The Telecommunications Services Sector Untethered and Poised to Grow

Introduction

Suffice it to say that the Telecommunications Services sector of today is not your grandfather’s Telecommunications Services sector. The explosion, and rapidly becoming ubiquitous implementation, of wireless technologies have been disruptive and game changing. As a result, the very nature of the established stalwarts within this industry have gone through an extraordinary metamorphosis. As wireline has given way to wireless, virtually every company in the Telecommunications Services sector has been forced to change their business models to align themselves with contemporary phone, Internet and cable offerings.

Included in the transformation of every company in this industry has been a massive amount of merger and acquisition activity. Moreover, these massive changes have required the major players to make massive capital investments in order to position themselves relevant in the rapidly-changing Telecommunications environment. Although this industry has always been capital-intensive in nature, the metamorphosis of wireline to wireless has, temporarily at least, increased the need for huge additional capital injections. Therefore, generating profitability over recent history has been a challenge.

On the other hand, there are early signs that these significant investments may pay off in the future. As a result, prospective dividend growth investors interested in investing in this sector would be well-advised to focus more on the future, while ignoring much of what has happened over the recent past. Perhaps for this sector at least, it may well be different this time.

Generally speaking, the Telecommunications Services sector consists of companies that provide wireless and wireline telephone and data services; cable and satellite television distribution services; and Internet access. According to Hoovers reporting in their

Telecommunications Services Industry Overview, the major sources of revenue for the Telecommunications Services sector are wireless services (39 percent of industry revenue); wireline services (33 percent of industry revenue); and cable distribution (24 percent).

Clearly the metamorphosis has significantly progressed; however, it’s important to note that wireline services remain an important part of this industry’s cash flow generation. Moreover, with earnings growth prospects still ill-defined, many managements are focused more on managing cash flows than earnings. Until the changes are complete and the industry’s future more defined, cash flow will be more important regarding maintaining their operations, maintaining their dividends, and perhaps paying down debt and buying back stock. The maintaining of dividends is the most important focal point of this article.

TheTelecommunications Services Sector

This is the tenth in a series of articles designed to find value in today's stock market environment. However, it is the ninth of 10 articles covering the 10 major general sectors. In my first article, I laid the foundation that represents the two primary underlying ideas supporting the need to publish such a treatise. First and foremost, that it is not a stock market; rather it is a market of stocks. Second, that regardless of the level of the general market, there will always be overvalued, undervalued and fairly valued individual stocks to be found.

My first article was titled "Searching For Value Sector By Sector," my second article was titled "Finding Great Value In The Energy Sector." My third article was titled "Finding Value In The Materials Sector Is A Material Thing." My fourth article was titled "The Industrial Sector Offers A Lot Of Value, Dividend Growth And Income." My fifth article was titledBeware The Valuations On The Best Consumer Discretionary Dividend Growth Stocks, and my sixth article was titled,Are Blue-Chip Consumer Staples Worth Today's Premium Valuations?, my seventh articleFor A Healthier Portfolio - Look Here, my eighth articleIs The Financial Crisis Over For Financial Stocks?, andImprove The Productivity Of Your Dividend Growth Portfolio With Technology.

As a refresher, my focus in this and all subsequent articles will be on identifying fairly valued dividend growth stocks within each of the 10 general sectors that can be utilized to fund and support retirement portfolios. Therefore, when I am finished, the individual investor interested in designing their own retirement portfolio should find an ample number of selections to properly diversify a dividend growth portfolio with.

This article will look for undervalued and fairly valued individual companies within the general sector 50-Telecommunications Services. Within this general sector, there are several subsectors, which I list as follows:

Telecommunications Services Conservative

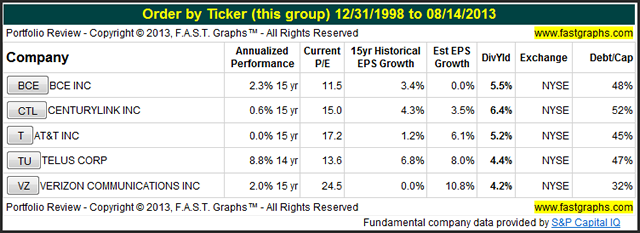

There were only five companies in the Telecommunications Services sector that I felt worthy of further scrutiny by the dividend growth investor. Consequently, instead of featuring a few companies on the conservative list, I will provide fundamental-oriented graphs on all five. However, due to all of the changes within this industry referenced above, historical capital appreciation performance, with the exception of Telus Corp (TU), has been below average. On the other hand, the dividend records of most of these selections have been reasonably consistent, with the exception of CenturyLink Inc (CTL). Consequently, the only performance that I will report will be the annualized performance reported on the portfolio review below. Note that this number includes capital appreciation and dividend income. However, later when I show the Earnings and Price Correlated FAST Graphs™ on each of the following companies, I draw the reader’s attention to the pink line which plots dividends per share. The actual dividends per share are also listed at the bottom of the graphs.

