Strong ETF Net Inflows for 2013

US-listed ETF1 net inflows totaled $185.5 billion in 2013, setting a new record. While the largest percentage of net inflows remained concentrated among a relatively small group of the 1521 US-listed ETFs, investors broadened their horizons more in 2013 than in previous years, as 312 ETFs had net inflows exceeding $100 million.

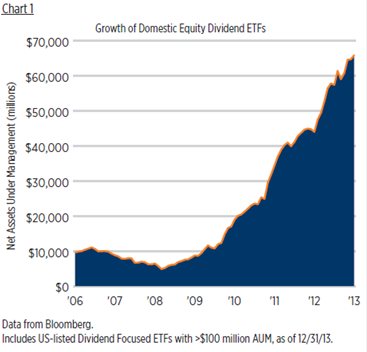

2013 was also a record-setting year for First Trust’s ETF complex. Net inflows for the 79 First Trust ETFs totaled $8.2 billion in 2013, with 24 ETFs exceeding $100 million in net inflows, increasing ETF assets under management (AUM) at First Trust to $19.7 billion. As of 12/31/13, First Trust was the 9th largest sponsor of US-listed ETFs. Strong Inflows Continued for Equity Income ETFs Equity income remained a prominent theme for ETF net inflows in 2013, continuing a trend that began in March of 2009. From 3/31/09 to 12/31/13, assets in domestic equity income ETFs grew from $5 billion to over $65 billion.

Generally speaking, investors in these ETFs were rewarded with solid returns during that stretch. However, looking ahead many equity income ETFs with overweight allocations to non-cyclical sectors may face headwinds in 2014, in our opinion, especially if mid- and long-term interest rates continue to trend higher. Investors with a preference for dividend-paying stocks, but concerns about rising interest rates, may consider reallocating assets from ETFs focused on high dividend yielding stocks to ETFs focused on dividend growth stocks.

Although equity income ETFs apply a variety of different strategies for constructing their respective portfolios, one common characteristic currently shared by many of these funds is a sector allocation that tends to overweight relatively high dividend yielding sectors with below average dividend growth (such as the utilities and consumer staples sectors), and underweight sectors with lower dividend yields but greater opportunity for dividend growth potential (such as the technology and financial sectors). As we discussed in last July’s edition of “Inside First Trust ETFs,” we believe that stocks with growing dividends may perform better than those lacking dividend growth during periods of rising interest rates. Indeed, this was the case in 2013, as the 10 year US Treasury yield increased by 137 basis points from 5/2/13-9/5/13. During that period, returns for the S&P 500 Utilities and Consumer Staples Sectors, were -9.4% and -2.8%, respectively, while returns for the S&P 500 Information Technology and Financial Sectors were +5.2% and +6.7%, respectively.

If interest rates continue trending higher in 2014 (First Trust economists forecast a 3.65% 10-year US Treasury yield by year-end), it may be prudent to consider repositioning equity income ETF assets to seek dividend growth. One ETF that may be considered by investors looking to increase exposure to dividend-paying technology companies is the First Trust NASDAQ Technology Dividend Index Fund (TDIV). For those seeking increased exposure to the financial sector, the First Trust NASDAQ® ABA Community Bank Index Fund (QABA) invests in a portfolio of community banks.

We believe this segment of the financial sector is particularly well positioned to benefit if the yield curve steepens in 2014. Finally, investors looking for a more diversified portfolio of stocks that have consistently increased dividends in the past, and may be well positioned to increase dividends in the future, may consider the First Trust NASDAQ Rising Dividend Achievers ETF (RDVY).

“Smart Beta”

In our opinion, one of the most interesting developments in the ETF industry in 2013 was the growing acceptance of ETFs tracking alternative strategies for selecting and weighting stocks, often labeled as “smart beta” strategies by ETF industry pundits. Of course, not all smart beta strategies are equally smart, and many investors may decide to wait for some of the newcomers to develop longer-term track records before considering them.

Are Commodities Due for a Rebound?

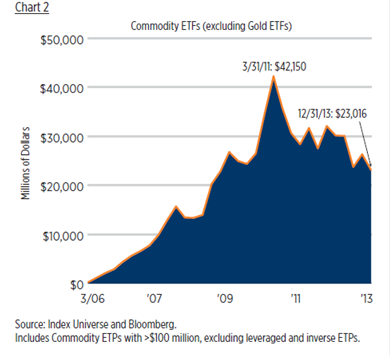

Assets in commodity ETFs declined in 2013, the first calendar year

since the introduction of the first gold ETF in 2004, with net outflows totaling $30.1 billion. The majority of these outflows came from gold ETFs, which collectively accounted for over $28 billion in net outflows. However, excluding gold ETFs, assets in other commodity ETFs have actually been trending lower since asset levels peaked in March of 2011 (See Chart 2).

Interestingly, 2013 marked the first instance since the inception of the DJ-UBS Commodity Total Return Index (on 12/31/1990) in which index returns were negative for three consecutive calendar years (2011-2013). In fact, the only other instance in which index returns were negative for two consecutive calendar years was 1997-1998.

Following that stretch, index returns rebounded sharply in 1999 (+24.3%) and 2000 (+31.8%). While past recoveries in commodity prices do not imply a similar recovery this year, we believe commodities may be due for a rebound in 2014, particularly if US economic growth accelerates (First Trust economists forecast 3.0% real GDP growth for 2014), and the nascent European economic recovery continues to gain stronger footing. We believe this actively-managed ETF offers several distinct benefits versus other broad-based commodity index ETFs.

Looking back at 2013—a year during which the ETF industry celebrated its 20th anniversary—it’s striking how much ETFs have evolved. Gone are the days that investors can safely assume that a given ETF tracks a traditional market-cap weighted benchmark index. Today, ETFs invest in a variety of asset classes, utilizing an assortment of strategies, involving both passive and active management. Understanding the most important differences between various ETFs now requires more work than in previous years. However, the reward for portfolio managers and financial advisors that are willing to spend more time to evaluate their options is a whole new set of tools with which to build better client portfolios.

© First Trust Advisors