IN THIS ISSUE:

1.October Jobs Report – Better Than Expected

2.Third Quarter GDP Report – Better Than Expected

3.Consumer Sentiment Continues to Fall in November

4.Obama Calls For Minimum Wage Hike to $10.10

5.An Objective Look at the Minimum Wage Debate

Overview

President Obama called for a whopping 39% increase in the minimum wage from $7.25 to $10.10 per hour last Thursday. There is already a bill working its way through in the Senate to do the same thing. If this legislation passes, the minimum wage will be increased 95 cents each year for the next three years starting this year, to bring it to $10.10 by 2015.

Many argue that this will be a huge job killer and could thrust the economy back into a recession. However, some of the critics I’ve read don’t consider that the 39% increase in the minimum wage will be phased in overthree years. Supporters of the wage hike argue that the seemingly huge increase merely restores the purchasing power for the low-paid workers in America. We’ll look into both arguments today.

Before we get to that controversial topic, let’s take a look at last Friday’s surprising unemployment report, last Thursday’s better than expected GDP report and the continued slide in consumer confidence.

October Jobs Report – Better Than Expected

Last Friday’s unemployment report for October was better than expected even though the headline jobless rate rose from 7.2% in September to 7.3% last month. Despite the government shutdown and the threat of default, the Bureau of Labor Statistics (BLS) said the US economy added 204,000 new jobs last month, far above expectations.

The BLS also revised upward the number of jobs that were previously reported for August and September by a total of 60,000. With these new revisions, that means employers added a monthly average of 202,000 jobs from August through October, up from 146,000 from May through July. Obviously, that is a significant improvement.

The reason that the headline unemployment rate went up last month, we are told, is that the BLS counted some of the 800,000 government workers that were furloughed on October 1 as unemployed, even though they were back on the job after the shutdown ended on October 16. This will almost certainly lead to another revision of the October data when the November jobs report is released on December 6.

Some earlier data have hinted that hiring was improving. Retail stores, shipping companies and other services firms stepped up hiring in October, according to private surveys of service firms. And the number of people seeking unemployment benefits has fallen back to pre-recession levels after four weeks of declines. Unemployment benefit applications are a proxy for layoffs. The steady decline suggests companies are cutting fewer jobs.

Friday’s report was not without any bad news, however. The number of people in the labor force fell in October as many simply gave up hope of finding a job. The percentage of people in the workforce is now at its lowest level in 35 years.

The report again confirmed that we have 11.3 million unemployed workers. About a third have been out of a job for six months or more, while 815,000 were so discouraged by their prospects that they have stopped looking for work. The report showed that 720,000 people left the labor force in October, an unusually large decline.

Finally, the U-6 measure of unemployment, which takes into account frustrated workers and people who are working part-time but would prefer to be working full-time,stood at 13.8% in October.

On balance, however, the October jobs report was seen as positive, especially with new jobs jumping above 200,000 on average for the last three months. It should be noted, however, that even at 202,000 jobs a month, it would take more than five years to return to pre-recession employment levels.

As the Economic Policy Institute points out, we need 8.0 million more jobs to get back to the pre-recession unemployment rate, and at the average rate of growth of the last 12 months, that won’t happen for another five years. There are currently over six million missing workers, and if these workers were in the labor force looking for work, the unemployment rate would be 10.8% instead of 7.3%. I actually wrote in detail about these missing workers in myMay 7 E-Letterearlier this year.

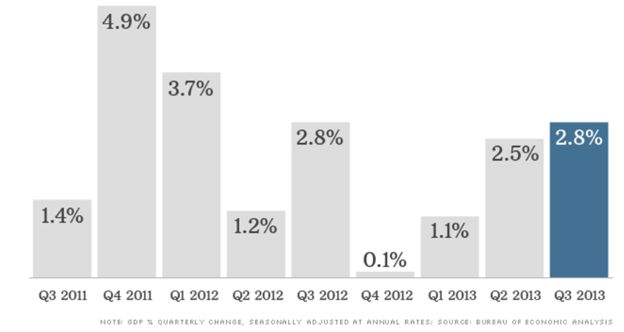

Third Quarter GDP Report – Better Than Expected

Friday’s surprising jobs report came just on the heels of last Thursday’s stronger than expected 3Q GDP report. The “advance” report showed that the economy expanded at a 2.8% (annual rate) in the July through September quarter. That was well above the pre-report consensus of only 1.9%-2.0% and the pace of 2.5% in the 2Q.

While the headline number was higher than expected, a look at the report’s internals tells a different story. First, the rate of increase in consumer spending is slowing down. Second, much of the gain in the 3Q was due to inventory rebuilding which is also expected to slow down in the current quarter. Third, the rate of growth in business investment (equipment, technology, etc.) slowed sharply in the 3Q.

I discussed last week’s GDP report in more detail in myblogon Thursday in case you want more analysis. And you probably should since most forecasters now expect the economy to be weaker this quarter.

Finally, there is a growing consensus that last Thursday’s advance GDP report is not as valuable as in the past. The reason is that the Commerce Department (like much of government) was shut down for 16 days at the beginning of October. As a result, Commerce didn’t have as much data to consider in making its first 3Q GDP estimate. For that reason, the next 3Q estimate due out on December 5 could be revised significantly.

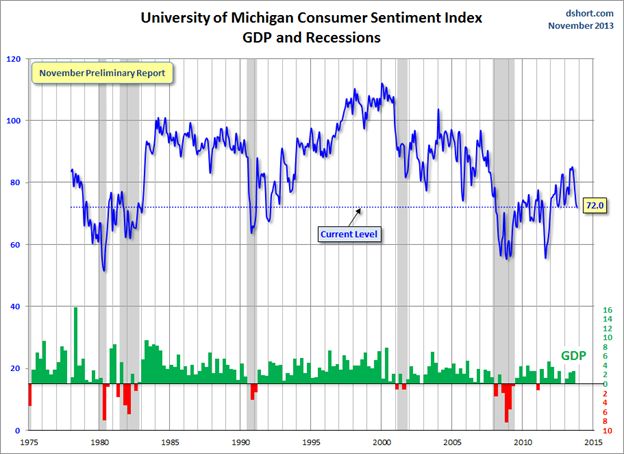

Consumer Sentiment Continues to Fall in November

Consumer sentiment continued to fall in early November to nearly a two-year low as lower-income households worried about their job prospects and financial outlooks, and negative views of the government lingered, according to a survey released on Friday.

The Thomson Reuters/University of Michigan’s preliminary reading on the overall index of consumer sentiment fell to 72.0 in November, its lowest since December 2011. That was beneath October’s final reading of 73.2 and the 74.5 economists had expected this month.

Lower-income households in particular worried about their future finances, in contrast to households with incomes above $75,000 which were more optimistic as increases in stock prices raised net wealth.

In the latest survey, consumers remained nearly as negative on government policies as they were last month, when a federal government shutdown prompted worries that growth would drag. The survey’s gauge of consumer expectations going forward edged down to 62.3, compared to 62.5 in October and analyst expectations of 64.0.

Obama Calls For Minimum Wage Hike to $10.10

Last week, President Obama called for a huge hike in the minimum wage to $10.10 per hour, up from the current wage floor of $7.25 in most states. That’s an increase of 39%, although it will be phased in over three years at 95 cents annually. Plus, once we get to $10.10 per hour, the president wants to index the minimum wage to inflation, thereby insuring that it goes up every year.

You may recall that Mr. Obama called for raising the minimum wage to $9 in his State of the Union address in February. Now he’s upped the ante to $10.10. The White House confirmed last Thursday that the president has decided to throw his weight behind legislation introduced earlier this year by Sen. Tom Harkin (D-Iowa) and Rep. George Miller (D-Calif.) to raise the minimum wage to $10.10 by 2015. The White House released the following statement:

“The President has long supported raising the minimum wage so hardworking Americans can have a decent wage for a day’s works to support their families and make ends meet, and he supports the Harkin/Miller bill that accomplishes this important goal.”

Harkin and Miller have said that a minimum wage hike to $9 would be insufficient. The president’s support of the $10.10 proposal may help more Democrats rally around the bill as the Senate takes it up in coming weeks. A spokesman for Rep. Miller added:

"We are very pleased President Obama endorsed a $10 an hour minimum wage bill. This action unites all Democrats and minimum wage advocates behind one proposal that addresses income inequality in a powerful way. Congress must move to raise the minimum wage now."

While the federal minimum wage has held steady since it was last raised to $7.25 in 2009, many states and municipalities have continued to raise or implement their own minimum wages. Just last week, New Jersey voters approved a minimum wage bump to $8.25 per hour. Last month, California lawmakers raised theirs to $10, making it the highest state minimum wage in the nation. Now the Democrats and the president want the federal minimum wage even higher than California’s.

* Recent increases in New Jersey and California are not indicated above.

The congressional Democrats’ proposal would raise the minimum wage to $10.10 through a series of increases over the next three years, and after 2015 it would be increased each year according to inflation.

The minimum wage would also soar for restaurant servers and other tipped workers whose employers can pay them as little as $2.13 before tips. The minimum wage for those workers would be set at 70% of the federal minimum wage. At $10.10 per hour, 70% would be $7.07 by 2015, or an increase of 232%. Wow! Imagine how many jobs will be lost in this industry if the Harkin/Miller bill is passed. Imagine the price of meals! Remember, ALL costs are passed along to the consumer, especially in this industry.

It is worth noting that this monster change in the food services industry will force tipped workers to pay taxes on most of their income, unlike tips which are not always declared. Instead of declaring and paying taxes on $2.13 per hour, it will go to $7.07 per hour. As a result of sharply higher food costs, tips could well become a thing of the past!

The $10.10 figure in the Harkin/Miller proposal isn’t arbitrary. Progressive economists like to point out that if the minimum wage had kept pace with inflation since its high in the late 1960s, it would now be above $10. It is true that if you use a common inflation calculator, the $1.60 minimum wage in 1968 adjusted for inflation would be over $10 per hour in 2013.

Still, opponents argue that a 39% increase in the minimum wage – even spread over three years – is just too large of an increase in a relatively short time, and that will be a serious drag on the still-weak economy.

Of course, it’s possible the president's $9 proposal in February could weaken Democrats’ bargaining position with the House GOP. Republicans will argue that the president felt that $9 was sufficient back February, so why not now? I fully expect them to seek a smaller minimum wage hike, if they agree to one at all. Republican leaders have already called the Harkin/Miller bill a job-killer. But is it really?

An Objective Look at the Minimum Wage Debate

As a free-market conservative, I have never been a big fan of the minimum wage, but it has been around in one form or another in the US since 1938. Like many other federal mandates that I also don’t care for, the minimum wage isnot going to go away. As such, I try to look at it objectively.

There are valid arguments on both sides of this polarizing issue. Very generally speaking, those in favor of the minimum wage argue that it lifts people out of poverty and helps low-skilled workers earn a living wage. Those who oppose the minimum wage argue that the requirement to pay higher and higher wages eliminates jobs, as employers find ways to reduce the number of employees, and thus job creation suffers. Nothing wrong with having different opinions.

But regardless of your opinion, there are some basic givens that don’t change. The first is, companies must earn more than they spend. Second, workers must produce more than they are paid. Third, increasing the minimum wage encourages companies to automate and switch to fewer higher-skilled, more productive workers who are worth the higher rate.

Assuming that minimum wage increases are going to happen from time to time – whether we agree or not – the question is, how much of an increase is too much?

Let’s say that a certain job can be done by one higher-skilled person who makes $18 per hour. Yet that same job could be done by two lower-skilled workers who make $7.25 per hour. In that case, it would make more sense to have the two lower-skilled workers do the job, with the benefit of one extra job added to the economy.

But what happens when the minimum wage is raised to $10.10 per hour as President Obama and Congress are now proposing? In that case, it makes sense to employ the one higher-skilled worker at $18 per hour because the two lower-skilled workers will have to be paid a combined $20.20 per hour.

And that’s before we even factor in Obamacare’s employer healthcare mandate.

The point is, if the minimum wage is hiked from $7.25 to $10.10 – an increase of 39% for most workers, and a whopping 232% for those who are paid mostly from tips – it will have a negative effect on the economy that is still weak.

Will it throw the economy back into a recession? Probably not, since it is to be phased-in over three years. But then again, with 4Q GDP expected to be less than 2%, it doesn’t take much to move the economy into negative territory.

The minimum wage is a federal law; thus, it has to pass in both houses of Congress. You can already see how this is going to play out. The Dems will pass the Harkin/Miller bill in the Senate, while the Republicans in the House are likely to block it. The Dems will chastise the GOP as a bunch of rich folks who want the poor to stay that way. The GOP will argue that the increase is a job killer that will hurt the economy. What else is new?

*****************

In closing, let me offer my sincere belated Veterans Day thanks to all of my readers who served in the US armed forces. Your sacrifices have preserved the freedoms we all enjoy, and to you we are all eternally indebted! Thank you & God bless!!

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management