Over the past few years, both “low volatility” and “dividend” strategies have resonated with ETF investors, many of whom were seeking more conservative approaches by which to increase exposure to stocks. Adding further demand for these strategies is a growing body of evidence that suggests an association between both factors and improved risk-adjusted returns.

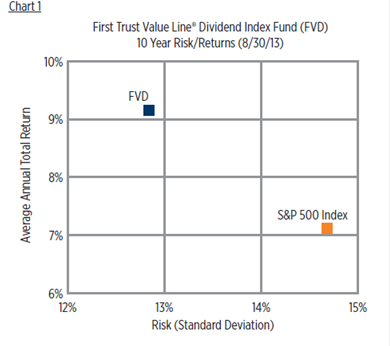

Unfortunately, while there are compelling theoretical justifications for investing in ETFs that track dividend and low-volatility strategies, and many have produced admirable short-term track records, the vast majority of ETFs in both categories lack long-term, real-world track records for investors to inspect. One notable exception, which recently reached its tenth anniversary, is an ETF that seeks less volatile stocks that pay above average dividends: the First Trust Value Line Dividend Index Fund (FVD).

In this newsletter, we will briefly consider the theoretical rationale for investing in low volatility and dividend-seeking strategies, we will explore how the Value Line Dividend Index selects stocks exhibiting these characteristics, and we will evaluate the results of this strategy over the past decade.

The case for low volatility

While traditional assumptions of the efficient market hypothesis suggest a direct link between a stock portfolio’s returns and level of risk taken to achieve those returns (in other words, higher returns can only be achieved by taking more risk), a growing body of research suggests that less volatile stocks may actually deliver similar returns to the broad market, but with less risk, thereby resulting in better-than-expected risk-adjusted returns.1 A number of theoretical explanations have been proposed to explain this suspected anomaly, most of which involve behavioral misjudgments made by investors that result in a tendency to overinvest in riskier (or more volatile) stocks, while underinvesting in less risky (or less volatile) stocks. This pattern may open the door for less volatile stocks to outperform in the future, while more volatile stocks underperform.

One critique against utilizing historical “low volatility” as a standalone factor in constructing an investment portfolio, is that, not only is this data necessarily backward-looking, but it also ignores how potential changes in macroeconomic conditions, company fundamentals, and valuations may cause certain stocks to exhibit substantial changes in volatility from previous periods.

The case for dividends

Over the past several decades, dividend paying stocks have posted higher returns than non-payers, and have often done so with significantly less risk. According to a study from Ned Davis research, from 1972-2012, dividend paying stocks from the S&P 500 Index returned 8.8% per year with a standard deviation of 17.0%, compared to non-payers, which returned 1.6% per year with a standard deviation of 25.6%.2 Among the dividend payers, the best performance with the least amount of risk was achieved by stocks that increased or initiated dividends, which returned 9.5% per year with a standard deviation of 16.2%. The worst performance came from companies that cut or eliminated dividends, which returned -0.3% with a standard deviation of 25.6%.

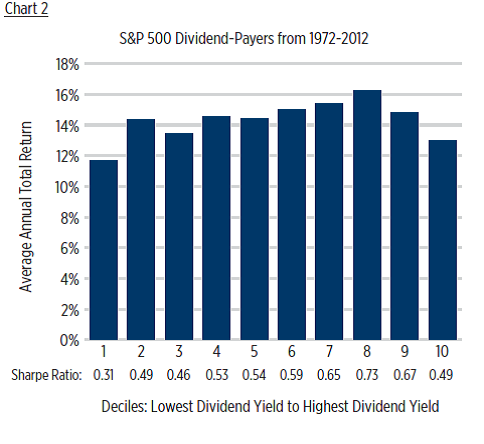

In light of the relationship between dividend paying stocks and better risk-adjusted returns versus non-dividend paying stocks, it’s not too difficult to understand why some investors have wrongly inferred that high dividend yields should correspond with high returns. However, this has not generally been the case. From 1972- 2012, the highest yielding decile of dividend paying stocks in the US produced the second lowest average annual returns among dividend payers, and the fourth worst Sharpe Ratio (see Chart 2 below). This is largely due to the impact of so-called “dividend traps”, stocks whose high yields are due primarily to stock price declines rather than dividend growth. When combined with worsening fundamentals, these companies are often forced to reduce or eliminate future dividend payments.

© First Trust Advisors