IN THIS ISSUE:

1.US Personal Savings Rate is Falling Once Again

2.Obama Unveils New“MyRA” Savings Accounts

3. The MainProblem With MyRAs – Low Returns

4.US Economy May be Stuck in Slow Lane Long-Term

5.91 Million Americans Aren’t Looking For Work

6. President Obama Lied About the Latest CBO Report

Overview

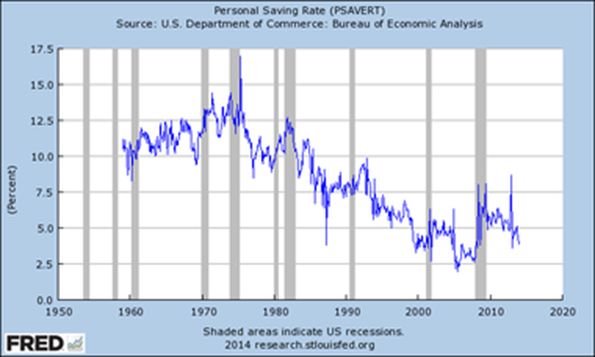

Today we weave together several different topics that are all connected in one way or another. We begin with the US savings rate which is trending lower once again. From 1975 to 2007, the savings rate fell to an all-time low of 2.4%. While it jumped up briefly after the 2008 financial crisis, it is now moving lower yet again.

In an effort to boost the US savings rate, especially for lower income groups, President Obama introduced a new type of starter retirement account for Americans of modest means that he called the MyRA, which stands for “My Retirement Account” and rhymes with IRA.

While the new MyRA may be well intentioned, it is fraught with problems – most notably that it can only be invested in government securities that have yielded paltry returns over the last decade or longer. And when inflation rises, MyRAs are sure to be a big disappointment. I’ll tell you why as we go along today.

Next, the recent Congressional Budget Office report, with its economic projections over the next 10 years, contained several troubling findings that the mainstream media and politicians in Washington deliberately didn’t tell you about. I’ll tell you why below.

Today there are 91 million Americans who are jobless and are not even looking for work. That is 37% of the US adult population, the highest reading in over 35 years. Fortunately, the number is not quite as bad as it looks on the surface, but it is still bad.

Finally, the president recently told a series ofwhoppers following the CBO’s latest report that claims Obamacare will cost 2.5 million jobs over the next decade. He lied, misrepresented and completely contradicted several key statements he has made in the past. Obama easily hit a new high in his presidency for deception. You really need to read this!

US Personal Savings Rate is Falling Once Again

The US personal saving rate peaked in 1975 at above 15% and since then plunged to below 2.5% in late 2006/early 2007. This represents a huge change in financial behavior on the part of the public. Following the Great Recession in late 2007/early 2009, savings habits improved to above 7.5% but have since reverted to below 4%, as seen in the chart below.

In his State of the Union address earlier this month, the president correctly noted that many Americans don’t have a pension and that “a Social Security check often isn't enough on its own.” Their financial security is going to depend on higher rates of savings, he said, and there are many things the president and Congress could do to address the low rates of personal savings in America.

Growth enhancing policies and a tax structure that allows people to keep more of their money would be a great starting point. Higher contribution limits and income limits for popular investment tools like the Roth IRA would also encourage more savings. And, even programs focused on basic financial literacy for those struggling to save would make a lot of sense.

But, rather than really push in directions that could encourage greater savings and wealth creation for all Americans, the president’s big idea was to create yet another savings product in an already crowded market – one aimed largely at lower income Americans.

Obama Unveils New“MyRA” Savings Accounts

In his SOTU speech, President Obama introduced a new type of starter retirement account for Americans of modest means that he called the MyRA, which stands for “My Retirement Account” and rhymes with IRA.

While most readers of my E-Letter are higher net worth folks who will probably never consider a MyRA, you may have kids or friends that might consider one. So I want to briefly explain why this new savings gimmick is a bad deal overall in my opinion, and you can pass this information along to those who might seek your advice.

The MyRA program allows the US Department of Treasury to create a new savings option for people who don’t have access to employer-provided retirement savings plans. Participants can start an account for as little as $25 and additional investments can be made for as little as $5. The investments are not tax deductible, and like Roth IRAs they grow tax free and can be withdrawn at any time without penalty, with one exception.

Principal can be withdrawn at any time with no penalty. However, anyone who withdraws any of the interest they earned in the account before age 59½ will get hit with taxes and a possible penalty, just like a Roth IRA.

While the specifics are still in the works, MyRAs would enable employees of companies that do not offer retirement accounts to save up to $15,000 in small increments if they so choose. Keep in mind that the upper savings limit is only $15,000 – I’ll come back to that later.

Most importantly, the government would guarantee that MyRA investors wouldnever lose their principal. Good deal, right? Not necessarily. It all depends on what savers could earn on their other retirement savings accounts – I’ll get to that just below as well.

MyRA money would only be invested in Treasury securities, which means the program gives the government a new set of purchasers for its debt. How convenient! It is less clear why investors need MyRAs. Individual retirement accounts (IRAs) already offer Americans a way to save for retirement and offer much greater flexibility since they can be invested in securities other than Treasuries.

The Main Problem With MyRAs – Low Returns

The president, who has a disdainful view of Wall Street, wants to make sure the MyRA accounts, first and foremost, protect Americans from loss. Uncle Sam will guarantee that there is no loss of principal. But, in return for 100% safety comes very low returns – what else is new?

Low returns that, in fact, could leave the poor Americans investing in MyRA programs worse offin real terms in the long run. And, ask just anyone in the investing world which returns matter, and they’ll tell you it’s all about “real returns” (ie - returns after inflation). So what kind of returns could MyRAs deliver?

Since Obama floated this MyRA idea earlier this month, analysts have been crunching the numbers. The results arenot pretty. An investor who would have put money into a MyRA in 2012 would have come out behind, once inflation is taken into account. In fact, over the last 10-year period, the real returns for an investor in a MyRA would be about 1.2% annualized when inflation (as measured by the CPI) is accounted for.

When we go farther back into time and look at returns from January 1, 1987 (when interest rates were substantially higher) to the present, MyRA investors would have earned 5.5% on average per year (gross, not inflation adjusted). That might impress some until they consider the fact that the S&P 500 Index returned apprx. 10.3% over the same period of time.

Small percentage differences matter over long periods of time. A $10,000 investment in the S&P in 1987 would have left a person with more than $80,000 today; meanwhile a MyRA investment would be worth only a little over $40,000 today. That’s huge!

This brings up another problem I noted above. The maximum amount that a person can put in a MyRA is only $15,000. Once a participant’s account balance hits $15,000, he/she will have to roll it over to a private sector Roth IRA, where the money can continue to grow tax-free – but the government’s no-loss guarantee goes away at that point.

Workers will have the option to switch to a Roth IRA at any time. But why limit the account to only $15,000? That’s because the government will use taxpayer money to fund the interest paid on the accounts. So it can’t be allowed to get too large lest it would lead to much higher budget deficits.

At the end of the day, the MyRA is just another “feel-good” government program with paltry returns aimed at lower income folks. When inflation picks up again in the future, MyRA savers may actually be losing purchasing power. And finally, it remains to be seen if MyRAs actually become popular. With an estimated 80% of Americans living paycheck to paycheck, my prediction is that they won’t become popular. We’ll see.

US Economy May be Stuck in Slow Lane Long-Term

In the 4½ years since the Great Recession ended, millions of Americans who have gone without jobs or raises in this slow growth economy are asking:

Is this as good as it gets?

It increasingly looks that way.

Two straight weak job reports for December and January have raised doubts about economists’ predictions of breakout growth in 2014. The global economy is showing signs of slowing – again. Manufacturing has slumped recently. Fewer people are signing contracts to buy homes. Global stock markets have sunk as anxiety has gripped developing nations.

Some long-term trends are equally troubling.

In myFebruary 6 blog, I wrote about the latest CBO report which concluded that Obamacare will result in the loss of 2.5 million workers over the next decade, as more and more people elect to simply drop out of the workforce rather than lose their healthcare subsidies.

Yet there was other alarming news in the latest CBO report that bears discussing today. The Congressional Budget Office foresees economic growth picking up only mildly through 2016, and then weakening starting in 2017 and beyond.

By the CBO's reckoning, the economy will soon slam into a demographic wall: The vast baby boom generation will retire. Their exodus – in addition to the loss of 2.5 million workers due to Obamacare – will significantly shrink the share of Americans who are working, which will hamper the economy’s ability to accelerate.

At the same time, the government will almost certainly have to borrow more, raise taxes or cut spending (or all three) to support Social Security and Medicare for those retirees.

Former Treasury Secretary Larry Summers and other noted economists have suggested recently that the economy might be in a semi-permanent funk. In November, Summers warned in a speech that the economy is trapped by “secular stagnation.” By that, he meant a prolonged period of weak demand and slow growth.

If the United States hasn’t already slipped into that period, the CBO predicts it could over the next four years. Again, that’s when the retirements of baby boomers would accelerate and start to restrain growth even more.

The CBO estimates that the economy will expand by only 2.7% in 2017 before declining to an average of 2.2% annual growth through 2024. That’s even slower than the current anemic recovery has been, on average, so far.

There are no documented examples of an economy that had to emerge from a financial crisis while simultaneously absorbing the effects of an aging population, noted Harvard University economist Carmen Reinhart, who has researched eight centuries of crises with her colleague Ken Rogoff. “These things are new,” she said.

Many Americans who endured the worst of the downturn remain wary, sensing that the recession caused an enduring economic downshift. Some businesses are still reluctant to hire despite higher revenue. And they’re wondering, when will we get back to normal? Historically, “normal” has been when GDP averages 3% or better.

Yet according to the non-partisan Congressional Budget Office, the US economy is likely to remain in the slow lane for another decade through 2024. That is as far out as their projections go.

Finally, I have yet to see anyone in the mainstream media touch any of these troubling long-term projections from the CBO. Certainly no politician is going to bring this up. Yet I believe that my clients and readers want to know these facts, troubling as they are.

91 Million Americans Aren’t Looking For Work

The official unemployment rate isn’t always the best measure of the job market, because it only includes people who have actively searched for work within the last four weeks. Many Americans just aren’t looking for jobs.

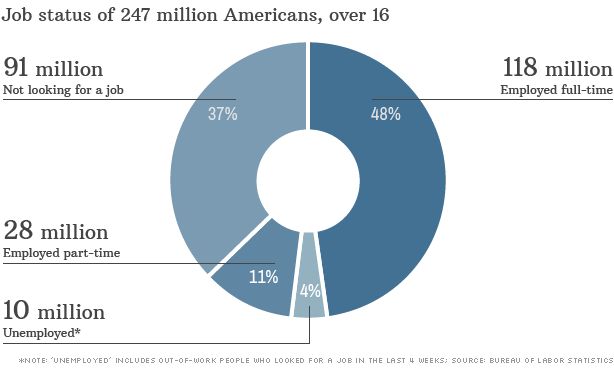

New facts from the Labor Department show that about 91 million adult Americans don't work, and aren’t looking for jobs. They make up 37% of the population – the highest level on record since 1978. Some of them are workers who’ve been out of a job for so long that they've given up entirely.

But it’s not quite as bad as it looks. In addition to discouraged workers, this group also includes people who are retired, enrolled in high school or college and those staying at home to take care of young children or elderly relatives.

Here is a complete view of the US working-age population, including everyone over age 16.

Full-time workers, at 118 million, still make up almost half of the population. About 48% of working-age Americans have full-time jobs, and another 11% work part-time. Historically, those numbers have been considerably higher.

President Obama Lied About the latest CBO Report

The president told a series ofwhoppers following the CBO’s latest report that claims Obamacare will eliminate 2.5 million jobs over the next decade. This was a new and devastating blow to Obamacare. In response, the president lied, misrepresented and completely contradicted several key statements he has made in the past about his signature healthcare plan. Obama easily hit a new high in his presidency for deception in the last week or so.

The media should be embarrassed for not reporting this – that is, if they were sharp enough to catch it in the first place. As a result, most Americans didn’t catch it either. But I certainly caught it and so did Peter Schiff, the CEO of Euro Pacific Capital, and one of my favorite writers.

If you have any interest in politics – conservative or liberal – you should read this article on Obama’s egregious contradictions of late:

About the Healthcare Law, President Obama Speaks With a Forked Tongue

I wish I had written it!

Best regards,

Gary D. Halbert

© Halbert Wealth Management