Introduction

One of the most widely-accepted and utilized methods of valuing a business in today’s world of modern finance is discounted cash flow (DCF) analysis. Obviously, in order to calculate valuation, practitioners must rely on mathematical formulas. However, the challenge with utilizing mathematical formulas to determine the net present value (NPV) of a future stream of income is in determining the proper inputs. Consequently, the accuracy of our result is subject to the principle “garbage in garbage out.” In other words, our calculations will only be good as the data inputs we use when running our formulas.

Consequently, this presents a real challenge because two of the most important inputs to the discounted cash flow (DCF) formula and net present value (NPV) formula require a modicum of accuracy when estimating the future growth rate of the cash flows and their present value. Moreover, the next most critical input is in choosing the correct (best guess) discount rate to apply. Unfortunately, no precise values are available. Instead, practitioners must rely on making the most reasonable assumptions and/or estimates for these critical inputs that they can. InPart 2AI wrote extensively about estimating future growth rates. In this Part 2B, my focus will turn to discussing the proper discount rate to input into our formulas.

Calculating The Correct Discount Rate

Academics studying and teaching modern finance theory support the utilization of the capital asset pricing model (CAPM) as their preferred method for determining the correct discount rate to apply to their formulas. However, I came across an interesting comment and contrary view posted by a reader who goes by “spielermanin” in the comment thread of an article on the financial blog Seeking Alpha authored by Bob Johnson. I felt this reader’s comment offered excellent insights into the challenge of choosing the correct discount rate and is presented in its entirety as follows:

“spielerman

In a Buffett case study that I use in an MBA finance course I teach, Buffett talks a lot about discount rates.

He uses a discount rate = 30 year treasury rate.

Here is the explanation…

Risk and discount rates. Conventional academic and practitioner thinking held that the more risk one took, the more one should get paid. Thus, discount rates used in determining intrinsic values should be determined by the risk of the cash flows being valued.

The conventional model for estimating discount rates was the capital asset pricing model (CAPM), which added a risk premium to the long-term risk-free rate of return (such as the U.S. Treasury bond yield).

Buffett departed from conventional thinking, by using the rate of return on the long-term (e.g., 30-year) U.S. Treasury bond to discount cash flows.

Defending this practice, Buffett argued that he avoided risk, and therefore should use a “risk-free” discount rate. His firm used almost no debt financing. He focused on companies with predictable and stable earnings. He or his vice chairman, Charlie Munger, sat on the boards of directors where they obtained a candid, inside view of the company and could intervene in decisions of management if necessary. Buffett wrote: I put a heavy weight on certainty. If you do that, the whole idea of a risk factor doesn’t make sense to me. Risk comes from not knowing what you’re doing. We define risk, using dictionary terms, as “the possibility of loss or injury.”

Academics, however, like to define “risk” differently, averring that it is the relative volatility of a stock or a portfolio of stocks—that is, the volatility as compared to that of a large universe of stocks. Employing data bases and statistical skills, these academics compute with precision the “beta” of a stock—its relative volatility in the past—and then build arcane investment and capital allocation theories around this calculation. In their hunger for a single statistic to measure risk, however, they forget a fundamental principle: It is better to be approximately right than precisely wrong.”

Although the capital asset pricing (CAPM) method is the most recommended calculation for determining the discount rate by academics, like Warren Buffett, I prefer a contrarian approach. However, before I delve more deeply into my views on the subject, I offer additional Warren Buffett insights on his views of the proper discount rate courtesy ofWarren Buffett’s Discount Rate used in DCF Posted by whatheheckaboom July 28, 2007.

“At the 1998 Berkshire Hathaway meeting, Buffett was quoted to have said:

“We don’t discount the future cash flows at 9% or 10%; we use the U.S. treasury rate. We try to deal with things about which we are quite certain. You can’t compensate for risk by using a high discount rate.”

With the above comment, I believe that Warren Buffett is highlighting the principle that too high of a discount rate will calculate a net present value (NPV) that would be unrealistically low. Conversely, using a discount rate that is too low will produce a value that is unrealistically high. This reminds me of the “Three Bears” porridge. It is no good if it is too hot, and no good if it’s too cold, to be good it needs to be just right.

“In order to calculate intrinsic value, you take those cash flows that you expect to be generated and you discount them back to their present value – in our case, at the long-term Treasury rate. And that discount rate doesn’t pay you as high a rate as it needs to. But you can use the resulting present value figure that you get by discounting your cash flows back at the long-term Treasury rate as a common yardstick just to have a standard of measurement across all businesses.”

There are two important points that I find valuable with the above quote. The notion of having a common yardstick that provides a standard of measurement across all businesses seem sensible to me. However, I would add that I would replace the word “all” with the word “most.” Second, I have to wonder if Warren Buffett was, in his wildest imagination, anticipating a 30-year treasury rate as low as today’s 3.69%.

“By this time, you would probably think that Buffett simply uses the long-term Treasury rate, while ensuring that the projected cash flows are pretty certain so that you don’t have to increase the discount rate to compensate for earnings risk. However, at the 1994 Berkshire Hathaway meeting, Buffett was quoted:

“In a world of 7% long-term bond rates, we’d certainly want to think we were discounting the after-tax stream of cash at a rate of at least 10%. But that will depend on the certainty that we feel about the business. The more certain we feel about the business, the closer we’re willing to play. We have to feel pretty certain about anything before we’re even interested at all. But there are still degrees of certainty. If we thought we were getting a stream of cash over the thirty years that we felt extremely certain about, we’d use a discount rate that would be somewhat less than if it were one where we expected surprises or where we thought there were a greater possibility of surprises.”

I believe the most relevant point that the above Warren Buffett quote made in 1994 illustrates is Warren Buffett’s willingness to think his way through the process. In other words, he was willing to rationally adjust his views on the discount rate when economic conditions and interest rate levels dictated that he should.

“This is clearly inconsistent with his remarks in 1997 and 1998 where he said he does not adjust the discount rate depending on the riskiness of the projected cash flows.” Also, in the 2000 Chairman’s Letter, he wrote:

“The oracle was Aesop and his enduring, though somewhat incomplete, investment insight was “a bird in the hand is worth two in the bush.” To flesh out this principle, you must answer only three questions. How certain are you that there are indeed birds in the bush? When will they emerge and how many will there be? What is the risk-free interest rate (which we consider to be the yield on long-term U.S. bonds)? If you can answer these three questions, you will know the maximum value of the bush – and the maximum number of the birds you now possess that should be offered for it. And, of course, don’t literally think birds. Think dollars .”

Finally, regarding the above Warren Buffett quotes, I believe the real lesson is the need to always be willing to apply critical thinking with the investment process. To me, I don’t believe Warren Buffett was being inconsistent, as much as he was making rational refinements and adjustments based on the prevailing economic circumstances of the times he was dealing with.

The 15 P/E Ratio As a Short Form DCF Formula

I have often written about how I feel strongly that the P/E ratio of 15 represents a valid and fair valuation proxy for most companies. For starters, the average P/E ratio for the Standard & Poor’s 500 over the past 200 years has been 15 (14 to 16). I do not consider this a coincidence, as my own research has convinced me that there is a valid reason supporting a 15 P/E ratio on most companies. I base this view on the earnings yield that a 15 P/E ratio calculates out to be. This iteration is discovered by reversing the formula to E/P.

Using a simple illustration of what E/P (earnings yield) calculates, assume $1 worth of earnings and divide it by a PE of 15. This equals an earnings yield of approximately 6.67%. Once again, I don’t consider this a coincidence, because 6% closely approximates the long-term return that common stocks have delivered throughout history. Of course, that number often deviates based on valuations and economic conditions, etc. However, during normal times, the 6% return seems like a reliable and reasonable expectation of returns on the average stock.

Furthermore, I added additional color on the subject inpart oneof this series, which included views that Ben Graham had on the relevance of the 15 P/E ratio. However, like most things in finance, it is not perfect or absolute. On the other hand, I do believe a 6% historical normal return, relating to a 6.67% earnings yield, all leave me to believe that a 15 P/E ratio offers a high level of credibility as a reasonable proxy of fair valuation.

With the above said, this also illustrates why I believe that a PE of 15, and its corresponding inverse E/P (earnings yield), also represents a short form formula for consideration as a proxy of discounted cash flows analysis. Therefore, my own research and experience leads me to conclude that it also represents a reasonable discount rate to input into my discounted cash flow (DCF) and/or net present value (NPV) formulas as well.

The Inverse of a 15 P/E as a Reasonable Discount Rate

To elaborate more on the 15 P/E ratio and its inverse as my discount rate of choice, I will once again turn to theF.A.S.T. Graphs™ FundamentalsAnalyzer Research Tool. The formulas used to generate both the historical and forecasting graphs are all based on discounting cash flow analysis (DCF) in one form or another.

The historical earnings and price correlated graphs could be thought of as discounting cash flow analysis (DCF) in reverse. In other words, they represent graphical evidence of how cash flows (earnings) based on a discount rate of 6.67% (P/E of 15) for most companies with earnings growth of 15% or less represent a proxy of fair valuation in real-world applications.

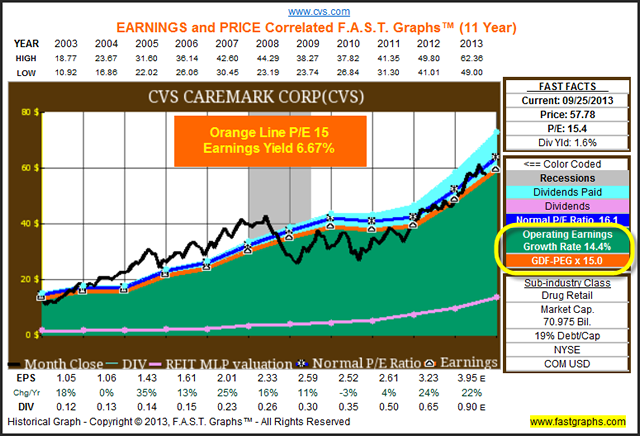

I offer the following 11-year earnings and price correlated graph on CVS Caremark Corp (CVS) as a quintessential example (Note: This is but one example of many that I could have used). The orange line on the graph represents a multiple of 15 times earnings (P/E of15) for each year’s reported operating earnings. Stated more plainly, the orange line is a 15 P/E that also represents an earnings yield of 6.67% across the entire line. However, the slope of the line equals the earnings growth rate. In the CVS Caremark example below, the slope of the orange line is 14.4% which is also their historical earnings growth rate.

Since my contention is that this is a useful proxy of fair valuation, the reader should then ask themselves whether or not the black monthly closing stock price line correlates to the orange earnings justified valuation line. Simple observation would suggest that it does. In other words, over the long run, price follows earnings and reacts to the 15 P/E (the orange line on the graph). At any point when the price deviates either over or above the 15 P/E ratio line, it eventually and inevitably moves back into alignment. Consequently, periods of overvaluation, undervaluation and fair valuation are clearly revealed.

Again, stated more plainly, a P/E ratio of 15 represents a solid, and I believe reliable and reasonable proxy of fair valuation for CVS Caremark. Stated differently, I believe that investing in CVS Caremark at a P/E ratio of 15 or less presents me with a reasonable opportunity for achieving attractive long-term returns. History, at least over the past 11 years, clearly indicates this to be true.

Consequently, I believe it logically follows that a P/E ratio of 15 might also represent a solid and reliable proxy of fair valuation for the future. Of course my hypothesis also requires that CVS Caremark will continue to grow in the future within a reasonable range of future growth that the company achieved in the past. The consensus of 24 analysts reporting to Capital IQ suggest that CVS Caremark is expected to continue growing at an above-average rate in the future.

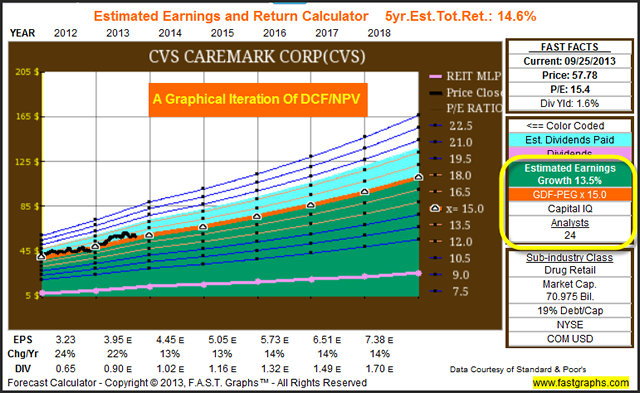

Moreover, as my historical graph above represents discounted cash flow analysis (DCF) in reverse, the estimated earnings and return calculator shown below provides a calculation of future discounted cash flow analysis in its more pure future form. My growth rate expectations of 13.5% are effectively input into the formula, and the P/E ratio of 15 represents my discount rate input.

Summary and Conclusions

The essence of making sound and prudent investment decisions implies that investors must make reasonable assumptions about the future in order to be successful. Moreover, we must also rely on the tools at our disposal to help us make the necessary and important calculations required to make sound long-term decisions. However, we must also recognize and accept that it is impractical to believe that we can make perfect decisions regarding when to buy, sell or hold a common stock.

On the other hand, the last statement in the paragraph above does not imply that we shouldn’t apply our best and most reasonable judgments. As long as we are accurate within a reasonable range of probabilities and possibilities, that it is feasible for us to make sound and profitable long-term investing decisions. These decisions do not need to be perfect to be of value. Instead, they only need to be reasonable and rational. But perhaps most importantly, we must be prepared to continuously monitor those decisions in order to stay current.

Disclosure: No position at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs