lots of New Faces on Fed Open Market Committee

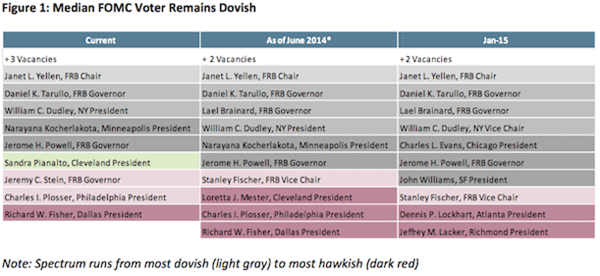

Over the past year, 75% of the FOMC’s membership has changed – more than twice the normal rate. The reason is the departure/retirement of five FOMC members: Chairman Ben Bernanke, Sarah Raskin, Elizabeth Duke, Jeremy Stein and Sandra Pianalto earlier this year. Add to that the annual rotation of four Federal Reserve Bank presidents, and that makes nine new faces out of 12 this year.

The FOMC is made up of 12 voting members – seven members of the Federal Reserve Board including the Chairman (or “Chair” in the case of Janet Yellen), plus the Vice Chairman, the president of the Federal Reserve Bank of New York and four Federal Reserve Bank presidents who rotate annually.

The chart below (middle column) shows the current voting makeup of the FOMC. You’ll notice that the background shading denotes policy leanings from most “dovish” (Yellen) to “hawkish.” Dovish members are likely to favor more liberal monetary policies such as QE and higher inflation, while hawkish members are likely to favor more conservative policies, lower inflation and less intervention by the Fed.

My favorite members of the FOMC are Richard Fischer (Dallas), Jeffrey Lacker (Richmond) and Charles Plosser (Philadelphia). These three were not big fans of QE.

So as you can see above, the FOMC is still dominated by policy doves who favor more liberal programs like QE. Plus, President Obama will nominate two more new members to fill the two current vacancies, and it’s a safe bet that these two new members will also be doves.

The Beginning of the End of the Stock Bull Market

We'll round-out today’s letter with an interesting article from Mark Hulbert, the well-known Editor of the circa-1980 Hulbert Financial Digest, which tracks the performance of investment newsletters. In the following piece, Mark argues that the very recent decline in corporate profits is likely to continue over time as they“revert to the mean.” If so, we may be looking at the beginning of the end of this aging bull market in stocks.

For the last couple of months, I have been concerned that the market is setting up for a downward correction of 15-20%. Mark believes it may be worse than that. So you may well want to read the following (well done as always) article and give it some serious thought.

QUOTE:

by Mark Hulbert

(MarketWatch, June 25) — Few paid attention a couple of weeks ago when the government announced that corporate profitability had declined markedly last quarter.

Yet future historians may eventually look back and pinpoint that report as the beginning of the end of this aging bull market.

That’s because the first-quarter’s decrease could signal the long-awaited return to historically average profitability levels. If so, the stock market will have to struggle mightily just to keep its head above water over the next five years.

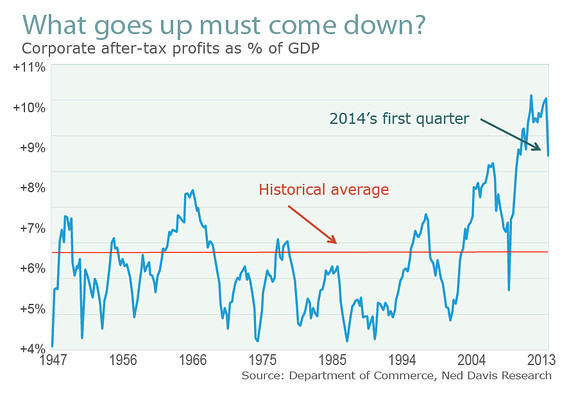

Here’s the sobering data: According to the latest calculations of the U.S. Department of Commerce, corporate profits in the first quarter of this year represented 8.8% of gross domestic product. That’s the lowest level in nearly four years, and represents a big drop from the 10%-plus profitability that prevailed in the last quarter of 2013.

Those who focus on corporate profitability have worried for some time that such a decline was imminent. That’s because, in the past, profit margins have exhibited a strong tendency to “revert to the mean,” according to James Montier, a member of the asset allocation team at Boston-based GMO. In other words, margins in the past have eventually declined whenever they rose significantly above their long-term average, and vice versa.

That long-term average is 6.3%, according to the government’s data. Unless corporate profitability has reached some kind of permanently high plateau, the recent drop is just the beginning of a much bigger decline.

What would it mean for the stock market if profitability reverted to the historical mean?

To calculate the consequences of a reversion to mean of corporate profitability, we must first make a few assumptions, as follows:

-

How long it takes for the mean reversion to be complete. I’ll assume five years, which is close to historical norms, according to Montier. He says that, whenever the profit margin in the past has risen to be at least 1% above its mean, or fallen to be at least 1% below, it was back at its mean in an average of 4.8 years.

-

How fast the economy grows over the next five years. I will assume there will be no recession, which is very generous. But I’ll do so in order to make my point. I’ll assume that nominal GDP will grow over the next five years at the same pace it has since the last recession — 4.1% annualized.

-

Where the stock market’s price/earnings ratio will be in five years’ time. I will assume it stays at current levels, which once again is generous, since it is already above the long-term average today.

Once we make these assumptions, calculating the stock market’s return over the next five years becomes a matter of simple math. The picture isn’t pretty: Its five-year return, annualized, is minus 2.8%.

If so, the S&P 500 in the summer of 2019 [currently above 1,960] would be trading at 1,703.

In fact, given the data, coming up with a rosy outlook for the next five years isn’t easy. If we assume that corporate profit margins stay constant, for example, then the stock market’s future growth will be the same as economic growth. That’s 4.1% annualized on a nominal basis, given my generous assumptions.

Even a return to the record levels of corporate profitability above 10% of GDP won’t produce anything like historically average stock market returns over the next five years. The only way for that to happen is for corporate profits to take an even bigger share of GDP in the future.

While anything is possible, that seems unlikely, according to Robert Arnott, chairman of Research Affiliates. For that to happen, the share of national income going to workers would have to shrink. In that event, Arnott says, “the backlash could be so widespread that it would turn Occupy Wall Street into a mainstream event.”

END QUOTE

Obviously, no one knows for sure when this very long bull market will come to an end, but we do know it will endat some point. Whenever it does and the next bear market unfolds, passive “buy-and-hold” strategies will get hammered. It may be wise to start thinking about getting the bulk of your portfolio into actively-managed strategies that can help you avoid potentially big losses. At Halbert Wealth Management, we can help with that.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.