I recently returned from my annual tour of our offices in the Asia-Pacific region. Two weeks, eight cities, 54 hours in flight and one suitcase. When I got home, my clothes burst out of the bag and marched into the washing machine on their own.

The schedule sounds grueling, but the quality of the conversations kept my energy at a very high level throughout. It’s always good to get a close-up of key markets to complement the wide-angle view one gets from a distance. Following are some impressions and themes that emerged from the dozens of meetings that took place during the journey.

The last item was the subject of the most angst: Australia faces mounting bills for its aging population, and it needs to address them now while they are still manageable. Encouraging people to work longer, indexing benefits to need, and promoting saving were among the planks in the platform. Kudos to Treasurer Joe Hockey for daring to tackle this challenge publicly; we could use some of that kind of initiative here in the United States.

The compensation for all of the travel time was some really good food. Barramundi with a view of the Sydney opera house; seafood stew looking out over Hong Kong harbor; lamb with cumin in Beijing; whole fish with red curry in Kuala Lumpur; and Christine’s salad with oranges, walnuts and pomegranate seeds in Balnarring were among the many highlights. I send thanks to my gracious hosts for sharing their ideas, their company and their cuisine.

My body clock is still centered somewhere between China and Chicago, so I’ve been a little slow at times this week. My partners say that they hardly notice the difference from my normal level of engagement. I’m not sure whether they’re being supportive or snide, but I am looking forward to a little rest this weekend.

EU Elections: Ripple or Sea Change?

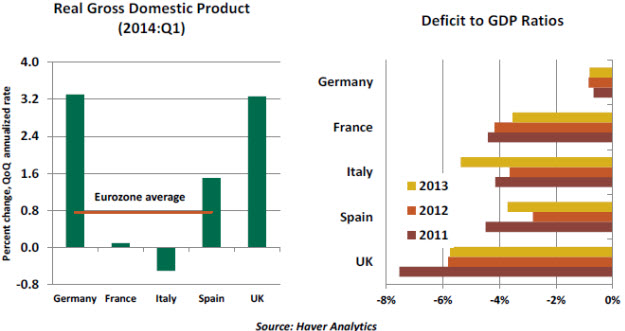

Last weekend’s European Parliament (EP) election generated reams of headlines about a “political earthquake,” yet virtually no market reaction. It’s possible that investors noted that the more-moderate blocs will continue to dominate the legislature. But it’s probable that, like most of the voters, they still don’t see the EP as having much real power. Although little may seem to change in the near term, the surge in support for right-wing populist parties will have an impact on various national political scenes and negative longer term economic and policy consequences at the EU level.

Another grand coalition of moderate center-left and center-right parties will dominate the next parliament. However, the final tally across all 28 countries saw aggregate support for euro-sceptic parties roughly double to about 20%, giving these parties 141 of the 751 seats. The combination of low turnout (43%) and a proportional representation voting system helped boost support for the extremists. Voters are also much more inclined to support fringe parties in an election that they see as less important to their daily lives.

It was in countries such as France and the Netherlands – where the impact of the 2008-09 recession still bites – that voters used the EP elections to vent their frustration. Economic performance across Europe remains very uneven, and very tough fiscal choices lie ahead.

At the national level, the big winner was Italian Prime Minister Matteo Renzi. His Democratic Party won a resounding 41% of that country’s EP vote, compared with just 21% for the left-populist Five-Star Movement. After only a few months in office, Renzi effectively has a renewed mandate to keep pushing for economic and political reform.

The biggest “loser” was French President François Hollande. Already plummeting in national opinion polls, his party was pushed into third place while support for the far-right Front National (FN) surged to 25%. The FN has only two deputies in the national parliament, but its showing in the European vote will further undermine an already-weak administration and make it harder to gather support for his government’s tentative reform program.

