“The man of system, on the contrary, is apt to be very wise in his own conceit; and is often so enamoured with the supposed beauty of his own ideal plan of government, that he cannot suffer the smallest deviation from any part of it. He goes on to establish it completely and in all its parts, without any regard either to the great interests, or to the strong prejudices which may oppose it. He seems to imagine that he can arrange the different members of a great society with as much ease as the hand arranges the different pieces upon a chess-board. He does not consider that the pieces upon the chess-board have no other principle of motion besides that which the hand impresses upon them; but that, in the great chess-board of human society, every single piece has a principle of motion of its own, altogether different from that which the legislature might choose to impress upon it.”

Adam Smith, 1723-1790

Philosopher and Political Economist

Author of “The Theory of Moral Sentiments” (1759) and “An Inquiry into the Nature and Causes of the Wealth of Nations” (1776)

Adam Smith played a leading role in the Scottish Enlightenment and his classic, “The Wealth of Nations”, which took him ten years to write, made him the father of market-based economics. Smith was a devout believer in the beneficial role that rational self-interest plays in a free market economy. He turned many common views of the time on their head. Sympathy, he said, could be self-interested. The individual’s income inured to society’s broader benefit. His was the revolutionary idea that many actors, all working for solely their own benefit, produce a better social outcome than even the most well-intentioned centralized planning by a monarch or parliament. The failure of planning and regulation is due in large part to, as Adam Smith puts it above, the tendency of “chess pieces” to move on their own principle of motion, as opposed to that intended by the “man of the system”-- or put more bluntly, the law of unintended consequences.

Recently the Fed indicated it may begin returning control over market pricing and interest rates to Adam Smith’s invisible hand… and borderline chaos erupted. The episode began mid-day May 22nd as Congress questioned Fed Chairman Bernanke and suddenly the cat was out of the bag and a paradigm shift ensued. Bond funds suffered some of their largest weekly redemptions on record. Rates spiked and markets swooned around the world through late June as investors assumed the worst. “The sky is falling… rates are rising!” the markets seemed to cry. Dare it be… is it finally upon us… an end to the salve of easy money?

What caused all the uproar? That day the Fed spoke of “tapering”, or reducing its bond buying program. In Fed-speak this means reducing the $85 billion of bonds it is buying each month, perhaps as soon as this Fall. It was this heretical notion of taking a step towards an economy where the Fed isn’t printing $2.5 billion dollars a day that caused the conflagration. Did people really expect that the bond buying would last forever? It’s not as if the Chairman said “We’re going to stop buying bonds and start selling them.” Rather, he said something along the lines of, “We might start to slow the rate at which we’re buying bonds sometime in the intermediate future… if the economy continues to recover.” To put this in terms of the famous helicopter analogy, Ben did not say “I’m going to start vacuuming up money from my helicopter instead of dropping it”, but rather he just said, ”I might start to drop a little less money from my copter in a few months if things keep getting better.” This ought to be a good thing. If the Fed follows through with tapering, then that would mean the economy is recovering, which is really the best thing for stocks… not even considering the end to any unintended consequences of money creation. Also note that the Fed is talking about ceasing only one of their big programs (bond buying), the other (super low short-term rates) is still solidly intact.

It’s interesting to note that the anticipation of higher long-term rates is now universal-- 57 out of 57 economic forecasters tracked by Bloomberg call for the 30 year Treasury bond yield to be higher at the end of 2013. I guess no one thinks that the economy might double (or is it now triple? quadruple?) dip and the Fed would back off on its plans? While we remain steadfastly contrarian, we do realize that sometimes the consensus is correct… but even in these cases there is little to be gained by acting on consensus convictions unless you act ahead of others (though almost by definition, once it’s consensus it’s probably too late).

Should one sell their stocks for fear of higher interest rates? Strict financial theory holds that higher interest rates make stocks less valuable and so would indicate yes. But we think no… at least not anytime soon. While interest rates themselves do affect stock values, other things that are going on in the economy and world are more important, and these other things usually are the driving root causes of changes in both interest rates and stocks. Besides, the initial reaction is already behind us: the Fed’s “tapering” talk sent stocks and bonds around the world down sharply, with the S&P 500 Index declining 5.8% from May 22nd through June 24th (the market has since recovered to new highs).

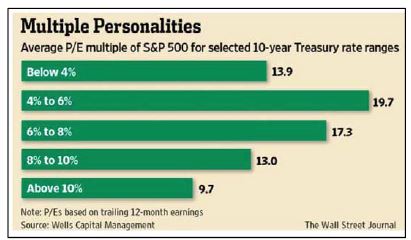

What does history say about the relationship between interest rates and stock valuation? History says “It depends.” The record suggests interest rates are adversely associated with equity valuation only when rates are sufficiently high, as this bar chart indicates.

The inflationary or deflationary pressures likely affecting interest rates in the first place at such times we believe is the more important valuation factor.

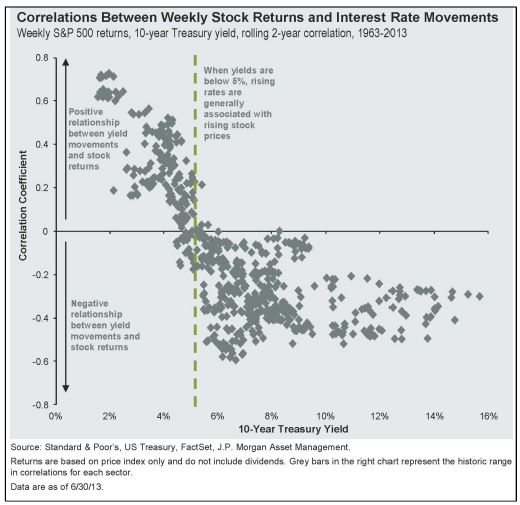

The true relationship between stocks and interest rates is complex and non-linear. The excellent chart atop the next page shows that the effect of the movement in rates on stocks changes depending on the level of rates. It shows the correlation between the S&P 500 Index and 10-year Treasury yields. When interest rates are below five percent, stock prices and yields have typically risen in concert. With current 10-year rates at about 2.5%, we might expect stocks and rates to have a solidly positive correlation, if the future is like the past. Given such a caveat, if one believes rates are headed higher from today’s low level, one wants to own stocks. It’s not until yields start getting closer to five percent that stock investors should fear further rate increases.

Rising interest rates are a different story for bonds, and the first half of 2013 was particularly rough sailing. In early June, long-term Treasury bond holders were staring at a twelve-month loss of 19%. Put another way, losses in the U.S. aggregate bond index through the first half of the year were the worst since 1994 when the Fed hiked rates four times (causing our home, Orange County, to file what was then the largest municipal bankruptcy in history… though Detroit has recently snapped up this ignominious honor via its recent filing).

Interestingly, despite this, from the viewpoint of an absolute-return- minded long-term bond holder, rising rates are actually a good thing. Unrealized losses indeed appear on one’s brokerage statement (really this is sort of an expression of how much more money one could have made if one waited to buy). However, if one holds to maturity one would still end up getting paid the par value at maturity, but will have reinvested the coupons at the new higher rates. This means that one actually ends up with more money given high rates at the end of the day than would have resulted under low rates. The cherry on top is that one can look forward to re-investing these more numerous dollars again at the new higher rates. In this way, interest rates are a sort of an ambiguous enemy of bond returns… the true enemy is inflation which absolutely eviscerates the purchasing power of any bond payouts.

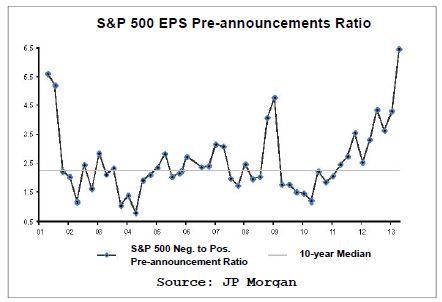

Source: JP Morgan

The Fed beginning to talk of the end of experimental, unconventional “quantitative easing” (QE) can be viewed as a first step towards less manipulation and more financial normalcy-- a good thing. Some economic prognosticators speak as if lowered rates bestowed a robust economy with only one drawback (potentially higher inflation). Remembering Adam Smith, we might ask, if prices are best determined by market forces, why not so with the price of money (which is what interest rates really represent)? Low rates encourage speculation by making it cheaper to use money (whether your own or borrowed) to speculate. “Might as well use that cash to buy those Modernist paintings that seem to go up every year- I’d only get 0.01% at the bank anyway.” Many have blamed the low rates of the last 20 years as contributing to or causing the tech-

stock and housing bubbles.

Less acknowledged is the fact that low rates make it less costly to do nothing-- and you usually don’t make a vibrant economy by encouraging people to do nothing. Think of all those millions of empty foreclosed houses that the banks own. Having all those houses sit empty isn’t productive, it isn’t efficient. If 10-year Treasury rates were 15%, they could sell those houses at a 15% loss and be made whole in about a year. Not selling would carry an opportunity cost of the 15% they could have earned. Instead, holding onto those foreclosed homes, and waiting and hoping for a price increase to avoid selling at a loss, costs the banks almost nothing, and so that’s what they do. Higher rates, if we get them, would make it more costly to speculate, more costly to do nothing, more costly to spend money frivolously, and hence have good reason to be welcomed.

Rising interest rates portend additional salutary effects. Deficits in defined benefit pension obligations are reduced. Life insurers can earn a margin above their fixed obligations. Net interest margins improve for banks. The money market fund business returns to for-profit status. Not to mention that private citizens can now save money and have its real purchasing power grow instead of being slowly destroyed, as happens with negative “real” rates (real being quoted minus inflation).