What follows is a graphical look at important fundamentals and metrics on each of the five selections on my conservative list. I will provide a brief description of each company, courtesy of Capital IQ, followed by a series of Earnings and Price Correlated graphs. For those not familiar with theFAST Graphs™research tool, here is a brief descriptionand a linkfor those that would like to know more:

The Orange Line and Green Shaded Area

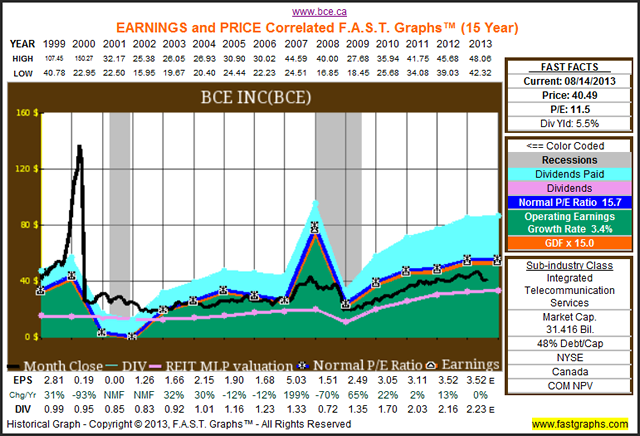

First,F.A.S.T. Graphs™plots the earnings of the company and calculates its growth rate for the time period being graphed. Then as a metaphor for intrinsic value, an orange line with white triangles is drawn based on applying widely-accepted formulas for valuing a business. The orange line represents the same P/E ratio on every point on the graph and is also reported in the orange rectangle in the FAST FACTS box to the right. The green shaded area is simply a mountain chart of the company's earnings each year.

Finally, I will provide FUN Graphs (Fundamental Underlying Numbers), reflecting metrics relevant to each selection’s potential to maintain and/or grow future dividends.

BCE Inc (BCE): Company Description

“BCE Inc. provides communications solutions to residential, business, and wholesale customers primarily in Canada. The company offers local and long distance telephone services under the Bell Home Phone brand; direct-to-home satellite television (TV) services under the Bell TV name; Internet protocol TV services under the Bell Fibe TV brand; and personal video recorders and online access services. It also provides data services, including Internet access services under the Bell Internet name; Internet protocol based services; and information and communications technology solutions. In addition, the company engages in the rental, sale, and maintenance of business terminal equipment; sale of TV set-top boxes; and provision of network installation and maintenance services for third parties. Additionally, it offers wireless voice and data communications products and services.“

BCE Inc: Earnings and Price Correlated Graph

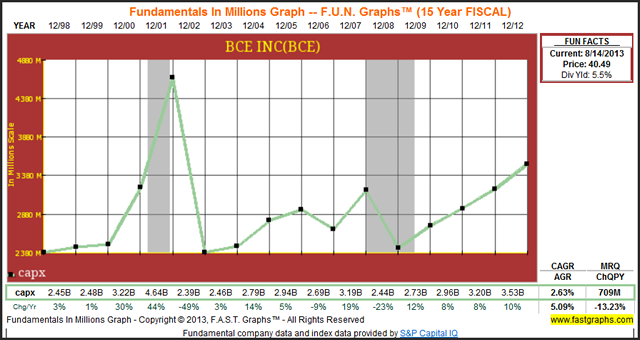

BCE Inc: Capital Expenditures (capx)

The changing Telecommunications’ landscape has required significant capital investment. Note how capex has increased over the last four years from 2.73 Billion in fiscal 2009 to 3.53 Billion in fiscal 2012.

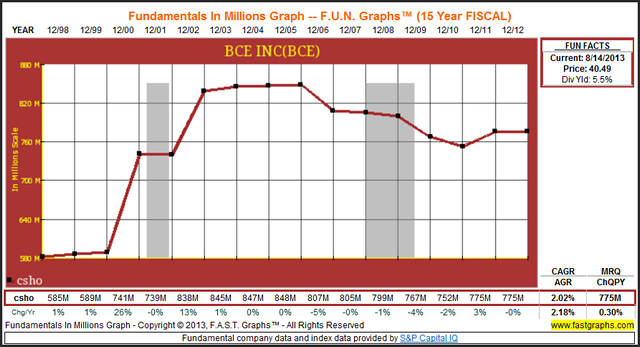

BCE Inc: Common Shares Outstanding (csho)

In order to fund the necessary capex, BCE Inc increased their common shares outstanding (csho) significantly in 2012. More recently since fiscal 2006 the company has embarked on a share count reduction.

