IN THIS ISSUE:

1. IsFed Responsible For 100% of Stock Market Gains?

2.Fed’s Unprecedented QE Bond Buying Binge

3.Stocks Soar When Fed Buys Bonds & Mortgages

4.Senator Rand Paul to Oppose Janet Yellen…Unless

5.Fed Claims That It is Already Audited Annually

6.Audit the Fed, But Don’t Put Congress in Control

Overview

My guess is that just about everyone reading my E-Letters would agree that the Fed’s massive “quantitative easing” (QE) program has had a bullish effect on the stock markets over the last few years. Several new reports conclude that the Fed’s unprecedented QE bond buying program is responsible for ALL of the stock market advance since the bottom in early 2009.

No doubt, the stock markets have shown a strong tendency to rally during weeks when the Fed is making its huge QE bond and mortgage purchases. But is this the only thing driving the stock markets to record highs? That’s what we’ll look into today.

On a related note, Senator Rand Paul has recently threatened to block the nomination of Janet Yellen as the next Fed chairperson – unless he can get a Senate vote on his new bill to “audit” the Fed. Of course, the Fed claims that it is already audited. So what gives? This is an interesting story that we will want to follow as it plays out; I’ll break it down for you today.

Is Fed Responsible For 100% of Stock Market Gains?

A recent article in Forbes was titled: "You Can Thank Ben Bernanke for 100% of the Stock Market Gains Since 2009." The staff writer, Robert Lenzner, claimed that recent data from J.P. Morgan Asset Management proves that:

“More than 100% of equity market gains since January 2009 have taken place during the weeks the Fed purchased Treasury bonds and mortgages.

And conversely, during the weeks when the Fed did NOT buy Treasuries or mortgage backed bonds, the stock market declined.”

While Mr. Lenzner presented these facts in the beginning of his column, he abruptly veered off to warn about how our out-of-control debt will someday lead to the demise of the economy and the US dollar. Eventually, Lenzner returned to the point that the stock market has gone up in sync with the Fed’s unprecedented quantitative easing program since early 2009.

The fact that stock market gains have been highly correlated with the Fed’s QE purchases is not new. This is why the financial markets and most investors hang on the Fed’s every word in policy statements and meeting minutes whenever the Fed Open Market Committee (FOMC) gets together every six weeks or so.

Lenzner’s point is not that QE has merely been bullish for stocks – we all know that. His point is, based on the J.P. Morgan data, that QE is responsible forALL of the gains in stocks since March 2009 when the bull market began. He offers the following chart:

*Note : Jon Hilsenrath is a writer for the Wall Street Journal. However,

he is widely known as the Fed’s mouthpiece in the media.

Fed’s Unprecedented QE Bond Buying Binge

Quantitative easing is an unconventional monetary policy used by central banks to prevent the money supply from falling when standard monetary policy has become ineffective. A central bank implements quantitative easing by buying specified amounts of financial assets from commercial banks and other private institutions in an effort to increase the monetary base.

The monetary base is defined as the sum of currency in circulation and reserve balances (deposits held by banks and other depository institutions in their accounts at the Federal Reserve). The assumption is that a growing monetary base should stimulate the economy.

Before the Great Recession began, the Fed had apprx. $750 billion of US Treasuries on its balance sheet. In late 2008, the Fed launched what is now known as QE1 by buying $600 million per month in mortgage-backed securities (MBS), in the hopes of reducing mortgage rates and rescuing the housing sector.

The Fed has continued QE, in one form or another, since then. The current QE3 involves monthly purchases of $40 billion in MBS and $45 billion of long-dated Treasury bonds. At the current rate of $85 billion per month, the Fed’s balance sheet will hit a record $4 trillion early next year.

While there is broad disagreement on whether or not this massive QE has really stimulated the economy, there is no doubt that it has significantly boosted the stock markets. As you can see in the chart above, the S&P 500 Index has more thandoubled since QE began.

