As I wrote in my latest Forbes article and in my current weekly column On My Radar, most investors are unaware and ill-prepared for the impact that rising interest rates will have on their bond funds and ETF investments. There has been an unprecedented period of Fed participation (manipulation) with six years of near zero-percent interest rate policy and trillions of newly created currency.

The Federal Reserve is waging a battle against deflation. Deflation can lead to depression. The Fed’s objective is to create inflation. Our risk is that they do not succeed. Unfortunately, our risk is also that they do succeed.

In inflationary periods, interest rates rise. Since the Fed sets short-term rates, let’s take a look at where the Federal Open Market Committee members believe interest rates are heading. Currently, 13 of the 16 FOMC participants believe the Fed will begin to raise rates in 2015. One sees rates beginning to rise in 2014 and the remaining two see rates rising in 2016. Their median year-end Fed funds rate target for 2015 is now 1.00%, up from 0.75% just three months ago. The year-end target for 2016 is now 2.25%, up from 1.75%.

All of this suggests that the FOMC will begin hiking rates sooner and perhaps more aggressively than what investors may be expecting. Also of note is that the FOMC participants see a 4% federal funds rate longer term. Rising rates spell trouble for unsuspecting bond investors.

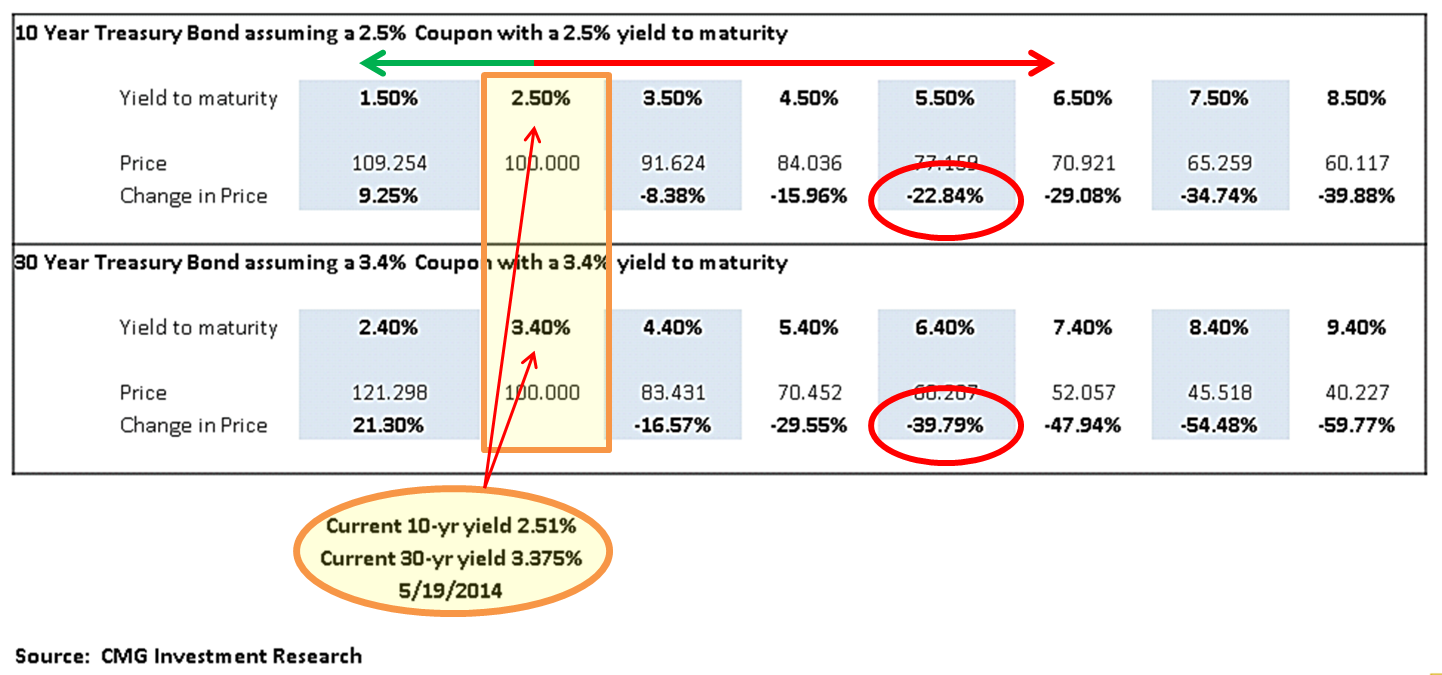

What is the potential impact? Recently, the yield on the 10-year Treasury note was 2.50%. That is 2.50% above the current Fed funds rate of 0%. If the Fed funds rate reaches 1% in 2015, then the 10-year Treasury is likely to yield 3.50%. Such a move higher will cause an approximate 8% loss in principal value; though rates could move even higher.

A 2016 Fed funds target of 2.25% puts the 10-year Treasury yield near 4.75% (an approximate loss of 18%) and a longer-term Fed funds target of 4% puts the 10-year Treasury yield near 6.50%, a loss in principal value of 29%. Further, if you own bond funds or ETFs with long-term exposure, the losses will be even greater. A behavioral disconnect exists as many individual investors are unaware they can lose money in their bond funds and ETFs.

The following chart shows the current yield on the 10-year and 30-year Treasury (orange highlight). The green arrow shows how much bonds will appreciate if rates move 1% lower. The red arrow shows the approximate loss for every 1% rise in interest rates. I’ve circled in red the potential loss should rates rise 3% above where they are today.

These are estimates, of course, yet the idea is to gain awareness of the large interest rate risk that may exist in your portfolio. While rates may continue to go lower before they go higher, most Wall Street analysts project the 10-year Treasury to yield north of 3% by year end. So far they are wrong yet at some point, with little room left on the downside, rates are likely to rise. It is important to protect your portfolio against the inevitable rise in interest rates while at the same time participating in bond returns when the trend for interest rates is down (such as year-to-date 2014).

What can you do? Tactically trade your bond funds and bond ETFs.

Years ago the late Marty Zweig created a tactical trend following bond model. We recently did some customized work and updated a model Marty co-created with Ned Davis Research in the mid 1980s. The rules have remained in place since then, the model has continued to perform well and it has been properly positioned in bonds this year. Of course, there are no guarantees in this business. This is a mathematical process you could track and trade on your own.

Here is how this particular tactical trend following process works:

- Score a +1 when the Dow Jones 20 Bond Price Index (index symbol $DJCBP) rises from a bottom price low by 0.6%. Score a -1 when the index falls from a peak price by 0.6%.

- Score a +1 when the Dow Jones 20 Bond Price Index rises from a bottom price by 1.8%. Score a -1 when the index falls from a peak price by 1.8%.

- Score a +1 when the Dow Jones 20 Bond Price Index crosses above its 50-day moving average by 1%. Score a -1 when the index crosses below its 50-day by 1%.

- Score a +1 when the Fed funds target rate drops by at least ½ point. Score a -1 when the rate rises by at least ½ point.

- Score a +1 when the yield difference of the Moody’s AAA Corporate Bond Yield minus the yield on 90-day Commercial Paper Yield crosses above 0.6. Score a -1 when the yield difference falls below -0.2. Score it 0 for a neutral score between -0.2 and 0.6.

- Add up the sum total of steps 1 through 5 once a week (the chart below reflects Friday’s close calculations). If the total sum is +1 or higher, invest in a total bond market ETF like NYSE: BND (the Vanguard Total Bond Market ETF) or NYSE: AGG (iShares Barclays Aggregate Bond Index ETF). If the aggregate score is -1 or lower, reduce your portfolio risk by shortening the maturity and buy NYSE:BIL (SPDR Lehman 1-3 Month T Bill ETF).

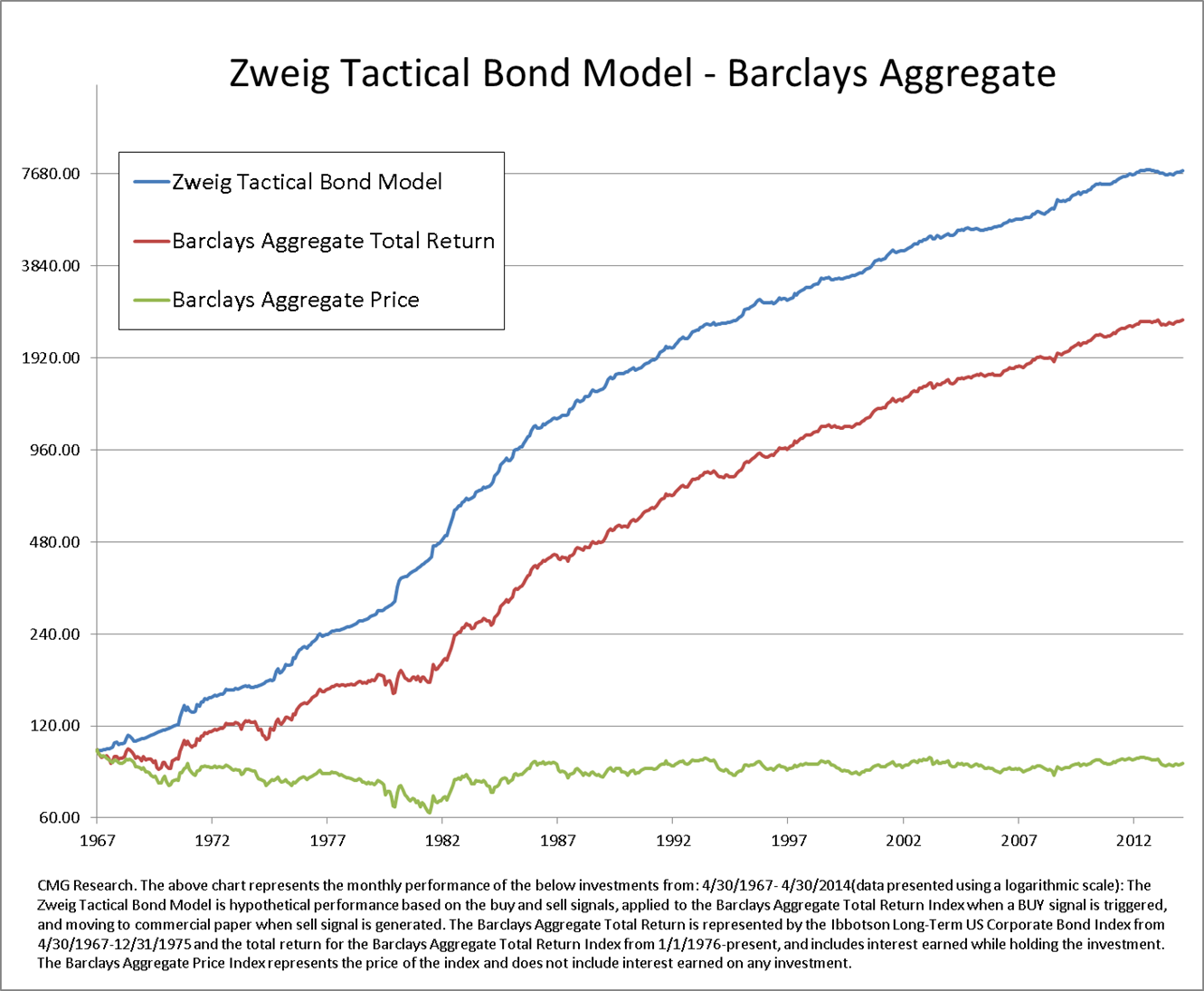

There are three lines reflected in the following chart. Each shows the growth of $100 from 1967 to present. The blue line reflects the Zweig Bond Model, the red line the Barclays Aggregate Total Return Index and the green line the Barclays Aggregate Price Index. When interest rates rise, bond prices fall. It is those dips in price, as reflected in the Barclays Aggregate Price Index (green line), the tactical strategy attempts to avoid.

Following the tactical signals of the Zweig Bond Model over this period would have returned approximately 9.71% vs. a buy-and-hold gain of 7.12%. The strategy did particularly well in the rising interest rate environments in the 1970s and early 1980s.

It has been a 30-year bull market for bonds. In order to be successful moving forward, investors need to be smarter and more flexible in their approach. It is the change in the interest rate trend we must consider as we view portfolio risk. The Fed and other central banks are doing all they can to create inflation and they are armed with considerable resolve. With interest rates near historical lows, it is inflation and rising rates that present considerable portfolio risk. It is time to tactically trade fixed income exposure. The bubble of all bubbles may just be in bonds.

Steve Blumenthal is CEO & portfolio manager at CMG Capital Management Group. He writes regularly for CMG’s Advisor Central. Click here for important disclosures.

© CMG Capital Management Group

© CMG Capital Management Group