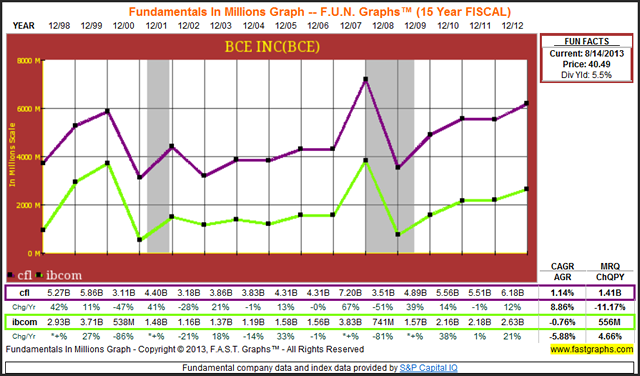

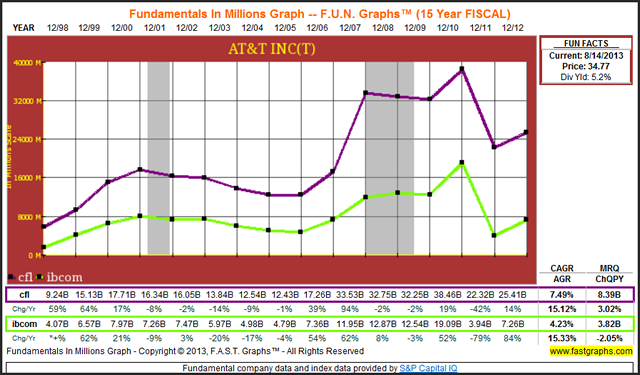

BCE Inc: Cash Flow (cfl) and Income Before Extraordinary Items Available For Common (ibcom)

Fortunately, BCE Inc is generating adequate cash flow to support their capital investment needs. Moreover, strong cash flow generation would indicate the ability to support future dividends, acquisitions and perhaps future share buybacks.

CenturyLink Inc - Company Description

“CenturyLink, Inc. operates as an integrated communications company. The company’s communications services include local and long-distance, network access, private line (including special access), public access, broadband, data, managed hosting (including cloud hosting), colocation, wireless, and video services. It also provides local access and fiber transport services to competitive local exchange carriers and security monitoring.

The company also provides local service in portions of Idaho, Ohio, Wisconsin, Virginia, Texas, Pennsylvania, Montana, Alabama, Nebraska, Indiana, Arkansas, Tennessee, Wyoming, New Jersey, North Dakota, South Dakota, Kansas, Michigan, Louisiana, South Carolina, Illinois, Georgia, Mississippi, Oklahoma, and California. It also operates 54 data centers throughout North America, Europe, and Asia.”

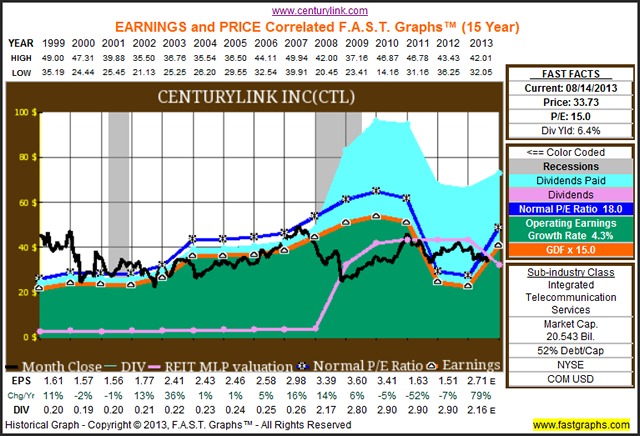

CenturyLink Inc: Earnings and Price Correlated Graph

Clearly CenturyLink Inc appears to be a company in transition. Although the current yield is high, the reader should note the recent dividend cut (the pink line on the graph).

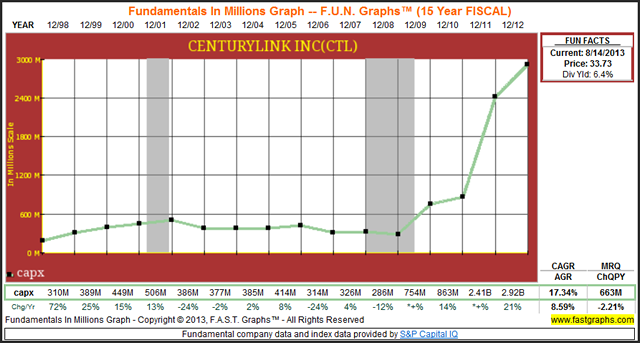

CenturyLink Inc: Capital Expenditures (capx)

CenturyLink Inc. has dramatically increased their capital expenditures under their new capital allocation strategy. Although this strategy appears necessary for the company to establish and maintain future profitable growth in the short run, it brought with it a dividend cut. Consequently, prospective and current investors should carefully consider what the future might hold.

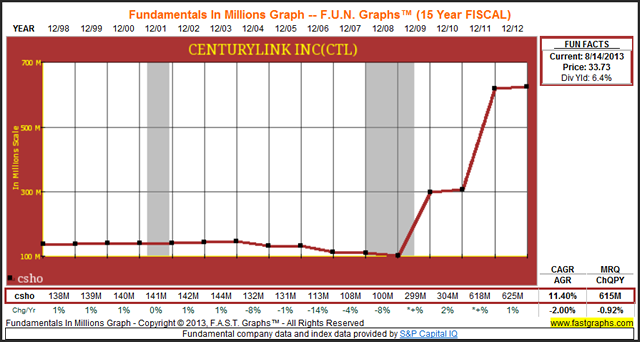

CenturyLink Inc: Common Shares Outstanding (csho)

In order to support their new capital allocation strategy, CenturyLink has dramatically increased their share count. Clearly this is a company in transition.

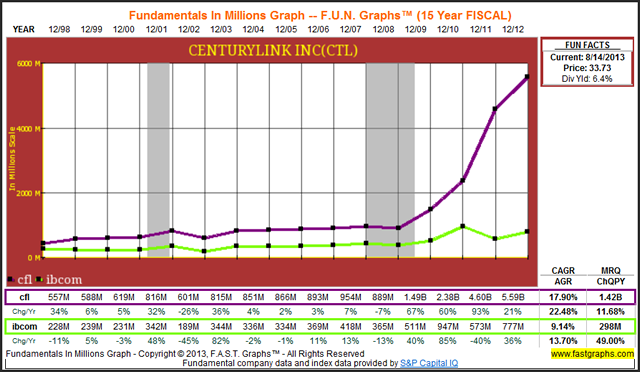

CenturyLink Inc: Cash Flow (cfl) and Income Before Extraordinary Items Available For Common (ibcom)

Strong cash flow generation may be a harbinger for future growth and profitability. However, the company’s current capital allocation policies need to be further scrutinized.

AT&T Inc (T) - Company Description

“AT&T Inc. provides telecommunications services to consumers, businesses, and other providers in the United States and internationally. The company operates in three segments: Wireless, Wireline, and Other. The Wireless segment offers various wireless voice and data communication services, including local wireless communications services, long-distance services, and roaming services. It also sells various handsets, wirelessly enabled computers, and personal computer wireless data cards through its owned stores, agents, or third-party retail stores; and accessories comprising carrying cases, hands-free devices, batteries, battery chargers, and other items to consumers, as well as to agents and third-party distributors. The company was formerly known as SBC Communications Inc. and changed its name to AT&T Inc. in November 2005. AT&T, Inc. was founded in 1983 and is based in Dallas, Texas.”

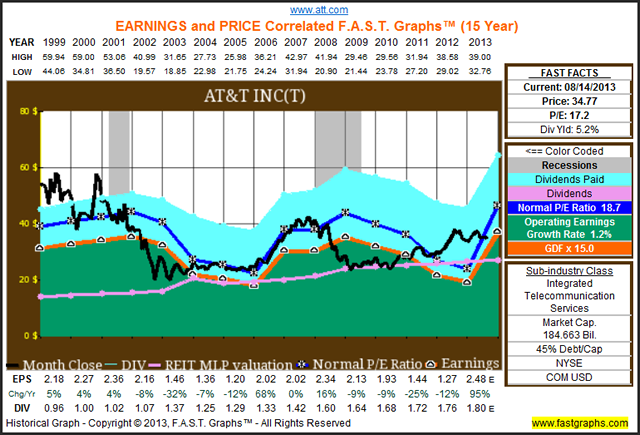

AT&T Inc: Earnings and Price Correlated Graph

The evolving landscape of the Telecommunications Services sector has had a profound impact on AT&T’s historical earnings. However, through it all, the company has maintained a steady dividend to the benefit of its shareholders.

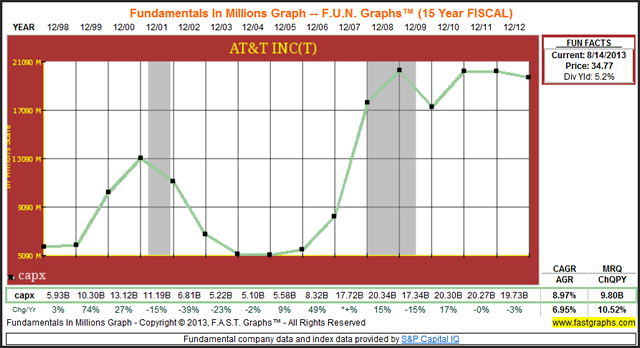

AT&T Inc: Capital Expenditures (capx)

Like most other Telecommunications Services sector companies, AT&T Inc has also dramatically increased capex in recent years. However, capex has leveled off over the last five years.

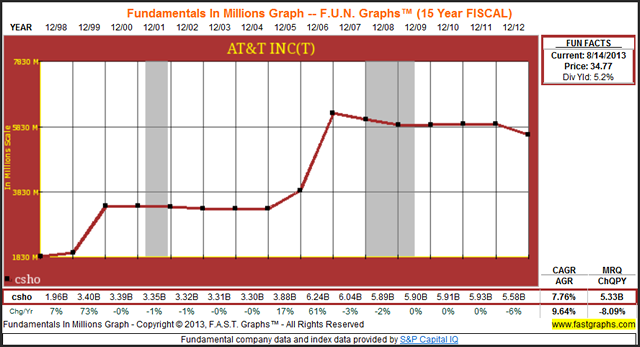

AT&T Inc: Common Shares Outstanding (csho)

After a period of increasing share count, AT&T Inc has been slowly reducing common shares outstanding since fiscal 2007. Common shares outstanding have fallen from 6.04 Billion in fiscal 2007 to 5.58 Billion shares in 2012.

AT&T Inc: Cash Flow (cfl) and Income Before Extraordinary Items Available For Common (ibcom)

After weakening in fiscal 2011, AT&T’s cash flows appear to be strengthening again. This is a metric that current and prospective investors would be wise to pay close attention to. Under the new Telecommunications Services sector paradigm, cash flows are paramount for dividend growth investors.

Telus Corp - Company Description

“TELUS Corporation provides telecommunications products and services primarily in Canada. Its telecommunications products and services include wireless, data, Internet protocol, voice, and television. The company operates through two segments, Wireless and Wireline. The Wireless segment is involved in the voice, data, and equipment sales. This segment sells wireless handsets to resellers and customer premises equipment. The Wireline segment offers data services, which include television; Internet, enhanced data and hosting services; and managed and legacy data services, as well as voice local, voice long distance, and other telecommunications services. As of June 11, 2013, the company had approximately 13.2 million subscriber connections, which included 7.7 million wireless subscribers, 3.4 million wireline network access lines, 1.4 million Internet subscribers, and 712,000 TELUS TV subscribers. TELUS Corporation was founded in 1993 and is based in Vancouver, Canada.”

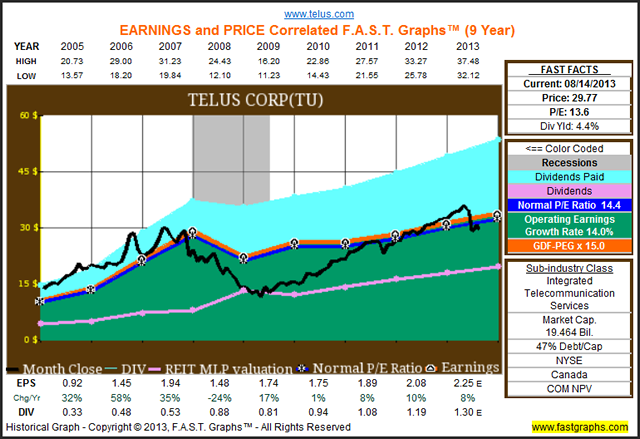

Telus Corp: Earnings and Price Correlated Graph

Telus Corp is one of the few companies in the Telecommunications Services sector that has shown above-average earnings growth in recent years. This has also translated into steady dividend growth that has averaged 21.2% since fiscal 2005.

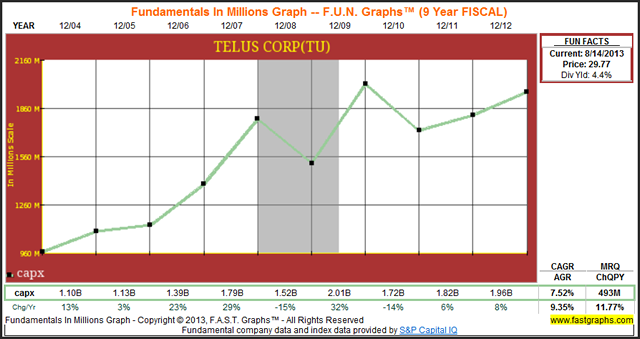

Telus Corp: Capital Expenditures (capx)

In spite of strong operating performance, like its peers, Telus Corp has made substantial capex investments in recent years. Nevertheless, management has been capable of maintaining profitability.

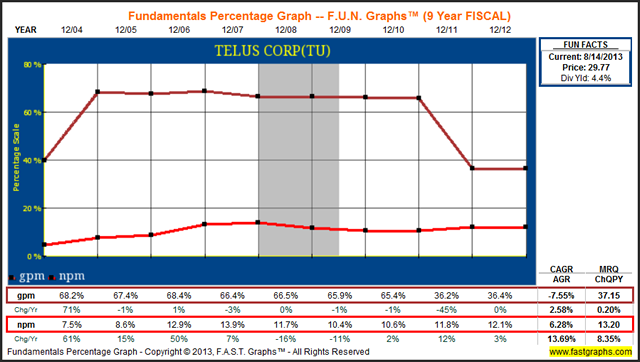

Telus Corp: Gross Profit Margin (gpm) and Net Profit Margin (npm)

Gross profit margin has fallen in fiscal 2011 and 2012 from 65.4% to 36.2% and 36.4% respectively. Nevertheless, the company has maintained a net profit margin of 11.8% and 12.1% for fiscal years 2011 and 2012.

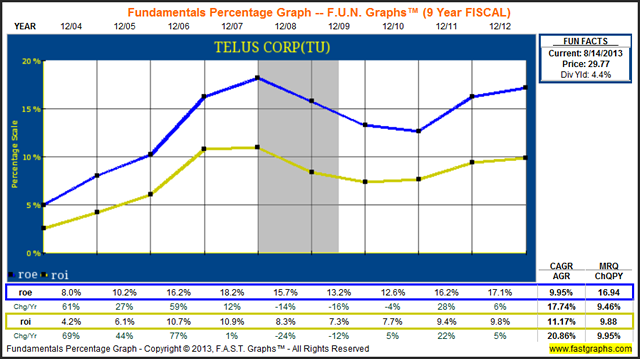

Telus Corp: Return on Equity (roe) and Return on Invested Capital (roi)

Even though Telus Corp has made substantial invesmtents in their business in recent years, their returns on equity and returns on invested capital have increased. Consequently, it appears that their investment strategies are paying off.

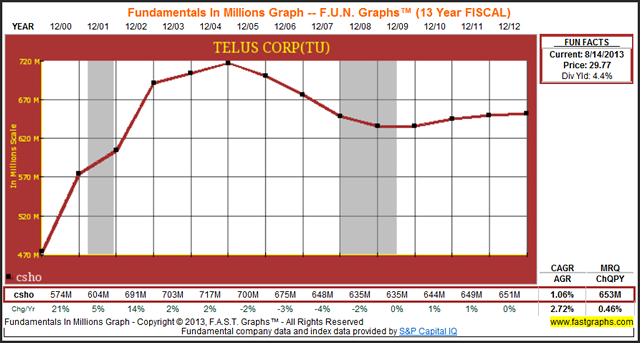

Telus Corp: Common Shares Outstanding (csho)

After initially increasing common shares outstanding in order to fund their capex needs, Telus Corp has dramatically reduced their share count since fiscal 2005. However, since fiscal 2010 share count has been modestly increasing.

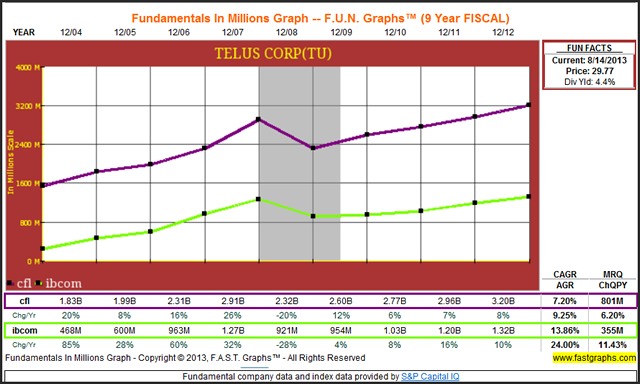

Telus Corp: Cash Flow (cfl) and Income Before Extraordinary Items Available For Common (ibcom)

In spite of all the changes with Telus Corp’s capital structure cited above, management has been able to maintain and grow cash flows. This augers well for future dividends and dividend growth.

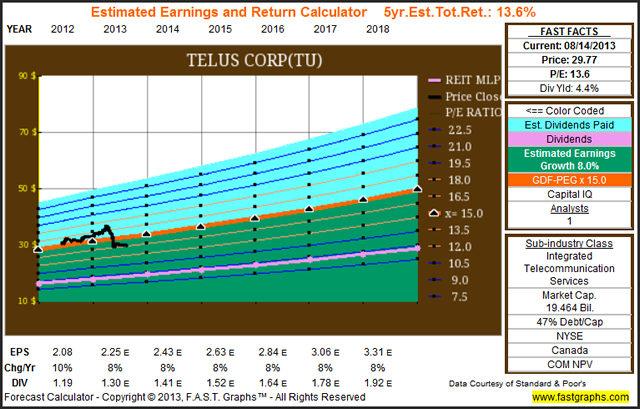

Telus Corp: Forecasting Graph

Since Telus Corp has produced the best earnings and dividend growth record among the group, I felt it appropriate to provide a look at the consensus estimates for future growth. Although there is only 1 analyst reporting to Capital IQ, a cross-check with Zacks shows that 8 analysts corroborate the forecast future 5-year growth rate of 8%.

Verizon Communications Inc (VZ) - Company Description

“Verizon Communications Inc., through its subsidiaries, provides communications, information and entertainment products and services to consumers, businesses, and governmental agencies worldwide. Its Verizon Wireless segment offers access to various wireless voice and data services comprising Internet access through smart phones and basic phones, and notebook computers and tablets; messaging services, which enable customers to send and receive text, picture, and video messages; and consumer-focused and business-focused multimedia applications. This segment also provides location-based services; global data services; HomeFusion Broadband, a high-speed Internet service for homes; other connection-related services, such as data access and value added services to support telemetry-type applications; and machine-to-machine services that support devices used in healthcare, manufacturing, utilities, distribution, and consumer products markets, as well as sells smart phones and basic phones, tablets, and other Internet access devices.

The company’s Wireline segment offers video services over its fiber-optic network; data Services comprising high-speed Internet and FiOS broadband data products, as well as local exchange capacity, managed, mobility, and security services; voice services, such as local exchange, regional, long distance, wire maintenance, and voice messaging services, as well as VoIP, and landline and wireless services; and local dial tone and broadband services to local, long distance, and other carriers. This segment also provides networking products and solutions, such as private Internet protocol services, and Ethernet access and ring services; and infrastructure and cloud services. As of June 20, 2013, it served 98.9 million retail customers. The company was formerly known as Bell Atlantic Corporation and changed its name to Verizon Communications Inc. in June 2000. Verizon Communications Inc. was founded in 1983 and is based in New York, New York.”

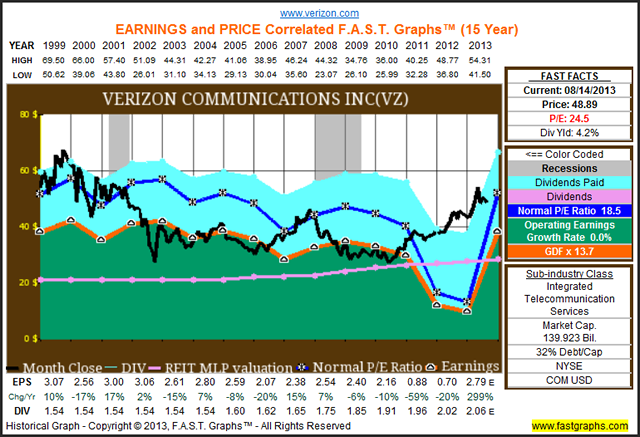

Verizon Communications Inc: Earnings and Price Correlated Graph

Verizon Communications Inc has also experienced earnings stress as the Telecommunications Services sector has evolved from wireline to wireless. However, their dividend record has shown steady, but low growth (the pink line).

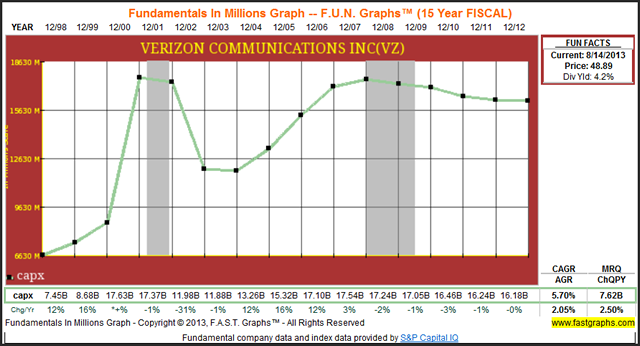

Verizon Communications Inc: Capital Expenditures (capx)

Although Verizon Communications’ capital expenditures dramatically increased from fiscal 1998 to fiscal 2000, they have maintained a reasonable investment strategy in recent years. In fact, capex has shown a moderate and steady decline since fiscal 2008.

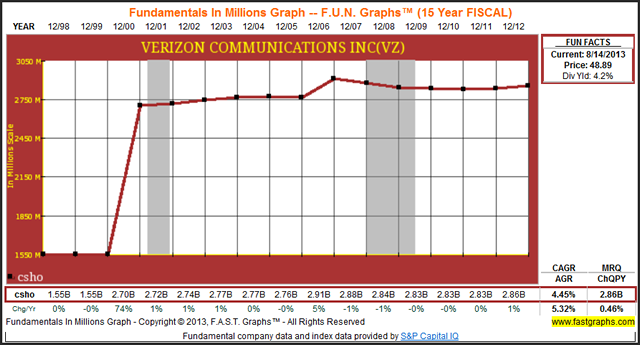

Verizon Communications Inc: Common Shares Outstanding (csho)

After following suit with their peers, Verizon Communications dramatically increased their share count in fiscal 2000. However, Verizon Communications has maintained a consistent share count ever since.

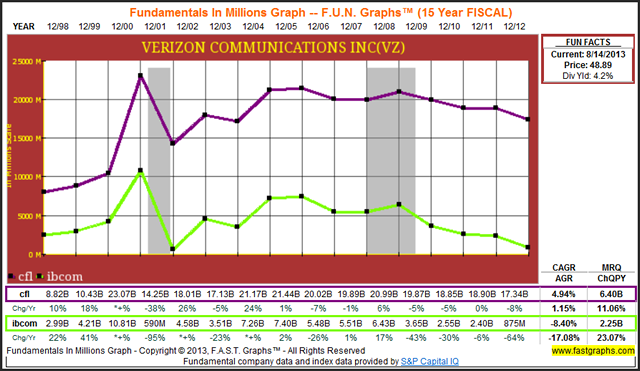

Verizon Communications Inc: Cash Flow (cfl) and Income Before Extraordinary Items Available For Common (ibcom)

One area of concern regarding Verizon Communications has been a steady reduction in cash flow since the Great Recession of 2008. This is a metric that current and prospective shareholders would be wise to follow closely.

Telecommunications Services Aggressive

The following portfolio review provides a list of additional Telecommunications Services sectors’ candidates that prospective investors may want to look at. However, I am not sure the label “aggressive” fits any companies within this sector. Nevertheless, I provide the following candidates for further review. On the other hand, I will not feature any company from this list, and instead suggest that prospective investors might be best served by looking for Telecommunications Services companies that I covered in the conservative portfolio above.

Summary and Conclusions

My review of the Telecommunications Services sector found a group of companies that were clearly in transition. Consequently, historical results, more than any other sector thus far reviewed, offer less insight than found in other sectors. In other words, more than any other sector, the dividend growth investor looking for a growing-dividend income stream for their retirement portfolios should focus on the future prospects of this industry.

Moreover, I suggest that further comprehensive research and due diligence is an absolute must before investing in any company within the Telecommunications Services sector. Change is rarely comfortable, and change is, has been, and most certainly will be the name of the game for the Telecommunications Services sector. But even though change is rarely comfortable, that doesn’t mean that it is necessarily bad. Competition within this sector is high, merger and acquisition activity will more likely than not continue, and innovation is manifesting at a feverish pace. With all this disruption comes higher risk, and this can lead to either higher returns or disastrous ones. Consequently, caveat emptor may more profoundly apply for the Telecommunications Services sector than for any other sector I have thus far reviewed.

My next and final article within this series will cover Sector 55 – Utilities.

Disclosure: Long T and VZ at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs