Emerging Market Woes abd Fed Tapering Equals Stocks Plunge

IN THIS ISSUE:

1. “Fragile Five”– Emerging Nations in Trouble

2. Fed Continues to Taper as Yellen Takes Over

3. GDP Rises by 3.2% in 4Q – Advance Estimate

4. Blog: Americans Are Still Pessimistic

5. Justice Dept. Indicts “2016” Film Producer Dinesh D’Souza

Overview

January saw US stocks record their first losing month since last August. After reaching new record highs at the end of December, the Dow Jones shed almost 1,000 points in the last half of the month and the decline continues. Analysts attributed the sell-off in large part due to troubling news from several emerging nations, in particular to the so-called “Fragile Five” – Turkey, India, Brazil, Indonesia and South Africa.

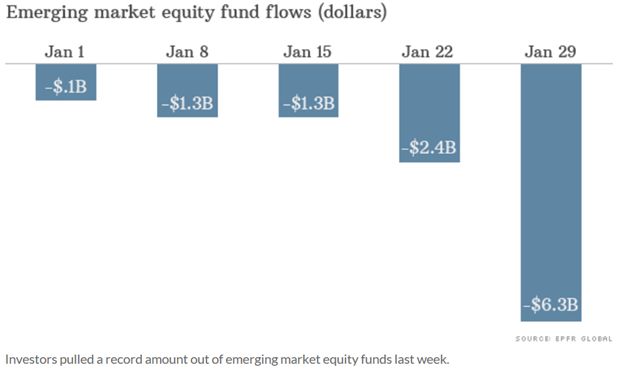

These countries and others have seen their currencies come under pressure due to capital flight, and most have had to raise interest rates significantly and drain reserves to support their monetary systems. Actually, it was Argentina that sparked the global sell-off by lifting its currency controls on January 24. Ongoing protests in Ukraine and Thailand have only added to a heightened sense of uncertainty in the developing world.

No doubt, this mini-storm is partly a reaction to the Fed’s decision to begin “tapering” its monthly purchases of Treasury bonds and mortgage-backed securities (MBS) starting in January. At its latest policy meeting last week, the Fed moved to reduce its QE purchases by another $10 billion in February. Obviously, the Fed is serious about ending QE and this, too, weighed heavily on stocks last month and again yesterday. Is this the much-awaited “correction” or something worse?

Next, we take a look at some of the latest economic reports. We got our first look at 4Q GDP last Thursday, with an advance estimate of +3.2%, about as expected. What was not expected was a huge drop in the manufacturing sector in January based on yesterday’s weak ISM Index report. There is also some weakness showing up in the housing sector. It will be interesting to see if the weaker economic news and the plunge in the stock markets will cause Janet Yellen to slow the Fed’s tapering.

Finally, if you watched the 2012 film documentary “ 2016: Obama’s America,” you may be interested to know that Obama’s Justice Department recently indicted the film’s producer, Dinesh D’Souza, on two alleged felony charges related to campaign-finance irregularities. Such violations, if true, are rarely prosecuted, but not in this case. They want to ruin his life. You can read the story at the end of today’s letter.

“Fragile Five”– Emerging Nations in Trouble

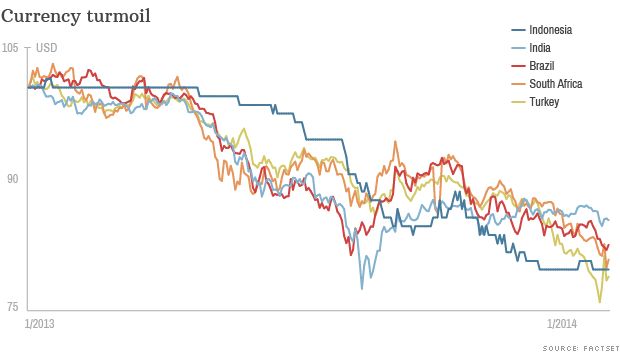

The so-called Fragile Five have seen their currencies plummet 15% to 20% over the past year. That includes Turkey, India, Brazil, Indonesia and South Africa. Those five are in addition to Argentina, Ukraine and Thailand that are experiencing similar troubles.

And that plunge continued in January despite a series of aggressive and, in some cases, unexpected interest rate hikes aimed at stopping the rout. So after years of rapid expansion, and relative calm, what's going wrong?

For one, economic growth has slowed. As a group, emerging and developing economies grew on average by 6.4% over the past decade. Last year, that number slipped to 4.5% and it’s forecast to rise only modestly in 2014.

In addition, signs of instability in China’s huge shadow banking system have raised fears of a credit crunch that would make it hard for Beijing to deliver its 7.5% growth target. China’s first decline in factory activity in six months has only made matters worse.

Cheap money is also drying up. The Federal Reserve said last week that it will continue pulling back on its stimulus, to the tune of another $10 billion this month. That means the central bank will pump $65 billion a month into the US economy, down $20 billion from December. And the flow of cash is likely to cease completely by the end of this year. We will talk more about that as we go along today.

But that doesn’t entirely explain the dramatic moves seen in some markets. Take India, for example. India’s finance minister said last Thursday, “ The Fed’s decision was expected and should not in any way surprise or affect the Indian markets. ” Yet India’s central bank surprised investors with an interest rate hike last Friday in an effort to stabilize its currency.

India’s finance minister was talking up his country’s prospects at the recent World Economic Forum ahead of national elections, but a weak coalition government and continued policy stagnation are likely to remain in place going forward.

In general, the gradual normalization of US monetary policy (ending QE) and rising interest rates in many countries have made it less attractive to invest in emerging markets, particularly those which have failed to tackle deep-rooted fiscal problems during the last several years or longer.

And that’s where the Fragile Five come in. Over the past year or two, all have experienced slower growth, along with a heavy and growing dependence on foreign capital, and stubbornly high inflation of between 6% and 11%.

Many analysts believe that the currencies of the Fragile Five had become overvalued in the last several years, and that the latest downward pressure was more or less inevitable given the slowdown in the global economy. As a result, some forecasters believe that the currencies of Turkey, South Africa and Brazil still have further to fall.

In Turkey, where the lira fell to a record low last week despite interest rates almost doubling overnight, the prime minister has faced calls to resign over a wide-ranging probe into political corruption. Local and presidential elections are due there later this year.

The African National Congress may well lose ground in parliamentary elections this year but is still likely to influence the next South African government. If so, that will reduce the chances of major reforms that are needed to help stabilize the nation’s currency and the economy.

Brazil may catch a temporary break from the currency pressure as it will host the soccer World Cup in June. In Indonesia, the popular governor of Jakarta is a clear front-runner for July’s presidential election, and some feel he may undertake meaningful reforms. Yet the biggest economies in Latin America and Southeast Asia are not out of the woods.

There is a risk that the economic and currency problems afflicting numerous emerging nations will spread to other countries. Almost all of these nations have significant exposure to China, which is seeing its own economy slow down.

The Fragile Five all face elections at some point in 2014, making painful reforms even less likely. So, political upheaval is another thing they have in common, and may be the single factor that determines whether they can bounce back or not.

The bottom line is that after a decade of blistering growth, many emerging countries have had a severe, albeit delayed, fall from grace after the Western-led global financial crisis that started in 2008. With elections looming, 2014 will be a challenging year on the political front. This could continue to weigh on global equity markets in the weeks and months just ahead.

So for now, we need to keep our eyes on Turkey, India, Brazil, Indonesia, South Africa, Argentina, Venezuela and even China.

Fed Continues to Taper as Yellen Takes Over

Last Friday was Ben Bernanke’s last day as Chairman of the Federal Reserve, capping eight years in that role – including the financial crisis that unfolded in 2008 and the more than $4 trillion in QE purchases since then. It remains to be seen whether or not history will be kind to Mr. Bernanke.

Janet Louise Yellen (age 67) was sworn in yesterday as the new head of the Fed, and as such she becomes one of the most powerful women in the world. She served as the Fed Vice Chair since 2010, and before that she was the president of the Federal Reserve Bank of San Francisco. Ms. Yellen has instructed her staff to refer to her simply as “Chair” rather than “Chairwoman.”

Yellen is widely considered to be one of the more “dovish” (more concerned with unemployment than with inflation) members of the Fed’s policy committee. As such, she would be less likely to push for higher interest rates. Moreover, as a Keynesian economist, she may be likely to advocate for higher inflation, since she considers that to be good for the economy. We can argue about that, of course.

However, Yellen appears to be fully onboard with the Fed’s effort to halt quantitative easing by the end of this year. The Fed Open Market Committee (FOMC) met last week, and as expected, voted to reduce monthly QE purchases by another $10 billion this month to $65 billion. That is down from purchases of $75 billion in January and $85 billion in December. The FOMC policy statement read as follows regarding tapering:

… the Committee continues to see the improvement in economic activity and labor market conditions over that period as consistent with growing underlying strength in the broader economy. In light of the cumulative progress toward maximum employment and the improvement in the outlook for labor market conditions, the Committee decided to make a further measured reduction in the pace of its asset purchases.

Beginning in February, the Committee will add to its holdings of agency mortgage-backed securities at a pace of $30 billion per month rather than $35 billion per month, and will add to its holdings of longer-term Treasury securities at a pace of $35 billion per month rather than $40 billion per month.

The FOMC meets seven more times this year. If the current $10 billion per meeting reduction in QE purchases continues, the program would end in December of this year. That remains to be seen, of course, but that is the general expectation – IF the economy continues to grow at least modestly.

The next FOMC meeting will be on March 18-19 after which Ms. Yellen will hold her first press conference as the new Fed Chair. It will be interesting to see if the FOMC reduces QE purchases by another $10 billion at that time.

GDP Rises by 3.2% in 4Q – Advance Estimate

The Commerce Department reported last Thursday that gross domestic product rose 3.2% (annual rate) in the 4Q of last year. That was about in-line with pre-report expectations but down from 4.1% in the 3Q. For all of 2013, GDP rose 2.73%.

The report said that growth in the 4Q came mainly from consumer spending, exports, non-residential fixed investment and state and local government spending. As expected, there was a deceleration in inventory growth. The second estimate of 4Q GDP growth will be released on February 28.

Most forecasters continue to expect GDP to rise by more than 3% in 2014. That remains to be seen, of course, especially in light of the emerging market troubles discussed earlier, not to mention the current plunge in the stock markets.

One somewhat troubling spot for the economy that will heavily weigh on the Fed’s decision to further taper is the residential sector. Real residential investment plunged 9.8% in the 4Q and monthly indicators – including housing starts, permits, and new home sales – all posted lackluster readings in December. New home sales numbers, which were released last week, dropped to a 414,000-unit pace, with downward revisions to the previous three months.

There is one large caveat to keep in mind, however. Unseasonably cold weather likely played a large role in the weak readings and could further dampen housing market indicators in the next couple of months. Softer data certainly would bring into question the sustainability of the housing recovery. The fate of the housing market could well give Janet Yellen & Company second thoughts about tapering too fast.

On another front, the much-watched ISM manufacturing index plunged much more than expected yesterday, falling from 56.5 in December to only 51.3 in January. That was lower than even the most pessimistic pre-report estimate.

Stocks plunged yesterday after the ISM figures showed its new orders component declined by the most since December 1980, as a number of companies said adverse weather slowed business. General Motors and Ford said that fewer Americans ventured out to motor-vehicle dealerships during the coldest January in two decades.

Blog: Americans Are Still Pessimistic

A new NBC News/Wall Street Journal poll out last Tuesday found that 68% of Americans say the country is either stagnant or worse off since President Obama took office. Some 70% are dissatisfied with the economy. And a whopping 81% disapprove of Congress.

Obama Justice Dept. Indicts “2016” Film Producer Dinesh D’Souza

Finally, many of you will remember that I highly touted the 2012 documentary film “ 2016: Obama’s America ” that was co-produced by Dinesh D’Souza. While not a “hatchet job” on Obama, the film purported to trace the president’s left-leaning politics to the communism and anti-colonialism of his father in Africa.

Recently, the Obama administration indicted D’Souza for not one but two felony charges, arising out of alleged campaign-finance irregularities in 2012. Eric Holder’s Justice Department claims that D’Souza made some $20,000 or so in illegal campaign contributions, via other donors, to Wendy Long, the Republican candidate in the New York Senate race – contributions D’Souza could not lawfully make himself because he was already “maxed out” at the $5,000 ceiling. I have no idea if this is true or not.

What I do know is that this is the kind of case on which the government routinely declines criminal prosecution, handling it instead by an administrative fine. D’Souza has no criminal record. So this is clearly a vindictive prosecution that could well land D’Souza in prison.

Moreover, contrary to myriad of voter-fraud violations that Attorney General Holder will not lift a finger to pursue, the transactions at issue, if true, posed no conceivable threat to the integrity of the election process: Ms. Long lost by 46 points. As observed by no less than Harvard’s Alan Dershowitz – an Obama supporter:

“ This is clearly a case of selective prosecution.” There would, the professor added, be “ no room in jails for murderers ” if the Justice Department made a practice of such prosecutions.

The bottom line is that President Obama and Attorney General Holder are intent on ruining D’Souza’s life and making sure he cannot produce a planned sequel to the original 2016.

Best regards,

Gary D. Halbert

© Halbert Wealth Management