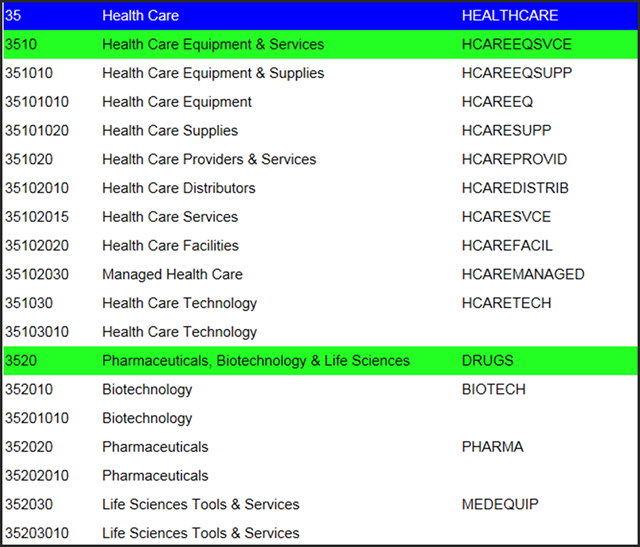

The Health Care sector is comprised of many diverse companies, as can be seen from the list of subsectors provided below. Historically the Health Care sector has been comprised of a significant number of companies with above-average growth rates of earnings. Consequently, a majority of the companies comprising the Health Care sector could be thought of as growth stocks over dividend growth stocks.

One of the primary reasons for this was that the sector was benefiting from the tailwinds of the powerful demographic forces of an aging population. Additionally, there were many scientific advances that also provided above-average growth to many companies in this sector. As a result, health care stocks were once considered defensive because they were mostly unaffected by economic weakness.

Big pharma was a major beneficiary of these two growth factors for many years. However, big pharma names like Pfizer (PFE) and Merck (MRK) were also classic above-average growing blue-chip dividend stocks. In days gone past, big pharma, and many other quality companies in the Health Care sector could be counted on to grow earnings, and dividends if they pay any, like clockwork.

However, since the recession of 2001, the characteristics and the attributes of big pharma changed dramatically. Instead of generating quintessential earnings growth patterns, their operating results became flatter (slower) and even cyclical. Consequently, it’s imperative that investor attitudes towards big pharma adjust to the changing operating environment of today. This will be elaborated on later.

The economic environment for the Health Care sector today has clearly changed and evolved. For starters, it has become more and more difficult for large multi-billion-dollar market cap multi-national drug companies to produce enough new blockbuster drugs to support their growth. Additionally, companies in the biotech segment have been developing more promising therapies that threaten blockbuster drugs from gaining traction. However, these are not the only headwinds now facing big pharma, and the entire Health Care sector for the matter. We now have the passage of the Health Care Reform Act that has brought significant uncertainty as to the ability of the entire sector’s capability for profitable future growth.

Nevertheless, the tailwinds of powerful demographics, mainly an aging population, cannot be ignored. Moreover, the jury is still out as to whether or not the Health Care Reform Act, aka Obamacare, will be a boon or a detriment to this sector. Consequently, valuations for many companies in this broad sector remain below historical norms, as well as intrinsic valuation, based on historical results. The real question that must be successfully answered is what is going to happen to future growth? The uncertainty behind this question is more likely than not the major factor keeping many of these companies at historically low valuations.

The Health Care Sector

This is the seventh in a series of articles designed to find value in today's stock market environment. However, it is the sixth of 10 articles covering the 10 major general sectors. In my first article, I laid the foundation that represents the two primary underlying ideas supporting the need to publish such a treatise. First and foremost, that it is not a stock market; rather it is a market of stocks. Second, that regardless of the level of the general market, there will always be overvalued, undervalued and fairly valued individual stocks to be found.

My first article was titled "Searching For Value Sector By Sector," my second article was titled "Finding Great Value In The Energy Sector." My third article was titled "Finding Value In The Materials Sector Is A Material Thing." My fourth article was titled "The Industrial Sector Offers A Lot Of Value, Dividend Growth And Income." My fifth article was titledBeware The Valuations On The Best Consumer Discretionary Dividend Growth Stocks, and my sixth article was titled,Are Blue-Chip Consumer Staples Worth Today's Premium Valuations?

As a refresher, my focus in this and all subsequent articles will be on identifying fairly valued dividend growth stocks within each of the 10 general sectors that can be utilized to fund and support retirement portfolios. Therefore, when I am finished, the individual investor interested in designing their own retirement portfolio should find an ample number of selections to properly diversify a dividend growth portfolio with.

This article will look for undervalued and fairly valued individual companies within the general sector 35-Health Care. Within this general sector, there are several subsectors, which I list as follows:

Since I am such a stickler for valuation, I am not willing to pay more for even the best company than I believe it is worth, based on fundamental values. Consequently, several of the best-of-breed health care companies were cut from my list based either on overvaluation, a lack of available estimates, or in some cases, negative estimates.

The primary dividend stalwarts that I've excluded based on what I've stated above are listed in alphabetical order as follows:

AmerisourceBergen Corp (ABC), AstraZeneca (AZN), Becton Dickinson & Co (BDX), Bristol-Myers Squibb (BMY), Eli Lilly & Co (LLY), Novartis (NVS), Owens & Minor, Inc (OMI), Patterson Companies (PDCO), Sanofi( SNY), STERIS Corp (STE).

Aggressive Health Care Sector Portfolio

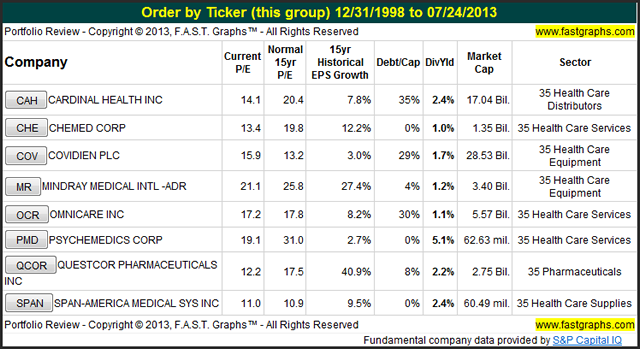

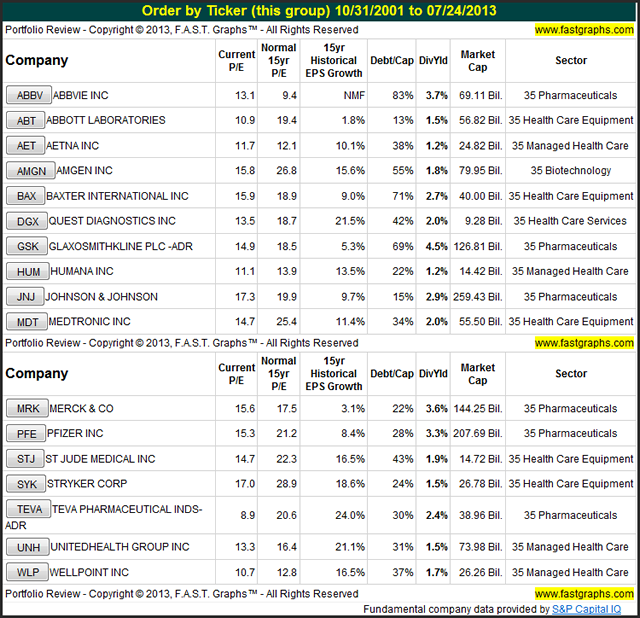

My screen produced eight aggressive health care dividend paying stocks that I felt were worthy of further scrutiny based on current valuation. The following portfolio review lists them in alphabetical order. There are many reasons why I classify these as aggressive over conservative. For example, it could be based on size, short histories of profitability, the natures of their businesses, etc.

Questcor Pharmaceuticals Inc (QCOR)

My featured selection from the aggressive portfolio of Health Care sector companies is Questcor Pharmaceuticals Inc. I chose this company because it provides characteristics and benefits that might satisfy the total return investor as well as the income-oriented dividend growth investor. Furthermore, the company operates as a biopharmaceutical focused on profitable niche markets. The following description is taken directly from their website:

“We are a biopharmaceutical company focused on the treatment of patients with serious, difficult-to-treat autoimmune and inflammatory disorders. Our efforts are currently focused on the fields of neurology, nephrology and rheumatology, areas of medicine which have significant unmet medical needs.

Our main product is H.P Acthar®Gel (repository corticotropin injection), a naturally-derived formulation of adrenocorticotropic hormones used in a variety of disorders having an inflammatory component.

We are currently supporting research in a number of rare conditions, where there is significant unmet need for treatment alternatives to standard therapies. We are also actively supporting research efforts to better understand disease processes and therapeutic mechanisms of action in conditions where Acthar might potentially play a role in treatment.”

