We have a policy in the house that phones are not allowed at dinner. For at least the 15 minutes that it takes for the children to wolf down their food, we like to create opportunities for conversation.

One recent Sunday, our meal was interrupted by a ringing sound from just underneath the table. I shot a dirty glance at the kids, but they each raised both of their hands in innocence. Turns out it was my wife’s phone, and she answered it without hesitation. After her brief chat, I shot her a dirty look … which she returned with a dirtier look. Clearly, I had forgotten that she is exempt her from all house rules.

It’s difficult to set one policy that works well for all constituents. That is a challenge faced by the world’s central banks, with the Federal Reserve and the European Central Bank dealing with especially difficult variants of this challenge.

Most world economies have moved beyond the Global Financial Crisis of 2008. Some have recovered more powerfully than others, but only a few have failed to advance from their low points. Forecasts from both the International Monetary Fund and the Organization for Economic Cooperation and Development call for further gains in the years ahead.

But beneath this smooth surface run strong cross-currents. Progress has been distributed very unevenly, and gaps between those who have benefitted most and least are widening. This can be observed along several axes.

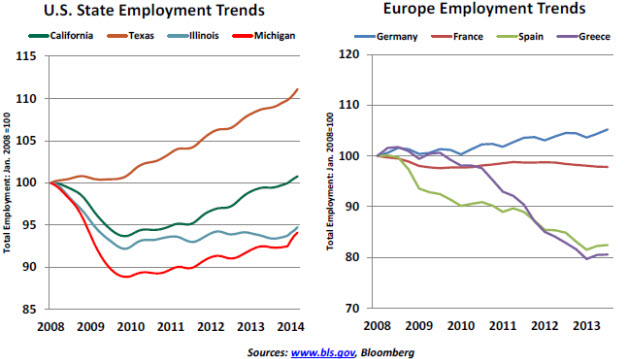

First, regional performance shows substantial variations. Much has been made of the disparity of outcomes within the Eurozone, but results from American states show similar divergence.

Both areas operate under a common monetary policy. But other policy sets can differ from place to place, affecting economic performance. Fiscal policy is a prime example; some locales have their finances well in hand, while others have been forced into austerity by current and future budget demands. The relative solvency of retirement and financial systems is often at the root of differences between states.

Those whose budgets are under stress often underinvest in education and employment programs. Poor schools can diminish the quality of a labor pool, making it more challenging for workers to find placement and risking an outmigration of companies and positions reliant on strong skill levels. This, in turn, can prompt an outmigration of the more capable employees, continuing a cycle that can hollow out an economy. We see signs of this in both America and Europe at the moment.

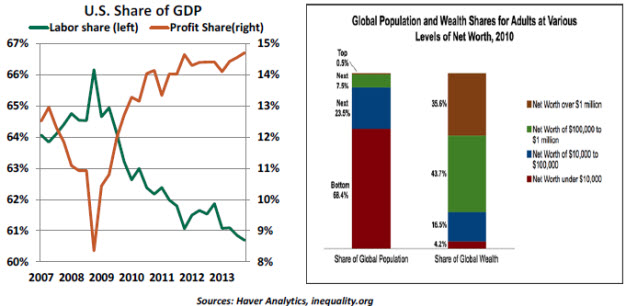

Accommodative monetary policy has certainly played a role in the significant gains seen in world equity markets, which have rallied to a series of record levels since bottoming in 2009. The Federal Reserve has made no secret of its desire to use asset valuation as a vehicle of stimulus; a portion of accumulated wealth translates to spending, which should ultimately prompt businesses to do more hiring.

But this translation has been very slow in coming. Those with significant equity holdings have become quite a bit wealthier, but those in the lower quintiles of the financial spectrum continue to struggle with lingering unemployment and slow wage growth. Rising inequality has garnered a lot of discussion in the United States, but it is very much a global phenomenon.

What these narratives illustrate is that in the process of trying to improve the aggregate, central bank policy can create and exacerbate asymmetries of local outcomes. These have been much more visible and problematic in the Eurozone, which has shared a monetary policy for less than 25 years and where internal differences matter greatly. But even in places where regional heterogeneity is not as apparent, unevenness of fortune among states or classes can polarize society and make for complicated politics.

Some suggest that these issues of distribution should come into the discussion of monetary policy. We disagree. The redress for this situation is outside the scope of central banking, and should be handled with sensible fiscal strategy. Because the latter has been found wanting over the past decade, pressure has increased on central banks to be all things to all people. This is an impossible task.

There is currently a modest degree of tension between governments and their central banks on this front, with EU Finance ministers and American legislators freely offering their prescriptions for monetary policy. Ms. Yellen and Mr. Draghi have politely parried this advice, subtly suggesting that legislatures focus on doing a better job of addressing their own challenges.

Granted, it is difficult to design policies that reverse inequality without upsetting some constituents. I am thinking of hiding my wife’s phone during Sunday dinner, but that could prompt a violent revolution. Best to keep the peace, for now.

Eurozone: Deflation and Debt Dynamics

Central bankers once focused exclusively on keeping inflation from getting too high. Today, they have the opposite problem. While much of the danger associated with a falling price level has centered on consumption (if goods are expected to cheaper tomorrow, they are not purchased today), the impact of disinflation on debt is also pernicious.

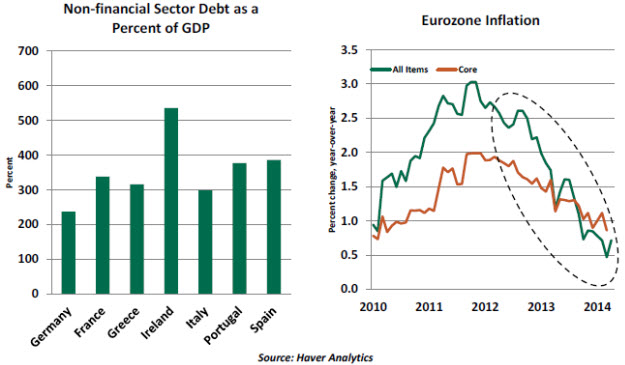

The Eurozone’s Harmonized Index of Consumer Prices shows a steady deceleration from a 1.1% year-to-year increase in April 2013 to a 0.7% gain in April 2014. These numbers indicate that the Eurozone is experiencing a disinflationary environment that could turn into deflation.

At any given time, prices of specific goods and services could be falling for a host of reasons. These sorts of price declines are not problematic and do not represent deflation. Deflation occurs when price declines are widespread to the extent that indexes such as the consumer price index capture the process and it becomes visible as a decline of the overall price index.

In a disinflationary/deflationary environment, debt service costs increase in real terms. The negative impact takes hold even before inflation readings turn negative. The process is set in motion when inflation is lower than the expected rate of inflation at the time debt was incurred. The current situation in the Eurozone echoes this description to a large extent. The impact of deflation on debt is best illustrated by an exaggerated example.

If someone borrows $100 at 3% interest for one year, he or she will return $103 at the end of the year. Assuming deflation is running at a 10% rate, the purchasing power of this amount will be roughly $114 ($103/0.9, to account for 10% deflation). As a result, in a deflationary situation, the debt burden of debtors will increase and they will cut back spending.

By contrast, in an inflationary situation, the borrower returns money that is worth less than the original amount borrowed. Assuming 10% inflation, $103 returned to the lender will be worth close to $94 ($103/1.1, to account for 10% inflation). Debt is repaid in dollars that are worth less than the original amount borrowed. The vicious impact of deflation is prevented if steady (but moderate) inflation prevails.

Also in a deflationary environment, as the real cost of borrowing becomes exorbitant, purchases of homes, business investment and other spending that entails borrowing will decline. The string of reductions in spending worsens the economic downswing. As debt service costs rise, the inability of debtors to service loans will translate into financial sector bankruptcies. Financial fragility inflicts additional harm on production and employment.

If deflation becomes entrenched in the Eurozone, the debt burden of the highly indebted public and private sector will increase and result in a significant reduction of spending. The adverse chain of events will tip the fragile economic recovery into a deep economic malaise once again.

Therefore, corrective policy actions are advised in a low inflationary environment as prevention is better than a cure. Mario Draghi’s indication that the European Central Bank “will be comfortable to act” at the June meeting is a step in the right direction to prevent a deflation in the Eurozone.

“Capital in 21st Century” – Policy Option and Critique

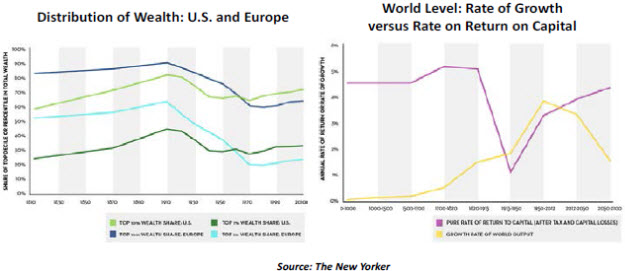

Last week’s discussion of Thomas Piketty’s book on capital ended with his conclusion that income equality has widened in several economies since the 1970s and if the rate of return on capital exceeds that growth rate of economy, it will persist in the future.

In Piketty’s world, capital and wealth are synonyms. Historical data reveal a notable concentration of wealth in advanced economies during the 19th century. War and economic depression reduced the concentration of wealth but a revival of these trends is visible in recent data.

His database indicates that the rate of return on capital generally exceeds the rate of economic growth, with the exception of a small period in the 20th century. If this is the norm, the current distribution of income and wealth implies that income and wealth of the affluent will grow faster than income from work and the current lopsided distribution of income is most likely to persist or become even more extreme.

This brings up the question: What justifies a higher rate of return on capital compared with the growth rate of the economy? It appears that Piketty assumes that capital is scarce, which results in the rate of growth of capital exceeding the growth rate of the economy. To Piketty’s credit, he notes that his prediction is one possible scenario; other more optimistic situations could materialize.

Piketty prepares for the worst and recommends a wealth tax that ranges from 0.1% to 10% combined with higher tax rates on high earners to break the skewed distribution of income. Intense debates about the proposal are underway, despite the fact that it would face immense legislative hurdles in most economies. By reducing returns to wealth, investment will diminish. This will impair job creation and productivity for a society.

Instead of taxing “capital” in the Piketty sense, progressive human capital policy to uplift people from the bottom is a more constructive proposal. Further, the flood of advances in technology and bioengineering could easily produce Schumpeterian type of “creative destruction” that has the potential of reducing the disparity between the rate of growth of capital and growth rate of the economy.

Piketty has elevated the income distribution debate to a new level, but his action plan is weak. While discussion of the topic is valuable, the hype he has generated likely exceeds his contribution to economic policy.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

(c) Northern Trust