Stocks for 2014: Fairly Valued Dividend Growth Stocks with an Emphasis on Dividends - Part 4

Introduction

Retired investors seeking high income to live off of during retirement, face greater challenges today than almost ever before. The days of high yields available from bonds and other fixed income vehicles are long gone. Consequently, generating an adequate level of current income on retirement portfolios is difficult to say the least. This is especially tricky for those investors with a low tolerance for risk.

Moreover, there’s no question that equity investments technically carry more risk than fixed income investments. This is widely acknowledged, and in the general sense, an unarguable position. However, this begs the question as to exactly how much more risk do equity investments carry versus fixed income investments? In other words, is the risk of investing in equities (common stocks) versus a fixed income instrument (bonds, CDs etc.) 100 % more risky, 50% more risky, 25% more risky, 10% more risky etc.?

These seem like important questions to ask and have answered. However, I have personally not come across any truly cogent analysis that precisely quantifies the greater risk of a stock or equity over a bond or other fixed income instruments. But with this said, my 40+ years of experience investing in equities leads me to conclude that most people overestimate the greater level of risk that equities possess. This is especially true regarding equities with long histories of paying dividends. Yes, I agree that there is greater risk, but I do not agree that the risk of owning equities is as great as many people contend or believe.

Equity Risk versus Fixed Income Risk

What complicates the matter even more is how risk itself is defined, thought of or interpreted. At the extreme, the question of risk implies the possibility of total loss. Although that possibility does exist, and in fact has occasionally occurred in the real world, I believe that the risk of total loss is rare enough to not be a major concern. Moreover, I believe this extreme risk can be mitigated with even modest due diligence and monitoring. Perhaps not totally eliminated, but certainly diminished.

Moreover, when evaluating the risk of investing in stocks, many investors are referencing price volatility. And usually, by volatility they mean the risk of the price of the stock dropping. However, I contend that if the price of a high-quality company does drop, but the underlying fundamentals of the business remain strong, that it represents opportunity rather than risk. About a year ago I wrote extensively on the subjectfound here.

Additionally, I also authored a two-part series on how investors can mitigate the investment risk associated with owning stocks.In part 1I elaborated more on the concept of volatility risk.

And then, inpart 2I expanded my discussion on risk to include numerous other risks associated with investing in common stocks.

And, for those interested in learning more about the volatility aspect of risk, I authoredanother articlein April 2012.

The primary point I expressed in this last article is my contention that it is not the volatility itself that establishes the risk of owning a stock; rather the greater risk rests in how people react to that volatility. The following excerpts from a comment shared by a regular reader of mine onmy most recent articlenicely summarizes this point.

“ my objective is to earn an income stream that is reliable, predictable and increasing. It's all about the income stream, what I refer to as my pension from Mr Market. I need to know what that pension is going to pay me in the distribution phase of my life. I can do that with dividend growth investing….

This year has seen the market correct to where it is down for the year. The Dow was down over 5% in January alone. Although the market continues to fall, my pension payment continues to rise. I will establish an all-time high in dividend income this month, and it has nothing to do with share prices. Market falls, I get a pay raise…..”

Income Risk

As I previously stated, equity risk is most commonly associated with price volatility and the accompanying potential for loss. However, for retired investors seeking income from their portfolios, there is also the issue of income risk. As it is with most types of risk, this is also a multifaceted concept. For example, there is the risk that your income will not keep up with inflation. Dividend growth stocks with a long history of increasing their dividends do mitigate some or even most of this risk, while a fixed income investment with a constant yield does not.

In contrast, there is the risk of your income falling on an absolute basis. With equities, this would occur with a dividend cut, or worse yet, a total elimination of the dividend. Note: As I was putting the finishing touches on this article, the oil and gas storage MLP, Boardwalk Pipeline Partners (BWP) did in fact cut their distribution by approximately 81%, and their stock price accordingly fell by approximately 40%. Although I do not consider this a high quality blue-chip dividend paying stock in the caliber of a Johnson & Johnson (JNJ), Coca-Cola (KO) or Procter & Gamble (PG), it does put a spotlight on the potential income (and volatility) risk of investing in high yielding equities.

In contrast, high-quality fixed income investments such as government bonds, virtually eliminate this risk altogether, but offer little or no protection against inflation. On the other hand, extremely high quality blue-chip dividend paying stocks such as found onDavid Fish’s lists of Champions, Contenders and Challengers or the Standard & Poor’s Dividend Aristocrats, have historically at least, provided a high level of protection against income risk.

Receiving an adequate level of income on your portfolio is another aspect of risk that should be considered. In the past, one of the most salient features of a bond was high yield. Consequently, it made sense to balance your portfolio with stocks and bonds because the yield advantage from bonds was high enough and the spread large enough to compensate for the lack of inflation risk. But as I’ve written about before, the interest income rates available from bonds and other fixed income instruments are not normal today, nor are they high enough.

With today's extreme, and in the minds of many, contrived low level of interest rates, the risk profile of bonds and fixed income are far from typical. More simply stated, the currently extreme low level of interest offered by bonds and other fixed income instruments have dramatically altered, and I contend, increased their risk profile. In essence, this has narrowed the risk profile between stocks and bonds, and especially so for higher-yielding dividend stocks. Since bonds no longer offer a significant yield advantage, inflation risk has increased and the scales are currently tipping more in favor of higher-yielding dividend paying stocks, at least in my humble opinion.

Moreover, I think it’s important that investors recognize that bond portfolios are also subject to price volatility. Although it is true that if you hold a bond to maturity you will eventually receive its par value. However, during the duration of the bond, the current market price can, and will, fluctuate relative to what current interest rates are doing. As a general statement, if interest rates are rising the market value of a bond will tend to temporarily fall, and vice versa.