By contrast, Chancellor Angela Merkel’s conservatives claimed first place in Germany’s EP vote, while the euro-sceptic AfD won just 7%. Already at odds on a number of fronts, the EP election has further driven a wedge between Germany and France, the Union’s two pillars..

None of the euro-sceptics elected to the EP last weekend will have any direct say in their respective national parliaments. But claiming seats at the EP gives euro-sceptic parties access to more funding and raises their profile at the national level. The results will also shift the national political discourse to the right in countries such as France, Netherlands, Denmark and the United Kingdom, where we can expect to see renewed debates about immigration and welfare policies.

So what does all this mean for the EU? For the next few months, policy-making will slow even more than is usual after a parliamentary vote. The new European Commission (the EU’s executive arm) must be appointed, along with a new Commission president. The EP is already showing signs of pushing back against the practice of positions being filled through back-room horse-trading among national governments. This could lead to a prolonged stalemate over appointments, which will hardly endear the European politicians to the voters.

To function as a true Union and unleash their full competitive potential, the 28 countries need a more unified approach to policy-making that tackles the rigid labor and product markets still plaguing some members and begins to reduce chronic high unemployment. The results of this election will likely have the opposite effect. Although elected to a European parliament, the various representatives are beholden to national electorates and national party organizations. A lot of them will now be even more leery of advocating anything that voters back home will see as “more Europe.” They will certainly be in no hurry to propose changes that would need ratification by national parliaments.

All of which suggests that any new reform proposals will be delayed until at least the end of this year; that moves toward increased fiscal integration will slow even further; and that completion of banking sector reforms could be delayed. Ultimately, it means that the European Central Bank will continue to be the only European institution capable of undertaking meaningful actions.

The EU did not fall apart in 2009-11, and it will not as a result of these elections. But it will continue to muddle through with ad-hoc responses to crises. Meaningful policy change will continue to occur mostly at the national level – which means some countries (Germany, Netherlands, Sweden, the United Kingdom) will continue to have more competitive economies while others may be left behind.

The schedule sounds grueling, but the quality of the conversations kept my energy at a very high level throughout. It’s always good to get a close-up of key markets to complement the wide-angle view one gets from a distance. Following are some impressions and themes that emerged from the dozens of meetings that took place during the journey.

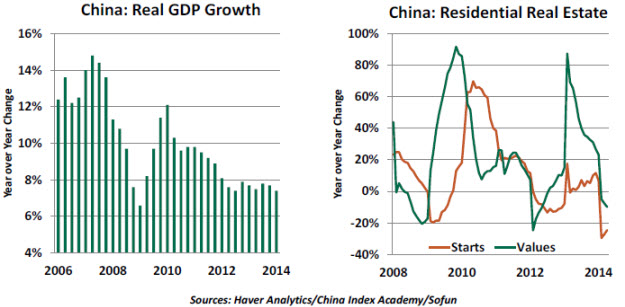

- The biggest question I took to Asia was whether China was headed for a hard landing. Those concerns were echoed loudly by clients in New Zealand and Australia. But as I got closer to the Chinese border, there was considerably more confidence that the challenges facing Beijing are manageable.

Australia and New Zealand have felt the impact of China’s slowing manufacturing sector, and those I spoke with in those countries asked tough questions about the country’s financial stability. To most Asians, however, the downshift in Chinese economic growth seems quite normal. They noted that recent readings on Chinese activity seem to be stabilizing, and they contended that the transition to a more sustainable level and composition of growth is being carefully choreographed.

Chinese real estate construction clearly has slowed,, and Chinese real estate prices are declining in some areas. Officials there are very much aware of this situation and understand how it might progress. (They are students of the U.S. experience of a decade ago.) They have immense reserves that could be used to fill any cracks that might emerge in their financial system.

I was reminded that China has dealt with a series of developing pains successfully over the past three decades and that policy-setting is not hindered by the messiness of multi-party politics. The current economic strategy combines selective short-term stimulus with long-term reform.

I left somewhat reassured but still wary. I remember analysts in the United States (including me) calming foreign observers in the midst of our housing boom, suggesting that the challenge was both well-understood by American policy-makers and manageable in scale. Those proved to be famous last words.

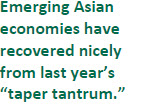

- The trip coincided with the one-year anniversary of Ben Bernanke’s hint that the Federal Reserve might begin tapering its asset purchases. That statement triggered very sharp market reactions that were particularly acute for some emerging markets.

After several months of malaise, equity markets in emerging Asia have recovered somewhat. Capital flows have resumed, and economic prospects seem solid.

Emerging Asian economies have held the lessons of their 1997-98 crisis closely, and the discipline borne of that experience has encouraged investors. This stands in contrast to some emerging markets elsewhere in the world that seem to make the same errors repeatedly.

- Tensions in Southeast Asia have escalated. Vietnam and China are in conflict over an oil-drilling rig that is anchored in disputed waters; a coup d’état placed the military in control of Thailand; and the sparring between Japan and China shows no sign of abating. I would agree with those who see Asia as a tremendously exciting place for economic development. But regional conflict there has deep historical roots and tends to resurface periodically. Investors will have to roll with those punches.

Within countries, the politics of inequality are thick. Developing countries progress unevenly at first (and sometimes for a long while afterward), and the resulting extremes of fortune can destabilize governments. Support for the market mechanism is often a casualty of regime change.

- Everywhere I went, there were complaints about housing. Foreign buyers, bearing cash, have been snapping up property at high prices. This has raised concerns over the stability of values and the accessibility of the market to native first-time homebuyers.

To curb the enthusiasm, policy-makers in a number of countries have been raising down-payment requirements and tightening lending standards. But these measures matter little to cash buyers. More recently, Singapore and Hong Kong (among others) have increased taxes on the most-expensive properties.

Nonetheless, investors continue to flock in. To many of them, purchasing property in foreign capitals diversifies their portfolios across asset classes and currencies. It also serves as a hedge against a significant financial correction or harsher regulation at home.

This situation should serve as a cautionary tale for those who would like to apply macro-prudential tools to control financial excess. Cooling overheated markets is a very difficult thing to do.

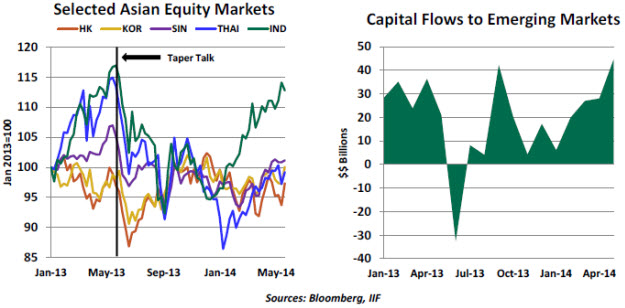

- Australia should be the economic envy of the developed world: no recessions in 22 years; AAA-rated credit; a diverse industrial base; normal levels of interest rates; and very modest levels of national debt. And yet when the Treasurer announced the annual budget earlier this month, he made it seem like the country was on the road to ruin.

The last item was the subject of the most angst: Australia faces mounting bills for its aging population, and it needs to address them now while they are still manageable. Encouraging people to work longer, indexing benefits to need, and promoting saving were among the planks in the platform. Kudos to Treasurer Joe Hockey for daring to tackle this challenge publicly; we could use some of that kind of initiative here in the United States.

The compensation for all of the travel time was some really good food. Barramundi with a view of the Sydney opera house; seafood stew looking out over Hong Kong harbor; lamb with cumin in Beijing; whole fish with red curry in Kuala Lumpur; and Christine’s salad with oranges, walnuts and pomegranate seeds in Balnarring were among the many highlights. I send thanks to my gracious hosts for sharing their ideas, their company and their cuisine.

My body clock is still centered somewhere between China and Chicago, so I’ve been a little slow at times this week. My partners say that they hardly notice the difference from my normal level of engagement. I’m not sure whether they’re being supportive or snide, but I am looking forward to a little rest this weekend.

EU Elections: Ripple or Sea Change?

Last weekend’s European Parliament (EP) election generated reams of headlines about a “political earthquake,” yet virtually no market reaction. It’s possible that investors noted that the more-moderate blocs will continue to dominate the legislature. But it’s probable that, like most of the voters, they still don’t see the EP as having much real power. Although little may seem to change in the near term, the surge in support for right-wing populist parties will have an impact on various national political scenes and negative longer term economic and policy consequences at the EU level.

Another grand coalition of moderate center-left and center-right parties will dominate the next parliament. However, the final tally across all 28 countries saw aggregate support for euro-sceptic parties roughly double to about 20%, giving these parties 141 of the 751 seats. The combination of low turnout (43%) and a proportional representation voting system helped boost support for the extremists. Voters are also much more inclined to support fringe parties in an election that they see as less important to their daily lives.

It was in countries such as France and the Netherlands – where the impact of the 2008-09 recession still bites – that voters used the EP elections to vent their frustration. Economic performance across Europe remains very uneven, and very tough fiscal choices lie ahead.

At the national level, the big winner was Italian Prime Minister Matteo Renzi. His Democratic Party won a resounding 41% of that country’s EP vote, compared with just 21% for the left-populist Five-Star Movement. After only a few months in office, Renzi effectively has a renewed mandate to keep pushing for economic and political reform.

The biggest “loser” was French President François Hollande. Already plummeting in national opinion polls, his party was pushed into third place while support for the far-right Front National (FN) surged to 25%. The FN has only two deputies in the national parliament, but its showing in the European vote will further undermine an already-weak administration and make it harder to gather support for his government’s tentative reform program.

By contrast, Chancellor Angela Merkel’s conservatives claimed first place in Germany’s EP vote, while the euro-sceptic AfD won just 7%. Already at odds on a number of fronts, the EP election has further driven a wedge between Germany and France, the Union’s two pillars..

None of the euro-sceptics elected to the EP last weekend will have any direct say in their respective national parliaments. But claiming seats at the EP gives euro-sceptic parties access to more funding and raises their profile at the national level. The results will also shift the national political discourse to the right in countries such as France, Netherlands, Denmark and the United Kingdom, where we can expect to see renewed debates about immigration and welfare policies.

So what does all this mean for the EU? For the next few months, policy-making will slow even more than is usual after a parliamentary vote. The new European Commission (the EU’s executive arm) must be appointed, along with a new Commission president. The EP is already showing signs of pushing back against the practice of positions being filled through back-room horse-trading among national governments. This could lead to a prolonged stalemate over appointments, which will hardly endear the European politicians to the voters.

To function as a true Union and unleash their full competitive potential, the 28 countries need a more unified approach to policy-making that tackles the rigid labor and product markets still plaguing some members and begins to reduce chronic high unemployment. The results of this election will likely have the opposite effect. Although elected to a European parliament, the various representatives are beholden to national electorates and national party organizations. A lot of them will now be even more leery of advocating anything that voters back home will see as “more Europe.” They will certainly be in no hurry to propose changes that would need ratification by national parliaments.

All of which suggests that any new reform proposals will be delayed until at least the end of this year; that moves toward increased fiscal integration will slow even further; and that completion of banking sector reforms could be delayed. Ultimately, it means that the European Central Bank will continue to be the only European institution capable of undertaking meaningful actions.

The EU did not fall apart in 2009-11, and it will not as a result of these elections. But it will continue to muddle through with ad-hoc responses to crises. Meaningful policy change will continue to occur mostly at the national level – which means some countries (Germany, Netherlands, Sweden, the United Kingdom) will continue to have more competitive economies while others may be left behind.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.