Stocks Soar When Fed Buys Bonds & Mortgages

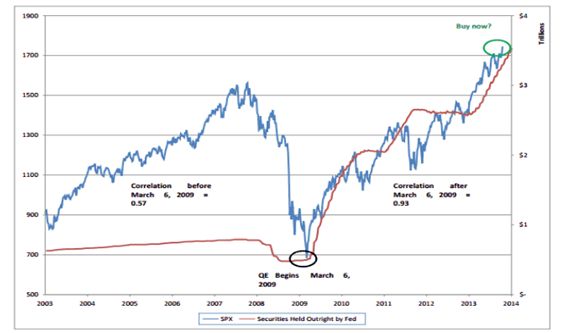

Andreas Calianos of Dome Equity periodically writes financial columns for Minyanville, a popular investment website, and he saw the same Forbes article I referenced above. He was not sure he believed the claim that QE accounted for 100% of stock market gains, so he went to the Treasury website and pulled data from the weekly “Factors Affecting Reserve Balances.”

Specifically, Calianos looked at the weekly average dollar value of securities held outright by the Fed. This includes Treasuries, agency debt and MBS. The chart below graphs 566 weekly observations of this Fed data compared to the S&P 500Index from December 2003 through mid-October, 2013.

A simple correlation of stock prices vs. QE from the start of the data to the S&P 500 low in early March 2009 is quite low at 0.57 as you can see below. However, since that time – March 6, 2009 – the correlation has been a stunning 0.93. Perfect correlation is 1.0. With that knowledge, Calianos was convinced that the Forbes article was valid. Take a look at his chart below:

This chart should scare anyone who looks at it, especially for those in traditional buy-and-hold portfolios! The Fed’s balance sheet is now over $3.7 trillion. The current QE3, or as some call it, “QE-Infinity” ($85 billion/month), was approved on an 11-1 vote in the Fed Open Market Committee in September last year. At each meeting since then, the Fed has voted to continue it, as they did again last Wednesday.

But that will change at some point. At $85 billion a month, that’s over a trillion a year that will stop flowing into the economy, perhaps sooner rather than later!

The bulls cheered when President Obama nominated Janet Yellen to replace Ben Bernanke as the head of the Fed. There has been speculation that Ms. Yellen might go so far as to push for even larger QE purchases. However, even the dovish Ms. Yellen knows that QE must end at some point, or it will begin to devalue the US dollar even more in the future. So, QE will have to slow down at some point, presumably in the near future, and eventually must end altogether.

When that happens, it will almost certainly bevery bad for stocks.

In a recent Bloomberg survey, economists project that QE “tapering” will begin in March 2014, based on the median estimate. But could it happen sooner? Don’t forget, there’s one more FOMC meeting this year on December 17-18 at which time Bernanke will hold his final press conference.

I will be surprised if there is not some additional discussion about ending QE at that last Bernanke FOMC meeting. Also, you can bet the markets will be hanging on Janet Yellen’s every word as she begins her congressional hearings in the days ahead. I have read one intelligent article that argues Ms. Yellen isn’t nearly as dovish as she is perceived. We’ll see.

Senator Rand Paul to Oppose Janet Yellen…Unless

Shortly after President Obama nominated Janet Yellen to replace Ben Bernanke as the next chairperson of the Federal Reserve, Senator Rand Paul (R-Kentucky) threatened to block her confirmation – unless Senate majority leader Harry Reid will allow a vote on Paul’s “Federal Reserve Transparency Act” (S. 209).

The Fed Transparency Act would require a full audit of the central bank’s nearly $4 trillion balance sheet, including gold holdings, but would also mandate an examination of how the Fed operates, of its foreign entanglements and how it determines monetary policy. The Fed’s most private records and correspondence would have to be opened to auditors, along with its un-redacted minutes.

Rand Paul’s father, former Texas congressman Ron Paul, for years called for legislation requiring an audit of the Fed. Finally, in July of last year the House passed an “Audit The Fed Bill” with an overwhelming bipartisan vote of 327-98. Yet it never saw the light of day in the Senate because Majority Leader Reid refused to bring the measure to a vote.

Now Rand Paul is threatening to block the confirmation of Janet Yellen as the next Fed chair if Senator Reid continues to refuse to allow an up or down vote on the Fed Transparency Act. Of course, Rand Paul cannot block Yellen’s confirmation singlehandedly. He will need the support of another 40 Senators or so, and it remains to be seen if he can get it.

Senator Paul made his plans known last week in a letter to Harry Reid. Paul stated:

“As the Senate debates the nomination of the next head of the Federal Reserve, there is no more appropriate time to provide Congress with additional oversight and scrutiny of the actions and decisions of the central bank.” I agree.

Yellen, currently the Fed’s vice chair, is expected to be confirmed, but Paul’s hold could complicate the process if Republicans decide to rally around a call for a vote on his Federal Reserve Transparency Act. In order to get around a hold, 60 votes would be needed.

Fed Claims That It is Already Audited Annually

Federal Reserve officials, including current Chairman Ben Bernanke, oppose Rand Paul’s bill, arguing it would threaten the central bank’s independence by adding a new dimension of political pressure to its monetary policy decisions.

More importantly, the Fed claims that it is already audited annually by the Comptroller General of the United States with additional oversight from the US General Accounting Office. Here is what the Fed says on its own website:

Does the Federal Reserve ever get audited?

Yes, the Board of Governors, the 12 Federal Reserve Banks, and the Federal Reserve System as a whole are all subject to several levels of audit and review:

- TheGovernment Accountability Office (GAO)conducts numerous reviews of Federal Reserve activities.

- TheBoard's financial statements, and its compliance with laws and regulations affecting those statements, are audited annually by an outside auditor retained by theOffice of Inspector General (OIG).

- The Board'sOIG auditsand investigates Board programs and operations as well as those Board functions delegated to the Reserve Banks. Completed and active GAO reviews and completed OIG audits, reviews, and assessments are listed in the Board'sAnnual Report. (Before 2002, the reviews were listed in the Board'sAnnual Report: Budget Review.)

- Thefinancial statements of the Reserve Banksare also audited annually by an independent outside auditor.

In the strictest sense, the Fed is audited. However, those audits and reviews by the OIG and the GAO are based on financial statements that are prepared by the Fed itself. As noted above, Rand Paul (and his father before him) is pushing for a much broader audit scope that would include all of the Fed’s assets, activitiesand internal communications. The Fed doesnot want this!

Audit the Fed, But Don’t Put Congress in Control

As much as I would like to see a full, in-depth audit of the Fed, there are some reasons to be careful about how we do it. The last thing we want to do is turn the Fed into a political football (although some say it already is). Many conservatives, including Ron Paul, would like nothing more than todo away with the Fed entirely. But the fact is, the Fed is simplynot going to go away. So, let’s figure out how to oversee it properly.

A more in-depth, comprehensive fiscal audit of the Fed is not in itself objectionable, even among some Democrats. The problem is having Congress insert itself into the Fed’s internal monetary policy deliberations, which have generally been insulated from the political process.

What Ron Paul (and now his son) has wanted is for the Comptroller General to audit the Fed and then return a “detailed description” of its operations to Congress, along with “recommendations for legislative or administrative action.” In following, Congress would pass regulations on what the Fed can and cannot do.

The problem should be obvious: Political majorities in Washington ebb and flow over the years between Republicans and Democrats. If given defacto control over the Fed, neither party is above using the central bank for its own political purposes. Depending on your political persuasion, control of the Fed could be dangerous no matter which party controls Congress.

This is why many – including Bernanke and Greenspan before him – argue that it’s best to leave the Fed the way it is. But I think that misses the point. I would argue that we could have a much more in-depth audit of the Fed without empowering Congress to regulate its day-to-day operations.

I would also argue that Congress could establish some guidelines for how much money the Fed can create to pursue stimulus programs like QE. As discussed earlier, the Fed’s balance sheet has exploded from $750 billion in late 2007 to almost $4 trillion today. At the least, I would argue that there should be some statutory limit on this.

It will be very interesting to see how this plays out in the days and weeks ahead as the congressional hearings over Janet Yellen’s confirmation to replace Bernanke unfold. It remains to be seen just how hard the members of the Senate Banking Committee will press her on how and when she would propose to start tapering QE purchases. I’ll bet she won’t give a hard answer on that.

Finally, I would much prefer someone more conservatively minded – like Richard Fisher (Dallas Fed) or Charles Plosser (Philly Fed) – to be the next Fed chair. Yet barring some surprise, I expect Yellen will be confirmed. The confirmation hearings are currently expected to begin on November 14.

Best regards,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management