IN THIS ISSUE:

1.3Q GDP Surprise – Too Much Better Than Expected?

2.Why This Doesn’t Feel Like a 4.1% Economy

3. How Will the Fed Taper Going Forward?

4.Conclusions – Consumer Confidence is the Key

Overview

In today’s abbreviated holiday E-Letter, we’ll look at last Friday’s surprising report on 3Q GDP. In its third estimate of 3Q GDP, the Commerce Department reported that the economy surged by more than anyone expected. Given the surprisingly strong numbers, more than a few are questioning the report’s accuracy and wondering if it will be revised lower in January.

One reason for all the questions revolving around Friday’s strong GDP report is the fact that consumer confidence plunged in October and November and has yet to recover. Since consumer spending accounts for 70% of GDP, the recent drop in consumer confidence has to rebound if the economy is to accelerate.

Even if last Friday’s super-strong GDP report proves to be accurate, today’s economy certainly doesn’t feel like one that is growing at an annual rate of over 4%. While some areas of the economy are improving, only 24% of Americans believe economic conditions are getting better, while nearly 40% say the nation’s economy is actuallygetting worse. Today we’ll talk about why consumer confidence has tanked even as the economy is seemingly improving.

On a different front, the Fed moved last Wednesday to reduce its $85 billion in monthly bond and mortgage purchases to $75 billion starting in January. I discussed the details of the Fed’s latest policy announcement in myblogon Thursday. The burning question now is: How quickly will the Fed phase-out its QE purchases altogether? I’ll tell you what the latest thinking is below.

3Q GDP Surprise – Too Much Better Than Expected?

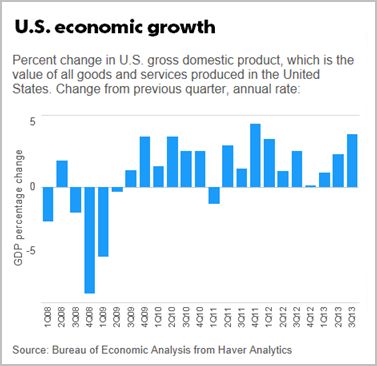

On Friday, the Commerce Department released its third estimate of 3Q GDP, and it wasfar above expectations. The government reported that the economy expanded by a whopping 4.1% (annual rate) in the 3Q. That was well above the pre-report consensus of 3.7% and a significant jump from the 3.6% they reported earlier this month, not to mention the advance estimate of 2.8% reported in early November.

This was the first time the economy has grown by more than 4% since the 4Q of 2011. If correct (and not revised lower later on), that means the economy has gone from dead in the water in the 4Q of last year at only 0.1% to 4.1% in just a year. If true, why does it not feel that way? More on that question below.

It is rare for the Commerce Department to miss a major economic number this badly – from a pedestrian 2.8% in early November to 4.1% last Friday. While I have always advised clients and readers to accept government economic reports at face value, this one makes even me raise an eyebrow, especially with the president’s approval rating at an all-time low and consumer confidence down sharply.

According to the Commerce Department, the increase in 3Q GDP primarily reflected positive contributions from private inventory investment, consumer spending, non-residential fixed investment, exports, residential fixed investment, and state and local government spending, that were partly offset by a negative contribution from reduced federal government spending and imports.

The report indicated that the big jump in 3Q inventories accounted for appx. 40% of overall GDP growth during the quarter. Companies stockpiled $115.7 billion worth of goods on warehouse and store shelves. Economists worry that GDP could fall in the final months of 2013, perhaps sharply, if companies are unable to sell all the goods they stockpiled in the 3Q. A survey of economists by MarketWatch forecasts GDP growth to drop to 2.1% in the 4Q.

Friday’s report also noted that consumer spending, the main driver of the US economy, rose 2% in the 3Q instead of the lackluster 1.4% as initially estimated. This, too, contributed to the Commerce Department’s significant upward revisions to GDP since its first estimate in early November.

Yet the news about consumer spending wasn’t entirely positive. While Americans spent a little more on recreational pursuits in the 3Q, the bulk of the increase in consumer outlays was directed towardhealthcare and gasoline – necessities that deprive households of discretionary income to spend on other goods and services.

As expected, President Obama seized on the latest GDP figures in his remarks on Friday. “We head into next year with an economy that’s stronger than it was when we started the year. Our businesses are positioned for new growth and new jobs. And I firmly believe that 2014 can be abreakthrough year for America.” [Emphasis added, GDH.]

Why This Doesn’t Feel Like a 4.1% Economy

It remains to be seen if last Friday’s surprising GDP number will hold up or not. As noted above, it is very unusual for a GDP estimate to go from 2.8% in early November to 4.1% as reported last Friday. While I’m not suggesting that the Commerce Department fudged the numbers, it will be very interesting to see if that number gets revised downward. Unfortunately, the first revision (if there is one) won’t come until January 30 when the government releases its first estimate of 4Q GDP.

Yet even if the 4.1% number does hold up, this economy just doesn’t feel like it’s growing nearly that rapidly. No doubt there are some good things happening. The unemployment rate is the lowest in five years, even though almost 11 million people are still out of work. The housing sector – which got us into this mess in the first place – is bouncing back. Home sales, prices and construction are all on the rise.

Auto sales recently had their strongest level since 2006. Gas prices have fallen significantly this year, and the stock markets have risen to new record highs . And there’s some reason to be hopeful for next year too. Last week, the Fed announced a slightly improved outlook for the economy in 2014.

Yet for many Americans, all the good news in the larger economy isn’t translating over to everyday life. As noted above, only 24% of the public believe economic conditions are improving, while nearly 40% say the nation’s economy is actuallygetting worse, according to a recent CNN poll. Meanwhile, the Consumer Confidence Index declined rather sharply in the last two monthly reports. This is not good.

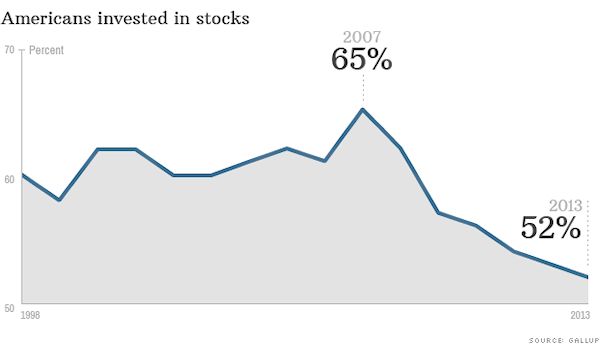

The economy still feels depressing because for many people, it is. Those at the very top have bounced back for the most part, largely due to the soaring stock markets. Yet we have not seen a similar rebound among the middle and lower classes in most cases. Stocks may be rising, but only half of Americans actually own them.

Sure, most big companies are flush with cash, but workers’ wages are up only about 1% from a year ago, making it harder for average folks to make ends meet. Then there are those who still cannot find work. As noted above, almost 11 million Americans remain unemployed, and 37% of them have been out of a job for at least six months.

While last Friday’s better than expected GDP report is welcome news, the improvement wasn’t nearly as good as it looked and isn’t expected to last. The Fed predicts the economy will grow 3% next year, marking more solid, but still not robust, improvement ahead.

So, will 2014 be the economy's “breakthrough year” that President Obama predicted on Friday as he was about to depart on his Christmas vacation in Hawaii? Probably not, in my opinion.

How Will the Fed “Taper” Going Forward?

As everyone reading this knows, last Wednesday the Fed moved to reduce its $85 billion in monthly bond and mortgage purchases to $75 billion starting in January. I discussed the details of the Fed’s latest policy announcement in myblogon Thursday. The burning question now is: How quickly will the Fed phase out its QE purchases altogether?

In its policy statement released last Wednesday, the Fed said it will slow its QE buying “in further measured steps at future meetings” if the economy improves as forecast. At his press conference following the meeting last Wednesday, Bernanke elaborated:

"If we’re making progress in terms of inflation and continued job gains, then I imagine we’ll continue to do, probably at each meeting, a measured reduction [in purchases]."

Bernanke also hinted that reductions of $10 billion per meeting would be the “the general range,” but he also said the range would be dependent on how the economy is doing. If the economy slows, the Fed may “skip a meeting or two,” and if the economy accelerates it may taper a “bit faster.”

At the rate of $10 billion in reduction per policy meeting, which are held eight times per year, the QE should stop before the end of next year. I continue to predict that the end of QE will be bad for stocks, but then you wouldn’t have thought that last Wednesday when stocks exploded higher immediately after the policy statement was released. We’ll see.

Conclusions – Consumer Confidence is the Key

Last Friday’s 3Q GDP report was a big surprise in that it was well above pre-report expectations at 4.1%. Many economists questioned whether that number was for real. One of the main reasons for questioning the much stronger than expected GDP estimate is the fact that consumer confidence has fallen rather sharply in recent months.

Most forecasters suggest that much of the reason for the drop in consumer confidence was the partial government shutdown in October, which may have put spending plans on hold for lots of Americans. That may or may not be true.

Yet as noted above, recent polls have shown that very few Americans (24%) believe the economy is getting better, and even more (40%) believe the economy is actually getting worse. I donot believe that the brief partial shutdown of the government is fully responsible for the recent drop in consumer confidence.

We know that consumer spending for back-to-school items was disappointing in late summer. Halloween spending disappointed as well. So did Black Friday spending. Likewise, surveys in early December found that 37% of shoppers planned to spend less on Christmas this year, while only 14% planned to spend more.

This is not good news, since consumer spending accounts for 70% of GDP.

The bottom line is: If the economy is set to improve in 2014, as most analysts predict in the wake of last Friday’s surprise GDP estimate of 4.1%, consumer confidence absolutelymust improve just ahead. We’ll see.

****************

Merry Christmas & Happy Holidays!!

Wishing you peace and joy,

Gary D. Halbert

© Halbert Wealth Management