- Is the U.S. economy under the weather?

- Japan is faltering a bit as year two of Abenomics begins

- Bitcoin has generated a lot of attention, some of it unwanted

We ushered in the new year on an optimistic note, on the back of a series of positive economic reports that suggested a bright 2014. Today, we find ourselves wondering if those high hopes have been buried under a mountain of snow.

The past two months provided a series of disappointing reports on sales, production and employment. There is little doubt that a good deal of the underage to expectations is due to the unusually poor conditions that have made winter 2014 one for the record books in many parts of the country. But the readings have prompted some to wonder whether the U.S. economy hit the wall late last year.

Our view is that we’re enduring a temporary setback that will end when temperatures return to normal. It is hard to think that the strong economic momentum seen in the second half of last year could dissipate so quickly.

Weather patterns affect many areas of economic activity. People and goods do not move as freely in the snow and the cold, curtailing everything from trips to the mall to shipments of raw materials. And construction slows as it becomes more difficult to move earth and work outside.

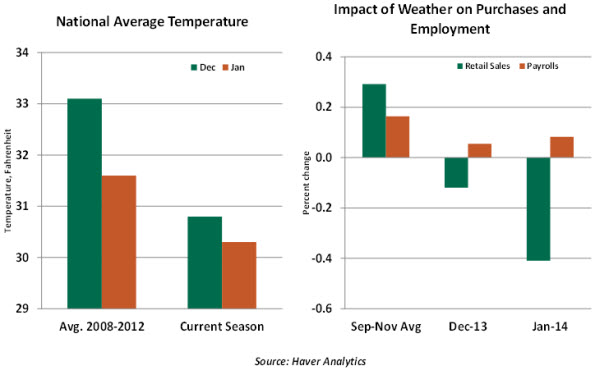

Most reported economic data is seasonally adjusted before publication. The adjustments remove the impact of holidays, normal climatic fluctuations and other sources of month-to-month variation (such as the spring selling season in housing). In general, seasonal adjustment techniques focus on a very short trailing history. As an example, retail sales are adjusted on a rolling basis, with the most-recent reference period beginning in 2008. Using this horizon, the deviation caused by the current cold spell relative to the last five years is clear to see.

There have been only six Decembers in the last 50 years that were colder than the one we just endured. Beyond the frigid temperatures, seasonal precipitation was well above average in many areas. (Can we export our excess snow to California?)

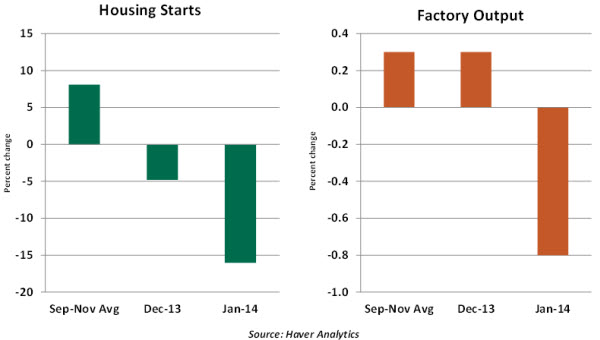

It is a challenge to separate the impact of adverse weather in economic data. A few series offer helpful background, such as the monthly tally of people not working because of weather. Unfortunately, this is the exception. On a broad basis, it is clear that the seasonally adjusted changes in retail sales, payrolls, housing starts and factory production numbers in December and January were much lower than the average change of the prior three-month stretch (September – November 2013).

From details of the retail sales report, weather-sensitive components such as apparel, restaurant meals and auto sales dropped sharply in December and January. Even online sales, which should not be affected by the weather, fell last month. Analysts think this might reflect consumer anticipation of large heating bills.

Hiring was soft in December and January, with overall payrolls coming in below the recent three-month average gain. Consistent with the retail sales numbers, hiring in the leisure and hospitality industry decelerated in December and January, while ground-breaking for new home construction posted a noticeable setback. Trucking tonnage fell sharply in January, and the subsequent delay in delivery of goods could have played a role in the 0.8% drop in January’s factory production.

Is there something more fundamental going on? Some cite January’s mild correction in the stock market, softer hiring conditions and rising mortgage rates as hindering consumption. And the very steep buildup in inventories during the third and fourth quarters last year may have led producers to slow things down a bit.

But this comes against the backdrop of a year’s worth of great equity gains, house price appreciation and job growth. Policy uncertainty is certainly not the problem it was for much of last year. Measures of consumer and business confidence do not yet reflect the negative tone seen in recent economic reports.

So to us, it seems premature to abandon the relatively constructive outlook with which we entered the year. First-quarter growth has been marked down, but there is great potential later in the year to make up some of the ground lost. The harsh conditions have thrown weather forecasters for a loop, but we’re not ready to discard our economic forecast.

Are Japan’s Arrows Pointed in the Right Direction?

Nearly 500 years ago, legend has it, a Japanese daimyo (territorial lord) promoted cooperation among his three sons by showing them that three arrows bound together were more difficult to snap than any single arrow.

Last year, new Japanese Prime Minister Shinzo Abe used this metaphor to promote three arrows of economic strategy: aggressive monetary ease, flexible fiscal policy and structural reform. The program aimed to pull the country out its deflationary spiral and put growth on firm footing.

As we approach the one-year anniversary of “Abenomics,” it is a good time to reflect on the past, take stock of progress and assess the future. Softer economic indicators in the second half of 2013 have raised concerns about the efficacy of the project and whether the three arrows can remain bound to one another.

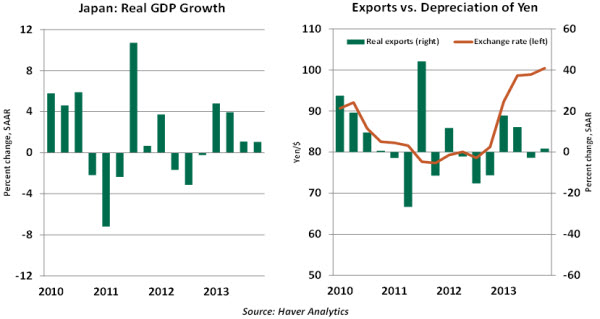

Japanese economic growth fell to an annual pace of a little more than 1% in the second half of last year, about a quarter of the rate seen in the first half. Weaker-than-expected exports and soft domestic demand are the main culprits.

On the trade front, Abe was depending on the weaker yen to make exports more competitive and imports more expensive. Instead, what occurred was a widening trade deficit, in spite of substantial currency devaluation. Export growth remained restrained as emerging market demand, particularly from China, softened. Conversely, imports surged as the weaker yen led to higher energy prices.

Domestically, Japan is far from realizing its “virtuous cycle” wherein strong corporate profits lead to an increase in employees’ wages and income, which then boosts consumption and fresh corporate investment. Instead, the country finds itself in more of a Catch-22. Corporate profits are up and companies are sitting on a lot of cash, but uncertainty about the sustainability of Abenomics has led to tentativeness around wage increases.

The outlook for Japanese consumers is, therefore, cloudy. The return of Japanese inflation to more-normal levels has diminished the real purchasing power of Japanese households. And the consumption tax increase to 8% from 5% that takes effect in April looms over the economy. While it is an important step toward fiscal consolidation and inspiring international confidence in the government’s policy, the hike also comes at an inopportune time.

Abenomics has proven that monetary stimulus can provide a short-term boost, but long-term stability is dependent on the third, or structural, arrow. Thus far, the government has been long on action items and short on concrete proposals. Agricultural reforms are tied up with the Trans Pacific Partnership (TPP) process and are unlikely to be finalized until negotiations are complete; there is opposition to TPP on both sides of the ocean that must be managed.

Meanwhile, efforts to increase potential growth by helping women in the workforce are running into cultural impediments. At 48%, Japan’s female labor participation rate is among the lowest in the developed world. But the full picture may be even worse: the nature of female participation follows a pronounced “M-curve” in which women leave the workforce during their most productive years, usually after marriage or child birth, and do not return until after their children are grown.

The structural arrow aims to remedy this by providing up to 400,000 daycare spots by 2017, increasing female representation among hired civil service workers to 30% by fiscal year 2015 and increasing the share of women in leadership positions to 30% by 2020. But overcoming the bias of women’s traditional roles in society will require more than just legislation.

Similarly, Japan is targeting immigration reform at skilled professionals and researchers to bolster research-and-development capabilities. But acceptance of outsiders has never been a strong suit.

Abenomics has provided its fair share of excitement and anticipation, and it has shown some tangible results. However, as Japan moves to lash the second and third arrows to the first, it may be limited by the ties that have bound that unique society for millennia.

Some Background on Bitcoin

During a long series of client events over the past month, discussions focused on some predictable topics. The struggles of certain emerging markets, the fiscal health of the United States and the Federal Reserve’s leadership transition headed the list.

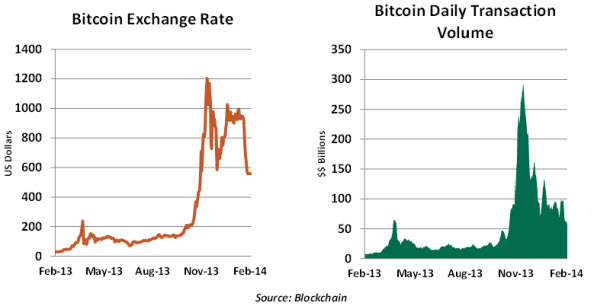

But another subject that generated a good deal of inquiry was (at least to me) a bit far afield. A surprising number of clients asked what I thought about bitcoin, the digital currency that has garnered considerable attention lately.

For those who have not been following the story, bitcoin is the brainchild of a mysterious programmer who created the currency in 2009. His aim was to offer a medium of exchange that was impervious to what he viewed as the reckless policies of traditional central banks. Bitcoins are gradually released via a computer network (to bitcoin “miners”), and they can be exchanged for a wide range of traditional currencies.

The advantage to the bitcoin is that its use circumvents toll-takers in the payments process, like credit card companies and banks. Once exchangeable only online, bitcoin is now accepted by an expanding number of traditional merchants. And bitcoins will soon be redeemable for traditional cash at ATMs in selected markets.

Technology has transformed the payments system in too many ways to count, most of them tremendously beneficial to consumers of financial services. But there are reasons to view bitcoin warily.

Because bitcoin transactions are “peer-to-peer” and anonymous, the virtual currency is perfect for illicit activity and money laundering. Recent fluctuations in the bitcoin’s value have been extreme, suggesting that it is not immune from speculation (or manipulation). The networks that create and store bitcoins have proven vulnerable to hacker attacks.

There is little oversight of the bitcoin market, which some observers see as a blessing and others see as a risk. Should there be more controls over the supply and application of this currency to safeguard its users and the financial system? Can a currency created out of thin air without a central bank behind it really command lasting respect as a store of value?

If bitcoin is to last, these questions must be answered satisfactorily. But bitcoin has already challenged our perception of what money is and how it can best be used to facilitate commerce. And that, in itself, has value.