IN THIS ISSUE:

1.The New Federal Budget Deal That Nobody Likes

2.Fed Considers New Strategy to Stimulate Economy

3. Former Fed Official Explains How This Would Work

4.Conclusions – This Would Be A Huge Surprise!

Overview

My readers know that the global financial world is waiting with bated breath for tomorrow’s Fed decision on whether to start to “taper” QE purchases now or wait until next year. The Fed’s Open Market Committee (FOMC) is holding its last policy meeting of the year today and tomorrow, and Chairman Bernanke will hold a press conference afterward.

The latest surveys indicate that most Fed watchers believe the FOMC will wait until next year to taper, but that remains to be seen. What is actually more interesting is some language that was buried in the minutes from the October 29-30 FOMC meeting. The minutes were released on November 20.

Within those minutes, we find that the FOMC is considering lowering or removing the interest paid to commercial banks on money they choose to leave on deposit with the Fed. The minutes reveal that at the late October policy meeting, the Committee members discussed the possibility that the FOMC might reduce or eliminate the 25 basis-points of interest the Fed pays to big banks that leave excess reserve deposits at the Fed. This is potentially very big!

Why would the Fed do this? The minutes suggest that the FOMC believes that reducing or eliminating the interest paid to commercial banks would spur those banks to draw down those deposits and use that money to make more loans, thus stimulating the economy – and pave the way for the Fed to start its QE taper. This is extremely interesting. I’ll lay it out for you today.

But before we get into that discussion, I’d like to analyze the latest two-year federal budget that was passed by the House last week, and may pass the Senate as early as tonight. The bipartisan budget deal was hailed as a major victory by lawmakers and the White House. But as I will explain below, the latest budget deal represents a sell-out by both political parties.

That’s a lot to cover in one letter, so let’s get right to it.

The New Federal Budget Deal That Nobody Likes

Last week, the House of Representatives passed a two-year compromise federal budget that neither Republicans nor Democrats are very happy with. Despite that, it was heralded as a huge victory (not by me) for the country since it avoids another likely government shutdown in mid-January.

Never mind that it increases the federal budget in each of the next two years – what else is new? And it rolls back some of the “sequester” spending cuts that Republicans fought for and won in 2011. Most conservatives (including me) are not happy about that; then again, most liberals are just as unhappy because several of their pet projects were not funded.

The House voted overwhelmingly (332-94) to approve the two-year budget deal crafted by Rep. Paul Ryan (R-WI) and Sen. Patty Murray (D-WA). The legislation won the support of 169 Republicans and 163 Democrats. It now heads to the Senate, where it will likely pass as early as tonight. President Obama has signaled that he will sign the bill into law.

The new budget deal sets federal discretionary spending at $1.012 trillion for the fiscal year 2014, and then rises to $1.014 trillion in fiscal 2015 – and both are above the FY2013 spending level. The deal also replaces the next round of sequester cuts slated to take effect in January with smaller, more targeted spending cuts, supposedly over the next decade. Absent the agreement, discretionary spending would decline to $967 billion early next year, with a large proportion of the cuts hitting the Pentagon.

Those cuts are out the window now. The agreement, which projects a scant $23 billion in net deficit reduction over the next 10 years, doesn’t extend expanded unemployment benefits that expire at the end of December. It also does nothing about the debt ceiling, which must be addressed sometime in the spring. Still, the new budget was hailed as a sweeping success by the mainstream media.

As noted above, neither party is jumping for joy over the agreement. House Minority Leader Nancy Pelosi (D-CA) told Democrats in a closed meeting that Congress needs “to get this off the table so we can go forward.” Speaker John Boehner (R-OH) told reporters last Thursday morning that the agreement is “not everything that we wanted, but it advances conservative policy and moves us in the right direction.” No it doesn’t – it just spends more!

Both parties believe that the budget helps them politically. With the threat of a government shutdown in January removed, Republicans think they can keep focusing on Obamacare, which has had a disastrous roll out. Democrats are already laying the groundwork to pressure Republicans to extend unemployment benefits, which expire at the end of December. And Democrats are sure to pressure Republicans in 2014 to vote on immigration reform, which has long been stalled in the House.

The bottom line is that the new budget deal passed by the House: 1) increases federal spending for FY2014 and FY2015; 2) eliminates the round-two sequester spending cuts that were to be enacted as of January 1; and 3) increases taxes on consumers, especially airline travelers who will see increased ticket fees. In short, this is abad deal all the way around.

Finally, there is one other serious problem with the new budget passed by the House. The bill includes a 1% reduction in cost-of-living benefits for many military retirees under 62 years old. That means that many of our current and future veterans would be taking a cut in benefits in order to pay for part of the increased spending I discussed above. This is a travesty! Hopefully, the Senate will strike this onerous provision from the new budget before they pass it today.

Fed Considers New Strategy to Stimulate Economy

As discussed above, the FOMC is holding its final policy meeting of the year today and tomorrow. All eyes in the global financial world will be watching intently tomorrow afternoon when Ben Bernanke holds his final press conference as Fed Chairman – to see if the Fed will elect to reduce QE purchases before the end of the year. Most hope it willnot, since it is so clear that the Fed’s massive QE purchases have driven most stock markets to new record highs.

If we look at the official minutes from the last FOMC meeting on October 29-30, which were made public on November 20, we find that there was considerable discussion by the Committee on when to taper QE purchases. But there also was some new discussion regarding an entirely different strategy to spur the economy.

Specifically, the FOMC discussed the possibility of lowering or eliminating the interest it pays to commercial banks on the money they choose to leave on deposit with the Fed. Currently, banks have a record $2.5 trillion on deposit with the Fed, on which they are paid interest of 0.25% annually – or about $6.25 billion a year.

To appreciate how significant this idea is, we need to understand why banks have chosen to leave vast sums of money on deposit with the Fed earning what would seem to be a paltry rate of only 25 basis points, rather than using that money to make far more profitable loans.

Banks are required to keep a minimum amount of cash on hand – called “reserves” – so they can fulfill withdrawal requests from their customers. Any reserves held over and above these minimum requirements are called “excess reserves.”

During strong economic periods, banks tend to hold the minimum required reserves, since they prefer to use the capital in more profitable ways (ie – loans). Prior to the financial crisis in 2008, excess reserves held at the Fed were a small fraction of the amount held at the nation’s central bank today. So, the question is, why are big banks holding a record $2.5 trillion with the Fed today?

The answer is that these huge Fed deposits are risk-free, whereas commercial loans arenot risk-free, especially since the financial crisis.

The Fed is interested in any ways it can find to stimulate the economy – and QE has not done the trick as the Fed had hoped. So, the FOMC is looking at other ways to boost the economy, and if it reduces or eliminates the interest on excess reserves banks hold at the Fed, that might encourage banks to make more loans.

Former Fed Official Explains How This Would Work

On December 10, former Fed Governor Alan Binder explained in an article published in The Wall Street Journal how and why the Fed might consider such a strategy, and encouraged the FOMC to do so. Below are a few excerpts from his article:

Todaybankshold a whopping $2.5 trillion in excess reserves, on which the Fed pays them an interest rate of 25 basis points—for an annual total of about $6.25 billion. That 25 basis points, what the Fed calls the IOER (interest on excess reserves), is the issue. Unlike the Fed’s main policy tool, the federal-funds rate, the IOER is not market-determined. It’s completely controlled by the Fed. So instead of paying banks to hold all those excess reserves [at the Fed], it could charge banks a small fee, i.e., a negative interest rate, for the privilege.

So Mr. Binder is suggesting not only that the FOMC cease paying banks 25 basis points, but also that it might even considercharging banks a small fee for parking excess reserves at the Fed. Mr. Binder also offered some insights as to why the Fed is seriously considering this possibility, based on language in the October 29-30 FOMC meeting minutes. Here are the specific FOMC minutes he referred to:

For example, most participants thought thata reduction by the Board of Governors in the interest rate paid [to banks] on excess reserves could be worth considering at some stage. [Emphasis added, GDH.]

Mr. Binder went on to emphasize why that new language in the Fed minutes is so significant:

I can assure you that those buried words were momentous. The Fed is famously given to understatement. So when it says that “most” members of its policy committee think a change “could be worth considering,” that’s almost like saying theylove the idea. That’s news because they haven’t loved it before. [Emphasis added, GDH.]

Binder goes on to explain why the mountain of excess reserves sitting at the Fed does nothing whatsoever to help the economy:

Excess reserves sitting idle in banks’ accounts at the Fed do nothing to boost the economy. We want banks to use [ie- loan] the money. If the Fed turned the IOER negative, banks would hold fewer excess reserves, maybe a lot fewer. They’d find other uses for the money. One such use would be buying short-term securities. Another would probably belending more, which is what we want. [Emphasis added, GDH.]

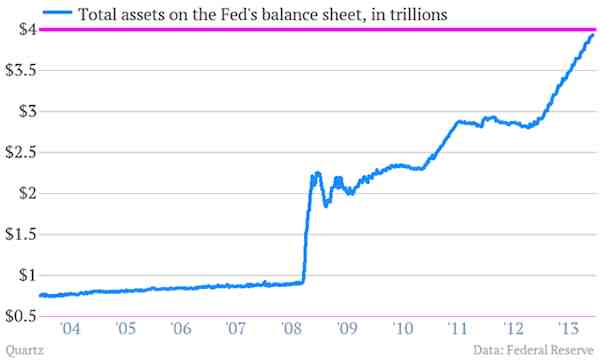

Finally, we know that FOMC members are not sleeping well knowing they cannot continue to grow the central bank’s balance sheet indefinitely with QE purchases. In fact, QE purchases are about to top the massive $4 trillion level any day now, as seen in the chart above. According to Binder, charging interest on reserves could assist in this area as well:

A second reason for cutting the IOER answers some of the criticisms the Fed has taken for its asset-buying programs called quantitative-easing: Doing so would stimulate the economy without increasing the size of the Fed’s balance sheet. In fact, the Fed could probably shrink its balance sheet.

Conclusions – This Would Be A Huge Surprise!

What you have read here today ishuge news that has been largely missed by the mainstream media and even some ardent Fed watchers. Let’s summarize by pointing out what we know for sure, and then what we don’t know.

First, commercial banks have piled up record amounts of excess reserves – $2.5 trillion and rising – at the Fed in recent years, rather than loaning that money to customers who clearly need such loans.

Second, the FOMC clearly discussed reducing or eliminating the interest paid to banks for keeping excess reserves on deposit with the Fed at its October 29-30 policy meeting. This hasnot been discussed as a policy option in at least the last several years since the financial crisis began.

Third, a highly respected former member of the Fed has gone public to: 1) emphasize that the FOMC discussed this action at its October 29-30 policy meeting; and 2) encourage the current FOMC members to take this action.

Fourth, these things donot happen by accident. It is almost certain that Mr. Binder’s public comments were coordinated with Fed Chairman Bernanke beforehand. This suggests that the Fed is seriously considering this option.

What we don’t know is whether the Fed will continue this discussion at its FOMC meeting today and tomorrow, but I highly suspect it will. If it does, we don’t know if that discussion will be reflected in the official policy statement issued tomorrow. It was not mentioned in the last policy statement on October 30, and only became known when the FOMC minutes were made public on November 20.

In addition, if the Fed gets serious about cutting the interest it pays banks on excess reserves, it is not clear yet what effects that would have on the stock and bond markets. That remains to be seen. But generally speaking, the financial markets don’t like big surprises. And this one – if it happens – will be a major surprise.

Finally, I don’t know why the mainstream media hasn’t (to my knowledge) picked up on this potentially huge news. Remember you read about it here first!

Holiday Best Wishes

I sincerely hope that all of you are further along on your holiday shopping than I am. After hosting a big group of family and friends at our house for Thanksgiving, and with the two holidays so close together this year, I am really behind on my Christmas shopping.

Even so, I love this time of the year, especially with the kids home from college. It already feels like the holidays to me. Now if I can just get my shopping done by this coming weekend! While it is a hectic time, let us not forget the Reason for the Season and be thankful for all our blessings.

And speaking of blessings, I thank you as always for reading my weekly letters and the blog. Your comments and suggestions are always greatly appreciated!

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management