Stay the Course or Take an Unconstrained Approach to Bonds

While investors may be prone to react to the last “expert” they heard and follow the pack, many advisors generally advise their clients to “stay the course.” Yet these same advisors are constantly on the lookout for more productive ways to navigate today’s treacherous investment waters for their clients, especially in the bond market. Many advisors realize that we are currently experiencing a unique risk setting with respect to the bond market; the confluence of a bear bond market, potentially imminent rising rates and uncertain Fed policy decisions. Many advisors seem to be looking for what their pre-retiree and retiree clients really need … strategies that have the potential to deliver:

1) Capital preservation in today’s threatening environment

2) Capital appreciation to maintain purchasing power and avoid running out of retirement funds

3) A continuing flow of income when needed.

A weakness of the guidance to manage a bond meltdown, for the investor or planner, is treating the “bond market” as a single homogeneous asset class. The assumption is that all bonds react essentially the same way to economic forces such as interest rates, with maturity and duration being meaningful differentiators. This approach makes the news easier to communicate given the limits of TV time and print space. Unfortunately, it leaves out other vital factors.

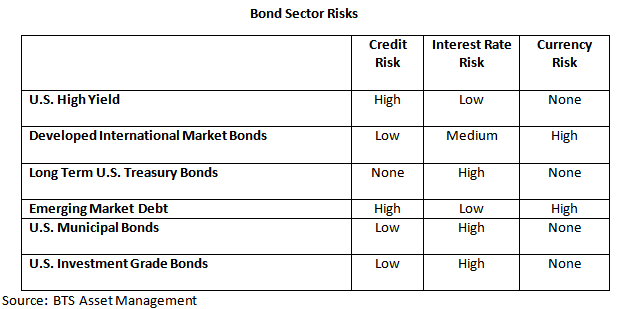

Just as many equities (e.g. growth, value, large, small, domestic, international and commodities (e.g. agricultural, minerals, financials, energy, gold) react differently to economic stimuli, bonds are also not all alike. Each bond class reacts in its own way to those stimuli. Interest rate changes are the primary, though not only, factor affecting values of highly rated bonds, such as U.S. Treasuries and AAA rated corporate bonds. The bond market rarely moves in a straight line up or down. Those with experience and an understanding of market indicators will be on the lookout for the “right bond at the right time” to try to take advantage of trading opportunities. The values of lower rated bond classes may be significantly affected by business factors, and less so by interest rate changes.

As the table below shows, interest rate changes may have a relatively low effect on the value of High Yield bonds, yet credit ratings of the issuing companies have a significant effect. The opposite tends to hold for long term U.S. Treasury bonds.

Understanding the differing nature of the various bond sectors is key to potentially profiting from a bond investment strategy. The pundits and media folks usually ignore these differences, probably because they are not as easy to understand or as exciting as forecasting a bust in bond prices. But for an investor, these differences may be crucial to managing risk and maximizing returns. When perceived risk increases in one bond class, there is often opportunity in another.

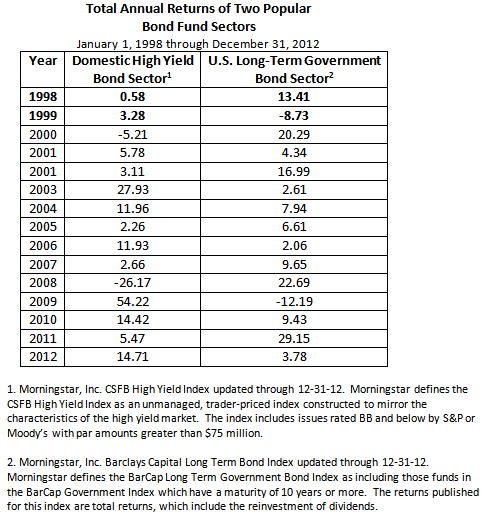

As the following table demonstrates, there have been many periods when U.S. Government bonds have had low or negative returns, while High Yield bonds have had higher, positive total returns. The reverse also appears to be

evident.

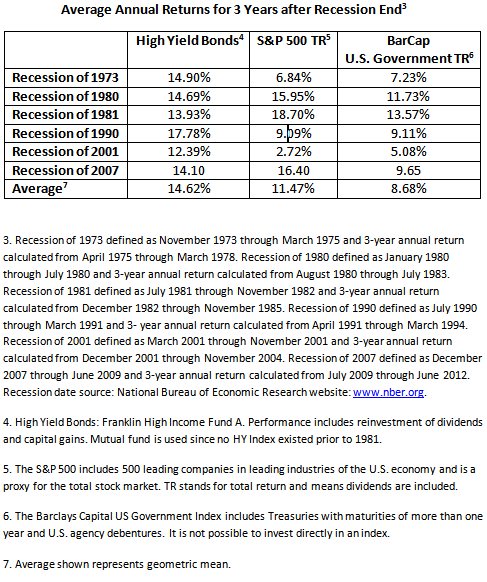

Moving between different bond classes at the appropriate time may help manage risk in a bond portfolio, as well as seek the returns that “baby boomers” and others need. While the economy continues to recover and interest rates continue to rise, the question often raised is how a bond strategy may be structured to potentially grow. This goes to the core of the “bond bust” argument because we have seen U.S. Government bonds lose value at different times. Recall, however, that credit risk is a prime driver of High Yield bond values. Part of the definition of an economic recovery involves business improving, and with it, the credit quality of corporate debt. As a result, during economic recoveries, High Yield bond prices have historically outperformed U. S. Government bond prices.

Take a look at how High Yield bonds, the S&P 500, and U.S. Government Bonds have performed in some recovery periods after major recessions.

Rising Rates Impact on Bonds

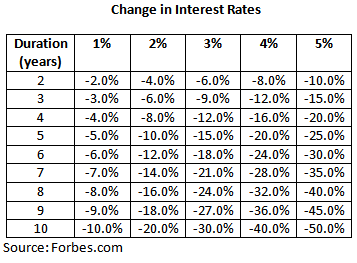

The question becomes how much market value can bonds lose if rates rise? This depends on the bonds duration or price sensitivity to changes in interest rates.

This table illustrates the anticipated loss in market value in a rising interest rate environment.

The longer the bond’s duration, the greater the risk of loss if rates move up. Bond investors, especially those holding longer maturity bonds, may see increasing losses in a rising rate environment. In the minutes from the September FOMC meeting, Chairman Bernanke anticipates keeping rates low so long as unemployment is below 6 1/2 % and inflation stays below the 2% Fed target. We believe the Fed will eventually raise rates to more normal historical levels by the end of the decade. Chairman Bernanke noted during his press conference after the September meeting, that he thought policy rates could move from the current 0.25% to 1% in 2015 and 2% in 2016; after that another 2% toward the end of the decade. This may suggest that longer duration bonds could be under severe pressure this decade.

Time for an Unconstrained Approach to Bonds

Investors and advisors alike may be increasingly concerned about the effect that higher interest rates and expanding federal and municipal debt could have on medium and long term bond prices. Holding long term bonds in the years ahead may suggest enduring volatility and loss of capital, especially at a time when investors may still be trying to recover from the market crash of 2008-09. The prospect of this happening has resulted in some investors keeping their money on the sidelines, unsure of what lies ahead. As interest rates are likely to eventually move higher; it also seems likely that monetary policy rates could return to a normalization level (closer to the average of 4% as opposed to today’s 0 -.25%). Note that a zero rate Fed policy stance is unique in history and these types of events put us in uncharted territory. We may experience an unprecedented series of events in the years to come, a by-product of our recent Great Recession, slow recovery and bear market in bonds. How then may advisors prepare for this and take advantage of the differing performance of the various bond sectors for their clients in varying economic and market conditions?

Today’s environment calls for an unconstrained approach to bonds with the ability to move between bond asset classes based on economic indicators and market opportunities. The potential discrepancy in results among bond asset classes may be more pronounced than we have seen in the past 30 years which, in our view, creates opportunity for a more tactical approach. Now may be the time for an unconstrained approach to the bond market.

© BTS Asset Management