IN THIS ISSUE:

1. Consumer Confidence Highest Since Late 2007

2. Jobs Numbers Hit Milestone, Deep Problems Continue

3. Teen Unemployment Rate Tops 50% in Some Cities

4. A Third of 18-34 Year-olds Now Live With Their Parents

5. Household Formation in America Continues to Plunge

6. Over Half of Americans Can’t Afford Their Homes

7. Conclusions – Where Do We Go From Here?

Overview

As is true more often than not, there are mixed signals in the economy. There are indeed some “green shoots” emerging that suggest the economy is finally gaining some momentum. Yet there are also continued troubling signs that, while not warning of an impending recession, suggest that we could be stuck in a structural period of continued below-trend growth.

Today, we'll look into the latest economic indicators – good, bad and in between – and see if we can make any sense of where we are. My view is that the economy is most likely to remain in sub-par growth (ie - below 3%) for at least the rest of this year and maybe longer. Yet as we’ll see below, some others feel that the economy is nearing “breakout velocity.” We’ll see, but I am not so optimistic. Let’s hope I’m wrong.

A new report finds that President Obama’s economy is the worst in over 80 years. You can read this story at the first link in SPECIAL ARTICLES below.

Let’s start with the latest good economic news.

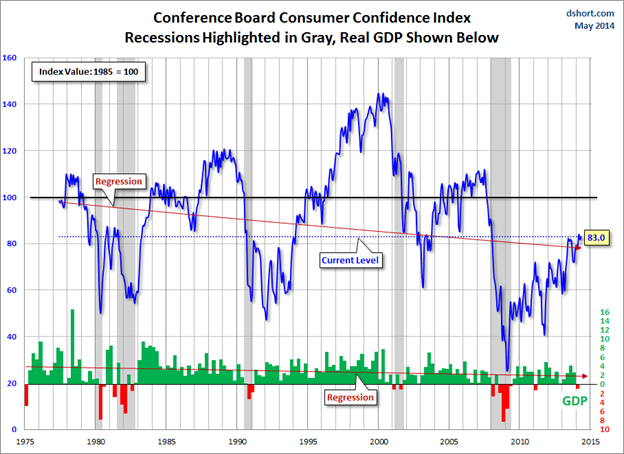

Consumer Confidence Highest Since Late 2007

The Consumer Confidence Index rose to 83.0 in May, according to the Conference Board Survey. That’s the highest level since December of 2007. The Conference Board said the percentage of consumers expecting their incomes to grow over the next six months was also the highest since December 2007.

Rasmussen tracks a daily Investor Confidence Index which has been rising steadily over the last three months and stood at 126.6 as of last Sunday. And why not? Stocks are at all-time record highs and bonds have risen higher than just about anyone expected this year.

Orders for durable goods have been considerably stronger than expected over the past two months. The ISM manufacturing index rose to 55.4 in May, its highest reading this year, and confirmed the 12th consecutive month of expansion. Of the 18 manufacturing industries tracked by the ISM, 17 reported growth in May with one reporting no change for the month.

On the housing front, April numbers were better than expected and beat their March readings in new and existing home sales and in housing starts and new building permits. The median sales price for new homes climbed to a new high of $275,800 in April, according to the Census Bureau.

And now let’s shift to some of the not-so-good news.

Jobs Numbers Hit Milestone, But Deep Problems Continue

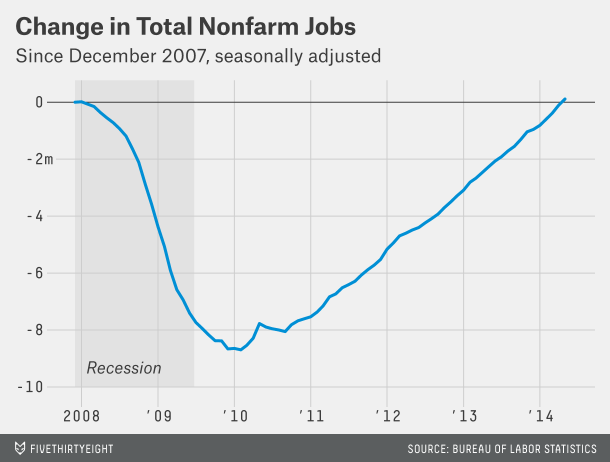

Six-and-a-half years after the Great Recession began – and five years after it officially ended – the US has finally surpassed its pre-crisis employment peak. But the job market is far from fully healed as I will discuss below.

Jobs numbers released by The Bureau of Labor Statistics (BLS) on Friday were better than economists were predicting. Non-farm payrolls went up by 217,000 jobs in May, slightly above the 215,000 that economists were expecting. The unemployment rate, which is drawn from a different survey of households, remained unchanged at 6.3% and was 0.1% better than the 6.4% pre-report consensus.

This was the fourth consecutive month that non-farm payrolls increased more than 200,000. It was the first time that we have seen four consecutive months of 200,000 or more new jobs since October of 1999.

The labor force participation rate remained unchanged from the dismal 62.8% rate reported for April, the lowest rate in decades. The BLS said Friday that the participation rate has shown no clear trend since last October but is down by 0.6% over the past 12 months.

The number of long-term unemployed – defined as those who have been jobless for 27 weeks or more – was essentially unchanged at 3.4 million in May, accounting for 34.6% of the country’s unemployed population.

The BLS also reported that 7.3 million people were working part-time because their hours had been cut back or because they were unable to find a full-time job. This brings the total unemployed and under-employed rate to 12.2%, down from 13.4% in May 2013. In May, average hourly earnings rose 5 cents to $24.38. Over the past twelve months, average hourly earnings have risen only 2.1%.

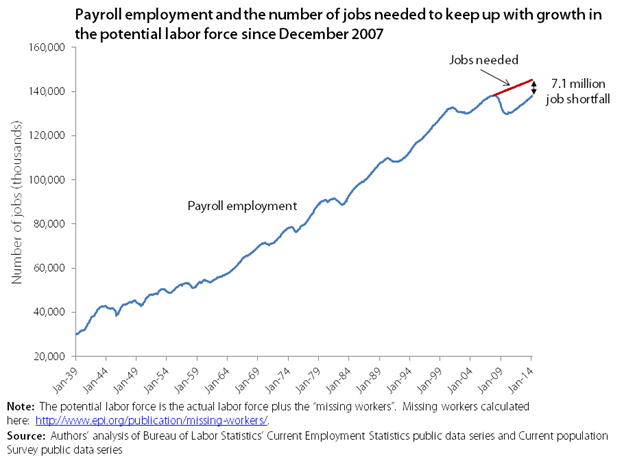

Here’s the milestone I noted above. With the 217,000 jobs added in May, we have finally recovered the almost nine million jobs that were lost during and just after the Great Recession. But getting back to square-one isn’t much to celebrate. There are over 6 million more working-age Americans today than when the recession began.

Adjusting for population growth, we’re still over 7 million jobs short of where we were 6½ years ago. So, we are still far, far from healthy labor market conditions.

And now let’s turn to some downright ugly reports.

Teen Unemployment Rate Tops 50% in Some Cities

The issue of teen unemployment is a complex one that has grown worse over the years. Teens aged 16-19 without high school diplomas have been hit especially hard by the Great Recession. The Census Bureau reports that as of the end of April, teen unemployment in this age group soared to 54.2% in the Riverside-San Bernardino area in Southern California.

The same Census report says that teen unemployment in the Portland-Vancouver-Beaverton, Oregon metro area was at 53.8% at the end of April. Teens around the country are missing out on valuable work experience this summer as they continue to suffer through an extended period of high unemployment and difficult job prospects.

The national average unemployment rate for this age group and skill level is 21.6%, but the high jobless rate for the least skilled young people is not limited to the West Coast. Here are the other eight cities that round-out the Census Bureau’s Top 10 worst cities for teen unemployment:

Los Angeles-Long Beach-Santa Ana, CA (39%)

San Diego-Carlsbad-San Marcos, CA (37.5%)

San Francisco-Oakland-Fremont, CA (35.2%)

Philadelphia-Camden-Wilmington, PA-NJ-DE (33.2%)

Chicago-Naperville-Joliet, IN-IN-WI (33%)

Pittsburgh, PA (32.9%)

Sacramento-Arden-Arcade Roseville, CA (32.1%)

Baltimore-Towson, MD (31.4%)

A Third of 18-34 Year-olds Now Live With Their Parents

Increasing numbers of young Americans are heading to college because they can’t get a job, and they’re racking up big debt to pay for rapidly increasing tuition costs. Even those graduating from college often confront a challenging job market, which eventually leads many to just drop out of the labor force altogether.

This in turn has led to an increasing delinquency rate for student loan borrowers. So it's no surprise that young people are increasingly opting, in many cases out of necessity, to live at home with their parents.

In his latest monthly chart book, Deutsche Bank’s Torsten Slok tracks the rise of 18- to 34-year-olds currently in this position. And there are a lot. Slok points to the latest Census Bureau data showing that over 31% of this broad age group now live with their parents. This does not include those who live with their grandparent(s) or other relatives.

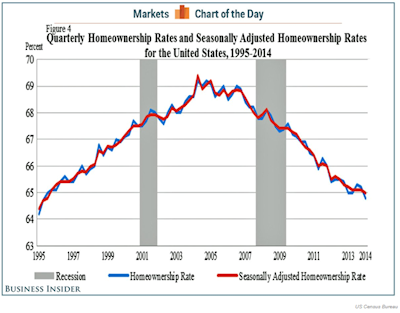

Slok sees this as a bullish force to come in the housing market in the years ahead, because the homeownership rate is at a 19-year low in the US. While sales are up recently, ownership rates are actually down as more concerned Americans are opting to rent rather than buy.

According to new Census data, the homeownership rate slipped to 64.8% in the 1Q, down from 65.0% a year ago and 65.2% in the previous quarter. This is the lowest level since 3Q 1995.

According to new Census data, the homeownership rate slipped to 64.8% in the 1Q, down from 65.0% a year ago and 65.2% in the previous quarter. This is the lowest level since 3Q 1995.

Some argue that this long-term trend will reverse soon, and it may. However, tight mortgage credit, especially for first time homebuyers, may contribute to a continued downtrend in the homeownership rate in coming years. A disproportionate share of new household formations are going into rentals and multi-family housing.

Household Formation in America Continues to Plunge

When a person establishes a residence, whether that’s an apartment or a house or another dwelling, that person is forming a “household.” Over the five years during and after the 2007–09 recession, the number of households established in America plummeted by about 800,000 a year from the previous seven years.

From 2007 through 2011, an average of roughly only 550,000 households formed each year in America, according to the Census Bureau. This number was the lowest level since records started being kept after World War II, and was 59% below the annual average of 1.35 million household formations from 2000 to 2006.

Mainly because of a weak labor market that held down incomes, the rate of household formation cratered during the recession and subsequent recovery. The decline in household formations is the main reason why the housing industry did not play its traditional role of driving the economic recovery.

After previous recessions, residential investment typically accounted for 1-2 extra percentage points added to annual GDP. By contrast, during the first two years of the current recovery, residential investment made no contribution to GDP growth.

The household formation crash also indirectly contributed to other woes, including falling house prices, diminished household wealth tied to lower home values and weaker demand for expensive goods such as autos, appliances, home furnishings, etc.

Most economists agree that the plunge in household formation since 2012 means that there is a flood of pent-up demand out there. Along with population growth, a healthier employment situation should push household formations up to about 1.5 to 1.6 million a year over the next several years. But that remains to be seen.

Over Half of Americans Can’t Afford Their Homes

Over half of Americans (52%) have had to make at least one major sacrifice in order to cover their rent or mortgage over the last three years, according to the recent “How Housing Matters Survey” conducted by Hart Research Associates.

These sacrifices include getting a second job, deferring saving for retirement, cutting back on healthcare, running up credit card debt, or even moving to a less safe neighborhood or one with worse schools.

What’s more, at least 15% of American homeowners are living in housing markets where the monthly mortgage payment on a median-priced home requires more than 30% of the monthly median household income. That threshold has long been considered the maximum for rent/mortgage repayments. Housing costs above that threshold are unaffordable by historic standards.

Although mortgage rates are still quite low, down payments, poor credit and tighter lending standards remain three of the biggest hurdles for buying a home, especially among young people. The slow jobs recovery for young adults has made it harder for them to save and to get approved for a mortgage.

Some people also appear to be cooling on one major facet of the American dream: home ownership. About 43% of respondents in the How Housing Matters Survey say owning a home is no longer “an excellent long-term investment and one of the best ways for people to build wealth and assets.”

Over half of those surveyed said buying a home has become less appealing. Although 70% of renters still say they aspire to own a home, some 58% believe that “renters can be just as successful as owners at achieving the American dream.”

In the years after the recession of 2008, more than 7.5 million homeowners lost their homes to foreclosure or short sales, and about 9 million more homeowners are still underwater and owe more than their property is worth. If one looks at the last seven years as a predictor of housing market behavior in the future, it certainly should give one pause about whether buying a home is a good investment or not.

The good news is that rising home prices over the last couple of years have lifted millions of homeowners out of negative equity. Since the lowest point in the housing market crash, rising prices have led to an additional $4 trillion in housing equity.

Home prices, including distressed sales, increased 10.5% in April 2014 year-over-year, according to the latest survey from mortgage-data firm CoreLogic, representing the 26th consecutive month of annual increases in home prices.

Conclusions – Where Do We Go From Here?

As we have seen above, there are mixed signals in the economy. There are indeed some “green shoots” emerging that suggest the economy is finally gaining some momentum. Yet there are also continued troubling signs that, while not warning of an impending recession, suggest we could be stuck in a structural period of continued below-trend growth.

I believe that the most likely path is one of continued slow growth in the US economy for at least another year or more. Like me, most forecasters have pared their estimates of 2014 GDP growth to something below 3%, with many now converging on a 2% trajectory for this year, well below their estimates at the end of 2013.

The fact that 1Q GDP came in so far below expectations at -1% cannot be ignored. The third and final government estimate of 1Q GDP growth will be out on June 25. We’ll have to see what that report has to say, but it will be very surprising if that number is revised up significantly.

In the meantime, we’ll have to wait until late July to see what the first estimate of 2Q growth will be. That report will be quite interesting in that most forecasters expect it to show 2Q growth of at least 3%. I’m not so confident, but we’ll see.

Onerous New EPA Regulations Will Hurt the Economy

In case you missed it, the EPA issued some sweeping new regulations last week that require coal-burning power plants to cut carbon dioxide emissions by 30%. If these new regs stand, it will almost certainly mean that many of these older power plants will be shuttered in the years ahead. If so, electricity prices could skyrocket.

The mainstream media did its very best to cover-up this news, but you need to know about it. Read my BLOG from last Thursday to get the details.

As always, I welcome your comments and suggestions.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.