Stocks for 2014: Fairly Valued Dividend Growth Stocks with an Emphasis on Dividends - Part 4

Introduction

I am a firm believer that common stock portfolios should be custom-designed to meet each unique individual’s goals, objectives and risk tolerances. With that said, I believe it logically follows that in order to create a successful portfolio, the individual investor must first conduct some serious introspection to be sure that they truly “know thyself.” Therefore, I believe the first, and perhaps most critical step, towards designing a successful equity portfolio is to ask your-self, and honestly answer several important questions.

As an aside, I feel this first step is critical regardless of whether you are a do-it-yourself investor (DIY) or are inclined to hire professionals to manage your portfolio. My point being, that even the best designed portfolio will fail if the person for whom it is constructed to serve is not emotionally capable of sticking with it through all market environments. It is an undeniable truth that there is no such thing as a perfect stock portfolio that is capable of providing uninterrupted positive performance under all market and economic scenarios. In other words, as investors, we must be prepared and capable of weathering the occasional storm. To be clear, this paragraph is alluding to the inevitability of stock price volatility over time, and the respective individual investor’s ability to deal with it.

Consequently, a few of the most important questions that must be honestly answered are: How will I be able to handle the inevitable price volatility that goes hand-in-hand with the long-term ownership of stocks (businesses) in an equity portfolio? Will I be able to stay calm or am I more inclined to panic during bad markets? Am I comfortable being a long-term investor, or do I prefer investing as a swing trader? These are the types of questions that must be honestly answered and considered carefully in order to build and manage an equity portfolio that’s ultimately successful and appropriate for you.

With the above thoughts in mind, this series of articles is offered in order to provide reasonably valued common stocks of various kinds providing the potential of something for everyone. Inpart 2andpart 3my focus was on providing ideas for investors most interested in total return. Consequently, growth ideas trumped dividend ideas. In this part 4, and all remaining additions, the focus will shift from growth to income. Therefore, the emphasis of this and all remaining articles will be on dividend income and the growth thereof. Hence, and to summarize, my second and third articles may be more relevant to investors seeking total return, whereas this and all subsequent articles should be more relevant to investors focused on maximizing their dividend income streams.

A Few Words on Total Return Performance Standards and Reporting

There are very rigid regulatory and industry standard performance reporting requirements. The objective is to require and assure that any and all management firms, to include mutual funds, indices, ETF’s and RIA’s etc., calculate and report performance numbers that are apples-to-apples comparisons. Therefore, all performance reporting is presented on a level playing field. In a general sense, this is a very good thing that provides investors a level of confidence when comparing the performance of one group to another.

On the other hand, like most things in life, there are certain weaknesses and flaws with strictly adhering to these standards that can, in effect, be partially misleading. The calculation of total return numbers represents a case in point. Although I agree, that when the rules are strictly followed as they are required to be, total return calculations tend to be quite accurate. In simple terms, the calculation of total return includes both the capital appreciation component and the dividend income component on equity portfolios over the time period being measured. However, a total return calculation, though accurate, does not always or adequately tell the whole story regarding performance.

This point is especially relevant and important to retired investors with the objective of maximum current income. The problem is that the two components of return, capital appreciation and income, are being reported in the aggregate. However, for the income investor, total return calculations do not satisfactorily reflect the area of performance that is most relevant to them. To these investors, the dividend yield or income component is what matters most. However, total return calculations do not separately report the capital appreciation component and the dividend component.

I offer the following examples of calendar year 2013 performance on portfolios that I manage on behalf of clients to illustrate my point. The dividend growth portfolios that I manage produced a total return of 31.64% in 2013. In comparison, the S&P 500 produced a slightly higher total return of 32.39% during calendar year 2013. Therefore, at first glance, it appears that the S&P 500 outperformed my dividend growth portfolios, albeit it only modestly. However, if the two components of return are looked at separately you would discover that my dividend growth portfolios outperformed the S&P 500 on the area of performance that mattered most - dividend income.

The current dividend yield and the total cumulative dividends paid in 2013 were substantially higher on my dividend growth portfolio than it was on the S&P 500. To put it simply, it logically follows that the capital appreciation component on the S&P 500 was greater than on my dividend growth portfolios, but not the dividend income portion. Since my dividend growth portfolios were designed to produce current income at reasonably controlled levels of risk, it is clear that they outperformed the S&P 500 where it mattered most - income.

Furthermore, so far in early 2014, the current yield of my dividend growth portfolios is slightly over 3% whereas the S&P 500 is only offering a current yield of 2%. Accordingly, the yield advantage continues on, regardless of whether or not capital appreciation turns out to be more or less than the S&P 500 in 2014. In other words, I am confident that my dividend growth portfolios will continue to produce more yield in future time than the S&P 500, just as they have in past time. This is important because the dividend income is being distributed without the need to harvest principal.

Moreover, the vast majority of stocks in my dividend growth portfolios are blue chips with long histories of increasing their dividend every year. To be clear, the dividend income on my dividend growth portfolios increased from the prior year in 2007, 2008, 2009, 2010, 2011, 2012 and again in 2013. In contrast, the S&P 500 had a sharp 21% decline of their dividend in 2009. Of course, both my dividend growth portfolios and the S&P 500 experienced sharp declines in stock price (negative capital appreciation) in 2008 during the Great Recession. However, the important difference was that my dividend growth portfolios continued to produce higher income each and every year, which is the primary investment objective of the portfolios.

The above performance examples are not offered to brag or as an excuse. Instead, they are offered to illustrate an important principle that is often overlooked when comparing performance results, especially when the focus is only on total return. Although everyone is happy to achieve high total returns on their portfolios, if the investment objective is dividend income, which is most relevant to retired investors, then total return does not tell the whole story. However, current reporting standards do not accommodate the separation of the two components of return - capital appreciation and dividend income.

There is another important principle relating to capital appreciation that only focusing on total return tends to ignore or overlook. The capital appreciation component of the total return calculation represents what is commonly called anunrealized gain. In other words, capital appreciation is not captured unless and until the security is sold. In contrast, dividend income is a realized return because it is paid in cash. Consequently, to that extent, the capital appreciation component is potentially illusionary, while the dividend component is real.

Fairly Valued Dividend Growth Stock Research Candidates for Current Yield

The primary focus of this article is on dividend income, and the long-term growth of that dividend income. Consequently, I screened the universe for high-quality dividend paying stocks with current yields above 2.5% and a history of increasing their dividend each year. Of equal importance was identifying those high-quality dividend paying stocks that were at, below or very near fair valuation currently.

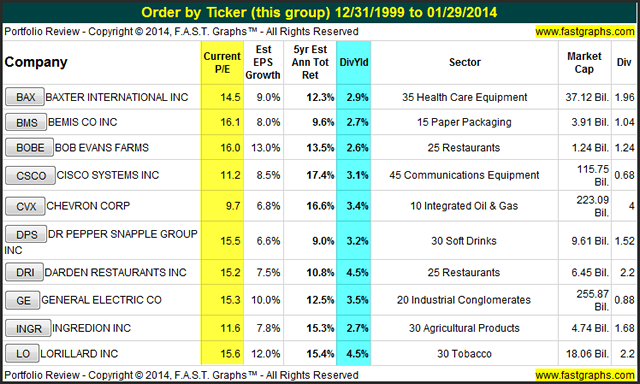

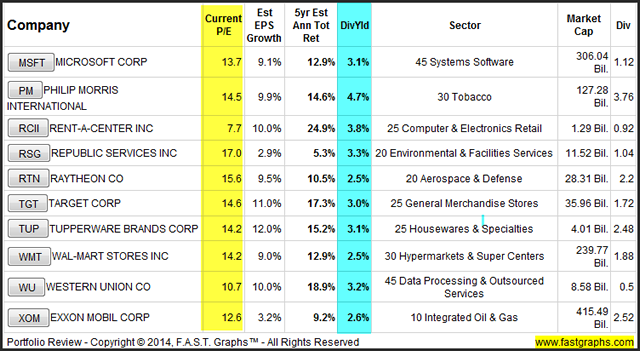

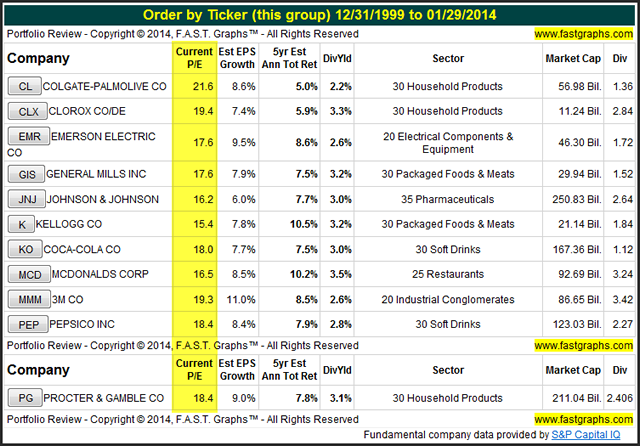

The following portfolio review generated in alphabetical order lists 20 potential research candidates that meet my criteria. As a generalized and oversimplified statement, I believe that most of these candidates would represent sound purchases for the dividend growth investor at a P/E ratio of 15 or below. Consequently, a few of these candidates have current P/E ratios that are modestly above that threshold. However, I believe that the reader should consider that fair valuation should always be thought of as a range of valuation. Therefore, my 15 P/E ratio objective could be thought of as a P/E ratio range of 14 to 16. On that basis, they would all represent candidates that are at least worthy of further due diligence and/or consideration.

Portfolio Review: 20 Fairly Valued Dividend Growth Stock Research Candidates for Current Yield

Inpart 1of this series I highlighted two sample candidates, Chevron and Wal-Mart Corporation. With this article, I will highlight two additional above-market yielding dividend growth stocks.

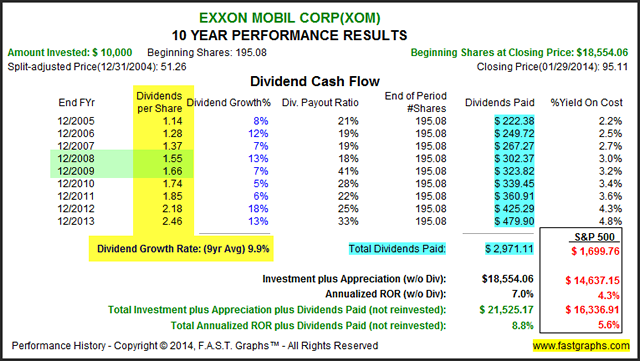

Exxon Mobil Corporation: (XOM)

Exxon Mobil Corporation engages in the exploration and production of crude oil and natural gas, as well as the manufacture of petroleum products, and transportation and sale of crude oil, natural gas, and petroleum products. At this point, the reader should note that major oil producers have seen their earnings capitalized at a discount to companies in other industries with similar records of earnings and dividend growth. Therefore, I believe that prospective investors should take that fact under careful consideration when considering investing in the integrated oil and gas sector.

Considering that the average company as measured by the S&P 500 is currently commanding a P/E ratio slightly above 16, Exxon Mobil Corp. with a P/E ratio of only 12.6 appears to be a bargain. In truth and fact, this may be so. However, as I previously stated, prospective investors should be aware of the typical discounted valuation these companies have received over the last decade or longer as depicted by the dark blue line (normal P/E ratio line) on the Earnings and Price Correlated Graph below. The orange line represents the typical fair value P/E ratio of 15, which clearly illustrates that Exxon Mobil Corp.’s stock has rarely traded at a normal 15 P/E ratio since 2005.

'

Associated 10-year Performance Report – Focus on Dividends

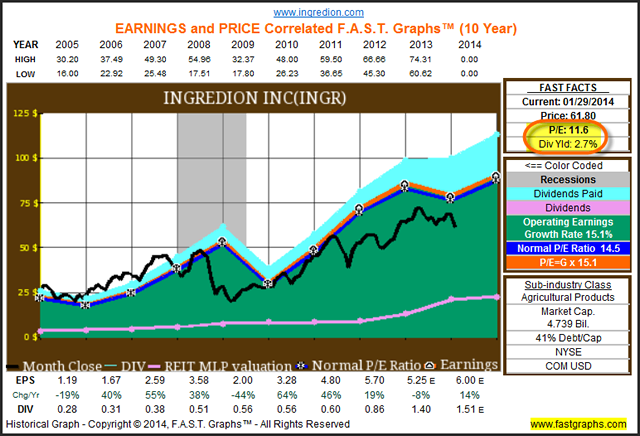

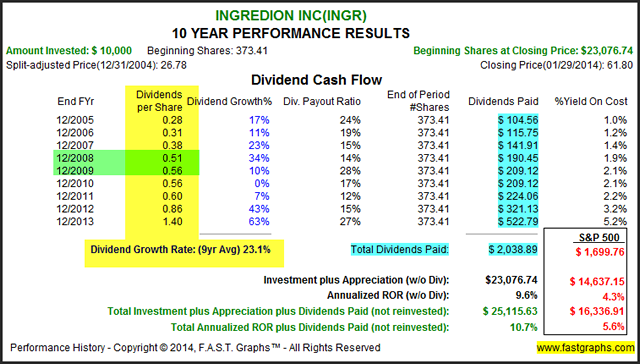

Ingredion Incorporated: (INGR)

My second example, Ingredion Incorporated, manufactures and sells starches and sweeteners derived from the wet milling and processing of corn and other starch-based materials to a range of industries, including the food, beverage, brewing, pharmaceutical, paper and corrugated products, textile, and personal care industries, as well as the global animal feed and corn oil markets.

Perhaps this company’s current low valuation can be attributed to a moderate drop in earnings for fiscal 2013. On the other hand, current forecasts for a resumption of operating earnings growth to record numbers expected for 2014 might represent a great long-term buying opportunity.

Associated 10-year Performance Report – Focus on Dividends

10 High-Quality Blue-Chip Quality Premium Candidates

As regular readers of my work know, I am a stickler for only investing when I believe a company’s stock is trading at or below fair value. As a general rule, I stand by that investing philosophy and belief. However, there are exceptions to every rule. Accordingly, there is a group of extremely high-quality blue-chip dividend paying stalwarts that arguably can only be normally purchased at a premium to my strictest definitions of fair valuation based on earnings. I have previously written about these quality premium candidatesfound here.

Consequently, as a bonus of sorts, I offer the following 11 high-quality blue-chip dividend paying stalwarts that appear to be sound investments today, assuming you’re willing to pay a quality premium to invest in them. However, perhaps a few explanatory remarks regarding the justification supporting these stocks’ commanding a quality premium valuation is in order. First of all, by a quality premium I’m suggesting that these stocks are routinely awarded a higher valuation (P/E ratio) on their earnings than is awarded to the typical or average company. In other words, the market is asking you to pay more for one dollar’s worth of these companies’ earnings, than it generally asks you to pay for other companies with comparable earnings records and growth rates. This begs the simple question, why?

As a general tenet of investing, higher quality implies lower risk. For example, with bonds, corporate bonds are generally required to pay higher interest rates than government bonds. This is, in essence, the equivalent of the quality premium on equities. More simply stated, investors are willing to accept less return for lower risk. Paying a higher valuation for a blue-chip stock represents the same principle. In theory at least, investors seem willing to pay up for quality.

The following 11 names are commonly considered as the crème de la crème of dividend paying blue-chip stalwarts. These companies are all Dividend Champions or Aristocrats and offer consumers products and services that are among the world’s leading brands. I believe that few could argue that these are all great and renowned publicly traded corporations.

Portfolio Review: 11 Fairly Valued “Quality Premium” Dividend Growth Stock Research Candidates

Earnings and Price Correlated Graphs Depicting Quality Premium Valuation

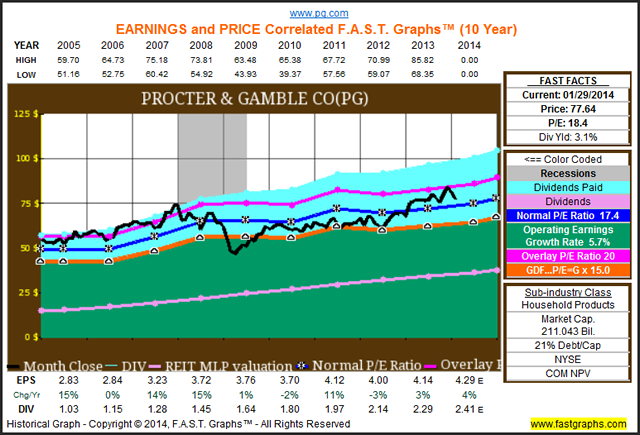

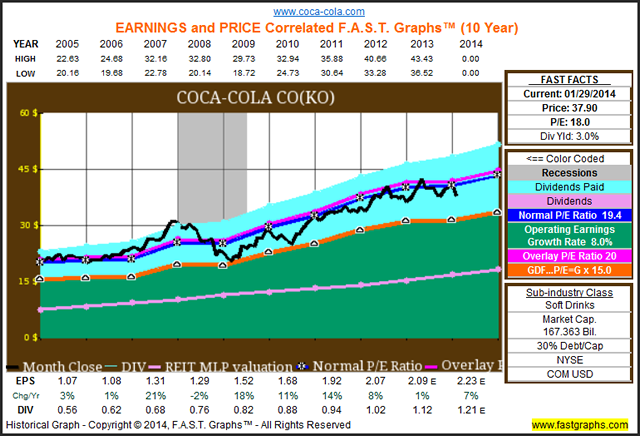

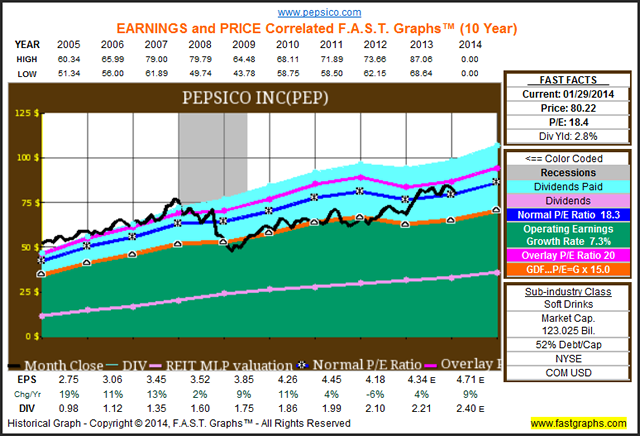

Although my quality premium valuation hypothesis is only a theory, real-world evidence seems to validate the premise. The followingEarnings and Price Correlated F.A.S.T. Graphs™on four of these leading dividend growth stocks provide the evidence I am referring to. There are three valuation lines on the graphs that I would like to direct the reader’s attention to.

The first is the orange earnings justified valuation line which depicts the theoretical fair valuation P/E ratio of 15, which commonly applies to the average company based on the rate of change of earnings growth. By using this line as a barometer or guide to a typical measurement of fair value, we discover that each of these companies’ stock price (the black line) tends to be above this standard valuation metric.

This brings us to the dark blue line (normal P/E ratio line) that illustrates the valuation that the market has typically applied to each of these companies. Here we discover that during normal economic times stock price has correlated more closely to this higher valuation line with these examples. However, the reader should also note that the time period presented (calendar year 2005 to current) also includes the Great Recession of 2008 which brought the price of most stocks temporarily lower, and these quality premium blue-chips were no exception. On the other hand, in each example below, we see that the stock price of these quality names is returning to their more normal valuations (the blue line).

The magenta valuation line on each graph is one that I added utilizing the P/E overlay option of F.A.S.T. Graphs™. I included this line because it is more representative of the normal valuations of these blue chips over the past two decades. In other words, the longer timeframe diminishes the temporary effects that were brought by the Great Recession. Therefore, I feel that the magenta line is more representative of the typical quality premium valuation that the market has historically applied to these names.

The point of this exercise is to illustrate and provide evidence that a quality premium valuation is the norm for these blue chips. Even so, it is up to the individual investor to decide for themselves whether this evidence supports investing in these high quality companies at their typical premium valuations. On the other hand, a review of the performance reports included would support the notion that the decision to invest in these names at a quality premium valuation is a sound one. This position is further supported by the impeccable dividend records of each of these companies.

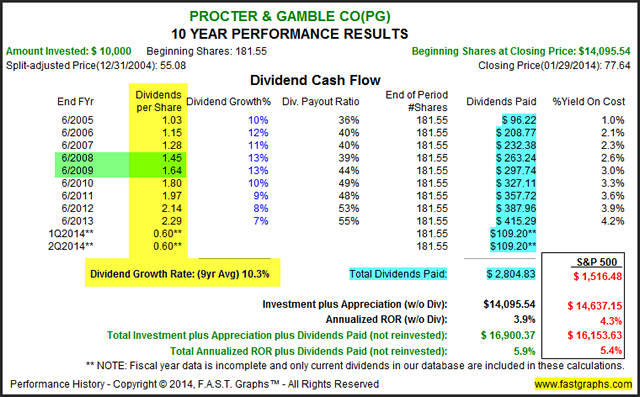

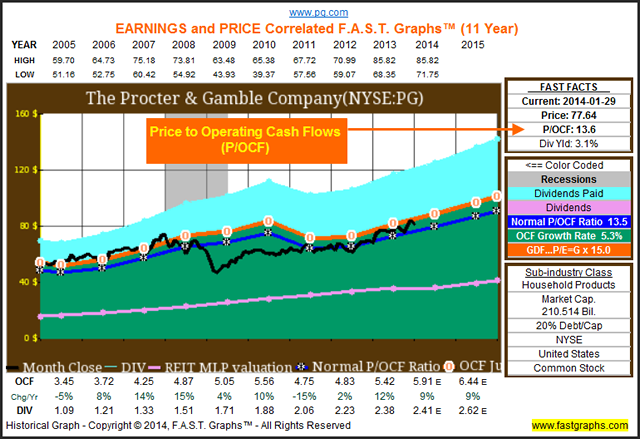

Procter & Gamble: (PG)

The Procter & Gamble Company provides branded consumer packaged goods. The company’s products are sold in approximately 180 countries and territories primarily through retail operations including mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, high-frequency stores and e-commerce. The company has on-the-ground operations in approximately 70 countries.

Associated 10-year Performance Report – Focus on Dividends

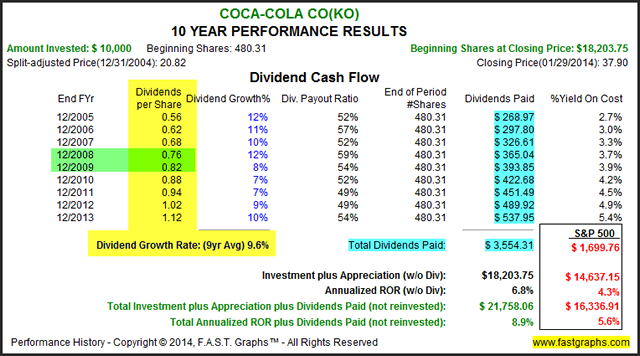

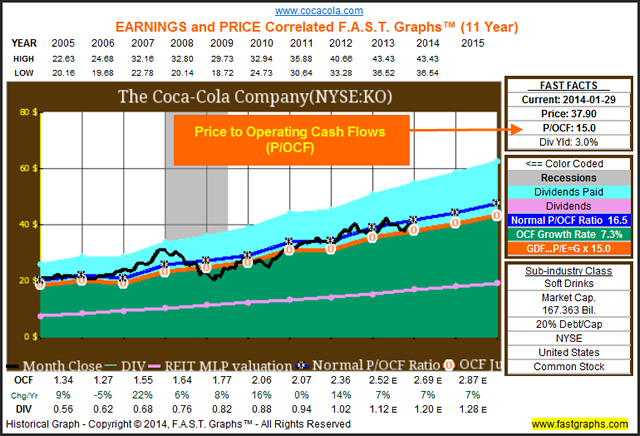

Coca-Cola: (KO)

The Coca-Cola Company operates as a beverage company. The company owns or licenses and markets approximately 500 nonalcoholic beverage brands, primarily sparkling beverages and also various still beverages, such as waters, enhanced waters, juices and juice drinks, ready-to-drink teas and coffees, and energy and sports drinks.

Associated 10-year Performance Report – Focus on Dividends

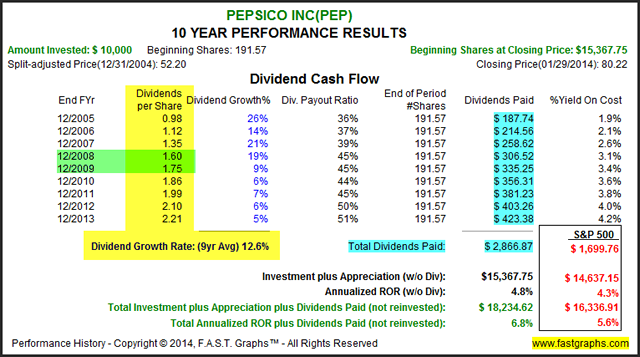

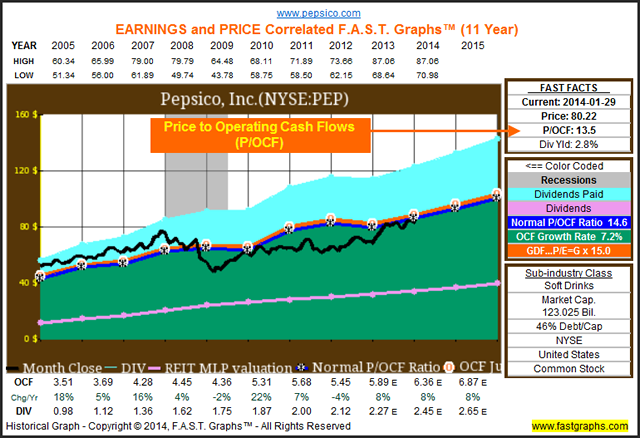

PepsiCo, Inc.: (PEP)

PepsiCo, Inc. operates as a food and beverage company worldwide. Through its operations, authorized bottlers, contract manufacturers and other partners, the company makes, markets, sells, and distributes various foods and beverages, serving customers and consumers in approximately 200 countries and territories.

Associated 10-year Performance Report – Focus on Dividends

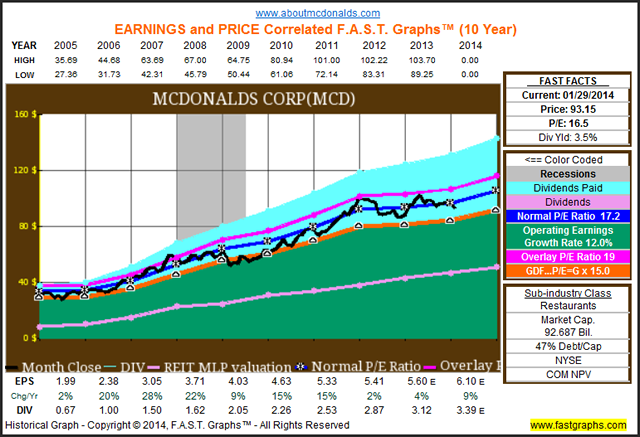

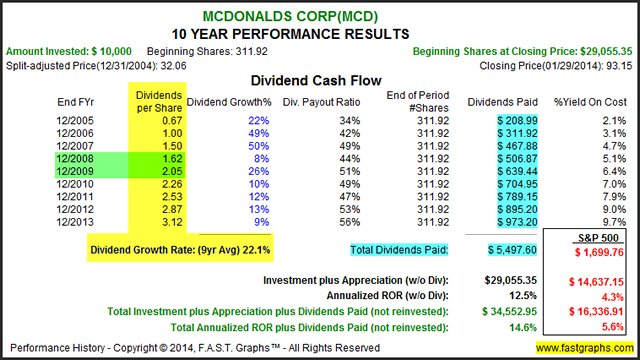

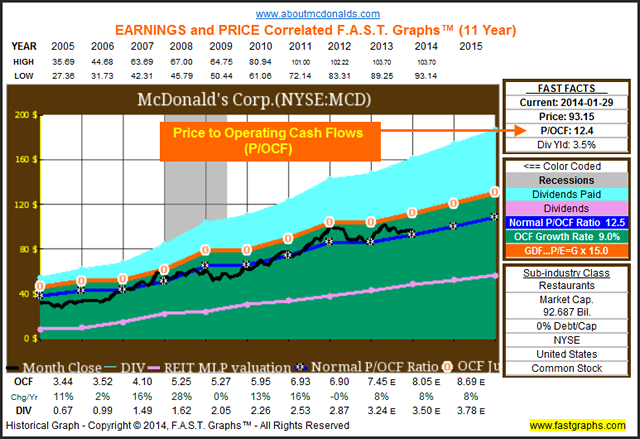

McDonald’s Corporation: (MCD)

McDonald’s Corporation franchises and operates McDonald’s restaurants in the restaurant industry. The company’s restaurants serve a menu at various price points providing value in 119 countries worldwide.

Associated 10-year Performance Report – Focus on Dividends

Valuation Based on Operating Cash Flows

The F.A.S.T. Graphs™ Fundamentals Analyzer Software Tool is currently testing the launching of our new and improved version based on Standard & Poor’s Capital IQ’s recently launched global database. One of the many great benefits available from the new database is the addition of extensively more comprehensive estimates available for various fundamental metrics. Our current legacy database only provided estimates for operating earnings, which is quite common for most available databases. Therefore, our new version will include the option to evaluate stocks based on operating cash flows for C-Corps and reported FFO (funds from operations) on REITs, with two years of forward estimates.

Personally, I have always considered cash flows to be a vital and important fundamental to analyze in addition to, and in conjunction with, analyzing any given company’s earnings and price relationship. However, many decades of researching and analyzing common stocks have convinced me that the correlation of price to operating earnings represents the most valid valuation measurement for most companies. On the other hand, as I previously pointed out in this article, there are exceptions to every rule.

Therefore, since I was researching the above quality premium blue-chip dividend paying stalwarts for this article, I thought it would be interesting to review them based on my new toy utilizing earnings and operating cash flows. What I discovered was astonishing. The correlation between stock price and operating cash flows for this quality equity class is profound. To be clear, the operating earnings and price relationship for most companies remains the standard, at least in my opinion. However, the price and operating cash flow correlation on these quality premium dividend paying stocks is simply too remarkable to dismiss.

Consequently, I offer the four featured examples presented above based on stock price correlated to operating cash flows as a sneak preview. Clearly, and for reasons that I am not yet certain about, valuing these businesses based on operating cash flows appears to be a valid option. For disclosure, I am long all four of the following companies. However, in the past I was unwilling to invest in them when their prices were above their earnings justified valuations. Therefore, it took the Great Recession of 2008 to induce me to invest. Perhaps I may alter my views after discovering the significant correlation that this additional research has uncovered. Maybe this old dog can learn a few new tricks after all.

Procter & Gamble: Fair Value Based on Price to Cash Flow

Coca-Cola Co: Fair Value Based on Price to Cash Flow

PepsiCo: Fair Value Based on Price to Cash Flow

McDonald’s: Fair Value Based on Price to Cash Flow

Summary and Conclusions

Even after the stock markets’ run up over the past few years, I believe there are still attractive individual stocks (businesses) available. Even though many of the dividend growth stock candidates presented in this article are trading at or near all-time highs based on stock price, that does not in itself suggest that they do not remain sound long-term investments. The majority of the companies in this article are also generating all-time high levels of earnings and dividends. Consequently, their valuations are not necessarily at all-time highs, only their stock prices.

Finally, this article is not intended to provide a comprehensive list of all potential dividend growth stocks that are fairly valued. In my article next in this series, part 5, I will review dividend paying stocks with higher yields suggested for investors seeking maximum current dividend income. Therefore, part 5 will include a few fairly valued select REITs, MLPs, utility stocks and other miscellaneous candidates with a focus on higher current yield.

Disclosure: Long CL, CLX, EMR, GIS, JNJ, KO, MCD, PEP, PG, BAX, CSCO, CVX, DPS, DRI, GE, MSFT, RSG, TGT, WMT at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs