Are Blue-Chip Consumer Staples Worth Today's Premium Valuations?

Introduction to theConsumer Staples Sector

The Consumer Staples sector consists of companies that provide essential products. In other words, Consumer Staples are products that people cannot or are unwilling to do without. As a result of the essential nature of Consumer Staples, there are several attributes that distinguish this sector from most others. First of all, the essential nature of the products that Consumer Staples’ companies produce, are for the most part, non-cyclical. Second, Consumer Staples tend to be very insensitive to economic cycles. Therefore, their businesses tend to remain strong and healthy even during recessions.

Because of the stability and consistency that many Consumer Staple companies possess, you will find many of the bluest of blue-chip companies within this sector. However, finding these blue-chips at attractive valuations is often difficult or rare. The best-of-breed Consumer Staples companies often command quality premiums relative to companies in other sectors with equivalent fundamental attributes. To state this more simply, moderate overvaluation relative to intrinsic value based on cash flows and earnings is very common for companies in this sector.

Since I am such a stickler for valuation, I am not willing to pay more for even the best company than I believe it is worth, based on fundamental values. Consequently, several of the best-of-breed Consumer Staples companies were cut from my list based solely on valuation. To be clear, many of these stocks are currently trading at historical normal valuations, but above what I would consider to be their intrinsic value. Since this moderate overvaluation tends to be the norm with these companies rather than the exception, some prospective investors might be willing to pay the premiums for many of these names, but not me.

The dividend stalwarts that I’ve excluded based on what I’ve stated above are listed in alphabetical order as follows: Colgate-Palmolive Co (CL), Clorox Co (CLX), Campbell Soup Co (CPB), Flowers Foods Inc (FLO), General Mills Inc (GIS), Kimberly-Clark Corp (KMB), Coca-Cola Co (KO), Pepsico Inc (PEP), Procter & Gamble Co (PG), Reynolds American Inc (RAI), JM Smucker Co (SJM), Sysco Corp (SYY), Unilever Plc-ADR (UL) and Unilever NV-ADR (UN).

To be clear, most of the names cited above are currently trading at historically normal premium valuations. Consequently, I consider them overvalued, and therefore, they were excluded. Another interpretation can simply be that these are quality blue-chips worthy of the premium valuations that the market is currently awarding their shares. In other words, all of the names cited above could be included as retirement portfolio candidates for the prudent dividend growth investor willing to pay a premium price for quality.

Procter & Gamble: A Classic Example of Premium Valuation

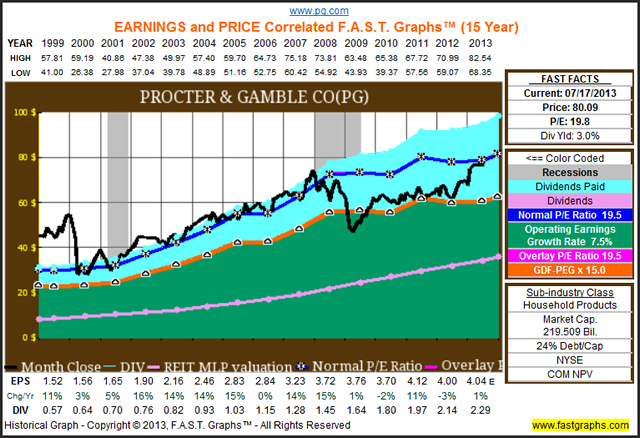

The following earnings and price coerelated graph on Procter & Gamble illustrates how the market tends to price this blue-chip at a premium. The orange line on the graph represents an fair value earnings justified PE ratio of 15, and the dark blue line represents the historical normal PE ratio of 19.5 that the market has typically valued Procter & Gamble at.

Furthermore, we see that the Great Recession of 2008 did bring Procter & Gamble’s price down to its earnings justified level and stayed there through much of 2012. However, with the bull run in 2013, Procter & Gamble’s share price has now returned to its historical normal PE ratio. Consequently, it could be argued that buying Procter & Gamble today at its historical normal PE makes a certain amount of sense. Even though the price was adjusted downward during the recession, it has since moved back into alignment with its historical normal value. However, I have never been able to make myself pay more for a company than I believe it is worth. For disclosure, I bought Procter & Gamble after it reverted to the mean, and still hold it currently.

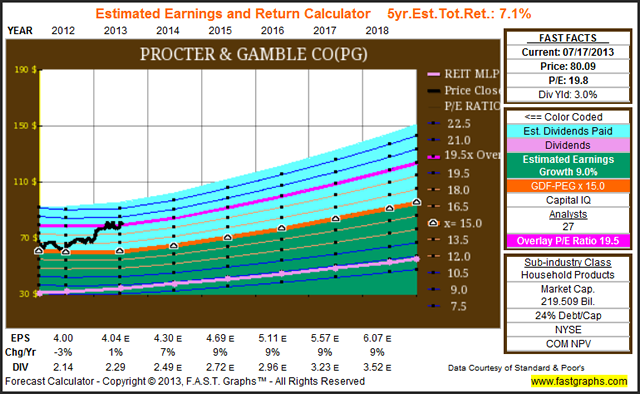

The following estimated earnings and return calculator defaults to valuing Procter & Gamble based on the consensus of 27 analysts forecasting 5-year earnings growth at 9% (the dark orange line). However, utilizing the PE overlay feature of FAST Graphs™, I have included the historical normal PE ratio of 19.5. In other words, based on estimates that are consistent with Procter & Gamble’s historical growth, it would be fairly valued based on its historical normal PE, but overvalued based on my definition of True Worth™.

The Consumer Staples Sector

This is the sixth in a series of articles designed to find value in today's stock market environment. However, it is the fifth of 10 articles covering the 10 major general sectors. In my first article I laid the foundation that represents the two primary underlying ideas supporting the need to publish such a treatise. First and foremost, that it is not a stock market; rather it is a market of stocks. Second, that regardless of the level of the general market, there will always be overvalued, undervalued and fairly valued individual stocks to be found.

My first article was titled Searching For Value Sector By Sector, my second article was titled Finding Great Value In The Energy Sector. My third article was titled Finding Value In The Materials Sector Is A Material Thing. My fourth article was titled The Industrial Sector Offers A Lot Of Value, Dividend Growth And Income, and my fifth article was Beware Of The Valuations On The Best Consumer Discretionary Dividend Growth Stocks.

As a refresher, my focus in this and all subsequent articles will be on identifying fairly valued dividend growth stocks within each of the 10 general sectors that can be utilized to fund and support retirement portfolios. Therefore, when I am finished, the individual investor interested in designing their own retirement portfolio should find an ample number of selections to properly diversify a dividend growth portfolio with.

This article will look for undervalued and fairly valued individual companies within the general sector 30-Consumer Staples. Within this general sector, there are several subsectors which I list as follows:

Consumer Staples In Value: Aggressive Candidates

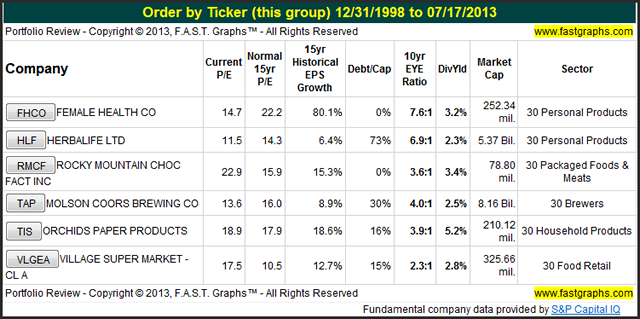

As I screened the universe of Consumer Staple companies I did find seven candidates that fit my aggressive criteria. This means that they are not blue-chip dividend stalwarts, but nevertheless appear to be interesting companies that are trading at reasonable valuations with the potential for solid long-term performance. However, as you can see from the portfolio review below, some of these companies are very small, and therefore, additional due diligence and caution is suggested.