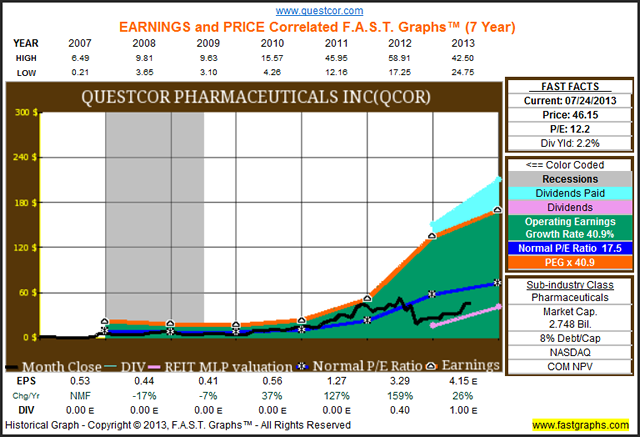

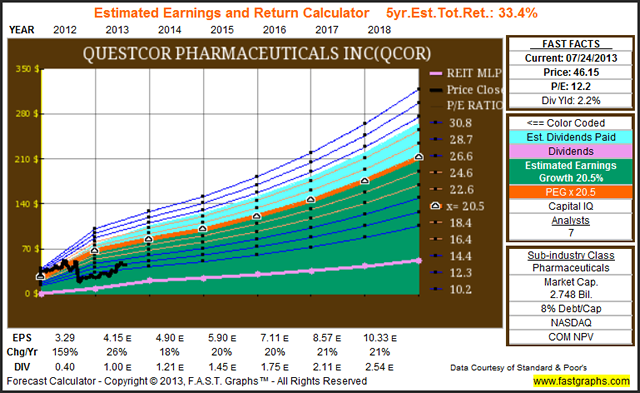

The following Earnings and Price Correlated FAST Graphreveals the opportunity behind Questcor Pharmaceuticals. Earnings growth has averaged 39.7% (the slope and P/E ratio of the orange line) and the company has commenced paying a dividend since December 2012, as depicted by the light blue shaded area. Clearly, the historical operating results have been nothing short of spectacular and the company currently offers an above-market dividend yield of 2.1%. Furthermore, a 2.7 billion-dollar market cap leaves plenty of room for future growth, and the 8% debt to capital ratio implies healthy financial shape.

Perhaps most importantly, Mr. Market has historically valued this company at a discount to its growth rate by applying a normal P/E ratio of 17.5 (the dark blue line). Consequently, it is arguable that the current P/E of 12.2 reflects the uncertainties of the Health Care Reform Act discussed above.

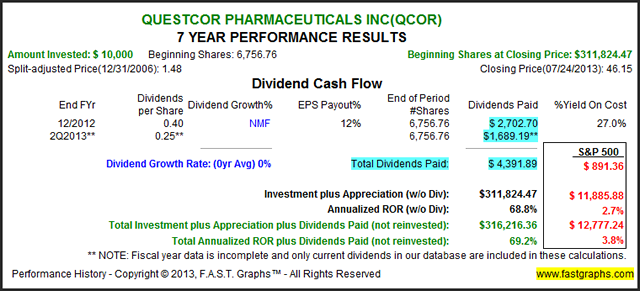

In spite of the fact that Mr. Market has shown a penchant for discounting the intrinsic value of this quality biopharmaceutical, historical performance has been spectacular. A $10,000 investment on December 31, 2006 today would be worth $311,824.47, representing an annualized rate of return of 68.8%. Add in over $4,000 in dividends, and the total annualized return, including dividends, becomes 69.2%. Consequently, Questcor has lavishly rewarded shareholders with both above-average income and significant capital appreciation. If this doesn’t prove that it is a market of stocks rather than a stock market, then I don’t see how anything can.

The consensus of 7 analysts reporting to Standard & Poor’s Capital IQ expect continued above average earnings growth of 20.5% per annum for Questcor. Accordingly, although it would be naive to expect to duplicate Questcor’s historical performance, there appears to be significant future performance left in this interesting small cap biopharmaceutical. Further due diligence is suggested, but certainly appears worthy of the effort.

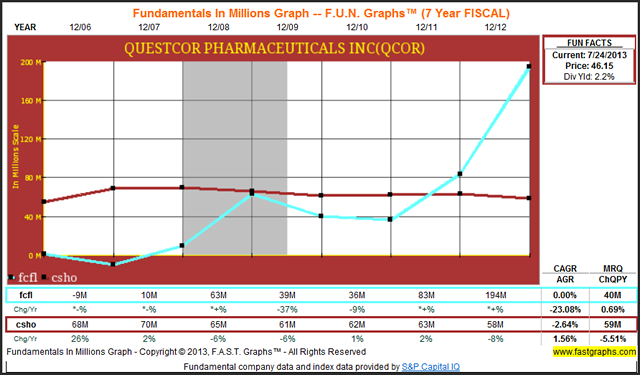

Finally, courtesy of FUN Graphs, there are two additional fundamental metrics that appear to support a closer look at Questcor. Free cash flow (fcfl) has advanced from 10 million dollars in 2007 to over 194 million dollars by year-end fiscal 2012. This rendition of free cash flow is after dividends have been paid, indicating that not only is the current dividend safe, but there appears to be ample room for it to continue to grow.

In addition to the initiation of a generous dividend, Questcor has also been rewarding shareholders by buying back their shares. Share count has fallen from 68 million shares in 2006 to 58 million shares by fiscal year-end 2012. Reducing share count supports continued earnings growth going forward.

Conservative Health Care Sector Portfolio

My screen produced 17 conservative Health Care dividend paying stocks that I felt were worthy of further scrutiny based on current valuation. The following portfolio review lists them in alphabetical order.