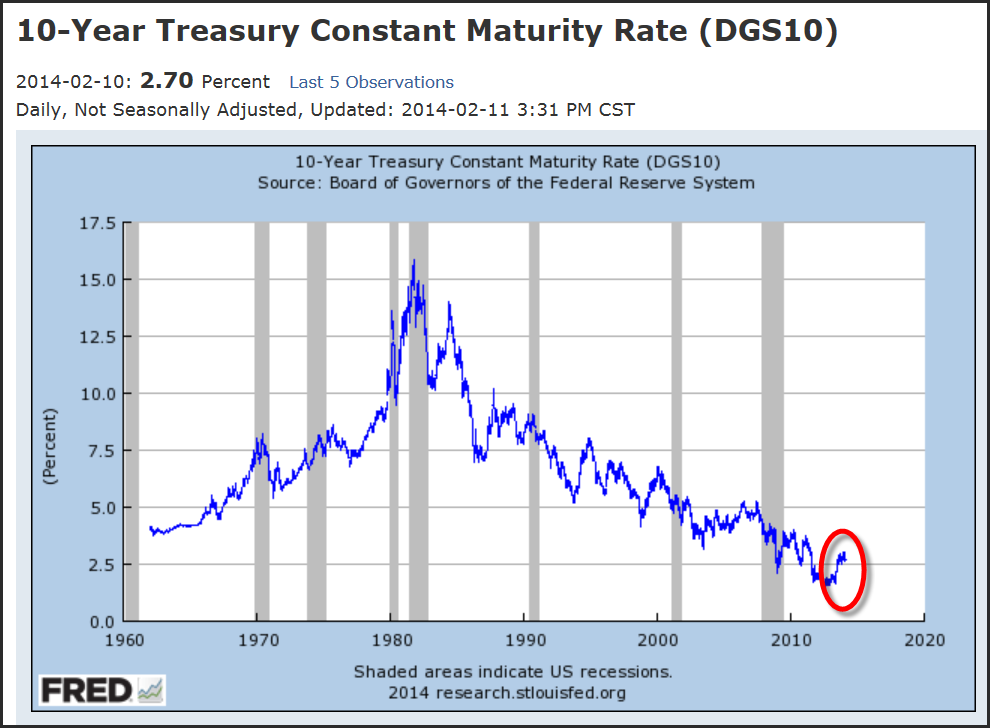

The following graph of 10-year treasury bonds illustrates both how low current rates are, and that they have been rising recently. The point being, bonds can also experience price volatility risk, just as equities do. The only difference might be what causes the price volatility of the bond versus what might cause the price volatility of stock, but the potential price volatility is there nevertheless.

Equities for High Yield in Today’s Low Rate Environment

With due consideration given to all of the many facets of risk discussed above, this article is focused on fairly valued higher-yielding dividend paying stocks. Consequently, the focus of the following research candidates is for generating the highest possible yield on an investor’s retirement portfolio. However, I feel that it’s very important to again point out that this list of candidates is comprised of companies possessing various levels of the risks previously discussed. Moreover, these are also candidates that might be utilized to augment the yields available from a more broadly diversified dividend paying stock portfolio.

Therefore, I think it’s important to again emphasize that in the general sense, higher yield would imply higher risk. However, as I discussed in the introduction, risk is in many ways a relative term. My point being that the following list is comprised of certain higher-yielding dividend paying stocks with low or reasonable levels of risk, as well as some candidates and asset classes that can carry higher levels of risk. Therefore, it’s up to the reader to pick and choose according to their own portfolio construction and tolerances for risk. In other words, I’m not suggesting creating an entire dividend portfolio with this group. Instead, I’m suggesting supplementing or augmenting a dividend growth portfolio by sprinkling in some higher-yielding selections.

My goal is simply to provide research candidates that appear fairly valued based on fundamentals and currently offer yields of 3% or better. But as always, further due diligence is not only suggested, but I feel required. Additionally, since diversification is such an important component of risk control, I present these research candidates in order by sector.

Moreover, I am not suggesting the following is a comprehensive list. Instead, these represent companies that I have hand-selected based on looking for fundamental characteristics that I personally covet as important. I placed a high emphasis on fundamental value and consistency regarding dividend payment histories. Therefore, although the list was not generated in a precisely scientific fashion, I did personally conduct a cursory, but not extensively thorough, review of each. Under each sector, I have also provided an expanded sample or two utilizing various iterations of earnings (funds from operations or operating cash flow when appropriate) utilizing theF.A.S.T. Graphs™research tool. To save the reader from excessive verbiage, I will let the graphs speak for themselves on each selection.

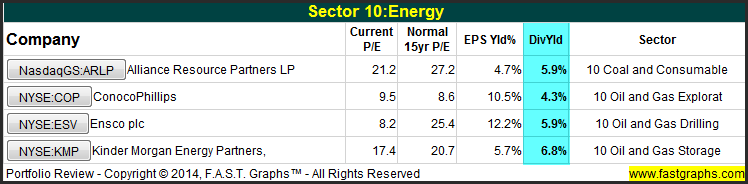

Sector 10: Energy

The Energy Sector is comprised of several higher-yielding dividend paying stocks. However, I also included a couple of MLPs that because of certain tax considerations may not be appropriate for all investors for their retirement portfolios. But, for those that can handle receiving and reporting a K-1, the income and growth opportunities available from investing in select MLPs might be attractive.

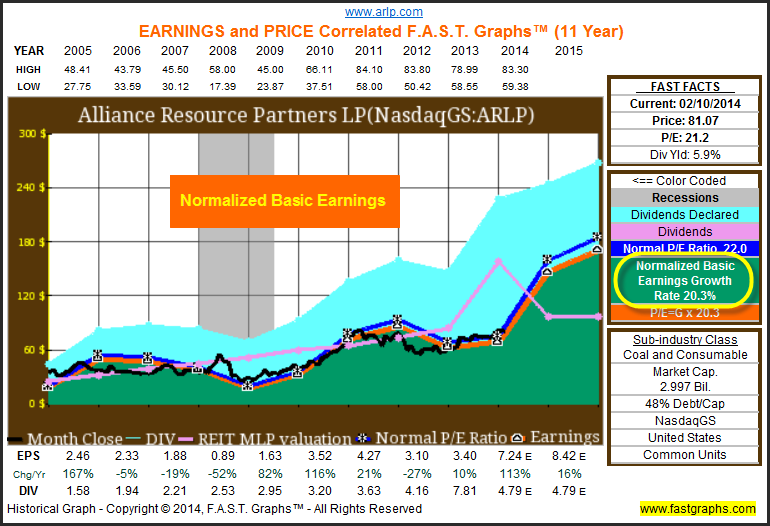

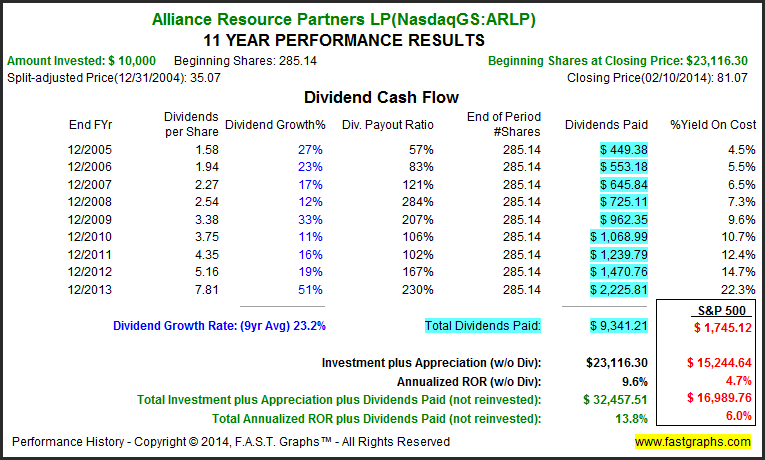

Alliance Resource Partners (ARLP)

Sector 15: Materials

Although I only selected one company in the Materials Sector that offered a dividend yield of over 3.2%, I included it because I had not previously reviewed it. Therefore, I thought it might be an interesting candidate that many readers might have overlooked in the past.

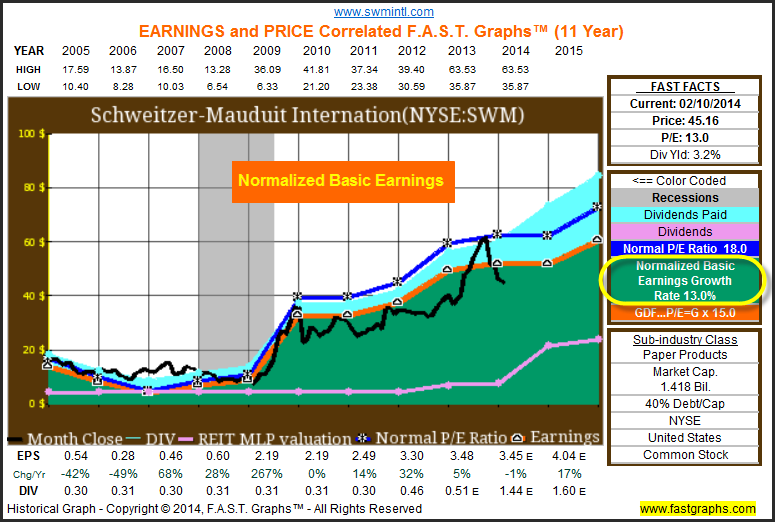

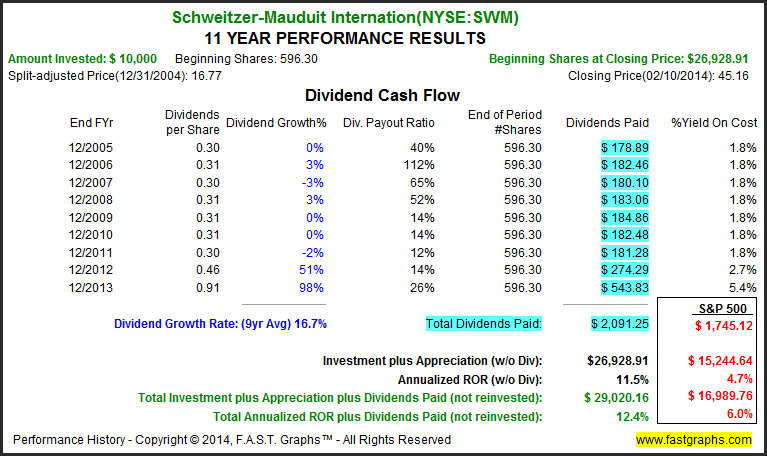

Schweitzer-Mauduit International (SWM)

Schweitzer-Mauduit International, Inc. manufactures and sells paper and reconstituted tobacco products to the tobacco industry, as well as specialized paper products for use in other applications in the United States of America.

Sector 20: Industrials

As it was with the Materials Sector, I also only included one company in the Industrial Sector that met my yield requirement to be included in this article. Moreover, I feel this particular selection provides both an above-average yield, and the opportunity for attractive total return. However, from the risk perspective, the company has only been public since September 2007, consequently lacking the long history that I would typically prefer.

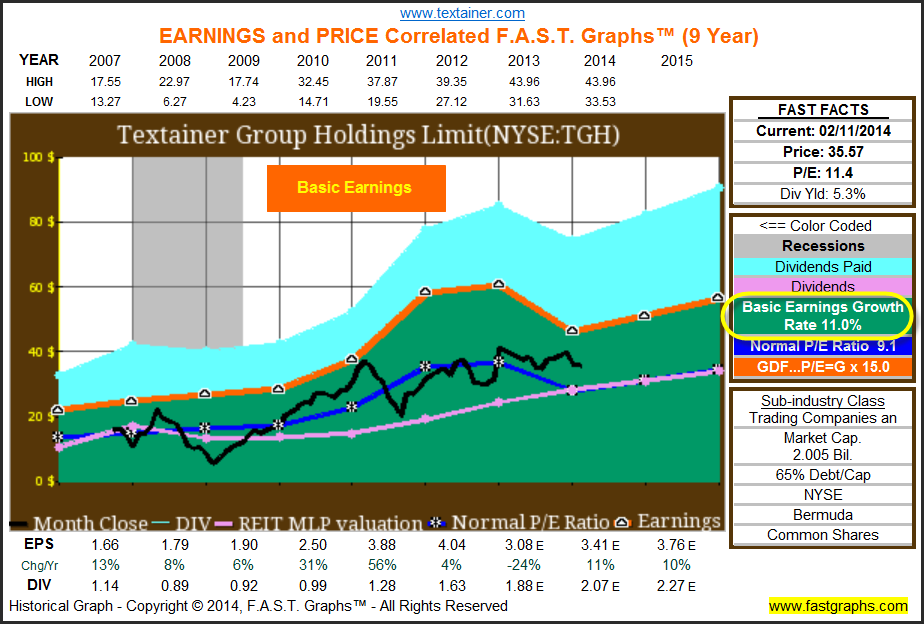

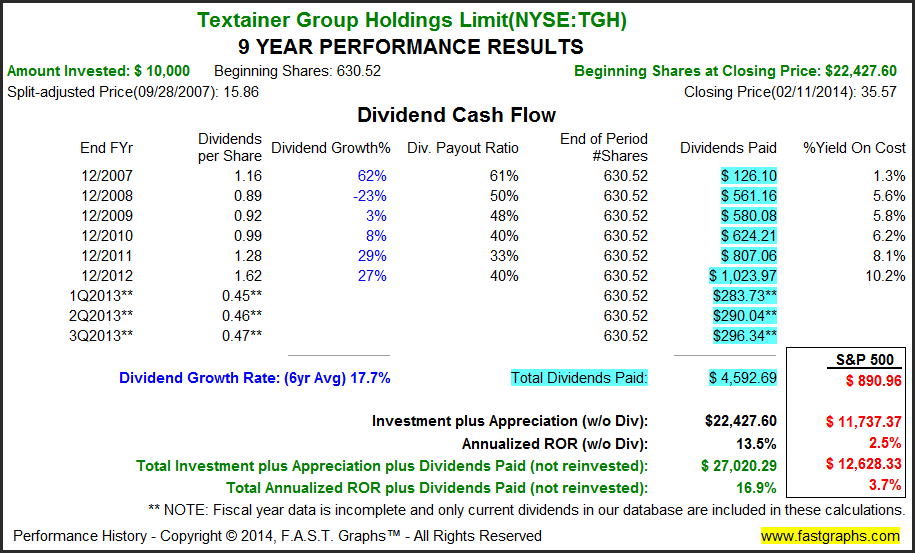

Textainer Group Holdings (TGH)

Textainer Group Holdings Limited engages in the purchase, ownership, management, leasing, and disposal of a fleet of intermodal containers.

Sector 25: Consumer Discretionary

I only came up with two candidates in the Consumer Discretionary Sector. And, although neither of these candidates is devoid of risk, I believe they both offer what appears to be an attractive risk reward opportunity.

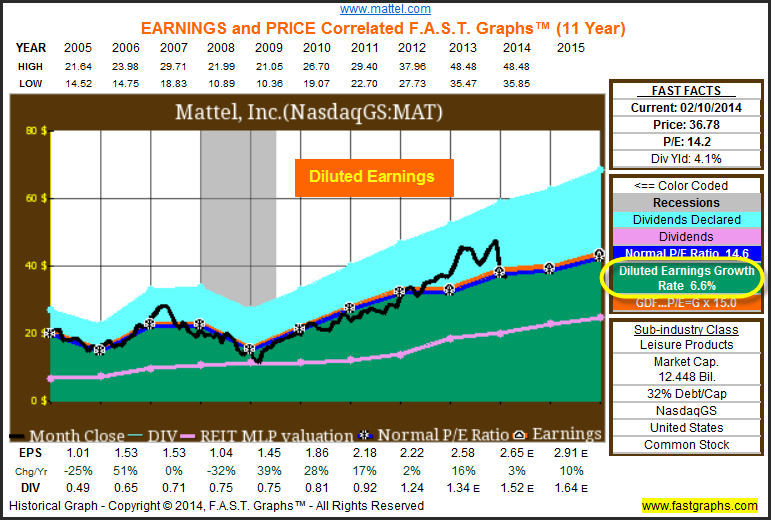

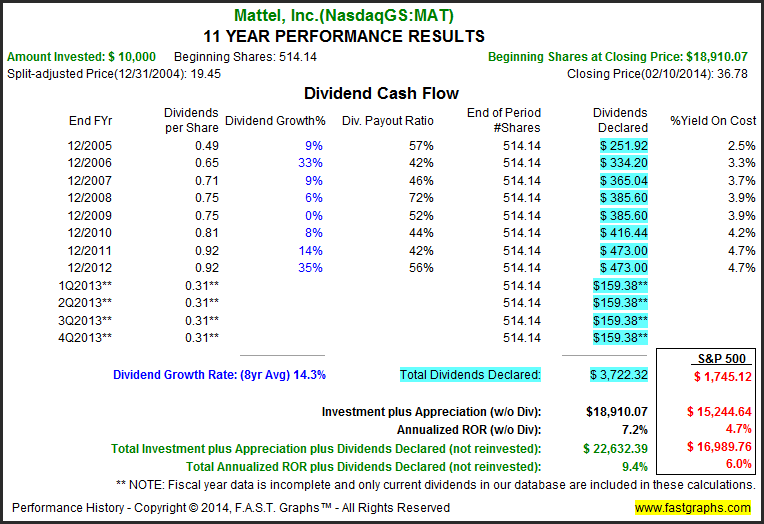

Mattel Inc (MAT)

Mattel, Inc. engages in the design, manufacture, and marketing of toy products worldwide.

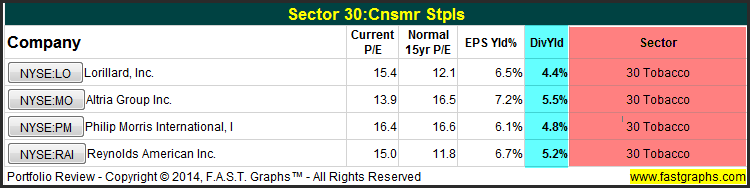

Sector 30: Consumer Staples

In the Consumer Staples Sector, each of my candidates operates in the tobacco industry. As I previously mentioned, I do not necessarily like their product lines, but find it hard to argue with their track records of growth and income growth.

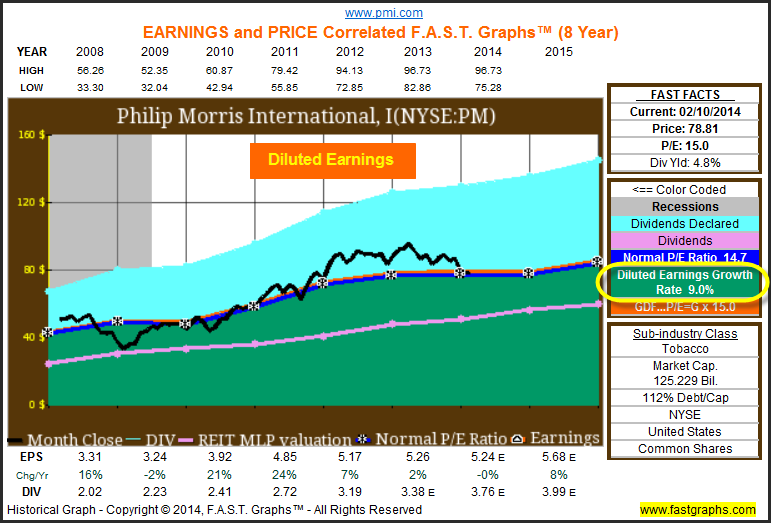

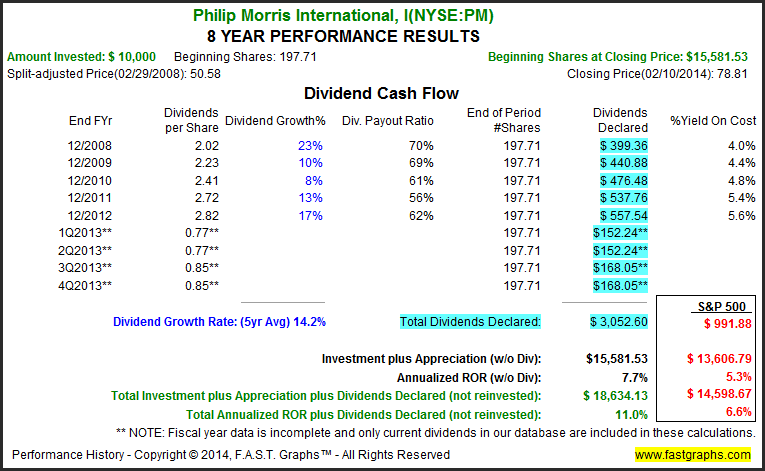

Philip Morris International (PM)

Philip Morris International Inc. engages in the manufacture and sale of cigarettes and other tobacco products in markets outside of the United States of America. The company’s products are sold in approximately 180 markets. Its portfolio comprises both international and local brands.

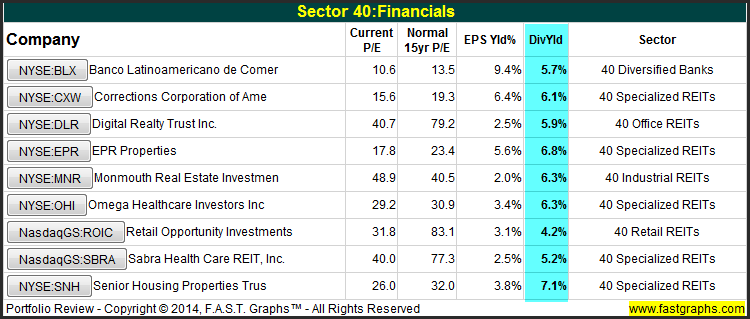

Sector 40: Financials

Regarding the Financial Sector, the majority of the candidates I present are REITs. This may be one industry that provides high yields in today’s environment, coupled with reasonable levels of risk. Moreover, select REITs can also provide attractive total return prospects.

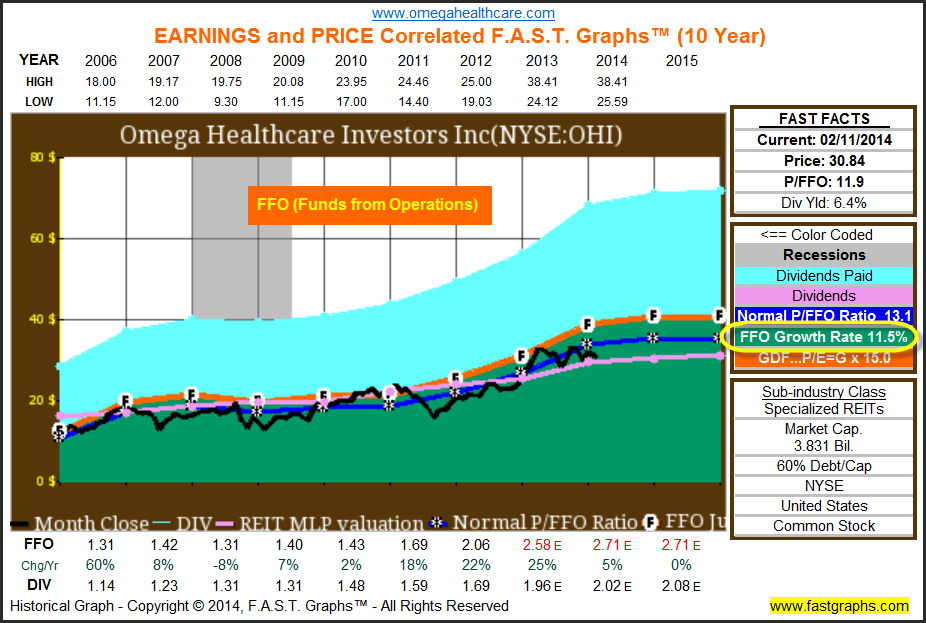

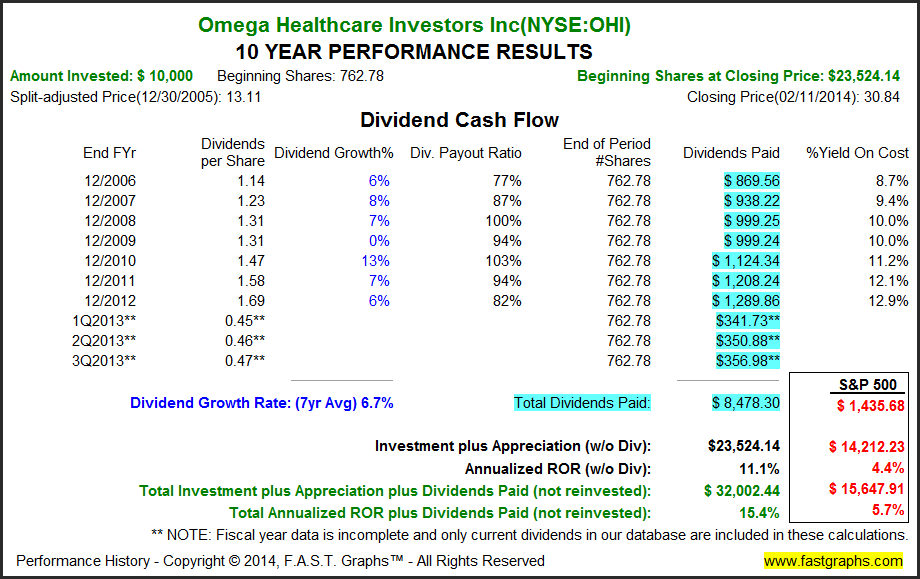

Omega Healthcare Investors Inc (OHI)

Omega Healthcare Investors, Inc., a self-administered real estate investment trust (REIT), invests in income-producing healthcare facilities, principally long-term care facilities located in the United States.

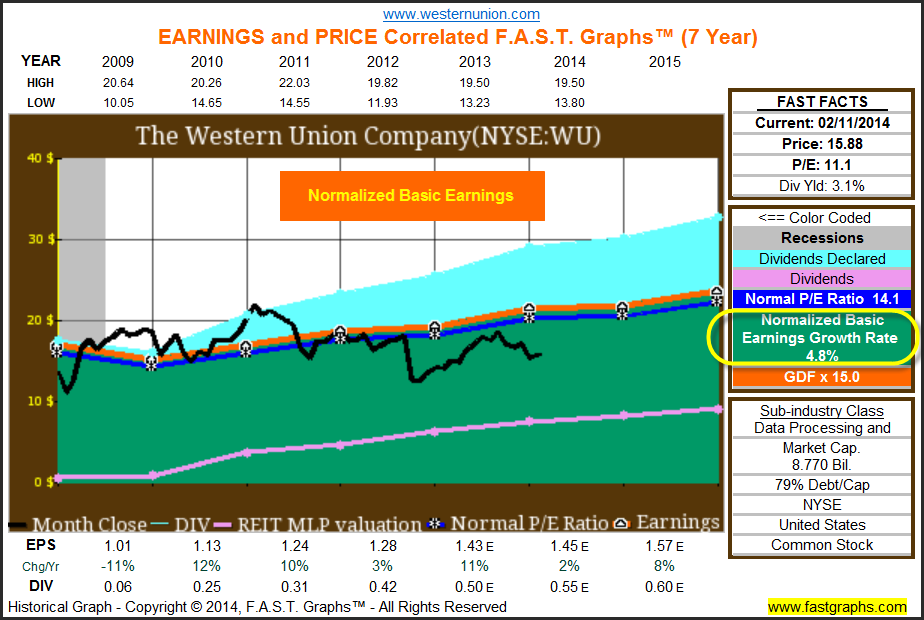

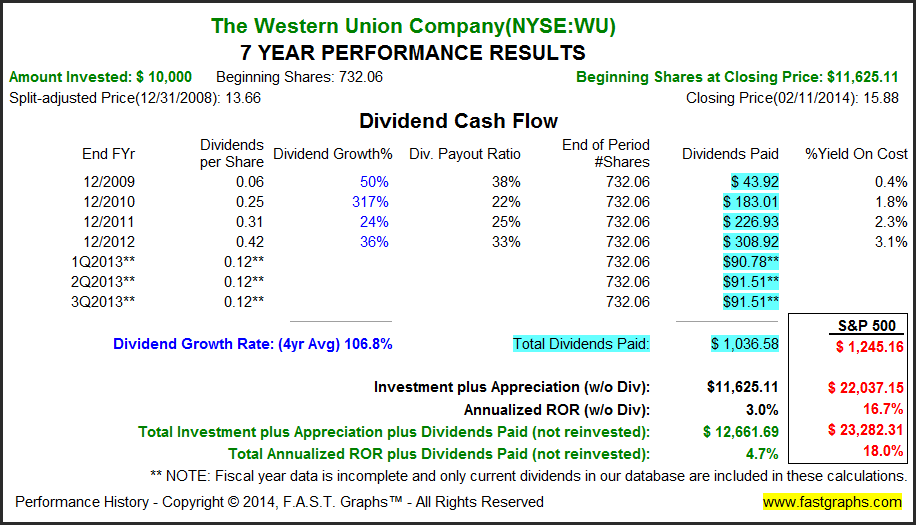

Sector 45: Information Tech

I only provide one review candidate in the Information Technology sector. However, I felt this candidate was worthy of inclusion based primarily on its consistent dividend record since 2009.

The Western Union Company (WU)

The Western Union Company provides money movement and payment services to people and businesses.

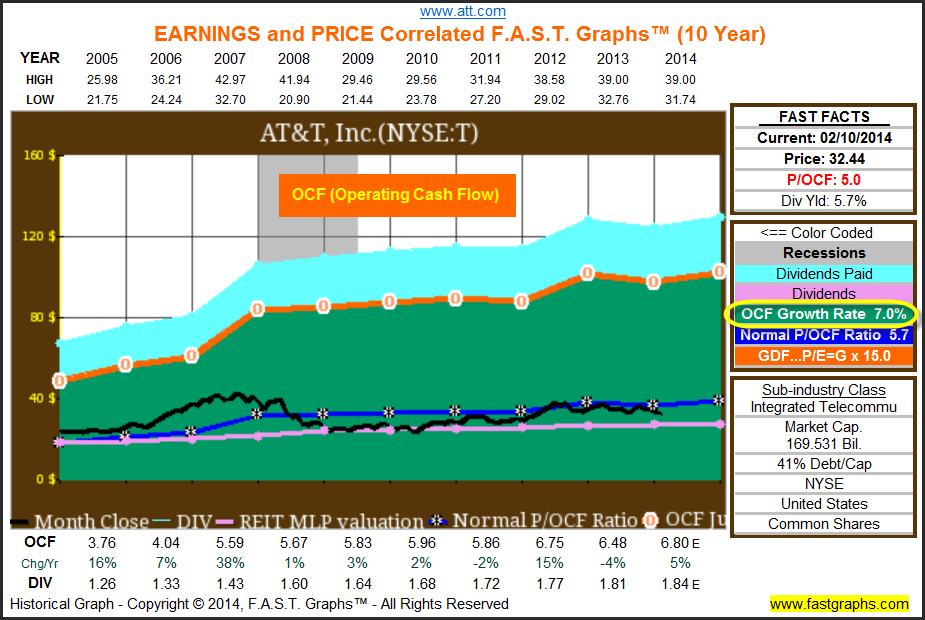

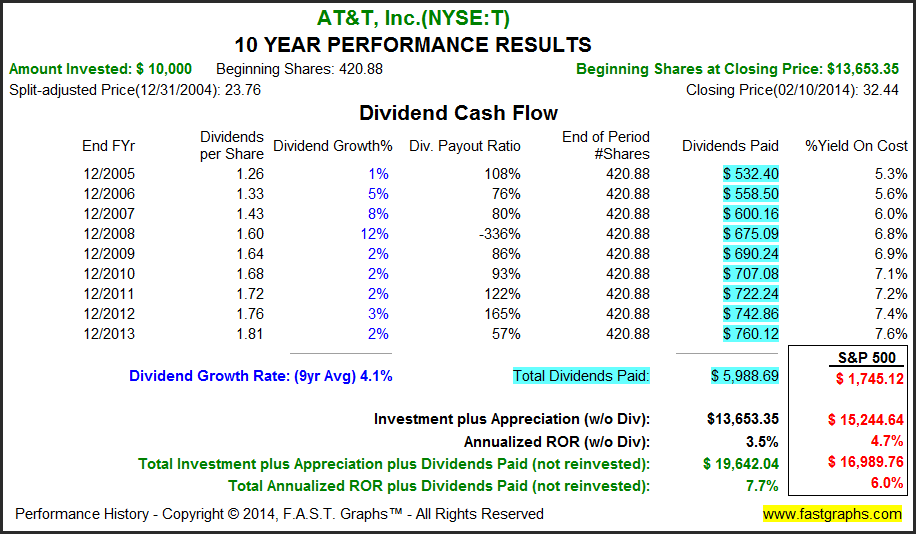

Sector 50: Telecom Services

My only selection in the Telecom Services Sector is AT&T, Inc. I think it’s important for investors to recognize that today’s AT&T is not the same as the AT&T of yesteryears. In 2005 SBC purchased the former parent AT&T and took on its iconic name and stock symbol. Consequently, I’m only showing the company since the merger. Similar to utility stocks, I consider this candidate primarily for the consistency of its dividend and high current yield.

AT&T Inc (T)

AT&T Inc. provides telecommunications services in the United States and internationally. The company offers its services and products to consumers in the U.S. and services and products to businesses and other providers of telecommunications services worldwide.

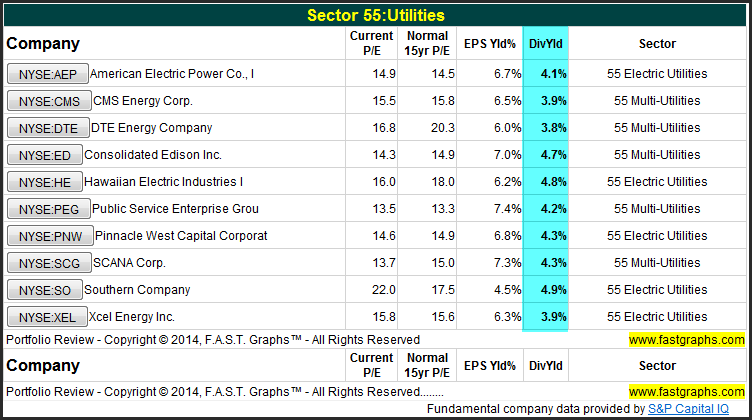

Sector 55: Utilities

I have several selections in the Utility Sector. Since these are all typically low growth entities, I always stress the importance of only investing when fair valuation is manifest. There was a brief period of time during the spring of 2013 were many utility stocks had become moderately overvalued. However, more recently many utilities have come back into alignment with what I think of as their earnings justified valuation. I have long held that the primary purpose of investing in utilities is for current yield due to their low growth prospects.

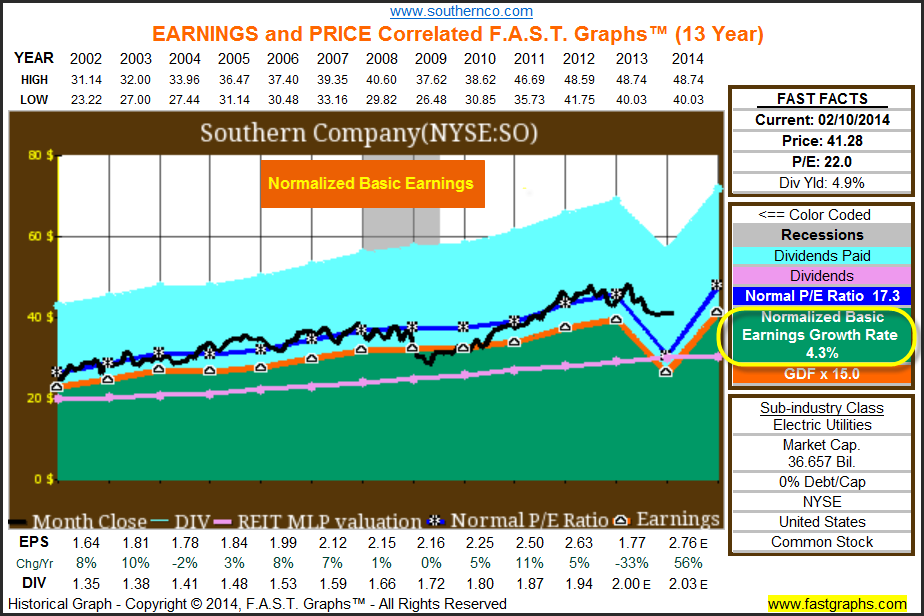

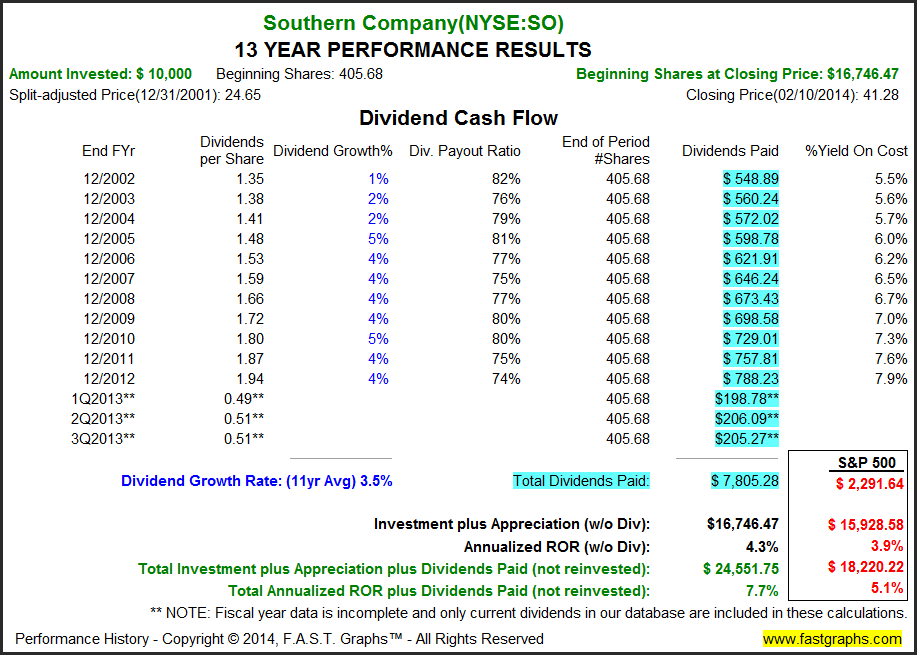

Southern Company (SO)

Southern Company, an electric utility company, engages in the generation, transmission, and distribution of electricity through coal, nuclear, oil and gas, and hydro resources.

(Note:Full year 2013 includes after-tax charges totaling $729 million, or 83 cents per share due to construction of the integrated coal gasification combined cycle facility in Kemper County, Mississippi (Kemper IGCC) significantly impacted the presentation of earnings and earnings per share for the three and twelve months ended December 31, 2013.)

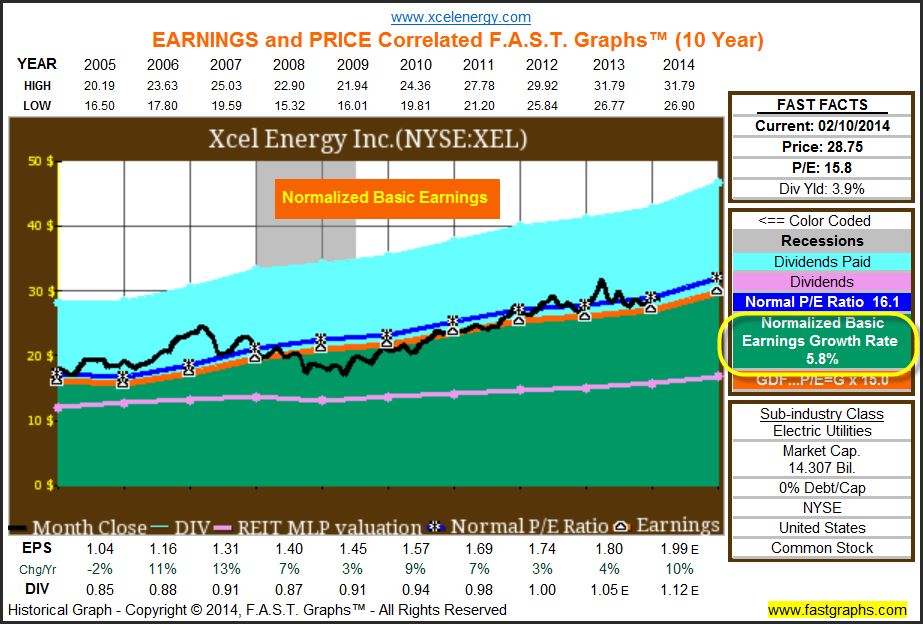

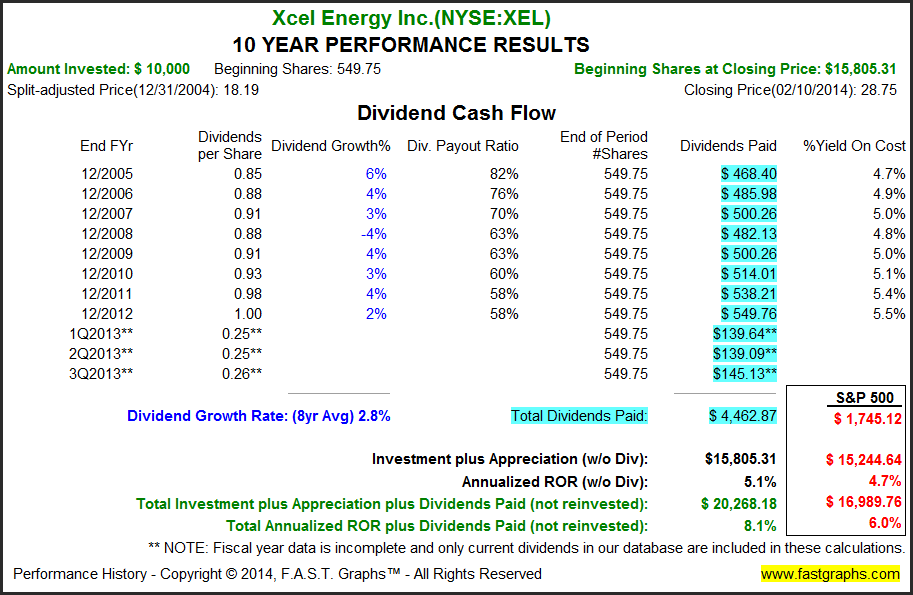

Xcel Energy Inc (XEL)

Xcel Energy Inc., through its subsidiaries, engages in the generation, purchase, transmission, distribution, and sale of electricity in the United States.

Summary and Conclusions

Earning an adequate yield on retirement portfolios is more challenging today than it has been in many years. However, I strongly caution investors against succumbing to the temptation of reaching for yield too aggressively. The general statement higher yield carries higher risk, is generally valid and true, but not necessarily in every specific case. On the other hand, it does not also logically follow that every common stock that carries a higher yield is too risky to invest in. Nor does it logically follow that a given stock with a higher yield than another similar quality stock is the riskier choice.

There are times when a low valuation is the source of the higher yield, and a true low valuation mitigates risk. Therefore, a truly undervalued blue-chip with a higher yield than a fully valued, or even moderately overvalued comparable blue-chip, may actually be the lower risk choice at that time. As I stated in the introduction, there are many facets and even levels to the concept risk, therefore, it behooves every investor to evaluate as many aspects of risk as possible.

However, with all that I have stated in this article, I do think there is a place for higher-yielding common stocks in most every retirement portfolio. Personally, I would not suggest building an entire portfolio of higher-yielding equities. However, a few strategically-placed higher-yielding stocks could make the difference in receiving an adequate level of current income. On the other hand, I tend to eschew the extremely high-yielding equities such as Mortgage REITs. True, the yields look very tempting in today’s low interest rate environment, and the amount of leverage required to earn those yields seems dangerous to me.

Furthermore, there is the definition of high-yield itself. For example, a blue-chip utility stock with an above-average yield but below-average growth might be a good source for current income at the sacrifice of above-average total return. However, the 4% yields available from many quality utility stocks today, is in stark contrast to the 6% to 8% yields available from many high quality REITs or MLPs. On the other hand, many high quality REITs and/or MLPs also carry the opportunity for higher total returns by offering more growth potential than available from a regulated utility stock.

Additonally, there are the higher yields available from companies operating in the tobacco industry. Many companies in this controversial industry have long-established records of raising their dividends based on strong earnings growth legacies. But the option of investing in an industry that provides such controversial (albeit it legal) products raises its own category and unique concept of risk. Nevertheless, the yields and growth are there, at least historically.

The bottom line is that for investors looking for current income, there are many classes and types of higher-yielding dividend paying equities that might foot the bill. However, the risk issues and considerations are both different and important when considering these types of equities. Finally, I believe they should be used sparingly and strategically according to the specific goals, objectives and risk tolerances of each individual investor.

In my next article, part 6 of this series, I will review the challenges and opportunities available with investing in dividend paying cyclical or semi-cyclical equities. As a sneak preview, I will be offering examples of companies with cyclical records of earnings growth, yet with consistent records of dividend increases each year. The challenge with this type of dividend paying stock is greater price volatility during times when earnings are dropping. The opportunity is often found from picking up higher yield opportunities when prices are low prior to a cyclical earnings recovery.

Disclosure: Long ED,SCG,SO,ARLP,COP,KMP,TGH,DRI,DLR,OHI,SNH,T,BWP,JNJ,KO,PG,MO,RAI, at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.