This Bentonville, AR based mega-retailer perennially ranks amongst the top of the Fortune 500 list and likely needs no introduction. In lieu of a business summary, we thought it might be interesting to highlight some prominent statistics. For instance, every week more than 245 million customers visit Wal-Mart’s (WMT) 11,000 stores under 69 banners in 27 different countries. Last year alone the company had sales of about $466 billion while employing 2.2 million associates.

To put some of those numbers in context, Wal-Mart employs more people than the entire population of New Mexico; which makes sense given that Wal-Mart is the top employer in 25 of the United States. Each week nearly a third of the U.S. population visits one of Wal-Mart’s 4,786 U.S. stores. With sales over $450 billion Wal-Mart by itself would rank as the world’s 26th largest economy, just behind Norway. Or perhaps you might even be interested to know that Wal-Mart parking lots collectively take up roughly the size of Tampa, FL.

Just think: all of this massive scale began with a single store and a 44-year-old entrepreneur. But this article isn’t about swaying one’s opinion about Wal-Mart. Instead, it’s an update on the current prospects of the business.

Directly to the point of recent company news, Wal-Mart just announced the election of a new CEO, Doug McMillon. Doug, 47, will succeed current CEO Mike Duke on February 1st of 2014. Interestingly, Mr. McMillon began his career as a summer associate in 1984 – working his way up to eventually lead the international unit of the business. If the future is anything like the past operating results of Wal-Mart, then the business will be just fine.

In respect to returning value to shareholders, Wal-Mart has demonstrated a continued propensity to deploy cash via dividends and share repurchases. For instance, Wal-Mart has not only paid but also increased its dividend for 39 straight years. In addition, these increases have come in at a rate of about 18% per year over the last decade, while the company still only pays out about a third of its earnings. With regard to Wal-Mart’s share repurchase program the company has been especially proactive by decreasing common shares outstanding from about 4.45 billion in 1999 to today’s number closer to 3.27 billion. Further, the company recently authorized a new $15 billion share repurchase program that mirrors the $14 billion in completed purchases over the last 2 years.

Yet none of this is to suggest that the company is without risks. For instance, perhaps some might believe that Wal-Mart will fall short in fighting off e-commerce rival Amazon (AMZN). Conceivably, same-store sales might continue to decline as a result of a weakened consumer. And of course there’s always litigation risk with such a large company being involved in so many operating facets. In fact, the company listed 14 separate risk factors in its most recent 10-K. With the above being stated, let’s take a look at the company through the lens of fundamental analyzer software tool, F.A.S.T. Graphs™.

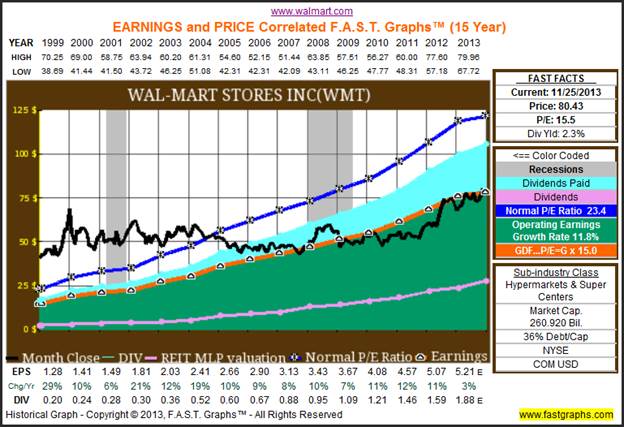

15 Years of Growth

Wal-Mart has grown earnings (orange line) at a compound rate of 11.8% since 1999, resulting in a $260+ billion dollar market cap. In addition, Wal-Mart Stores’ earnings have risen from $1.28 per share in 1999, to today’s forecasted earnings per share of approximately $5.21 for 2013. Further, as described, Wal-Mart has not only paid a dividend (pink line) but also increased it for 39 straight years.

For a look at how the market has historically valued Wal-Mart, see the relationship between the price (black line) and earnings of the company as seen on the Earnings and Price Correlated F.A.S.T. Graph below.

Here we see that Wal-Mart’s market price previously began to deviate from its justified earnings growth; being consistently overvalued in 1999 and taking a full 8 years to come back to fair value around 2007. Today, Wal-Mart appears to be in-value in relation to both its historical earnings and relative valuation.

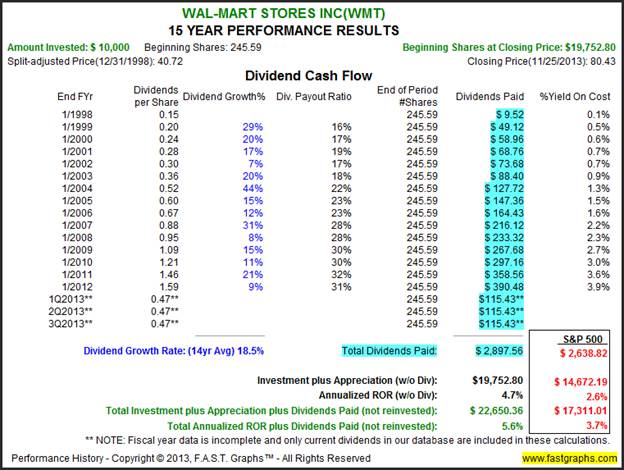

In tandem with the strong earnings growth, Wal-Mart shareholders have enjoyed a compound annual return of 5.6%. Note that this outcome greatly trails the business results of the company due to the high initial valuation. A hypothetical $10,000 investment in Wal-Mart Stores on 12/31/1998 would have grown to a total value of $22,650.36, without reinvesting dividends. Said differently, Wal-Mart shareholders have enjoyed total returns that were roughly 1.3 times the value that would have been achieved by investing in the S&P 500 over the same time period. It’s also interesting to note that an investor would have received approximately 1.1 times the amount of dividend income as the index as well. This isn’t a spectacular result, but it is notable given that Wal-Mart shares began the period trading at about 43 times earnings.

But of course – as the saying goes – past performance does not guarantee future results. Thus, while a strong operating history provides a fundamental platform for evaluating a company, it does not by itself indicate a buy or sell decision. Instead an investor must have an understanding of the past while simultaneously thinking the investment through to its logical, if not understated, conclusion.

In the opening paragraphs potential catalysts and risks were described. It follows that the probabilities of these outcomes should be the guide for one’s investment focus. Yet it is still useful to determine whether or not your predictions seem reasonable.

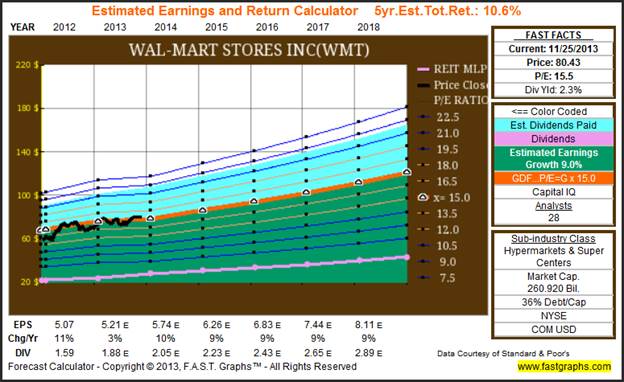

Twenty-eight leading analysts reporting to Standard & Poor’s Capital IQ come to a consensus 5-year annual estimated return growth rate for Wal-Mart of 9%. In addition, Wal-Mart is currently trading at a P/E of 15.5, which is inside the “value corridor” (defined by the orange lines) of a maximum P/E of 18. If the earnings materialize as forecast, Wal-Mart’s valuation would be around $121 at the end of 2018, which would be a 10.6% annualized rate of return including dividends. A graphical representation of this calculation can be seen in the Estimated Earnings and Return Calculator below.

It’s paramount to remember that this is simply a calculator. Specifically, the estimated total return is a default based on the consensus of the analysts following the stock. The consensus includes the long-term growth rate along with specific earnings estimates for the next two upcoming years. Further, the dividend payout ratio is presumed to stay the same and grow with earnings. Taken collectively, this graph provides a very strong baseline for how analysts are presently viewing this company. However, a F.A.S.T. Graphs’ subscriber is also able to change these estimates to fit their own thesis or scenario analysis.

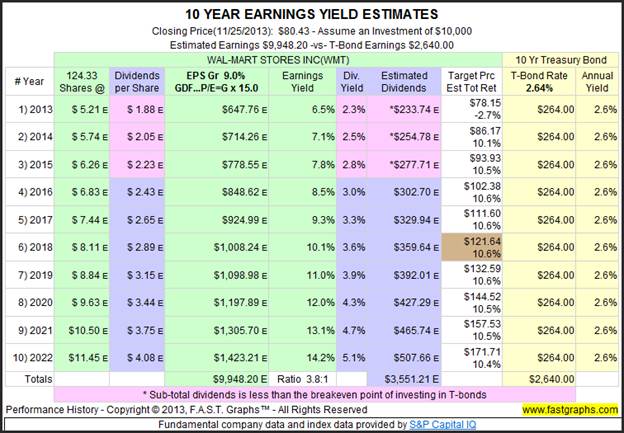

Since all investments potentially compete with all other investments, it is useful to compare investing in any prospective company to that of a comparable investment in low risk treasury bonds. Comparing an investment in Wal-Mart to an equal investment in a 10-year treasury bond, illustrates that Wal-Mart’s expected earnings would be 3.8 times that of the 10-year T-Bond Interest. This comparison can be seen in the 10-year Earnings Yield Estimate table below.

Finally, it’s important to underscore the idea that all companies derive their underlying value from the cash flows (earnings) that they are capable of generating for their owners. Therefore, it should be the expectation of a prudent investor that – in the long-run – the likely future earnings of a company justify the price you pay. Fundamentally, this means appropriately addressing these two questions: “in what should I invest?” and “at what time?” In viewing the past history and future prospects of Wal-Mart we have learned that it appears to be a strong company with solid upcoming opportunities. However, as always, we recommend that the reader conduct his or her own thorough due diligence.

Disclosure: Long WMT at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S. T. Graphs