“There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is a part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present.”

John Kenneth Galbraith, 1908-2006 Professor, Author & Diplomat

Recipient of the Medal of Freedom (1946) and the Presidential Medal of Freedom (2000)

John Kenneth Galbraith was a force in the fields of politics and economics. He wrote into his 90s, with many of his 48 books covering economic history, a subject we find to be the oft forgotten friend of investors. His work made it clear that economics is not a hard science which can be reduced to simple trustworthy mathematical equations. Galbraith constantly challenged the “conventional wisdom”, and in fact pioneered the term. Galbraith came to dismiss the then, and still now, common notion that individuals and markets always act rationally.

Is the current market rational? Last year the S&P 500 Index total return exceeded the total return of long-term Treasuries by an astounding 45%, the widest spread since 1958. Are the future earnings of U.S. companies really worth some 30% more than a year ago…or more precisely is the completely rational perception of those earnings rightly 30% higher today than it was a year ago? Regardless of whether it was warranted or not, stocks soared into year-end, producing new all-time highs even as the Fed announced the “tapering” of its bond buying to “only” $75 billion per month (down from $85 billion per month during 2013 but still expanding the Fed’s balance sheet going forward)1. Investors were turned sanguine by the Fed’s parallel plan to keep short-term interest rates low for longer… interpreted to mean into 2016 or (as we would add) until their hand is forced by inflation or a currency crisis. In truth, lower interest rates really do justify higher asset prices…as long as interest rates remain low. Hence all this market action might be a rational response to Quantitative Easing (QE), but such a conclusion begs the question of what might come our way once QE is discontinued, and if QE/low rates can’t go on forever, was the associated asset price ascent ever really justified?

Rational or not, investors certainly adopted more risk during 2013 as all the following occurred:

- Bond mutual funds experienced their largest net outflow in history ($88 billion).

- U.S. equity mutual funds saw modest net positive inflows ($16.7 billion) for the first time in the last eight years.

- Gold’s 28% plunge was the sharpest since 1981 (despite the volatility of gold’s price, it is often viewed as a refuge from risk).

- Ever-hungry-for-yield-investors gobbled up a record-setting near $1 trillion new issuance of leveraged loans and high-yield bonds.

- Initial Public Offerings (IPOs) raised the most money since the dot-com pinnacle year of 2000 (currently more than 60% of newly listed companies lack profits…we remind investors that “hope is not a strategy”).

- Secondary offerings of stock ran at a torrid pace (over $160 billion - the most since at least 1995).

The above mentioned extensive share issuance warns of a complacent investment environment. We also point out that, despite the robust equity offerings, there has been an actual reduction in net shares outstanding, as corporations issue Fed-induced cheap debt at low interest rates and buy back stock. More debt and less equity is again another sign of complacency… CFOs are willing to up the risks of their enterprises.

Some treat share buybacks as if they are always and everywhere a good thing…they are not. Corporate managers who think about returning capital to shareholders are indeed well guided. However, unlike a dividend, a share buyback does not return capital equally. A share buyback only returns capital to those who wish to sell their shares. And here is the key point: if the shares are overvalued when repurchased, extra capital is returned to the sellers at the expense of all other shareholders. That’s right. Buybacks that happen when shares are overvalued destroy value for shareholders. How else could it be when you use perfectly good money to buy something that is too expensive? Alternatively, when savvy corporate leaders buy back their own shares at depressed prices, they increase value for shareholders at the expense of the sellers. Unfortunately, managements tend to buy back shares when flush with cash, and they are flush with cash when times are good, and when times are good shares become overvalued. Simply look at the above chart to see when buybacks peaked…near the stock market peak preceding the financial crisis. Hence, it is questionable whether stock buybacks have really created value over the long term for investors who have “stayed the course”. Consequently, it is the mark of a great manager who buys back shares when their share price is low and these are the companies Knightsbridge seeks. The U.S. stock market is at its highest point ever. Should no one be worried? Not necessarily.

All-time highs can be a regular occurrence for quite a while. Remember hearing for years that interest rates “are at all-time lows”? As strange as it seems to have “historic” events happening every day, this was actually true at each point in time, because the subsequently more extreme events that later rendered the aforementioned event un- historic were yet to occur. The fact that interest rates were at historic lows did not prevent them from going lower for another decade. All-time highs (or lows) do not in and of themselves portend a change in market direction or mean the end is nigh.

Should one worry about present market conditions? Yes.

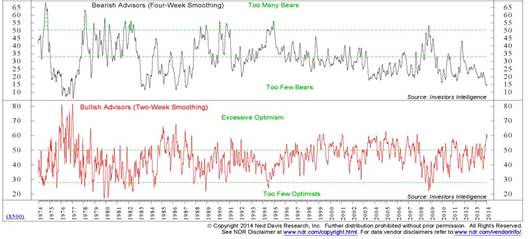

The “conventional wisdom” is that all is becoming well and so onward all ye investors, full steam ahead! Yes, economic conditions are improving, but economic success does not equal a rising stock market. Everyone is aware that China has been an economic juggernaut over the last several years. But not as many people are aware that their stock market has underperformed that of the U.S. over the last five years by some 95% (with China also lagging the U.S. over the last ten years). Stocks are discounting machines that look ahead, sometimes even around corners. The huge investment gains of 2013 already anticipated an improved 2014 landscape. We worry today’s market conditions are set to run afoul, buffeted on the winds of investor complacency into the shoals of disappointing mediocrity. Nonetheless, many are jumping on board the equity rocket ship, as the triumph of equities is expected to continue: the latest Barron’s survey reveals not a single Wall Street Strategist expects U.S. stocks to end 2014 in the red2. Unfortunately, past performance is not only no guarantee of future results, but it actually makes those future results more difficult to achieve. Like balloons, stock prices can venture quite far from intrinsic values into the sky, but eventually gravity tends to realign them with the Earth. Although it takes a crystal ball to accurately calculate the “true” intrinsic values of stocks, one can get an idea about this potential separation by looking at whether sentiment is exuberant or despondent. Witness the charts on the following page which speak to the ebullience of equity investors:

Incredibly, a record low 15% of investors surveyed by Investors Intelligence admit to being bearish (top panel – above). And investors are not simply neutral on stocks; the vast majority are bullish (bottom panel – above).

Investment newsletters are wildly bullish, recommending peak levels of exposure to stocks.

Shaded regions represent periods of U.S. recession

Source: Evergreen Virtual Advisor

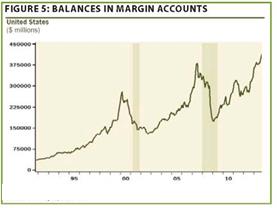

Accordingly, investors have put their money where their mouth is, borrowing the most ever to buy stocks on margin.

Investors are buying funds that bet on the market going higher while avoiding funds that do the opposite. There is five times as much investor money in bullish Rydex funds as there is in bearish Rydex funds.

Investment managers are all in, holding virtually no cash. Knightsbridge, however, elects to hold 13% cash in this environment, an amount which might well increase should equities climb higher.

We cannot help but recall the sage advice of Warren Buffett: “The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs3.”

Does all this investor enthusiasm mean stocks are overvalued? While this is unclear, at least one prominent commentator, our neighbor from across the street Bill Gross, CIO of PIMCO (the world’s largest bond manager) has recently stated that all assets seem bubbly and overvalued. With stocks at all-time highs, bonds having seen an epic bull market, and the real estate market bouncing strongly back, on the face it seems plausible. But what does that even mean ? Isn’t value inherently relative, and therefore isn’t something undervalued, almost by definition? Let’s explore this idea.

One conception of the “all assets are overvalued” idea, to which Mr. Gross is perhaps subscribing, is that assets are overvalued to what they should be or what they soon will be. This idea, at its heart, is really to say “interest rates won’t stay this low for very long”. Interest rates relate current money to future money. When rates are low, a dollar today won’t give you that much more ten years from now. To flip this around, it also says, the promise of a dollar ten years from now is still worth a good deal today. Hence, in a world with newly lowered interest rates, it makes perfect sense for all assets to receive newly raised values, in this new world, the higher prices are their fair values. Many conventional analyses (even some we have included in this letter) fail to recognize this possibility, of semi- permanently low rates and high asset prices. Price to sales ratios might indeed be far above their historical averages, but those other periods in history didn’t have 3% ten-year rates that justified a high ratio. To return to the idea that assets are overvalued in this framework, it is to say that the current low interest rates that (perhaps) justify these high prices won’t last. This is our best guess as to the worldview to which Mr. Gross is subscribing. Certainly we can all imagine a world in which interest rates return to their previous levels…but can you imagine a world in which interest rates stay at current levels for 20 years? Before you say it can’t happen, note that it has already happened…in Japan. A study of financial history reveals many patterns that repeat, but also reveals instances of regime changes where events cease to follow old patterns and instead move to a different tune for a significant period. As investors, we think it is important to remain open and sensitive to these possibilities, and not to be boxed into old ways of thinking if they become outmoded.

Another “all assets are overvalued” conception is that assets are uniformly overvalued, compared to…goods. In other words, future consumption is too expensive (overvalued) relative to current consumption. That is, after all, what assets really are, vehicles to turn current consumption into future consumption. Unfortunately, even if all assets are overpriced, and you can identify it (two big ifs), there is no clear prescription for action due to conflicting effects. One effect is that in knowing that future consumption is too expensive, you might try to shift your consumption forward, and consume more today. On the other hand, in knowing that your assets are unsustainably inflated, you’re aware that your future consumption won’t be as great as previously, so you might want to actually save more! Think about it: what would you do if I told you that next year I would take all your hundred dollar bills and turn them into ones. Would you save more because you’re going to have less in the future than you thought, or would you save less because you want to spend those hundred dollar bills today, because they’re still worth $100 if you spend them now. It would seem that one would want to avoid petty luxuries because of the overall diminishment in wealth, but shift whatever necessary purchases you could from the future to the present. That, and look for ways to produce future consumption (assets) that aren’t traditionally thought of as such. We have seen one prominent investment writer ponder the prospect of tree farms that don’t yield results for 30 some years.

Besides the question of how you protect yourself (much less use this mispricing to make money), what does an asset bubble do to society? In this respect it’s useful to review Galbraith’s concept of the “bezzle”. This is the dollar amount of undiscovered embezzlement, which has the curious effect of increasing the total amount of “psychic wealth” in society. The embezzler who has the ill-gotten funds can spend accordingly, and the unwitting victim still feels just as rich because she hasn’t discovered the shortfall yet. Society overestimates the amount of total value in the world by the amount of the bezzle.

This concept can be extended to asset mispricings in general and bubbles in particular. If you sold a 1985 Buick to your neighbor for $500,000, clearly, your neighbor has just lost about $499,000. That being said, he won’t realize, or feel this loss, until he tries to re- sell the car and discovers that it isn’t worth nearly what he paid. This is what happens when, say, we (as a society) greatly overvalue junk bonds, internet stocks, houses in Florida, or the mortgage obligations of construction workers. Later when prices adjust back to their real values, we experience the painful loss of this perceived wealth. Sometimes, these losses are so painful that we try to prevent them from happening at all by re-financing loans that can never be serviced in reality (Greece), getting the government, a.k.a. everyone, to suffer the losses (Government takeover of Fannie and Freddie that saved their respective bondholders), or lowering interest rates to raise asset prices (worldwide)4. Once the investing public realizes the assets have been overvalued, however, the adjustments must be made, otherwise the economic system will only work in fits and starts5. Instead of enduring the painful process of letting asset values adjust down to intrinsic values, it seems the Fed may instead be trying to keep asset values inflated until the underlying values catch up…hopefully it won’t be long.

But enough doom and gloom, whatever happens to asset prices, it is, after all, only accounting. The underlying wealth of the world is increasing, and the world of the future will indeed have more goods and services (a.k.a. wealth) than the world of the present. We at Knightsbridge are keeping a careful eye on both the accounting and the intrinsic to make sure that you get your fair share.

Very Truly Yours,

John G. Prichard, CFA

1 This $75 billion figure does not include the buying the Fed does to reinvest the proceeds of maturing bonds.

2 At the same time, strategists uniformly predict bonds to suffer losses from rising interest rates this year.

3 Incidentally, this is the favorite Buffetism of Howard Marks, famous investor and CIO of Oaktree.

4 Much like the other strategies for avoiding losses, this strategy doesn’t create value out of thin air. It simply gives to asset holders the future value that savers would have accrued from interest. Apparently if you take value from people who haven’t experienced it in their bank accounts yet they complain less.

5 One final insight: did your neighbor lose the $499,000 when he originally bought the car from you, or when he realized it was worth less? Either position can be argued but a lot can be said for the position that it was lost the moment the transaction was consummated. Similarly, the victims of Bernard Madoff’s fraud really only lost their initial investment, not the millions more that appeared on their fraudulent broker statements… those extra millions were never there to be lost in the first place.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management