Source: Strategas Research Partners

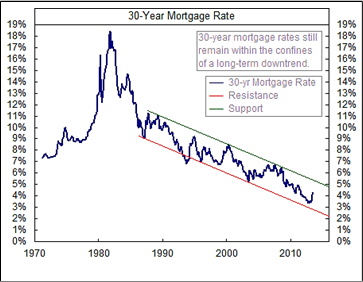

We also believe there is room for higher interest rates without derailing the housing recovery, given today’s low starting point. In fact, over the last forty years, median home price appreciation has been much greater under rising, as opposed to falling, mortgage rates (again, not because of rates per se, but because of what is going on when rates are rising). Today’s home prices also remain below the average multiple of income seen during the past forty years and ownership costs compare favorably to renting, even after the recent increase of near one percent in 30-year mortgage rates.

Source: www.chartoftheday.com

Turning back to the stock market, June losses were quickly reversed during July, and at the time of writing the Dow and S&P 500 trade above their year 2000 and 2007 peaks. While those years represented unsustainable market tops, today’s valuation, both in terms of dividends and earnings, compares favorably and assuages our nervousness associated with new highs. Corporations are on comparatively firmer footing given that companies currently carry roughly half as much debt relative to their book equity than they did at those times. Corporate cash as a percent of current assets has also doubled from the 14% level of 2000 to 28% today.

We are also pleased to see the absence of the sort of unbridled optimism that often accompanies market tops. Earnings expectations have come down meaningfully for the second quarter and full years 2013 and 2014. The ratio of companies releasing negative pre-announcement to positive pre- announcements is over 6.5, a ten-year high. This tends to be a good contrarian indicator because it’s harder to disappoint when your original hopes weren’t that high anyway.

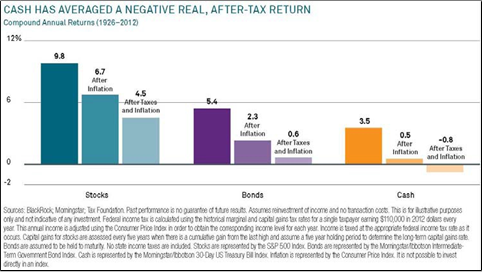

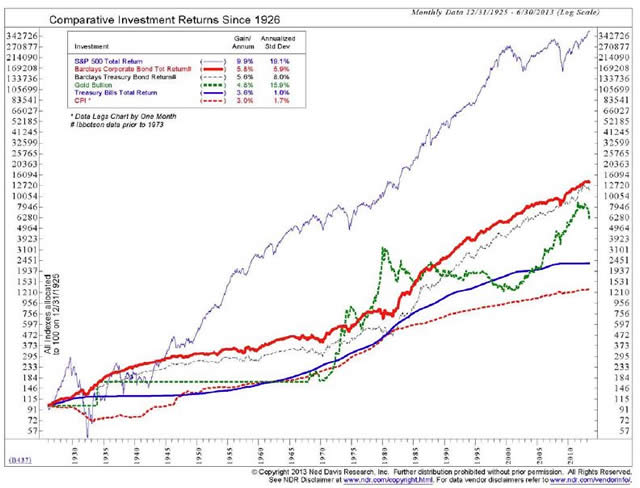

We would like to close this quarter with a reminder why it is worth the periodic anguish of opening the mail only to see a disappointing monthly brokerage statement. The chart below shows how hard it is to get ahead in bonds or cash after considering inflation and taxes. Since 1926, it has only been with stocks, that one’s purchasing power has increased meaningfully, by 4.5% per year, after assumed taxes and actual inflation (CPI). While Knightsbridge cannot control inflation, we do invest in a way that we have found can afford both higher stock returns and lower taxes than shown here.

We also point out the importance of a long-term perspective. On any given day stocks are virtually a 50/50 win/loss proposition; in any given few months, the prospects are not much better. The likelihood of witnessing growth in wealth increases markedly when you start measuring performance in periods of years. Going all the way back to 1871, 80% of five-year periods have produced positive total returns of stocks after inflation (see chart at the left). Interested parties can see an illustrative chart of various asset returns on the last page after the close.

Source: The Motley Fool

Source: The Motley Fool

Much as Adam Smith revealed to the world that the real wealth of nations lay not in gold and silver, but rather in goods and services, investing in the productive capacity of the companies that provide our goods and services has greatly outperformed the strategy of hoarding precious metals (though hoarders still would have done alright). Stocks have also greatly outperformed bonds, which could be said another way: choosing to receive the fruits of an uncertain future, whatever they may be, has been more rewarding than choosing to receive a fixed promise in the future. As our economy slowly and cautiously returns to normal, we expect the future to be like the past in this regard.

We greatly value the trust you place in us.

Very Truly Yours,

John G. Prichard, CFA

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

© Knightsbridge Asset Management