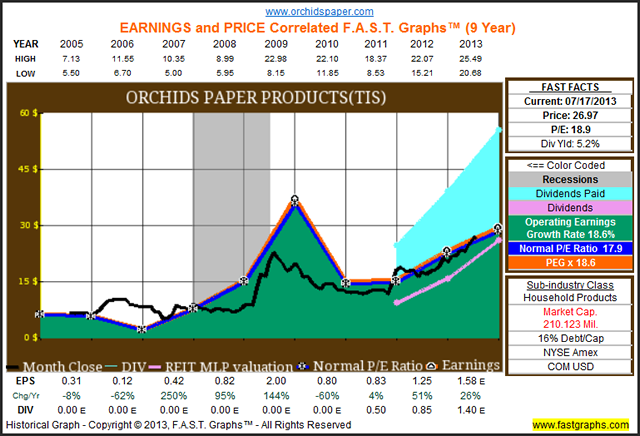

Orchids Paper Products Company (TIS): My Featured Aggressive Consumer Staples Company

Orchids Paper Products Company is a leader in the private label tissue industry, and I’m not sure you can think of a product that most people would consider any more essential than theirs. Consequently, this $210 million company with a 5.2% current yield and a history of above-average growth may be of interest to the more aggressive dividend growth investor.

Since going public in July 2005, Orchids Paper Products Company has generated significant profits and profit growth on behalf of their shareholders. The company’s operating earnings growth rate has averaged 18.6% per annum, and even though they’ve only paid a dividend since 2012, they have been very generous to shareholders, as depicted by the light blue shaded area on the graph below.

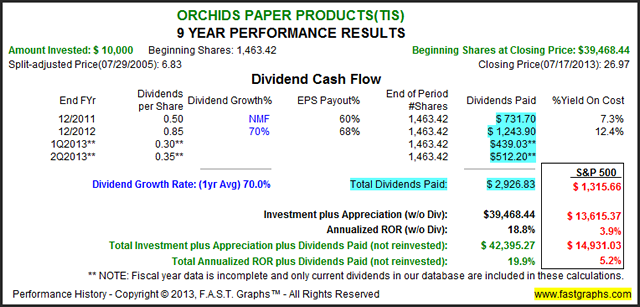

Orchids Paper Products Company’s excellent operating history has generated excellent long-term returns for shareholders. A $10,000 investment on July 29, 2005 when the company went public, would be worth $39,468.44 today. That represents an 18.8% compounded annualized return that is almost precisely correlated to the company’s operating earnings growth of 18.6%. Add in their substantial dividend payment over the last two years, and the company has outperformed the S&P 500 by orders of magnitude. Consequently, this may be a small dividend growth stock worthy of further scrutiny for the aggressive dividend growth investor.

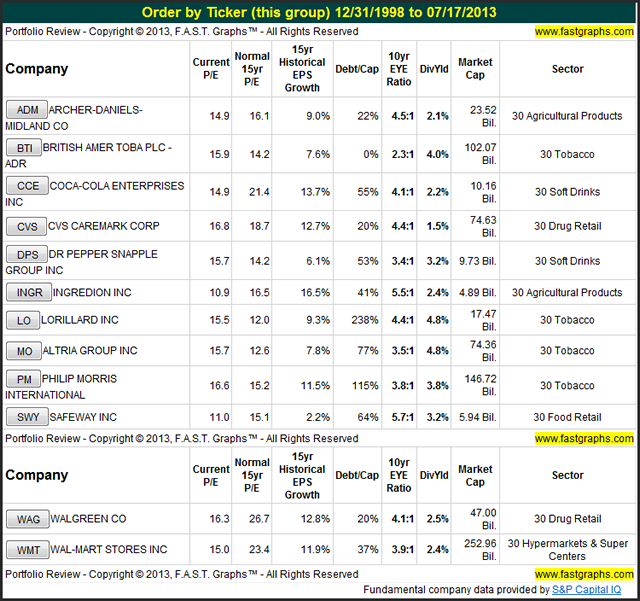

Consumer Staples In Value: Conservative Candidates

Even though many of the most well-known conservative blue-chip Consumer Staple companies are currently fully valued as referenced above, I was still able to find several well-known candidates that I feel are currently fairly valued. The following portfolio review lists 12 blue-chip dividend growth stocks currently fairly valued and listed in alphabetical order.

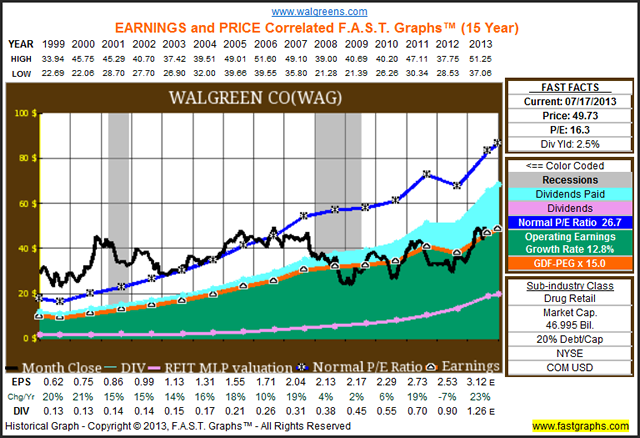

Walgreen Company : “Once Was Lost But Now Is Found”

I chose Walgreen Company (WAG) as my first featured Consumer Staples blue-chip dividend growth stalwart because I believe it offers a valuable lesson and insight into the importance of intrinsic valuation. Just like many of the premium valued blue-chips I mentioned in the introduction to this article, Walgreens was a company that the market was routinely pricing at a premium valuation prior to the Great Recession of 2008. However, since the fall of calendar year 2008, the market has been pricing Walgreen’s stocks more in line with its intrinsic value (the orange line on the graph).

The moral of the story is that premium pricing or valuation is more of an opinion than a principle. This is why I refrain from paying premium valuations for even the best of companies. I believe that premium valuation is an artificial construct, and therefore fragile. On the other hand, intrinsic value is not only more substantial, but also a principle worthy of relying on. Paying more for a company than its True Worth™ justifies can be permanently costly when, and if, attitudes change.

If you refer back to the Procter & Gamble example above, you would discover that Procter & Gamble lost its premium valuation temporarily, as its price has now moved back into premium valuation territory. On the other hand, Walgreens continues to be priced at its intrinsic value with no indication that it will move back to a premium anytime soon. Consequently, if you buy Walgreens at fair value, or Procter & Gamble for that matter, and it does move back to premium pricing, you receive a nice bonus. Moreover, you would earn this bonus while simultaneously assuming less risk thanks to the lower and more reasonable current valuation.

When you examine the performance of Walgreen’s when it was premium priced in 1999, you discover that its above-average operating earnings growth of 12.8% was wasted due to overvaluation. Thanks to overvaluation, shareholders only enjoyed capital appreciation of 3.7%, which is far less than the company’s excellent operating record should have justified.

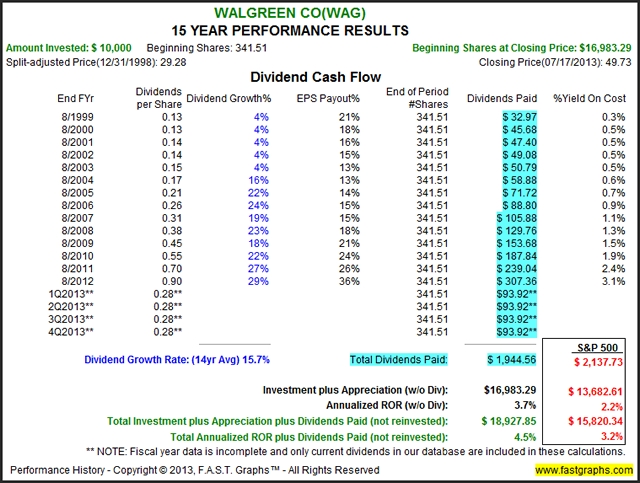

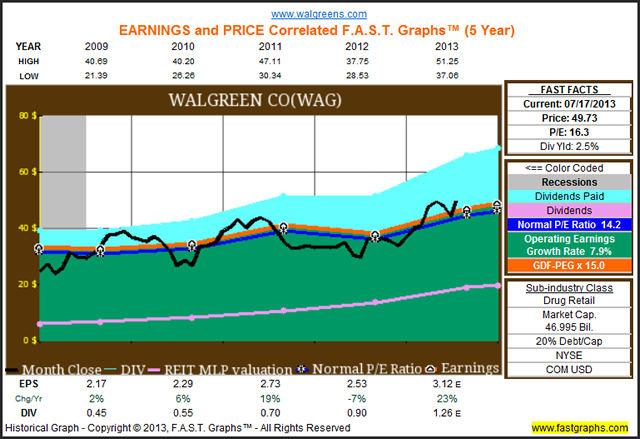

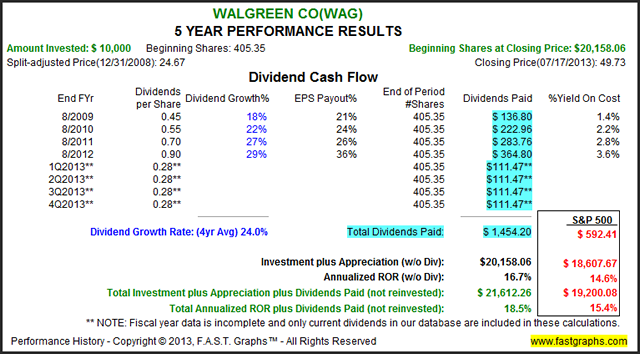

In contrast, if you evaluate Walgreens since the beginning of 2009 when its stock was trading at a discount to its intrinsic value, you discover an opposite phenomenon. During this period of time, Walgreen’s operating earnings growth rate did slow down to 7.9% from its longer-term average of 12.8%. However, a quick glance below the earnings and price correlated graph on the performance table shows that shareholders were rewarded with capital appreciation of 16.4%, which is significantly greater than the 7.9% operating earnings achievements. Simply stated, buying at a lower valuation that was supported by fundamentals, not only dramatically increases your rate of return, but simultaneously lowered the amount of risk you took to achieve it.

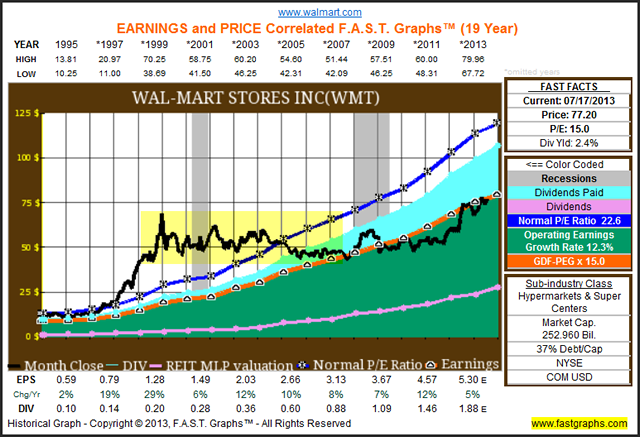

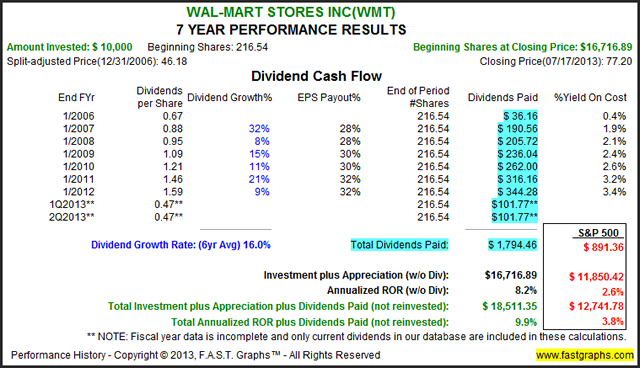

Wal-Mart Stores Inc.: My Featured Blue-Chip Dividend Growth Stock

Wal-Mart Stores Inc. (WMT) may provide one of the most interesting lessons in valuation of any company that I’ve ever examined. The following 19-year earnings and price correlated F.A.S.T. Graphs™on Wal-Mart Stores Inc. depicts a company with impeccable long-term operating success. The orange line on the graph plots Wal-Mart Stores Inc.’s earnings per share since 1995. You would be hard-pressed to find a company with a better long-term record of operating excellence than Wal-Mart has achieved.

On the other hand, the massive and ridiculous over-pricing of Wal-Mart’s stock during the irrational exuberant period 1995 to 1999 went far beyond the market applying a premium valuation. Instead, we see an excellent business that was so irrationally overvalued that in spite of earnings advancing like clockwork year-after-year, Wal-Mart’s stock price had nowhere to go but down.

Perhaps it was the belief in the quality of the company that kept its stock price so elevated for so long. In other words, investors apparently were reticent to sell their positions because of their belief in the strength and quality of the world’s leading retailer.

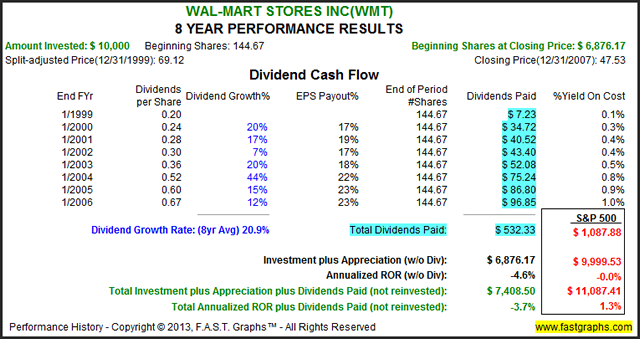

On the other hand, the enormous headwinds of extreme overvaluation precluded those same investors from making any money over calendar years 2000 to 2007. By utilizing the review feature of F.A.S.T. Graphs™, I learned that Wal-Mart’s operating earnings growth during that timeframe averaged 12% per annum. However, in spite of that stellar growth, shareholders would have lost an average of 4.6% per annum turning an original $10,000 investment into $6876.17. And, even though Wal-Mart raised their dividend every year, it wasn’t able to stem an annualized loss of 3.7% per annum.

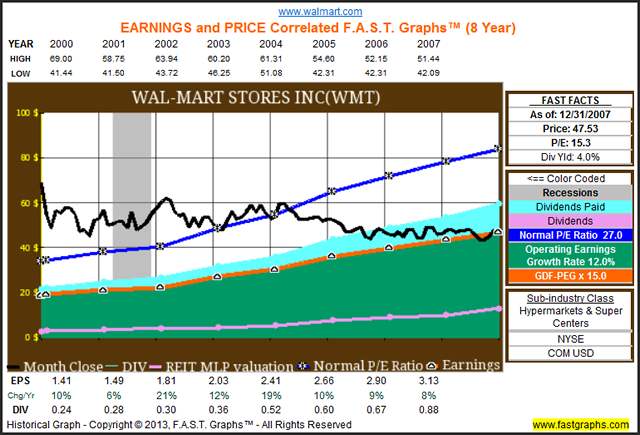

Wal-Mart Stores Inc: Fairly Valued And Growing Today

The following earnings and price correlated graph shows that Wal-Mart’s shares have been reasonably priced for the most part since calendar year 2007. I believe what you see in the graph below is the market coming to its senses while simultaneously providing prospective investors the opportunity to own one of the greatest businesses in the world at a very attractive valuation.

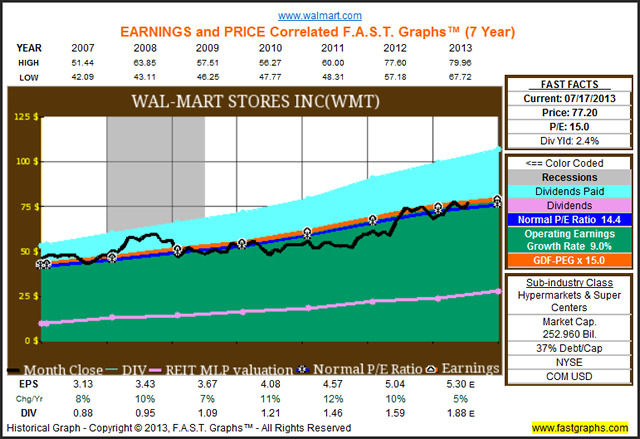

When you review Wal-Mart’s performance since it’s been reasonably priced, you see that fair valuation makes all the difference in the world. Instead of losing money, and in spite of the fact that its earnings growth rate has fallen to 9% per annum instead of double-digit growth, long-term Wal-Mart shareholders were rewarded according to the company’s operating achievement as evidenced by the associated performance report below.

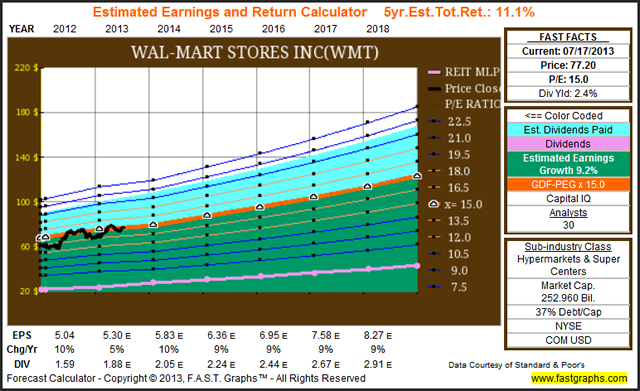

Wal-Mart Stores Inc: The Future

Wal-Mart is expected to continue growing over the next five years at approximately the same rate it has over the last seven. The estimated earnings and return calculator below shows that the consensus of 30 analysts reporting to Standard & Poor’s Capital IQ estimate Wal-Mart’s five-year earnings growth rate at 9.2%. Consequently, I believe that Wal-Mart represents the trifecta of above-average growth, above-average yield and sound valuation. Therefore, I believe that Wal-Mart represents the best current opportunity within the Consumer Staples sector today.

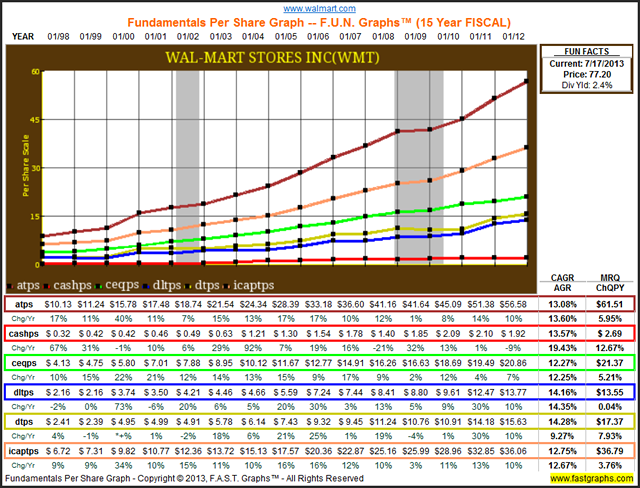

Digging Deeper Into Wal-Mart’s Fundamentals

Based on the essential fundamentals at a glance presented by the earnings and price correlated F.A.S.T. Graphs™plus dividends above, Wal-Mart appears to be a very attractive and sound long-term dividend growth stock. Therefore, I offer the following F.U.N. Graphs (fundamental underlying numbers) in order to take a deeper look into Wal-Mart’s fundamental strengths.

Wal-Mart’s Balance Sheet

A quick graphic glance at Wal-Mart’s balance sheet since 1998 shows continuing strength and improvement. The graph includes the following balance sheet metrics with acronyms:

- assets per share (atps)

- cash and equivalents per share (cashps)

- common equity or book value per share (ceqps)

- debt long-term per share (dltps)

- debt per share (dtps)

- invested capital per share (icaptps)

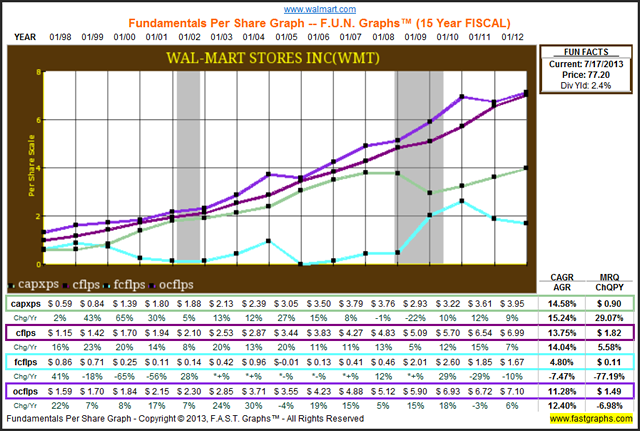

Wal-Mart’s Cash Flow Statement

A quick graphic glance at Wal-Mart’s cash flow statement since 1998 also shows continuing strength and improvement. The graph includes the following cash flow statement metrics with acronyms:

- capital expenditures per share (capxps)

- cash flow per share (cflps)

- free cash flow per share (fcflps)

- operating cash flow per share (ocflps)

Note: FAST Graphs™ calculates free cash flow (light blue line on the FUN graph) after dividends have been paid.

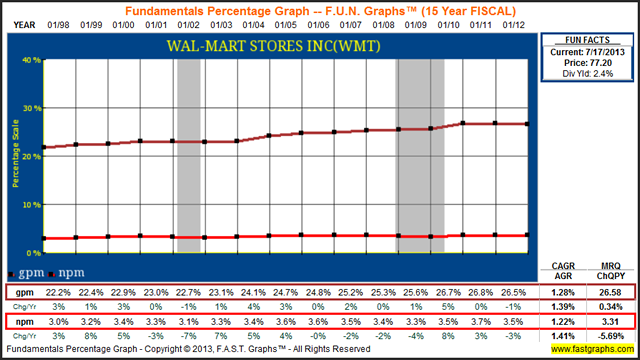

Wal-Mart’s Gross and Net Margins

One of the attributes of retail stores is relatively high gross margins. However, net margins tend to be very thin. This is especially true of grocery stores, which is becoming a larger component of Wal-Mart’s business. What makes up for the low net margin is the consistency of the business due to the essential nature of the products that Wal-Mart provides its customers.

The following FUN graph plots Wal-Mart’s gross profit margin (gpm) and net profit margin (npm):

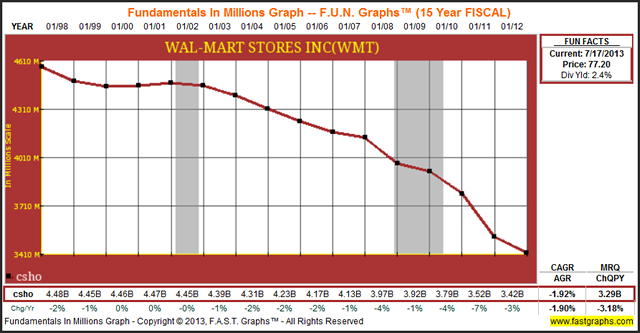

Wal-Mart’s Shares Buy-Backs

The following FUN graph plots Wal-Mart’s common shares outstanding (csho) since 1998. Clearly, in addition to a steadily-increasing dividend every year, Wal-Mart has also been rewarding shareholders with an aggressive share buy-back strategy. Buying back shares supports earnings growth, which ultimately rewards shareholders with more consistent and higher capital appreciation because in the long run earnings drive market price.

Summary & Conclusions

The Consumer Staples sector offers some of the highest quality blue-chip dividend growth stocks available to the retiree capable of providing both capital appreciation and an increasing dividend income stream. However, a side effect of the quality and consistency that many of the better names in this sector provide is that many of the best names are commonly premium priced. Because this premium pricing tends to persist is not necessarily dangerous relative to long-term losses. However, it does indicate taking a higher level of risk for a potentially lower rate of return than could be achieved with other companies in other sectors with similar fundamentals.

Whether or not to pay a premium for blue-chip Consumer Staples companies is a decision that each individual investor must make on their own. In my opinion, that’s okay, as long as those decisions are made with your eyes wide open. If you must own Colgate-Palmolive, Coca-Cola, etc., then you should be prepared to pay a premium.

On the other hand, if you are patient (I waited 14 years to buy Procter & Gamble on September 1, 2009) the opportunity to purchase blue-chip Consumer Staples at reasonable valuations may eventually occur. Then again, if you are willing to dig deep enough, you will more likely than not be able to purchase a great Consumer Staple at a sound valuation. The names on my conservative list represent examples today. But my current favorite is Wal-Mart, which I am currently conducting due diligence on pending purchase.

My next article will cover the Health Care Sector.

Disclosure: Long CL, CLX, GIS, UL, KMB, KO, PEP, PG, WAG, RAI, SYY at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs