IN THIS ISSUE:

1. More Bad News Expected Tomorrow for 1Q GDP

2. Why Healthcare Spending Was Below Expectations

3. More Businesses Closing Than Starting Up, A First

4. Signs the Economy May Finally be Getting Traction

5. Second Quarter GDP Expected to Come in Strong

6. Texas Immigration Crisis: UPDATE (They Knew)

Overview

The government’s final estimate of 1Q GDP comes out tomorrow, and it is expected to be revised from -1.0% to near -2.0%. Based on recently released data, it is clear that healthcare spending by consumers was considerably lower in the 1Q than first estimated. We’ll look at some of the reasons why.

From there, we’ll look at some disturbing economic data which show that businesses in the US are shutting down faster than new ones are starting up. This has never happened before in America according to a new Brookings Institute study.

Next, we’ll review some recent developments which suggest economic growth has accelerated sharply in the 2Q. Most forecasts for 2Q GDP are at 3% or better. Our first look at 2Q GDP will come in late July.

Finally, there is news that the US Immigration and Customs Enforcement (ICE) agency knew back in January that a flood of undocumented children – specifically 65,000 – were going to pour across the Texas border this year. They requested help on a government website. This has the potential to be really BIG!

More Bad News Expected Tomorrow for 1Q GDP

We’ll get the Commerce Department’s third and final estimate of 1Q GDP tomorrow morning at 8:30 Eastern. You may recall that the government estimated on May 29 that the economy contracted by a full 1% in the 1Q. Most forecasters are now estimating that tomorrow’s third estimate will be even worse. The consensus is for a further reduction to -1.8%, with numerous analysts predicting a drop to -2.0% or more.

So how did they get this one so wrong? If you recall, the first estimate in late April showed 1Q GDP down by only 0.1%; then came the second estimate at down 1.0%; and tomorrow we’re expecting another downward revision to near minus 2.0%. Here’s at least part of the explanation: The main culprit it now seems was lower than expected healthcare spending by consumers in the 1Q.

The Commerce Department’s Quarterly Services Survey (QSS) showed that healthcare outlays were not nearly as strong as the government had assumed when it published its first and second 1Q GDP estimates in late April and May. With the QSS data in, the government now knows that healthcare spending in the 1Q was well below the previous assumptions.

The mainstream media has led us to believe that the weak economy in the 1Q was caused almost entirely by the severe winter weather. Yet many of us felt that it had to be about more than just the cold weather. And as I will discuss below, in retrospect, it should not surprise us that healthcare spending was lower than expected in the 1Q, given all the uncertainties surrounding Obamacare.

So don’t be surprised if we see 1Q GDP revised down to -2.0% tomorrow morning. Expect the mainstream media to respond by saying it doesn’t matter because 2Q data is looking so much stronger. While that may be true, we won’t get our first look at 2Q GDP until the end of July.

Why Healthcare Spending was Below Expectations

The fact that healthcare spending was not up as expected in the 1Q really shouldn’t have come as a big surprise. There is still so much uncertainty on the part of consumers as well as healthcare providers due to Obamacare. Most consumers don’t know just what is covered, not covered or somewhere in between.

Many consumers who have purchased health insurance on the exchanges don’t know what medical services are covered by their insurance, and in many cases are not clear about what their deductibles and/or co-pays may be – much less their federal subsidies. Likewise, many physicians are still not clear how they will get paid for many procedures and even routine patient visits. Ditto for healthcare clinics and even some hospitals.

Likewise, it is still not abundantly clear what will be paid by Medicare and Medicaid. As a result, many consumers are delaying medical procedures and even doctor visits until they are more certain of their coverage and what their deductibles and/or co-pays will be.

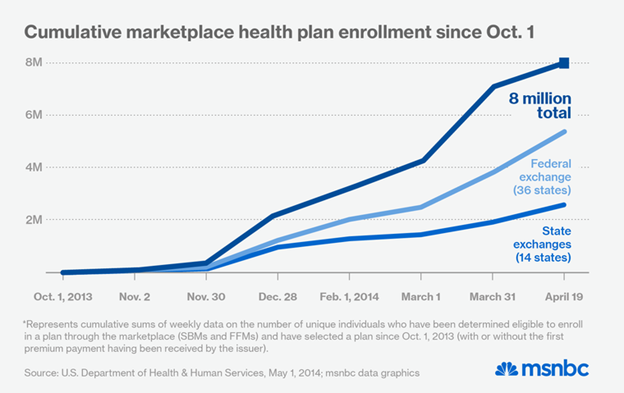

And let’s not forget that only apprx. 8 million people purchased health insurance on the federal and state exchanges during the initial enrollment period from October to April. It is not entirely clear how many of the 8 million were previously uninsured, but a recent survey from the Kaiser Family Foundation puts the number at 57%.

Also, the tepid economic recovery continues to impact the health sector. The slowdown – and even decline – in personal wealth has tamped down demand for healthcare. All of these uncertainties have created a “new normal” in healthcare spending patterns. And it’s still too early to see how all this will play out over the next few years.

More Businesses Closing Than Starting Up, A First

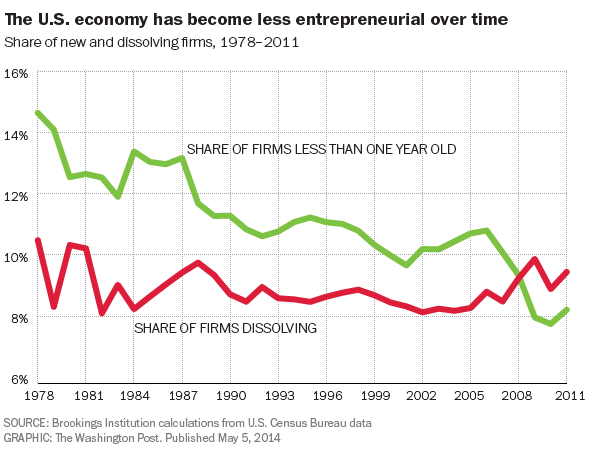

A new study from the Brookings Institute released in May found that more businesses in America have been closing down than those starting up, for the first time ever. Furthermore, this trend has continued since 2008 despite the economic recovery.

Brookings studied data from 1978 to 2011 and found that businesses were closing faster than new ones were being formed since 2008, a first for America. Overall, new businesses creation (measured as the share of all businesses less than one year old) declined by about half from 1978 to 2011. Put differently, the American economy is less entrepreneurial now than at any point in the last three decades.

Worst of all, this trend is showing no signs of reversing even though the economic recovery is now into its fifth year. The Brookings authors didn’t mince words about the stakes here: “If the decline persists, it implies a continuation of slow growth for the indefinite future.”

This lack of economic dynamism, particularly the steep drop since 2006, may be one reason why our current recovery has been so weak. The authors of the Brookings study dug beyond the national numbers to the state and metro levels and found that they generally mirrored the national trends.

Perhaps the worst statistic in the latest Brookings study is this one: From 1978 to 2011, the rate of new business formation has declined a stunning 47.2%, with the worst of the drop occurring since 2006.

The five healthiest states for business start-ups were New York, Illinois, Texas, New Jersey and Missouri. The five worst states were Alaska, Hawaii, Vermont, New Mexico and Wyoming.

Signs the Economy May Finally be Getting Traction

Enough of the bad news – let’s look at some encouraging developments. There are more recent signs that the economic recovery may be gaining some traction. The Fed periodically publishes the results of economic surveys it takes from businesses in each of the 12 Fed Districts. The so-called “Beige Book” is published eight times per year. The latest survey from June 4 showed improvement over the previous report in April. Here are some excerpts:

All twelve Federal Reserve Districts report that economic activity expanded during the current reporting period. The pace of growth was characterized as moderate in the Boston, New York, Richmond, Chicago, Minneapolis, Dallas, and San Francisco Districts, and modest in the remaining regions.

Consumer spending expanded across almost all Districts, to varying degrees. Non-auto retail sales grew at a moderate pace across most of the country… Increasingly strong new vehicle sales were reported by more than half the Districts, with most other regions seeing steady sales…Tourism was steady to stronger across most of the country--particularly in most of the eastern seaboard Districts.

Activity in the service sector, excluding finance, grew across most reporting Districts… Boston, Kansas City, and San Francisco noted particular strength among technology firms… Manufacturing activity expanded throughout the nation, and at an increasingly strong pace in a number of Districts--notably along the East Coast, as well as in the St. Louis and Kansas City Districts.

Residential real estate activity was mixed across the country, with some reports of low inventories constraining sales--specifically in the Boston, New York, and Kansas City Districts. Still, home prices continued to increase across most of the country, while the markets for both condos and apartment rentals were mostly robust… Both non-residential construction activity and commercial real estate markets were generally steady to stronger...

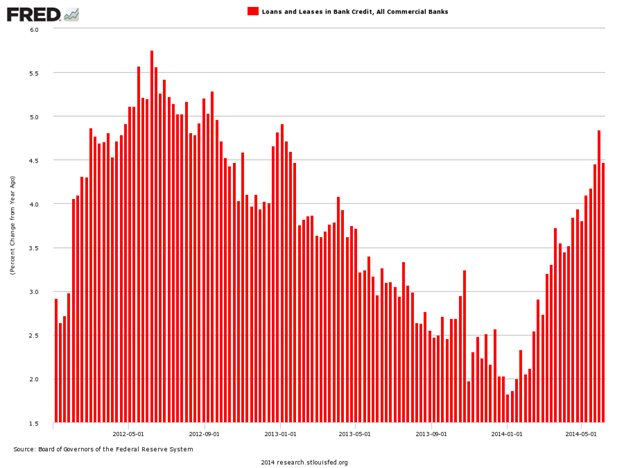

Overall lending activity increased throughout the nation. Roughly two-thirds of the Districts reported rising loan demand, with particular strength reported in New York and San Francisco. Credit quality and delinquency rates generally improved, while credit standards were mostly unchanged.

The Fed noted that the surveys’ indicators of future activity improved notably, suggesting that firms are more optimistic about continued growth over the next six months. The surveys’ indicators for general activity, new orders, and shipments were positive for the fourth consecutive month in most Districts. Current employment was also higher among most of the reporting firms in the latest survey.

As the Fed suggested above, the credit markets have improved significantly. Bank lending has certainly kicked into a higher gear. Here’s a look at the year-over-year growth in loans and leases at commercial banks.

Overall, the economic data released in May was quite solid, but some cautioned that it might be due to pent-up demand from the cold-weather winter. However, the reports we’ve seen so far in June also look strong overall. So maybe the economy has finally gotten some traction.

Second Quarter GDP Expected to Come in Strong

US wholesale inventories rose more than expected in April, bolstering views of an acceleration in economic growth to at least 3% in the 2Q. The Commerce Department reported on June 10 that wholesale inventories increased 1.1% after advancing by the same margin in March. The rise outstripped economists’ expectations for only a 0.5% gain.

Inventories are a key component of gross domestic product changes. The component that goes into the calculation of GDP - wholesale inventory excluding autos - increased 1.1%. A sharp slowdown in the pace of restocking by businesses helped to sink economic growth in the 1Q, but the upswing in March and April is expected to have continued since then. Data last week showed a rise in stocks at manufacturers in April and further gains are likely after a surge in automobile sales in May depleted stocks of some vehicle models.

Retails sales rose 0.3% in May, although less than expected, after rising 0.5% in April. Retail sales are up 4.3% over year ago levels. Non-store sales, which include sales made by online retailers like Amazon, were quite strong in May, growing 7.4%. Auto and motor vehicle dealer sales were a key driver for the retail sector, increasing by 11.1% over last year to $88.8 billion.

Retail sales are key to the consumption component of GDP. In 2013, US retail sales were estimated at $4.5 trillion (excluding food services sales) or 27% of GDP. Therefore, shifts in retail spending are key drivers for economic growth.

The Job Openings & Labor Turnover Survey (JOLTS) for April was issued by the Bureau of Labor Statistics on June 10. Job openings in the economy were reported at 4.45 million in April – up from 4.16 million in March. This was also the highest reported level for the number of job openings since September, 2007 before the recession began.

The private sector accounted for most of the increase in job openings, with gains in almost all sectors, with the exception of construction, education and health services. Job openings in consumer sectors like retail trade, accommodation and food services showed strong gains, along with manufacturing and professional and business services.

In summary, while the Commerce Department is expected to revise 1Q GDP down to near minus 2% tomorrow, most forecasters believe that the first estimate of 2Q GDP in late July will rise by at least 3% (annual rate).

I should also note that the Fed reduced its growth estimate for all of 2014 from 2.8-3.0% predicted in March to only 2.1-2.3% now. This forecast and others were released after last week’s Fed Open Market Committee (FOMC) meeting. For more complete details and analysis of last week’s Fed meeting and its latest economic forecasts, read my BLOG from last Thursday.

Texas Immigration Crisis: UPDATE (They Knew)

This is potentially huge! All the way back in January of this year, the US Immigration and Custom Enforcement (ICE) agency posted a government request for “escort services for unaccompanied alien children” coming across our borders. The request specifically stated that ICE was preparing for 65,000undocumented children.

The application, dated January 29, is posted on Federal Business Opportunities, a website that advertises government contract openings. Here is information from the application:

“U.S. Immigration and Customs Enforcement (ICE), a component of the Department of Homeland Security (DHS), has a continuing and mission critical responsibility for accepting custody of Unaccompanied Alien Children [UAC] from US Border Patrol and other Federal agencies, and transporting these juveniles to Office of Refugee Resettlement (ORR) shelters located throughout the continental United States.”

“ICE is seeking the services of a responsible vendor that shares the philosophy of treating all UAC with dignity and respect, while adhering to standard operating procedures and policies that allow for an effective, efficient, and incident free transport.”

“Transport will be required for either category of [Unaccompanied Minors] or individual juveniles, to include both male and female juveniles. There will be approximately 65,000 UAC in total: 25 percent local ground transport, 25 percent via ICE charter and 50 percent via commercial air.”

“Escort services include, but are not limited to, assisting with: transferring physical custody of UAC from DHS to Health and Human Services (HHS) care via ground or air methods of transportation (charter or commercial carrier).”

A spokeswoman for ICE, Barbara Gonzalez, confirmed the posting was authentic, but couldn’t provide additional information in response to questions from TheBlaze, one of the first news outlets to break the story.

The implication is obvious: As many suspected, somebody in the Obama administration had advance knowledge that tens of thousands of undocumented children would be flooding the border, illegally, and would require transportation to secure facilities.

The question is, how far does this news go? I first heard this story this morning on a local AM radio show. I then searched the Internet and found the story, including the quotes above on several conservative websites.

Sadly, it remains to be seen whether the mainstream media jumps on this or not. So far, FOX and the Washington Times are the only big media outlets to report it. If this story is true, and it certainly seems to be, it could be the biggest Obama scandal so far!

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.