Merck & Co (MRK)

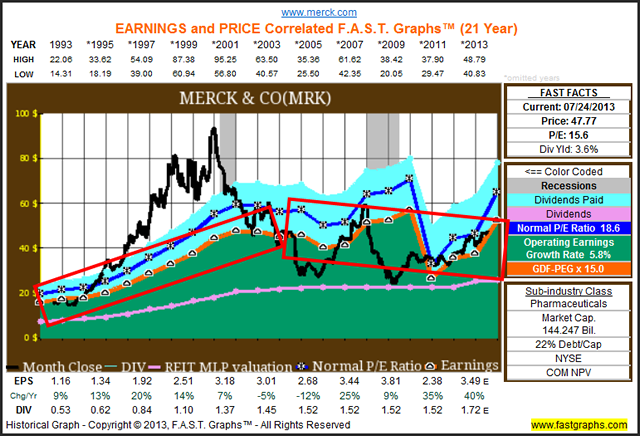

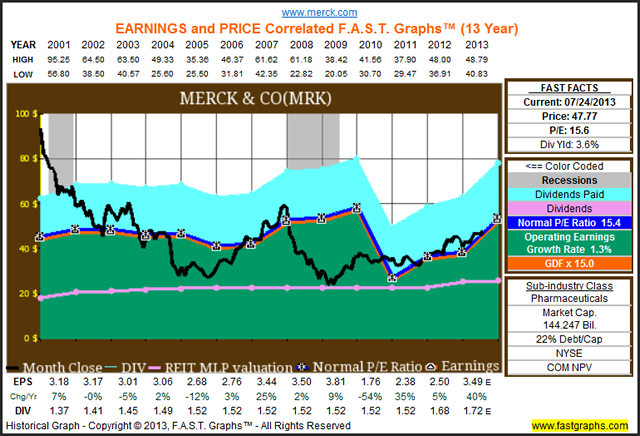

As I discussed in the opening paragraph of this article, and before I feature a few of my favorite conservative dividend paying Health Care stocks, I felt it would be useful to review a sampling of the big pharma company, Merck & Co. As the Earnings and Price Correlated FAST Graph on Merck & Co reveals, from 1993 to the end of 2001, Merck generated very consistent and strong historical earnings growth (note the steepness of the slope of the orange line). It is also interesting to note that this was during the irrational exuberant period that was characterized by excessive overvaluation.

However, since the recession of 2001, which I believe only coincidently correlates, Merck & Co’s earnings record became very inconsistent and cyclical. This same attributes of flat and inconsistent earnings growth over the last 15 years can also be seen with most of the other big pharma companies such as Pfizer, Astra Zeneca, Bristol Meyers, etc. Perhaps they became too big and their pipelines too meager to support continuing above-average growth. This radical shift and change in the operating performance of big pharma is an extremely important fact that investors must consider and factor into their thinking. I believe that many investors continue to see big pharma as the consistent growth stocks they once were. This is a mistake, as evidenced by their historical operating results.

By cutting eight years off of the above graph, we see that since 2001 Merck has only been able to generate earnings growth of 1.3% per annum. Moreover, not only has the growth been flat, but a significant amount of cyclicality has manifested itself during recent years. Although Merck currently provides a very attractive 3.6% dividend yield, prospective investors should consider Merck’s recent anemic level of growth.

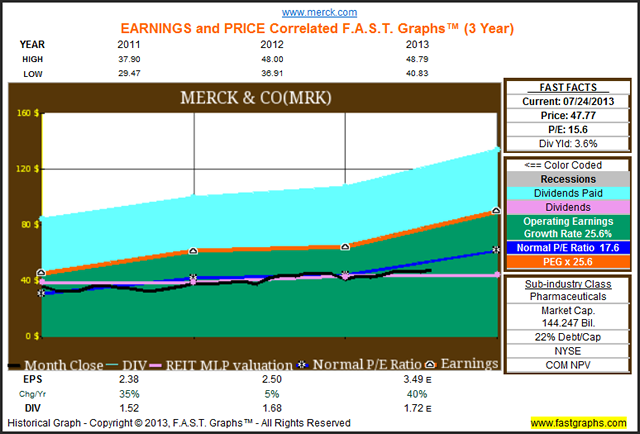

On the other hand, since calendar year 2011 Merck has once again generated some impressive growth averaging 25.6% per annum. But investors should also consider that much of this growth is a result of coming off of a low earnings base that was established in 2010 (see above graph). The point that I am trying to make, is that a company’s growth rate can be very dynamic. If you only relied on earnings growth over the last three years, Merck & Co would look extremely attractive. On the other hand, if you take a longer view of history, your attitude and opinion about the company would change. The morale of this story is statistics in a vacuum can be very misleading.

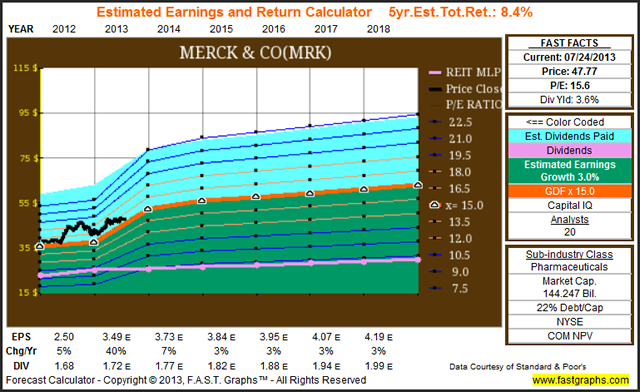

When looking to the future for Merck, the consensus of 20 analysts reporting to Standard & Poor’s Capital IQ are only forecasting earnings growth over the next five years at 3% per annum. Consequently, expectations of the future are more in alignment with the longer term 12-year history than they are with a more recent two-and-a-half year history. In short, this is not your grandfather’s big pharma anymore. Investors’ attitudes should adjust accordingly.

Amgen Inc (AMGN)

My first featured conservative dividend growth stock in the Health Care sector is Amgen Inc. This biotechnology company represents the new breed of pharmaceutical company that has been displacing the incumbent big pharma. The following taken directly from their website provides a brief description of Amgen:

“Amgen strives to serve patients by transforming the promise of science and biotechnology into therapies that have the power to restore health or even save lives. In everything we do, we aim to fulfill our mission to serve patients. And every step of the way, we are guided by the values that define us.”

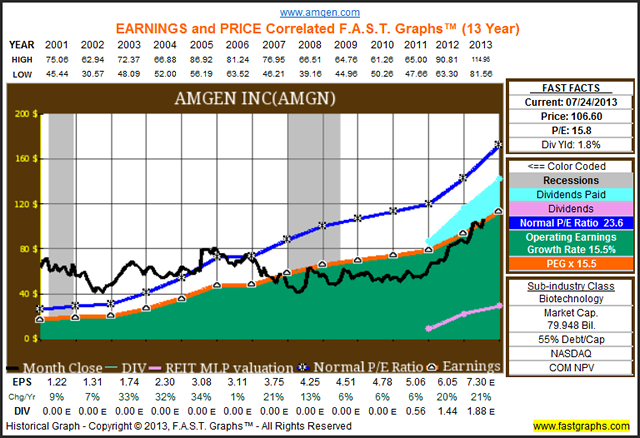

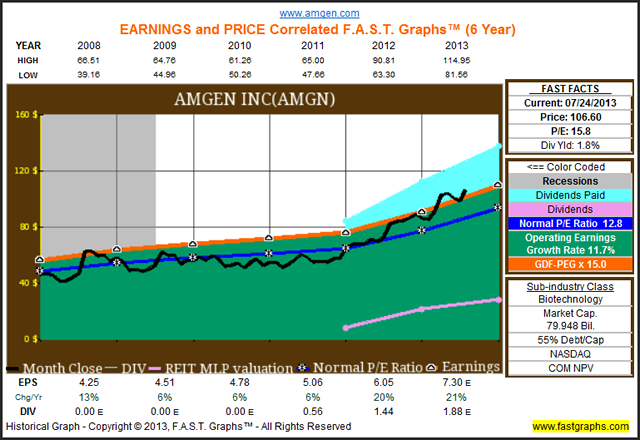

The following Earnings and Price Correlated 13-year FAST Graph on Amgen illustrates how biotechnology has supplanted big pharma as the pharmaceutical growth stocks of modern times. While the Merck example above produced very anemic growth since 2001, the biotechnology stalwart Amgen was able to grow earnings at 15.5% per annum. Although the company suffered from overvaluation prior to the Great Recession, its stock price has, as we will soon see, come into alignment with earnings justified valuations. Moreover, the company instituted a dividend in 2012, which now turns it into an early stage dividend growth stock.

The following Earnings and Price Correlated FAST Graph since the Great Recession, shows that Amgen produced consistent earnings growth of 11.7% per annum. But most importantly, it shows that Amgen’s stock price has correlated very closely to its operating earnings growth since that time. With a current blended P/E ratio of 15.8, Amgen appears fairly valued today.

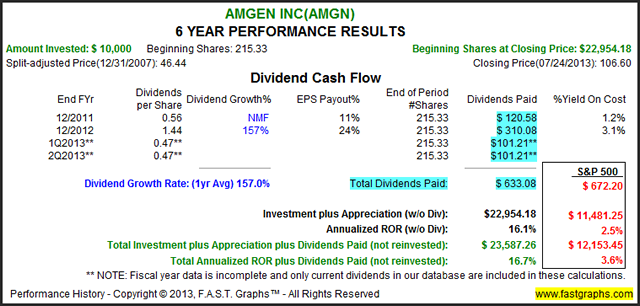

The associated performance of Amgen since 12/31/2007 shows that Amgen’s shareholders were rewarded with a rate of return that is closely correlated to the company’s earnings growth rate. This illustrates the power and benefit of investing in strong growth at a reasonable price. Amgen’s recent dividend sweetened the pot even more.

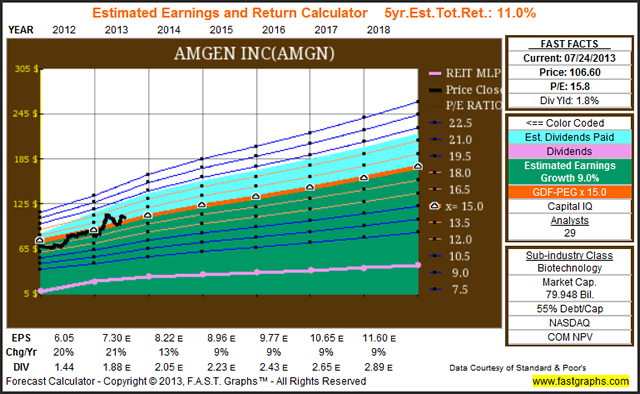

In contrast to the big pharma company Merck, the consensus of 29 analysts reporting to Standard & Poor’s Capital IQ expect Amgen to grow earnings over the next five years at an above-average rate of 9% per annum. Consequently, this further corroborates the notion that biotechnology companies like Amgen represent the new growth segment of the pharmaceutical subsector.

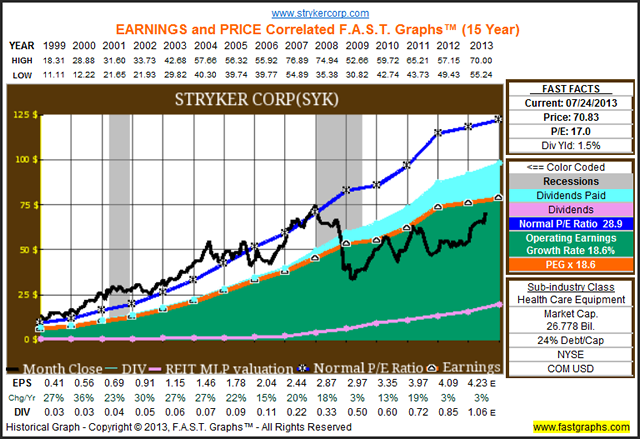

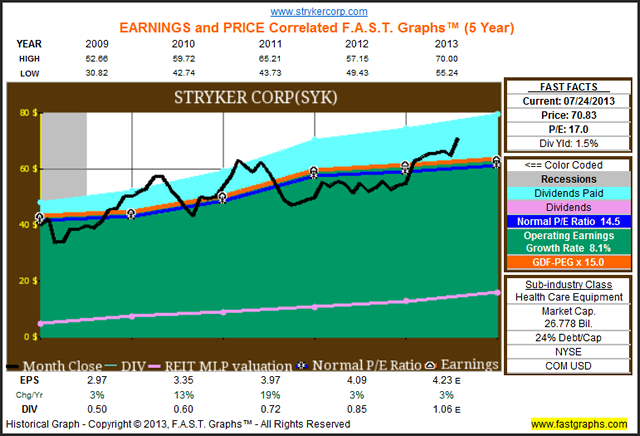

Stryker Corp (SYK)

Stryker Corp is one of the premier companies in the medical equipment and appliance subsector of health care that stands to benefit from the powerful tailwinds of our aging population. The following brief excerpt from their website describes the company:

“Stryker is one of the world’s leading medical technology companies and is dedicated to helping healthcare professionals perform their jobs more efficiently while enhancing patient care. The Company offers a diverse array of innovative medical technologies, including reconstructive, medical and surgical, and neurotechnology and spine products to help people lead more active and more satisfying lives.”

Perhaps the most important take-away from the Earnings and Price Correlated FAST Graph on Stryker is how the Great Recession of 2008 has provided the opportunity to invest in this subsector at more attractive valuations that are more in alignment with intrinsic value.

Prior to the Great Recession Stryker Corp, as well as peer companies such as Medtronic (MDT), were priced at premium valuations by Mr. Market. However, as the following post-recession Earnings and Price Correlated FAST Graph clearly reveals, Stryker and other medical equipment companies have become more rationally valued. In my view, this has greatly enhanced their appeal. Not only does this provide for higher total return, it accomplishes this by simultaneously reducing valuation risk. A better return at lower risk is always a good thing in my book.

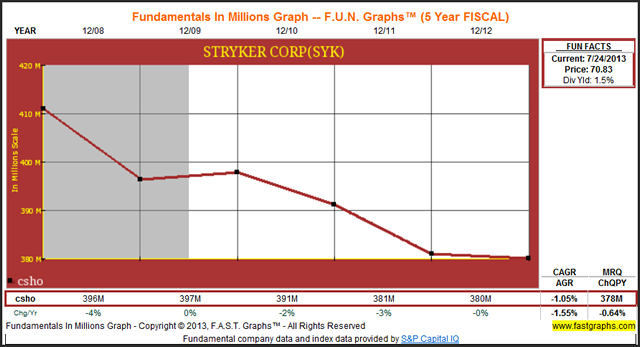

In addition to providing a steadily-growing income, Stryker has also rewarded shareholders through an aggressive share buyback program since 2008. Common shares outstanding (csho) have fallen from 395 million shares in 2008 to 380 million in 2012. A lower share count facilitates the company’s ability to continue growing earnings at above-average rates.

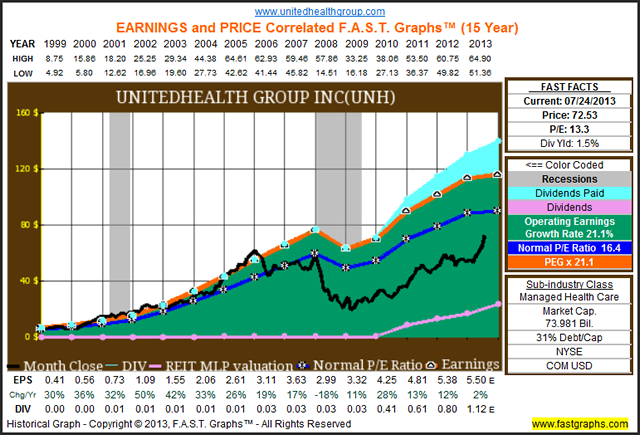

UnitedHealth Group (UNH)

My final featured company in the Health Care sector is UnitedHealth Group Inc, the premier managed health care insurer in the country. I found this particular subsector fascinating to review. In some ways the managed Health Care subsector has evolved similar to big pharma, but for different reasons. For many years major players such as UnitedHealth, Wellpoint, Aetna and Humana were quintessential examples of consistent above-average growing businesses.

However, that all changed because of two primary reasons. First from the challenges of the Great Recession, and next from the uncertainties of a rapidly-changing health care insurance environment. The Health Care Reform Act has been, and may even still be, a two-edged sword for this subsector. Initially, there were fears that the Health Care Reform Act might destroy the profitability and certainly the growth of the major players in this subsector. However, as more information on Obamacare has come to light, it is beginning to become evident that the Health Care Reform Act could be a windfall to these companies.

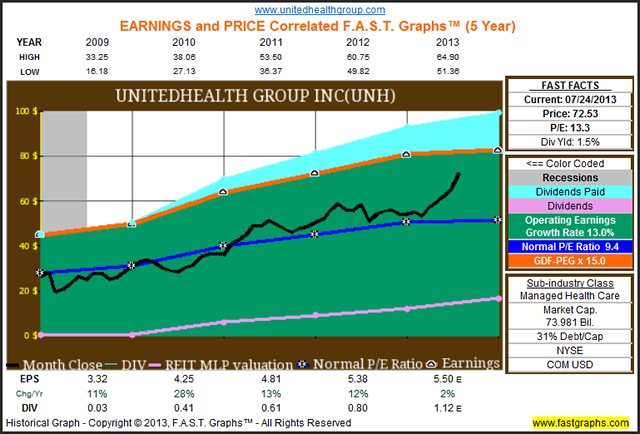

The following Earnings and Price Correlated FAST Graph on UnitedHealth Group reveals how stock price and earnings were highly correlated prior to the Great Recession of 2008 when UnitedHealth Group was a quintessential growth stock. Then after the Great Recession and the initial uncertainties of the impact of Health Care Reform, we see how the market has reset the valuation of UnitedHealth Group. Additionally, we see by the light blue shaded dividend expression, that UnitedHealth Group has simultaneously been morphing into a dividend growth stock deviating from its pure growth roots.

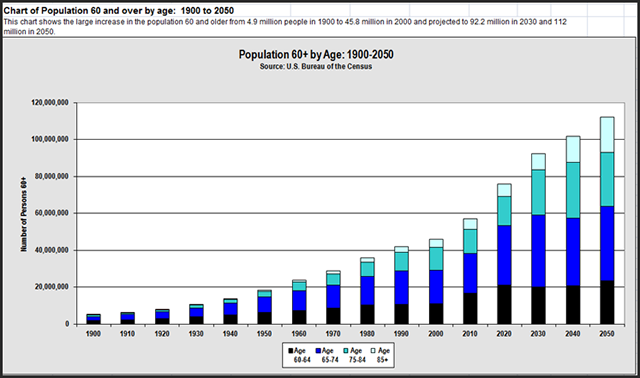

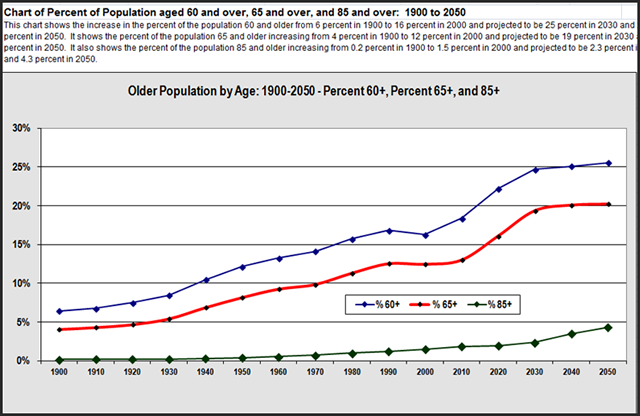

Another factor that cannot be ignored or denied regarding managed health care is the continuing powerful demographic forces of our aging population. In spite of the uncertainties of health care reform, demographics continue to provide significant long-term opportunities for this segment. Regarding health care reform, it currently appears likely that it may actually benefit this subsector; therefore, much of the uncertainty is lifting. This is translating into better stock performance.

The following graphs were taken from theAdministration On Aging, and provide clear evidence of the enormous opportunity that an aging population provides this subsector, assuming that the government doesn’t take away their ability to earn a profit.

However, the reader should also be aware of the complex nature of the Health Care Reform Act. The entire transcriptcan be found herefor anyone willing to endure the voluminous nature of this act, courtesy of the Kaiser Health News.

UnitedHealth Group Recent, Past & Future

In light of what I’ve shown above, the resetting of UnitedHealth Group can be seen by first reviewing the company’s Earnings and Price Correlated history since 2008. Earnings growth has been quite strong at 13% per annum, and the company’s stock price has been steadily reacting in a positive way as the uncertainties of health care reform have dissipated. Additionally, we see that the company’s dividend payout ratio has increased, as expressed by the pink line (dividends as a percentage of earnings) and the light blue shaded area after those dividends have been paid out.

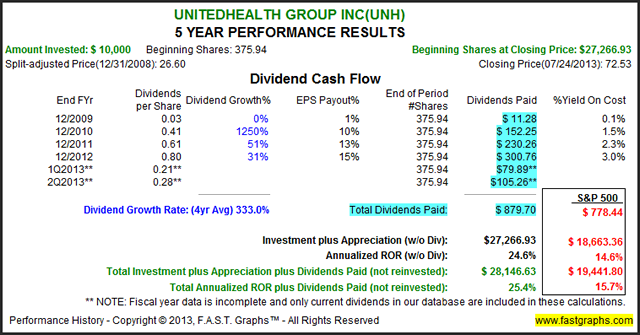

Shareholders with the courage and/or foresight to invest in UnitedHealth Group since 12/31/2008 were richly rewarded. A $10,000 investment on 12/31/2008 would have grown to $27,266.93 representing an annualized rate of return without dividends of 24.6%, far surpassing the S&P 500. Additionally, the dividend was raised from $.03 a share in 2009 to $.41 in 2010, and has continued to advance ever since.

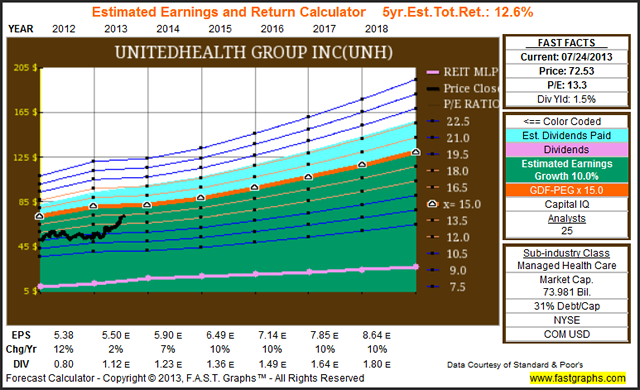

The consensus of 25 analysts reporting to Standard & Poor’s Capital IQ estimate 5-year forward earnings growth at 10%. Consequently, UnitedHealth Group, and I might add, most of its peers, appear to be attractive long-term investments at today’s valuations.

Since this article is earmarked to the dividend growth investor looking for quality fairly valued dividend growth stocks to add to their retirement portfolios, the following additional fundamentals support their inclusion.

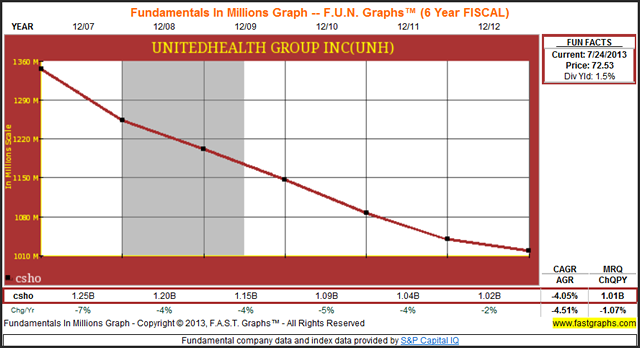

UnitedHealth Group is supporting shareholders and its future growth through an aggressive share buyback program. Common shares outstanding have decreased from 1.25 billion shares in 2007 to 1.02 billion shares by fiscal year-end 2012.

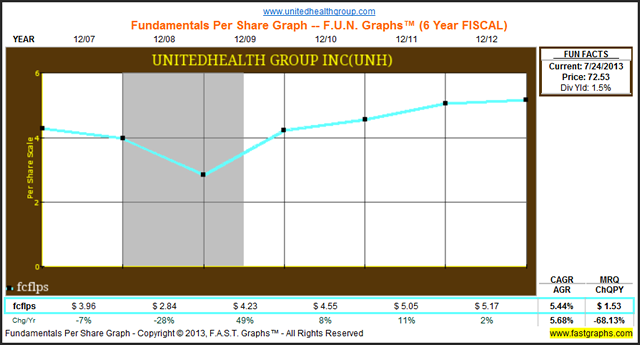

Additionally, UnitedHealth Group’s free cash flow per share has steadily increased since the Great Recession from $2.84 in 2008 to $5.17 per share by fiscal year-end 2012. This expression of free cash flow is after the company has paid a dividend, which indicates that the dividend is well-protected.

Summary & Conclusion

The Health Care sector appears to offer several high-quality dividend growth stock opportunities at today’s valuation. The tailwinds of the powerful demographic opportunities provided by an aging population are now supported by the headwind of uncertainty from health care reform that perhaps is now turning into a tailwind in its own right. As the old saying goes, “in every adversity lies the seed of a greater or equivalent benefit. ” Of all the sectors thus far reviewed, I believe that the Health Care sector provides some of the best opportunities I have thus far seen.

My next article will cover the 40-Financial Sector.

Disclosure: Long PFE, ABC, AZN, NVS, SNY, SYK, MDT, UNH at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs