Stocks 2014: Investing for Growth - The Power and Protection of High Compounding Earnings Growth

As I become more mature (translate: gotten older), my investment philosophy has slowly evolved into a more conservative posture. When I was a younger investor I felt I had time on my side, and therefore, was willing to take on greater risk as long as I believed that greater rewards could follow. In other words, if I made a mistake by investing in an aggressive and more risky growth stock that went badly, I felt I had adequate time to overcome or recover my losses. Consequently, as a younger investor I relished a good growth stock.

At this point I think it’s important to point out that my currently more conservative attitude towards investing in more conservative dividend paying stocks is not driven by fear. Thankfully, my long experience as a fundamental stock investor has taught me not to be afraid of stock market volatility. Instead, I feel I’m simply being a realist for a couple of important reasons. First of all, I believe that time in the market is more important than timing. But unfortunately, as a more mature individual I must acknowledge the reality that I do not have the time luxury I once did as a younger man. Second, I now have less of the need to build wealth coupled with a greater need and requirement for current income.

Consequently, my investment philosophy has morphed from pure growth into a growth and dividend income strategy. On the other hand, I have not completely forsaken my desire for capital appreciation because I also understand the reality of inflation. Therefore, for the most part I still look for above-average high quality growing blue-chip companies that can give me both attractive capital appreciation and dividend income growth. This is where the bulk of my investing has been in recent years, and in future articles in this series I will cover various categories of dividend growth stocks.

On the other hand, even today I still appreciate the powerful returns that a good growth stock offers. Therefore, I still allocate a portion of my investments into pure growth stocks. However, growth stock investing represents only a small part of my portfolio today. Because, as I hope to illustrate in this, part 2 of this series, which is focused primarily on pure unadulterated growth stocks, even a small allocation of growth stocks can produce game changing future returns. With these thoughts in mind, I believe that all common stock investors, regardless of their age or status, might be well served to sprinkle in a bit of growth. And of course, diversification among the growth portion can serve to mitigate some of the associated risks.

Growth Stocks Defined

Before I get too deep into this discussion on growth stocks, I feel it’s important that the reader understands my definition of what a growth stock is. The term "growth stock” suffers, as many other investing terms do, from what is often a cavalier or loose definition of what it truly is. Many investors and writers think of growth stocks as companies with high P/E ratios or high betas. However, neither of those characteristics are always representative of a true growth stock, at least by my definition.

In order for me to consider a company a growth stock, it must possess a record of consistent earnings growth exceeding 15% a year or better. When I think of a growth stock, my focus is on the growth of the business. Because, as a long-term investor I believe I am buying the future earnings power of the company under consideration. Consequently, the faster a company grows its earnings, the more future earnings I can expect to receive. But even more importantly, thanks to the power of compounding, I expect to receive significantly greater earnings sooner from a true growth stock than I can from an average growing business.

Moreover, since I understand that the market is always capitalizing earnings, the more earnings a business delivers me, the more future capital appreciation I can expect to receive. Therefore, a true growth stock that delivers above-average earnings growth can actually be less risky than many investors believe them to be. Of course, this is only true if the company delivers the faster earnings growth that I anticipate. But when it does, I can expect a decent return even if the company’s future P/E ratio is less than I paid today. I refer to this as thepower and protection of high compounding earnings growth.

The Power and Protection of High Compounding Earnings Growth

The review of a simple compounding table illustrates my points better than words. What actually happens as a result of faster earnings growth is that it shortens the time it takes to double earnings. Therefore, the following compounding table illustrates how an original $1.00 worth of earnings that are purchased today will double more often over a 10-year timeframe when earnings growth is higher. The tipping point becomes rather dramatic at 15% per annum or better.

People that do not understand the powerful force of compounding will often mistakenly assume that a 20% growth rate will produce twice as much future earnings as a 10% growth rate. However, compounding is more about geometry than it is simple mathematics. From the table below, note that $1.00 invested today that grows by 10% per annum does not double until the 8thyear. In contrast, $1.00 invested at 20% doubles in the 4thyear, and then again in the 8thyear. Therefore, doubling the growth rate from 10% to 20% doubles the number of doubles on your earnings in 10 years. This compounding effect is even more dramatic when you look at what happens with various growth rates by the 10thyear.

Increase the growth rate to 30%, and that first dollar will double 3 times instead of only once. Consequently, it is easy to understand why Albert Einstein said: “Compound interest is the eighthwonder of the world. He who understands it, earns it … he who doesn't … pays it.” Compounding is the power; and the higher level of earnings it produces is the protection that high-growth stocks can provide. However, earning high rates of earnings growth over an extended period of time is quite difficult. Few companies are capable of achieving high earnings growth, and therein resides the risk of growth stock investing.

Growth Stocks Are Not Your Grandfather’s Buick

At this point, I think it’s important to point out that investing in growth stocks is entirely different than investing in blue-chip dividend paying stocks. Growth stock investing along with greater profit potential also provides greater challenges and risks than investing in lower growth alternatives. For example, although investing at fair value (which I consider to be when the P/E ratio is equal to or lower than the earnings growth rate) will provide strong returns at reasonable levels of risk, assuming of course that the earnings growth materializes.

On the other hand, due to the power of compounding discussed above, you can actually overpay for a growth stock, and still achieve above-average long-term returns. However, by doing this you do assume a high level of short-term risk, even though long-term returns might still prove exceptional. But, and this is a big but, few investors are capable of enduring the short-term risk when and if it does manifest.

More simply stated, many investors will sell if the price of the stock falls dramatically even when earnings remain strong. The following 2 examples looked at through the lens of theF.A.S.T. Graphs™earnings and price correlated research tool will help illustrate my points through both a historical and a potential future perspective. Note that neither of the following 2 examples are offered as buy recommendations, instead they represent illustrative examples of my points stated above.

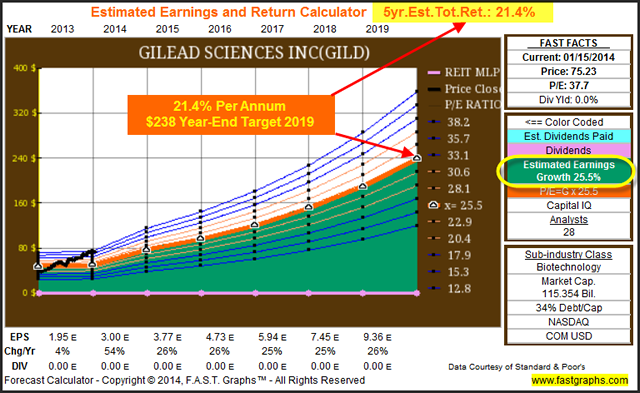

Gilead Sciences, Inc. (GILD)

Gilead Sciences, Inc., a biopharmaceutical company, that discovers, develops, and commercializes human therapeutics for the treatment of life threatening diseases in North America, Europe, and Asia. Based on the following 7 calendar year graph, note that the company’s stock price was technically overvalued at the beginning of 2008. The company’s P/E ratio at that time was approximately 26.5 and earnings growth was 19.4%. In other words, the company’s P/E ratio at purchase was higher than its subsequent earnings growth rate achievement.

Additionally, the reader should note that the current valuation is also high with a current P/E ratio of 37.7. I think we can only assume that this is a function of the 54% estimated earnings growth rate for 2014, and as I will show in a moment, the consensus five-year estimated growth rate of 25.5%. But the more important reason that I chose this example was to illustrate the effect of compounding earnings growth. (Note that operating earnings per share have nearly doubled from $1.09 in 2008 to $1.95 by 2013 and are expected to be nearly triple to $3.00 per share by fiscal year-end 2014).

The performance results associated with the above graph provides the first evidence that you can overpay for a high-growth stock and still earn high returns on your investment. When you consider that Gilead generated a total return of over 21% over a time period that included the Great Recession, the power and protection of higher earnings growth becomes evident.

The notion that you can overpay for a high-growth stock and still potentially earn exceptional returns is further supported by the following Estimated Earnings and Return Calculator, or what I like to call the earnings forecasting graph. The consensus of 28 analysts reporting to Capital IQ, expect Gilead to grow earnings by over 25% per annum for the next 5 years. However, based on my fair value formula for growth stocks of a P/E ratio equal to earnings growth rate, would suggest that Gilead is only technically worth approximately $55 per share (P/E ratio 25) currently.

Nevertheless, if the company does achieve this rate of earnings growth, and even if the future P/E ratio by year-end 2019 would fall to 25.5 from its current P/E ratio of 37.7, the five-year estimated total return of 21.4% would still mathematically indicate quite acceptable results. Consequently, the short-term risk I previously mentioned would be the possibility that Gilead’s stock price could fall by approximately a third to the mid 50s before rising to the estimated fair value of $238 by year-end 2019. Once again, all this is predicated on the company achieving its earnings growth target and rational cooperation from Mr. Market.

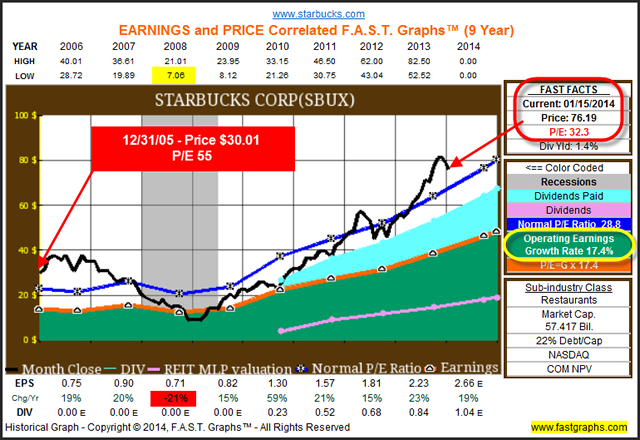

Starbucks Corp. (SBUX)

Starbucks Corporation engages in roasting, marketing, and retailing specialty coffee worldwide. The company operates in approximately 62 countries. I offer it as an example illustrating how you can overpay for a great growth stock and still earn above-average returns.

The following Earnings and Price Correlated Graphs for Starbucks Corp. are offered to illustrate how, thanks to the power of compounding earnings growth, long-term shareholders of Starbucks could not have overpaid for the stock, even when the price was dramatically overvalued. This once again illustrates the protection aspect of a high-growth stock that I discussed previously. On the other hand, and to be fair, I doubt few investors could have held the stock for 15 years considering all the peaks and valleys that they would have needed to ride out. Yet, for those investors that did, the long-term rewards were clearly quite strong with share price rising from $6.06 on December 31, 1999 to $76.19 by January 15, 2014.

In order to drive this point home even farther, I offer the following Earnings and Price Correlated Graph on Starbucks Corp. starting in 2006. At the beginning of 2006, Starbucks was trading at a P/E ratio of approximately 55 and a price of $30.01 per share. The short-term risk was clearly severe as stock price fell to a low of $7.06 per share in 2008 due to the converging factors of excessive overvaluation, followed by a 21% drop in earnings caused by the Great Recession.

However, earnings growth soon recovered to its more typical above-average growth rate and stock price responded. Consequently, we once again see Starbucks’ stock price overvalued with a current P/E ratio of 32.

Clearly, beginning overvaluation and the Great Recession took its toll, at least over the short run. Nevertheless, long-term Starbucks’ shareholders still received an acceptable rate of return of 12.7% per annum (note the initiation of a dividend in September 2010-the pink line and light blue shaded area on the graph) in contrast to the S&P 500’s total return of only 6.2%. My point being that you can overpay for a great growth stock and still earn acceptable rates of return. To me this is a vivid example of the power and protection of a high growth stock.

When the Risk of Investing in a Growth Stock Becomes Too High

Even though I have thus far argued that you can overpay for a high growth stock and still do reasonably well, there are limits to everything. Therefore, I offer the following two examples to illustrate how even great growth stories can become too overvalued and therefore too risky to invest in.

Netflix Inc. (NFLX)

Netflix, Inc. operates as an Internet television network. The company’s network has approximately 33 million members in approximately 40 countries enjoying approximately 1 billion hours of TV shows and movies per month, including original series. However, the question is; does Netflix’s earnings support its lofty valuation?

The following Earnings and Price Correlated Graph on Netflix vividly illustrates the risk and rewards of investing in high-growth stocks. Both volatility and overvaluation can be extreme at times, especially when a high-growth stock is popular. First, we see how extreme overvaluation in 2011 led to an unacceptable collapse in stock price by the 3rdquarter of 2012. Netflix fell from a high price of approximately $305 at its peak in 2011 to just under $53 by its low in 2012. But more importantly, I feel that that price action was justified based on the value of its earnings.

On the other hand, since Netflix’s stock price bottomed in 2012 the results have been nothing short of extraordinary. At its peak, Netflix’s stock price surpassed its previous high, and continues to surpass that previous high today. However, with a current P/E ratio north of 270, caution should be obvious. It should be clear and apparent that Netflix’s current earnings do not adequately support such a lofty valuation.

Next, let’s take a look at Netflix’s expected future earnings power and see if we find any justification for today’s high valuation there. The consensus estimates of 24 analysts reporting to Capital IQ expect Netflix to grow earnings over the next 5 years at the extraordinarily high rate of 33.1%. That is truly a phenomenally high rate of compounding earnings growth, if Netflix is truly capable of meeting those expectations. But more importantly, that would only support a 2019 year-end stock value of approximately $458 a share based on the P/E ratio equal to earnings growth rate rule.

Interestingly, that high rate of earnings growth would imply a positive annual rate of return of 5.2%. However, the question that should be asked is does that rate of return justify the potential risks of investing in Netflix at today’s lofty levels? I think not, and if history is any guide at all, shareholders of Netflix could be in for another very rude awakening, at least over the shorter run.

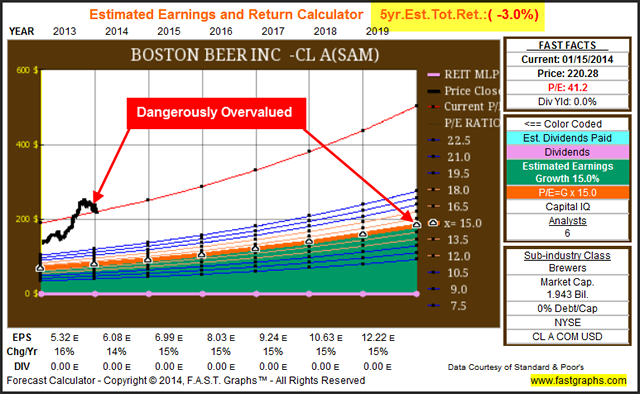

Boston Beer Inc. (SAM)

The Boston Beer Company, Inc. operates as a craft brewer in the United States, and represents a classic example of a high-growth stock. Since the beginning of 2004, Boston Beer grew operating earnings at over 21% per annum, and for the most part quite consistently. Furthermore, one reason I chose this example is because price tracked and correlated almost perfectly to operating earnings (the orange line) until the beginning of 2013. However, from then until now, the stock price went on a parabolic advance for no specific reason or justification that I can see, other than investor sentiment.

With the current P/E ratio above 41, I see little investment merit in owning the stock at such a lofty valuation. A quick glance at the monthly closing stock price appears to be indicating that I might not be the only one that sees potential trouble brewing (no pun intended) for future short-term stock performance stress. As consistent as Boston Beer’s earnings record has been, current valuation seems surely ahead of itself.

Given that the consensus of 6 analysts reporting to Capital IQ expect Boston Beer to grow earnings at 15% per annum over the next 5 years, that growth rate does not support current price, at least in my opinion. With valuation this high, if Boston Beer’s stock price followed the P/E ratio equals growth rate rule, then long-term investors could experience an annual loss of 3% per annum out to 2019. Yes, you can moderately overpay for a great growth stock as I suggested earlier, but there are limits. Personally, I believe that Boston Beer’s stock price currently exceeds those limits.

Growth Stock Research Candidates - Something for Everyone

What follows next is a listing of 80 high-growth stock research candidates that appear reasonably valued, or close to it, based on estimates of future growth. In order to compile this list, I scanned numerous indices to include the Fortune 500, the S&P 500, the S&P 400 Mid-cap, the S&P 600 Small-cap, the NASDAQ 100, and other miscellaneous sources. In addition to estimated future earnings growth above 15%, I placed a high premium on consistency of historical above-average earnings growth as well. Additionally, I looked for companies with track records of above-average earnings growth for at least the past 5 years, although I included a few select exceptions onto the list. I did all of this by hand, and reviewed each candidate individually via the F.A.S.T. Graphs™Fundamentals Analyzer Software Tool.

To a great extent, these selections are arbitrary and based on my own views about what constitutes a high-quality growth stock. Moreover, I cannot attest to the fact that each of these will be great future investments, or that they will all achieve the growth rate estimates expected. Therefore,these are not all buy recommendations. Instead, I offer them as a list of potential high-growth companies that appear fairly valued today, and therefore worthy of digging deeper into. I will leave it up to the individual investor to pick and choose based on each individual’s specific and unique goals, objectives and beliefs. On the other hand, I do believe there are a lot of excellent opportunities residing on these lists.

Moreover, I feel that this list contains candidates that are comprised of companies with various levels of quality and risk. Consequently, I offer the list in order of cap-size and expected growth rates from highest to lowest. After each segment I offer one or two expanded examples of companies that appeared especially attractive to me personally. Two additional high growth expanded examples can be found in part 1 of this seriesfound here. But that does not imply that all of them are sure to be great long-term investments. On the other hand, I do believe they are all worthy of further scrutiny and consideration.

For the sake of conciseness, I will let the Earnings and Price Correlated F.A.S.T. Graphs™on each company illustrate the value I see on each. Furthermore, I believe the true benefit of this exercise is through the careful scrutiny and analysis of each respective graph. For those not experienced in the utilization of the F.A.S.T. Graphs™research tool, I providethis link to my blogas a tutorial.

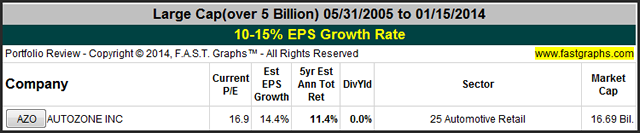

Large Cap (over 5 Billion) 10-15% EPS Growth Rate

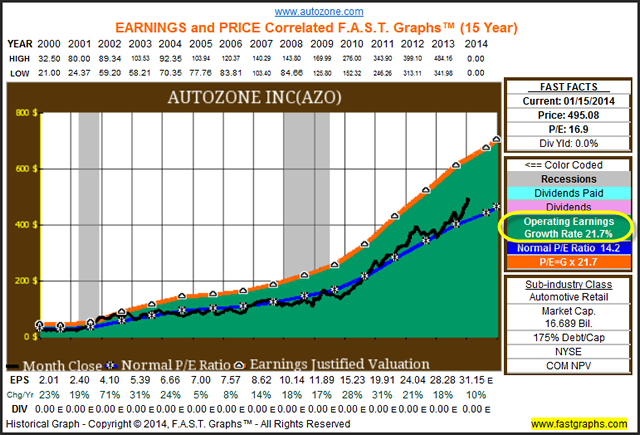

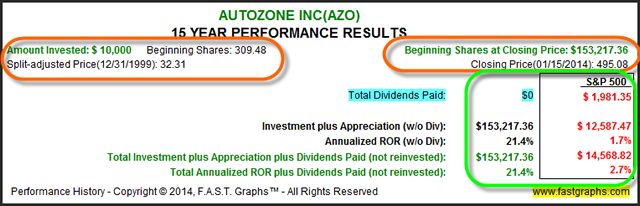

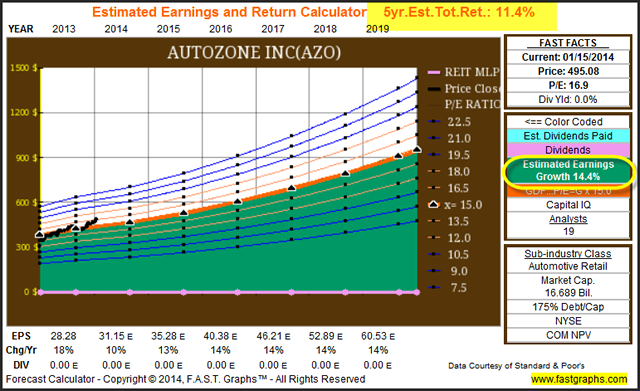

AutoZone Inc (AZO)

AutoZone, Inc. retails and distributes automotive replacement parts and accessories in the United States. As of August 31, 2013, the company operated 4,836 stores in the United States, including Puerto Rico, 362 in Mexico, and 3 in Brazil.

Large Cap (Over 5 Billion) 15-20% EPS Growth Rate

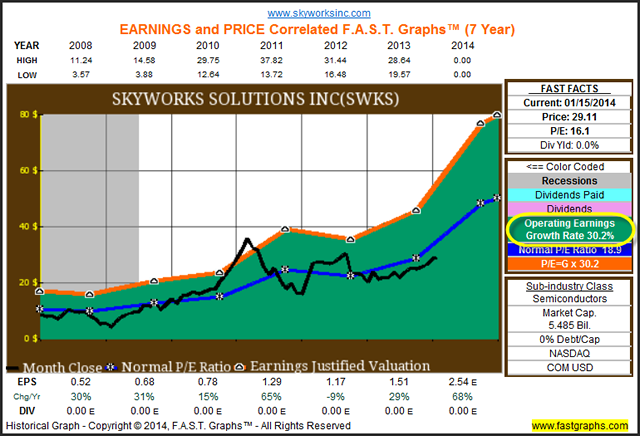

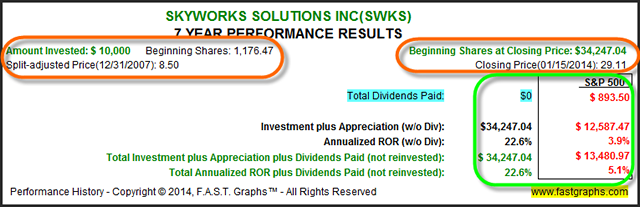

Skyworks Solutions Inc (SWKS)

Skyworks Solutions, Inc., together with its subsidiaries, provides analog semiconductors worldwide. The company supports automotive, broadband, cellular infrastructure, energy management, GPS, industrial, medical, military, wireless networking, smartphone and tablet applications.

Bed Bath & Beyond Inc (BBBY)

Bed Bath & Beyond Inc. operates a chain of retail stores under the Bed Bath & Beyond (BBB), Christmas Tree Shops or and That! (collectively, ‘CTS’), Harmon or Harmon Face Values (collectively, ‘Harmon’), buybuy BABY, and World Market or Cost Plus World Market (collectively, ‘World Market’)names.

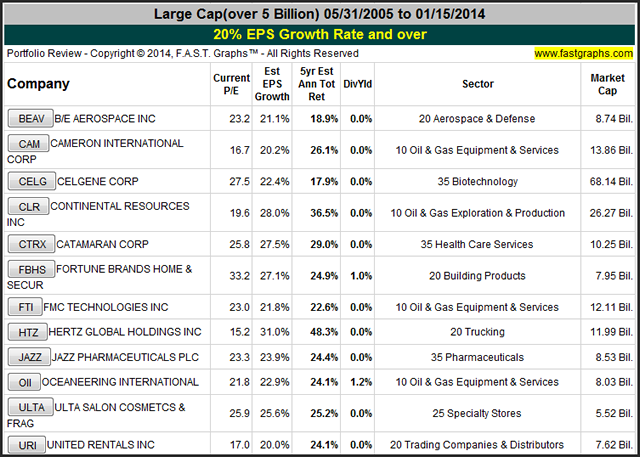

Large Cap (over 5 Billion) 20% EPS Growth Rate and Over

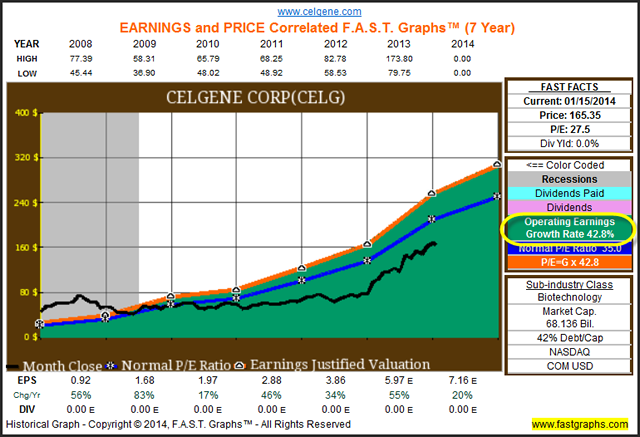

Celgene Corp (CELG)

Celgene Corporation, a biopharmaceutical company, engages in the discovery, development, and commercialization of therapies designed to treat cancer and immune-inflammatory related diseases.

Continental Resources Inc (CLR)

Continental Resources, Inc. operates as an independent crude oil and natural gas exploration and production company with properties in the North, South, and East regions of the United States.

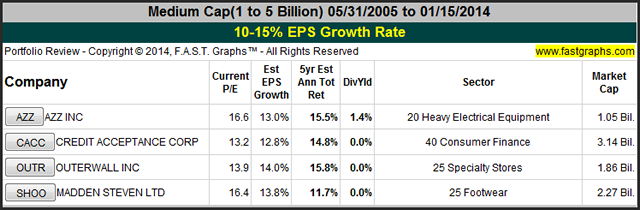

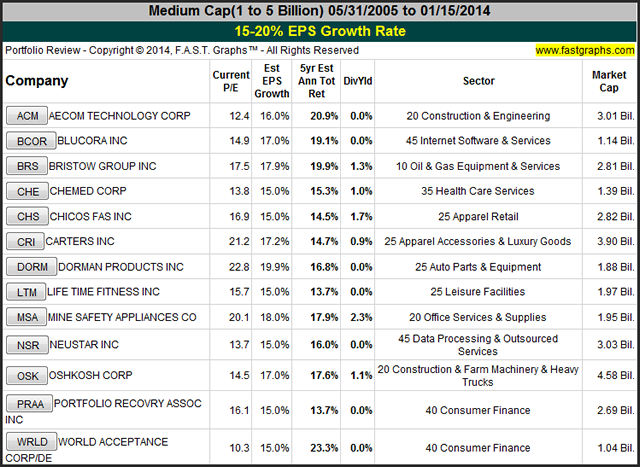

Medium Cap (2 to 5 Billion) 10-15% EPS Growth Rate

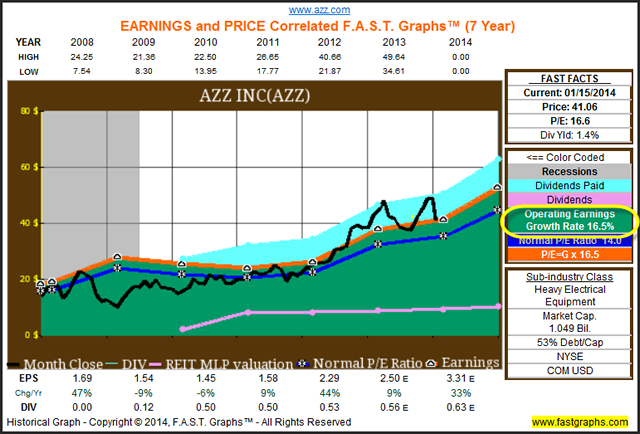

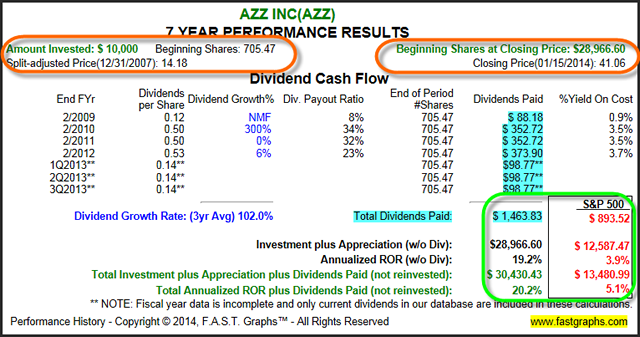

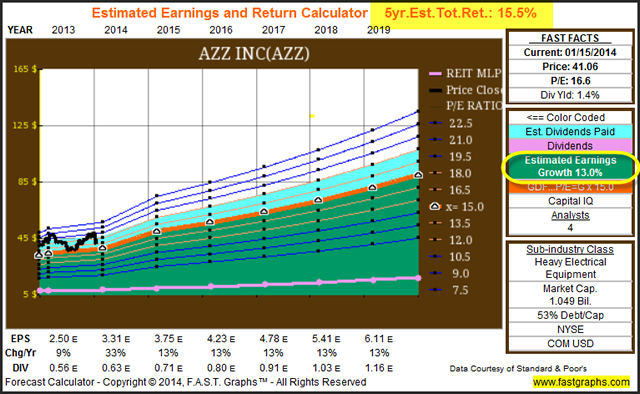

AZZ Inc (AZZ)

AZZ Incorporated manufactures electrical equipment and components, serving the power generation, transmission and distribution, and the general industrial markets. The company also provides hot dip galvanizing services to the North American steel fabrication market.

Medium Cap (1 to 5 Billion) 15-20% EPS Growth Rate

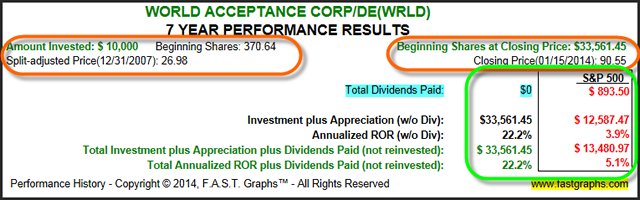

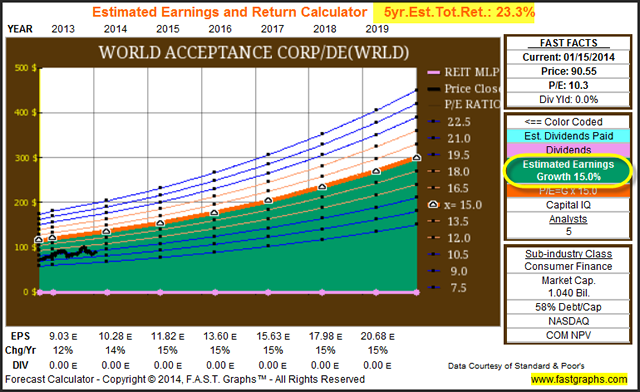

World Acceptance Corporation (WRLD)

World Acceptance Corporation engages in the small loan consumer finance business, offering short-term small loans, medium-term larger loans, related credit insurance, and ancillary products and services to individuals.

Carter’s Inc (CRI)

Carter’s, Inc. designs, sources, and markets branded apparel for babies and young children in the United States (U.S.). The company offers its products under the Carter’s, Child of Mine, Just One You, Precious Firsts, OshKosh, and other brands.

Medium Cap (1 to 5 Billion) 20% EPS Growth Rate And Over

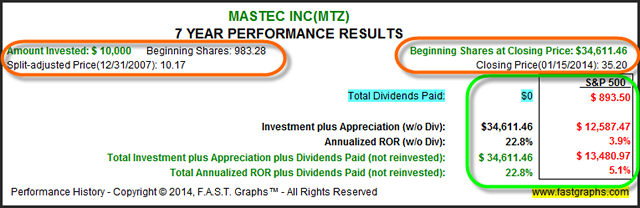

MasTec Inc (MTZ)

MasTec, Inc. operates as an infrastructure construction company in North America.

Small Cap (Up To 1 Billion) 15-20% EPS Growth Rate

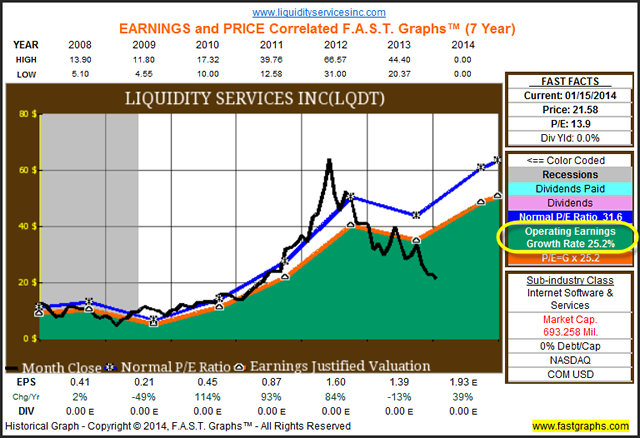

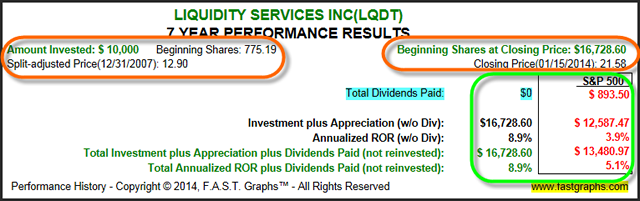

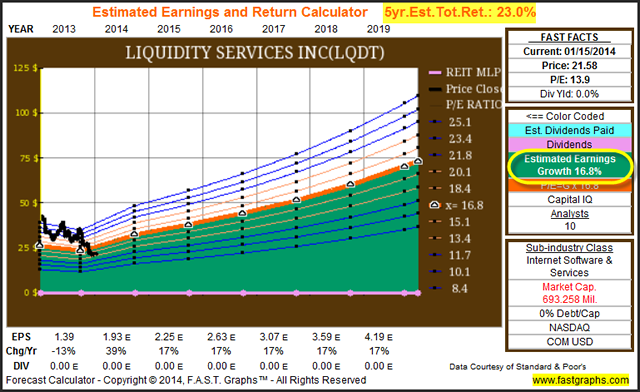

Liquidity Services Inc (LQDT)

Liquidity Services, Inc. operates various online auction marketplaces for surplus and salvage assets. The company enables buyers and sellers to transact in an online auction environment.

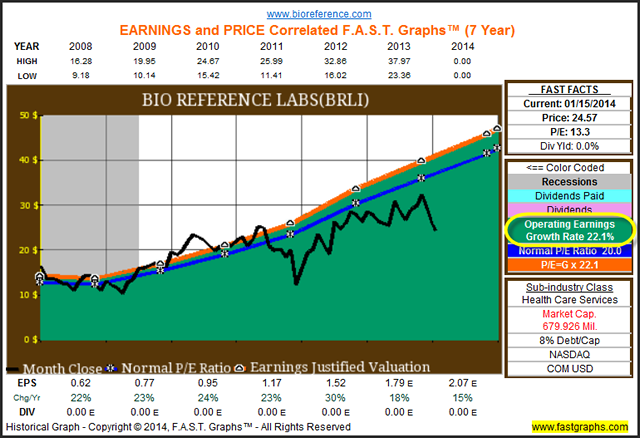

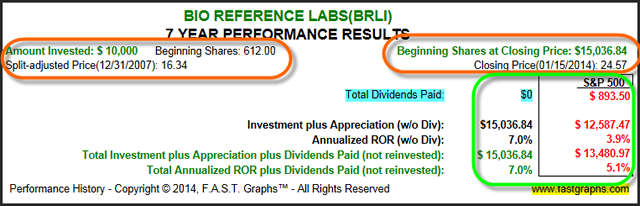

Bio-Reference Laboratories Inc (BRLI)

Bio-Reference Laboratories, Inc., a clinical testing laboratory, offers testing, information and related services to physician offices, clinics, hospitals, employers and governmental units.

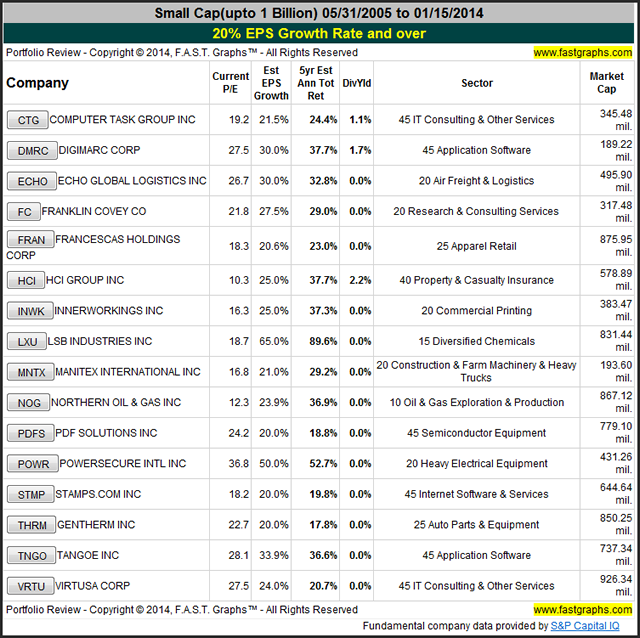

Small Cap (Up to 1 Billion) 20% EPS Growth Rate and Over

Computer Task Group, Incorporated (CTG)

Computer Task Group, Incorporated operates as an information technology (IT) solutions and staffing services Company in North America and Europe.

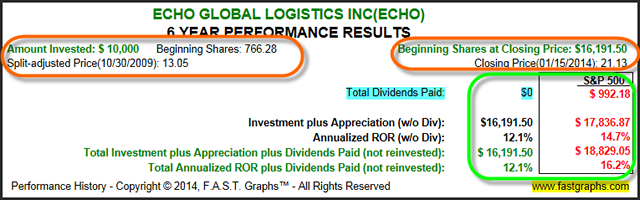

Echo Global Logistics, Inc (ECHO)

Echo Global Logistics, Inc. provides technology-enabled transportation and supply chain management solutions. The company utilizes a proprietary technology platform to compile and analyze data from its multi-modal network of transportation providers to satisfy the transportation and logistics needs of approximately 28,500 clients.

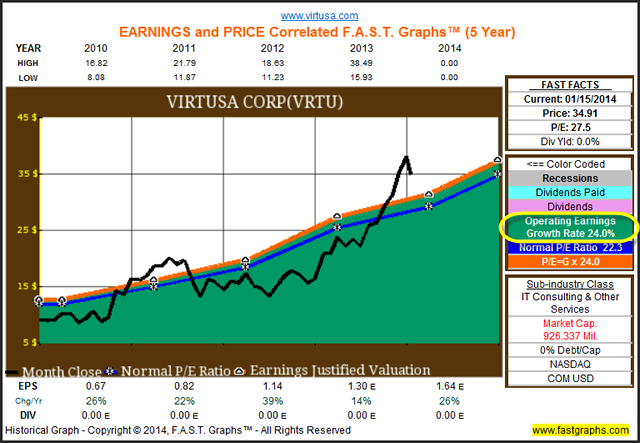

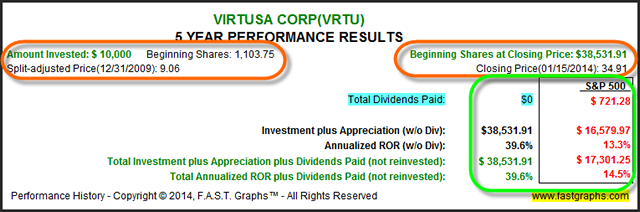

Virtusa Corp (VRTU)

Virtusa Corporation operates as an information technology services company. The company uses an offshore delivery model to provide information technology (IT) services, including IT and business consulting, application support and maintenance, development, systems integration, and managed services.

Special note:

The above list of potential high growth candidates represent only those companies that I feel were reasonably valued at current prices and expected earnings growth rates. The reader should know that I have excluded many of my most favorite growth stocks because I felt that they were overvalued in their own rights at today’s levels. Consequently, the above list is not offered as an exhaustive list of potential high growth candidates. Instead, it is comprised of only those companies that I feel reasonably valued, and therefore worthy of the more comprehensive research and due diligence efforts necessary to succeed as a high-growth stock investor.

Summary and Conclusions

Investing in high-growth stocks is not for everyone, and high-growth stocks are certainly not for the faint of heart. However, for those that do possess the intestinal fortitude to deal with the volatility and the higher risk that growth stocks have, the long-term rewards can be more than worth it. Moreover, I believe that the true benefits and rewards offered from owning high growth stocks requires the willingness and understanding to make a long-term commitment. For many high growth stocks, short-term volatility can be extreme, and therefore emotionally challenging.

Consequently, I believe that the only way to get the full complement of, and the ability to harvest their true return potential, is through owning them over a long period of time. This is because the true power of a high-growth stock rests with their ability to compound earnings at an above-average and high rate. By definition, compounding requires time. But, if your objective is to grow wealth, high-growth stocks can be one of the best investments available. As I illustrated in the article, you can pay more (a higher P/E ratio) for a fast-growing business and still receive above-average returns. On the other hand, if you follow the P/E ratio equal to growth rate valuation rule, both your risk and your long-term rate of return should be enhanced.

In my next article, part 3 of this series, I will review stocks that appear currently fairly valued for growth and income. Although the primary emphasis in part 3 will be on above-average total return through the combination of above-average capital appreciation and dividend growth, the majority of companies in this category are offered as more conservative selections than found in this article covering high-growth stocks. Moreover, although dividends and dividend growth will be secondary considerations to total return, each candidate in the growth and dividend category will pay dividends.

Disclosure: Long AZO, AAPL, ESRX, ATW, ECHO and NOG at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs