IN THIS ISSUE:

1. The Economy Keeps Limping Along

2. Americans’ Net Worth Hits New Record, But…

3. Gas Prices Could Hit $4 by Labor Day… Or Not

4. How Crude Prices Affect Gasoline Prices

5. Results From Our Financial Literacy Quiz

Overview

With the recent jump in gasoline prices, several energy analysts are forecasting that prices at the pump will top $4 a gallon (national average) later this summer. On the other hand, some analysts feel that gas prices will only go up another 5-10 cents a gallon just ahead, and then move lower in the fall. Of course, no one knows for sure. Today, we’ll take a look at what’s driving gas prices higher.

But before we get to that discussion, let’s take a quick look at the latest economic reports, most of which were disappointing. The only good news here – if you can call it that – is the economic data of late is not encouraging enough for the Fed to begin tapering its bond purchases anytime soon, as I discussed at length in last week’sE-Letter.

The Fed reported recently that Americans’ cumulative net worth has finally hit a new record high of $70.3 trillion in the 1Q, up $3 trillion from the 4Q of 2012. While this is good news on the surface, much of the increase came as a result of Americans spending less and paying off their debts. Slower growth in consumer spending is not good for the economy.

Last but certainly not least, I will reveal the results from our recentFinancial Literacy Test. This quiz was wildly popular with my readers. And today, I’ll tell you how you did – which was really good. You may be surprised at the results, including the two questions that stumped about half of those taking the test. My thanks to all who participated!

The Economy Keeps Limping Along

There haven’t been a lot of key economic reports out over the last two weeks, but what we did see was generally disappointing. After seeing consumer confidence hit a five-year high in June, and stocks soaring to new record highs, most analysts figured that consumer spending would be picking up significantly. Not so much.

On July 15, the Census Bureau reported that June retail sales rose only 0.4% as compared to the pre-report consensus of 0.8%. If you back out auto sales, which were quite strong in June (15.9 million units), the retail sales number fell to 0.0% last month. That’s no-doubt disappointing.

The retail sales report raises new questions about the strength of the US economy, the health of consumers and the timing of any Federal Reserve “tapering.” The data provided further evidence that the US economy didn’t grow very fast in the 2Q, with a real possibility that 2Q GDP will be only 1% or less when the first estimate is posted on July 31.

Not surprising, we continue to see forecasters revise down their estimates for 2Q GDP. Last week, J.P. Morgan Chase cut its 2Q forecast from 2.0% to only 1.0%. Barclays also cut its 2Q GDP estimate to 1.0% from 1.6%.

The only good news here – if you can call it that – is the economic data of late is not encouraging enough for the Fed to begin tapering its bond and mortgage purchases anytime soon, as I discussed at length in last week’sE-Letter. Bernanke was back before Congress last week promising once again that the Fed won’t halt its QE purchases for the “foreseeable future.” Stocks, of course, hit yet another new record high. Thanks, Ben!

The housing sector has continued to rebound strongly so far this year. Yet the latest data for June was a little weaker than expected. Housing starts and new building permits in June came in well below expectations and May levels. Sales of existing homes in June also disappointed on the downside. Sales fell 1.2% last month to 5.08 million units, which was lower than May sales and well below pre-report estimates. The new home sales report for June will be out tomorrow and is also expected to be slightly weaker than May.

Americans’ Net Worth Hits New Record, But…

Americans’ net worth has finally shaken off the effects of the recession and the bear market in stocks and hit a new record high recently, according to data released recently by the Federal Reserve. Taken together, American households were worth $70.3 trillion in the 1Q, up $3 trillion from the 4Q of 2012, and well above the recession-era low of $54 trillion.

The latest growth in net worth is in large part a function of gains in the stock market and home values. Nearly all of the $1 trillion in financial asset gains that households enjoyed in the 1Q were due to the stock market. In addition, residential real estate values climbed by over $780 billion in the 1Q. That sounds great.

However, net worth is a measure of households’assets minus liabilities, and it’s important to note that the latest Fed report also reflects falling household debt as consumers spend cautiously and pay down their debts. Credit card and mortgage debt both peaked in 2008 and have seen significant declines since then, according to the Fed. This makes declines in debt a mixed signal: it means healthier household balance sheets, but also reflects less growth in consumer spending.

This is another reason we are stuck in a slow growth recovery. Rising net worth is a good thing, of course, but consumer spending accounts for 70% of GDP. The economy is not going to have GDP growth of 4-5-6% if consumers are still deleveraging and paying down debt.

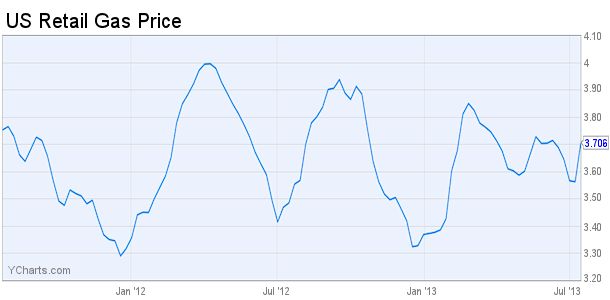

Gas Prices Could Hit $4 by Labor Day… Or Not

According to the US Energy Information Administration, the national average gas price was just above $3.70 for a gallon of regular as of July 19. That’s an increase of 14 cents a gallon over the prior week. Several energy analysts now predict that the national average gas price will hit $4.00 or above by Labor Day, including Stephen Schork, editor of The Schork Report, an energy newsletter.

There are several factors which can cause crude oil and gasoline prices to rise or fall, especially this time of year when demand is generally at its highest point. As we all know, crude oil prices drive the price of gas. The latest jump in oil prices began to intensify about the time that Egyptian President Mohamed Morsi was removed from office by the military.

Some analysts were surprised at the move since Egypt doesn’t produce much, if any, crude oil. However, a significant portion of oil produced in that region is transported via the Suez Canal to the West. Yet the Egyptian military has proven that it is more than capable of keeping that waterway open. So there must be something else behind this rally.

In the face of record-high demand for gasoline this summer, crude oil inventories have dropped by a record 27 million barrels over the last month, which is over 25% more than supplies fell in the same period last summer.

Second, North American refineries are currently operating at close to peak capacity, as refinery operators try to do every summer. But getting through a summer without problems can be the exception, not the rule.

There is word in the industry that the Irving Oil refinery in St. John, New Brunswick, Canada, may have to shut down for some unscheduled maintenance. That could send gas prices even higher in the Northeast US, since this refinery is one of the 10 largest in North America.

Crude prices are also being pushed upward by cuts in output from northern Iraq, Nigeria, Libya, Iran and Russia. And if there are any hurricanes, or even hurricane threats, to the oil platforms and refineries along the US Gulf Coast this summer, that could quickly cause price spikes across much of the nation.

Crude oil prices have risen from the April low near $98 per barrel to above $108 earlier this month, and is at $107 as this is written. Most energy analysts expect gasoline prices to rise another 5-10 cents a gallon just ahead to catch up with the crude oil price. That could happen over the next couple of weeks.

How Crude Prices Affect Gasoline Prices

Crude oil prices make up 72% of the price of gasoline. The rest of what you pay at the pump depends on refinery and distribution costs, corporate profits, and federal and state gas taxes. Usually, these costs remain stable, so that the daily change in the price of gasoline largely reflects oil price fluctuations.

It usually takes about five-to-six weeks for oil price changes to work their way through the distribution system to the gas pump. Oil prices are a little more volatile than gas prices. This means oil prices might rise higher, and fall farther, than gas prices.

Like most of the things you buy, oil prices are affected by supply and demand. More demand, like the summer driving season, drives higher prices. There is usually less demand in the winter. However, oil prices are also affected by crude and heating oil futures, which are traded on the commodities exchanges. These prices fluctuate daily, depending on what investors think the price of oil will be going forward.

Let’s take a quick look at who uses the most oil around the world. The US uses 21%-25% of the world’s oil, depending on which estimate you believe. Two-thirds of this is for transportation. The European Union is the next biggest user, at 15% of the world's oil production. China now uses 11%, as its use has grown rapidly.

To sum up, gasoline prices may move a bit higher in the next couple of weeks to catch up with the recent rise in crude oil prices. But barring any surprises, such as a hurricane or some other supply interruption, most energy analysts see gas prices falling as we head into the fall.

Results From Our Financial Literacy Quiz

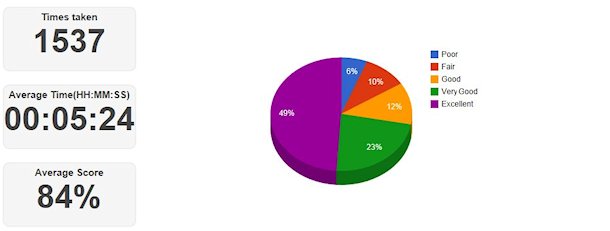

First, let me thank everyone who took our recent Financial Literacy Test and a special thanks to those who forwarded it on to friends, loved ones and maybe even a few school board members. So far, we’ve had over 1,500 people take the test, and we expect that number to top 2,000 soon.

As in the past, my readers aced the five FINRA (Financial Industry Regulatory Authority) questions, as well as most of the additional questions we added. The following charts show the test results and tell the story:

You will recall that the first five questions in our quiz came directly from the FINRA exam I highlighted in myJuly 9 E-Letter. On those five questions alone, my readers scored an average of 95.6%. I’d say that’s a solid A grade and is indicative of the sophistication of our subscriber base.

In contrast, the 25,000 respondents who took the recent five-question test administered by FINRA scored a dismal 58%, as compared to my readers who took our harder, 12-question test and scored 84%. Way to go!

While our testing method wasn’t scientific, it does seem to indicate that those who actively seek out financial information through the Internet, e-letters, etc. have a much better basic knowledge of financial/investing matters than the general public.

|

If you didn’t take the Financial Literacy Test, you really should! Just click on the button at right. |

|

On the seven additional questions we added in the test, our readers’ average score fell to 75.6%. Yet if you look at the individual question table above, you’ll see thattwo questions are responsible for most of the drop in the average score. Let’s take a closer look at those two.

The first of these was question #7 concerning “drawdown,” one of the most important measures of an investment’s risk available, and one that we use extensively in our due diligence evaluations. Drawdown refers to the worst-ever losing period for any given investment. For example, the worst-ever drawdown for the S&P 500 Index was 50.95% in the bear market of 2008-2009 during the recession and financial crisis.

Whenever we analyze a potential investment or investment advisor, one of the very first things we look for is the worst-ever drawdown. This is a key reading of how volatile that investment or money manager can be. We generally assume that the worst-ever drawdown can happen again in the future.

To be fair, it’s not surprising that over half of those who took our test missed this question. That’s because the financial services industry tries so hard to hide this term from you. As a general rule, you won’t find the word “drawdown” on mutual fund fact sheets, marketing materials or in prospectuses because it is often abig negative. Instead, they use less telling risk measures such as alpha, beta and standard deviation that are usually meaningful only when compared to benchmark indexes or other mutual funds.

While most investors focus on annualized returns when selecting an investment, they should also pay attention to the worst drawdown – even if you have to pry that information out of the investment’s sponsor.

There’s a lot more I’d like to say about the importance of drawdowns as a measure of an investment’s risk, but I don’t have the space to do so here. Instead, I’ll soon be releasing a Special Report that will tell you everything you need to know about this important analytical tool, and why it’s important that you consider it out onany investment you may consider.

The second question that gave quiz takers a challenge was #11 regarding which Treasury bond maturity would be affected most by an increase in interest rates. Almost half of those taking the test missed this one. As a general rule, the longer a Treasury bond’s maturity, the greater price is affected by an increase in interest rates. The chart at right shows the estimated effect of a 1% increase in interest rates on various types of bonds.

As you can see, the chart clearly shows that longer-duration bonds are far more sensitive to interest rate changes, even if the bonds are issued by the US Treasury and have no default risk. That’s a reasonable result since investors are tying their money up for a longer period of time if they hold the bond to maturity.

The good news is that 89% of my readers answered question #3 correctly. It was closely related to question #11 except that it sought to know whichdirection bond prices will typically go when interest rates increase. So the vast majority of readers got the direction right but weren’t as sure about how longer maturities affect price.

As long-time readers know, I have been concerned about the amount of money that has flowed into taxable bonds, and much of that into Treasuries. While these bonds and bond funds are currently experiencing outflows, there are millions of investors who are still invested in Treasury bonds because they are considered to be a “safe” asset. Unfortunately, this only applies to default risk. Interest rate risk has already started to negatively affect Treasury bond prices and it’s most likely going to get worse before it gets better.

Bonds 101 Video

To help my readers better understand the different types of bonds and how they work, we have prepared aBonds 101Videothat covers the basics of many types of bonds, how they work and what affects their value. This informative video is less than 15 minutes long and is easy to understand.

Not only is this video valuable for even experienced investors, it is invaluable for folks who don’t understand bonds very well. It’s also something that you might want to forward to your friends and family so they can benefit from this knowledge as well. To access this short but extremely valuable video, CLICK HERE.

If you watch the video, I would love to get your feedback. You can send me an e-mail at:

Thanks in advance!

Wishing you a great summer,

Gary D. Halbert

© Halbert Wealth Management