This Just In: The Secular Bear Market May Be About to Resume.

In our 2012 book, Investing in the Second Lost Decade we laid out the case for the secular bear market in equities lasting at least through the end of the decade. Since then prices of most averages have moved to all-time highs. It’s time to throw in the towel on the secular bear market for stocks… right? Not necessarily, because Table 1 shows that there are precedents during a secular bear where prices experienced a primary trend peak well above that of the official secular bear starting point. Table 1 shows that between 1902 and 1906 and 1966 and 1973 for instance prices reached their nominal secular bear market peak at the time of the third cyclical bull market high, well after the official start of the secular “downtrend.” This report will update evidence that could be nearing the next cyclical bear market within a long-term (secular) bear market for equities.

Table 1 Secular bear market rallies compared to the secular peak

|

Secular Peak |

Secondary Peak |

%Gain |

Tertiary Peak |

%Gain |

|

1902 |

1906 |

13 |

1909 |

17 |

|

1966 |

1968 |

14 |

1973 |

27 |

|

2000 |

2007 |

1 |

2013 |

22 |

When analyzing secular equity trends it would appear that nominal prices do not count for very much. It is inflation adjusted prices that are more meaningful over long periods of time. For example I might buy a stock today and perhaps double my money in 10-years but that is of little value if the CPI also doubles over the same period! In this respect at the end of December inflation adjusted equities were approximately 10% below their March 2000 starting point.

Causes of Secular Bears

We think there are three causes of secular bear movements. They are structural, psychological and instability in the commodity markets. In reality all three are interconnected. Let’s consider the structural argument first. When an economy overheats and falls into recession the factors that caused the contraction are relatively easily corrected. For example, it might be that inventories build up to excessive levels as confidence steadily grows during an expansion. When sales fall as the economy rolls over those inventories must be unwound, but that is a relatively brief process, extending over just a quarter or two. Structural problems on the other hand, are far more deep seated. They are caused by a decade or more in which a leading industry, often featuring a new technology, is very profitable gradually attracting more and more capital. Eventually overbuilding results in a state of overcapacity. Examples that come to mind, are canals in the early nineteenth century and railroads in the mid-part. More recently we saw the dot com bubble burst in 2000 and the speculative housing boom in 2007-2008. These represent serious distortions, but most of these structural imbalances can be worked off during the course of a couple of economic cycles. Inevitably though, this natural cathartic process is slowed because of government action, which is directed more at the symptoms than the root causes of the problem. For example, the unwinding of excessive manufacturing in the 1920’s was followed by the introduction of tariffs and international competitive devaluations.

It’s not hard to find examples of structural headwinds in the current cycle, whether it be an aging population or new government regulations emanating from the 2008 financial crisis etc. It’s true the deficit is shrinking, but that is only a cyclical event. Precious little is being done to solve the structural deficit problem. How much will it expand when the next recession hits? Somewhere in there a central bank bond buying program using 70x leverage sounds like the Fed is determined to outdo what private banks mistakenly did prior to the last crisis.

The second rationale for secular bears comes from very long-term swings in investor psychology. This is best captured by the cyclically adjusted Shiller P/E Ratio (see Chart 1) as it works its way higher over a couple of decades to a peak in excess of 22.5 and subsequently zig zags down for another 18 or so years to the 7 or 8 level. High readings indicate that investors are excessively optimistic, otherwise why would they be prepared to pay so much for stocks. At the other extreme, fear and pessimism are so rampant that investors demand to be paid a high rate of return in the form of a lower P/E. They need that level of compensation for the terrible times they perceive ahead. The red highlights in the inflation adjusted equity series in the upper panel reflect recessions. The previous three secular bears experienced lots of them compared to the single recession in 1990 during eighteen year 1982-2000 secular bull. Indeed the plethora of recessions reflects the structural problems associated with a secular bear. In addition, their persistent repetition help promote the mood of desperation and hopelessness, so necessary for the foundation of a new secular bull.

Chart 1 Inflation adjusted equities versus the Shiller P/E ratio (1900-2014)

The latest January data is in well above the 22.5, danger zone and is far closer to a secular peak than a trough. Bullish observers might argue that this was an aberration, as the P/E valuing techniques are not overvalued. However, we see the same type of overvaluation in dividend yields, currently at 2.09% compared to a typical secular low of 6-7%. The Tobin Q ratio, which measures the market’s replacement value typically peaks above $1.08. According the excellent dshort.com web site the latest reading is $1.05, well above the $0.30 level usually found at secular lows.

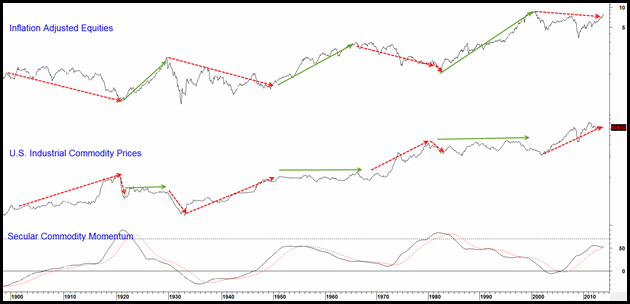

Unstable commodity prices, in whichever direction they develop, are also bearish for equity prices. In this respect Chart 2 compares inflation adjusted U.S. equities to U.S. Industrial commodity prices.

Chart 2 Inflation adjusted equities versus U.S. industrial commodity prices (1898-2014)

The green arrows flag the secular equity bulls. They are usually associated with commodity prices experiencing a trading range, or in some cases declining slightly. Contrast that to the fact that secular bears develop under a banner of sharply rising commodity prices as flagged by the long dashed red arrows. The three short arrows remind us that equities also do not like severe deflationary pockets, such as that the one that developed between late 1929 and 1933.

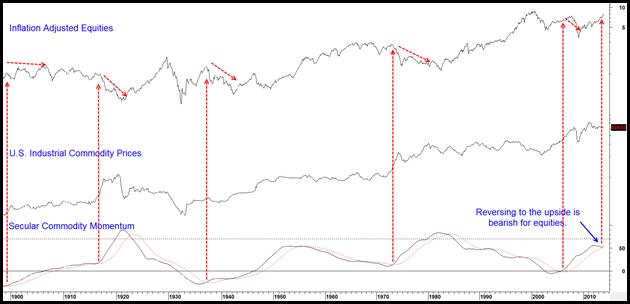

Chart 3 Inflation adjusted equities versus secular commodity momentum (1898-2014)

Chart 3 shows that when our secular commodity momentum indicator reverses to the upside the strongly rising commodity prices that it is forecasting sooner or later hurt stocks. Note that this indicator started to turn up again in December.

The Current Primary Trend

If the negative warning from this series is to pan out we really need to see some additional primary trend evidence pointing in the same direction. In that respect traditional primary trend measurements such as long-term smoothed momentum, the 9- or 12- month moving averages remain positive and will likely take a month or two before they signal a bear market. However, there are a couple of historically accurate relationships which are currently flashing a high risk environment.

Chart 4 Inflation adjusted equities versus the Shiller P/E / Corporate AAA yield ratio (1880-2014)

Chart 4 compares the rate of return between stocks and bonds using the ratio between the Shiller P/E and Moody’s AAA Corporate Bond Yield . A low reading indicates that stocks are undervalued against bonds and a high one an overvalued and risky situation for equities. Usually when the ratio reverses from an undervalued level, close to or below the green horizontal line, it represents a generational buying opportunity for equities. Since 1880 four such situations developed. Three of them, 1921, 1932 and 1982 represented secular lows. By the same token, eight prescient sell signals were also triggered as the indicator peaked at or above its overvalued zone. Two of those warnings were also associated with secular peaks, namely those in 1929 and 2000. A ninth sell signal was triggered a few months ago.

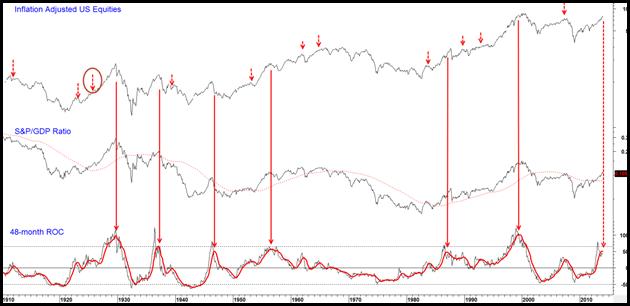

Chart 5 Inflation adjusted equities versus the S&P/GDP ratio(1900-2014)

Another way of assessing the popularity of equities is to consider the ratio between the S&P and GDP. It shows us when equities are over or under owned relative to the economy. The basic trends of this relationship reflect secular trends in inflation adjusted stocks. However, it is its momentum that is more reflective of the popularity swings in equities. In that respect, the six long arrows in Chart 5 indicate that whenever the 48-month ROC exceeds the +65% level and this is followed by a downside reversal in its MA, the equity market experiences a reversal of at least primary trend importance. Two such signals, 1929 and 2000, were secular tops. The small arrows above the inflation adjusted stock series all indicate reversals in the MA of the ROC that took place from above the zero level. Thus, in the last 114 years, a combined total of 17 signals were triggered: only one, in the mid-1920’s, failed. Some of them may look inconsequential, but remember the chart covers a long period of time. Consequently, the slightest squiggle can represent a meaningful decline. For example, the average stock lost 20% in 1994, which appears on the chart as a straight line.

Don’t Let This Secular Bear Eat Your Portfolio

The secular bear market for stocks that began in 2000 will continue to frustrate buy and hold investors. At present some indicators are in the process of reversing from very extended levels, providing strong warning signals that we could be nearing the next cyclical bear market within a long-term (secular) bear market for equities. As this secular bear market continues risk management will be crucial as investors will need a defensive game plan to protect wealth during cyclical down turns and one for offense, to grow wealth during favorable conditions. The active business cycle investment strategy we utilize in the Pring Turner Business Cycle ETF (DBIZ) is designed to help investors survive and prosper during the inevitable boom and bust periods that lie ahead.

DISCLOSURES: The views expressed herein represent the opinions of Pring Research, are provided for informational purposes only and are not intended as investment advice or to predict or depict the performance of any investment. These views are presented as of the date hereof and are subject to change based on subsequent developments. In addition, this document contains certain forward-looking statements which involve risks and uncertainties. Actual results and conditions may differ from the opinions expressed herein. All external data, including the information used to develop the opinions herein, was gathered from sources we consider reliable and believe to be accurate; however, no independent verification has been made and accuracy is not guaranteed. Neither Pring Research, nor any person connected with it, accepts any liability arising from the use of this information. Recipients of the information contained herein should exercise due care and caution prior to making any decision or acting or omitting to act on the basis of the information contained herein.

Copyright © 2014 Pring Research. All rights reserved.