Beware Of The Valuations On The Best Consumer Discretionary Dividend Growth Stocks

Introduction to theConsumer Discretionary Sector

The Consumer Discretionary sector consists of businesses that sell nonessential, and therefore, discretionary goods and services. Companies in this sector include retailers, media companies, consumer services companies, consumer durables and apparel companies, automobiles and components companies. Since so much of what this sector offers is discretionary items, companies in the sector tend to do best when the economy is strongest. Unfortunately, as we will soon see, so do the prices of their stocks tend to perform best when the market is performing best.

The Consumer Discretionary Sector

This is the fifth in a series of articles designed to find value in today's stock market environment. However, it is the fourth of 10 articles covering the 10 major general sectors. In my first article I laid the foundation that represents the two primary underlying ideas supporting the need to publish such a treatise. First and foremost, that it is not a stock market; rather it is a market of stocks. Second, that regardless of the level of the general market, there will always be overvalued, undervalued and fairly valued individual stocks to be found.

My first article was titledSearching For Value Sector By Sector, my second article was titledFinding Great Value In The Energy Sector.My third article was titledFinding Value In The Materials Sector Is A Material Thing. My fourth article was titledThe Industrial Sector Offers A Lot Of Value, Dividend Growth And Income.

As a refresher, my focus in this and all subsequent articles will be on identifying fairly valued dividend growth stocks within each of the 10 general sectors that can be utilized to fund and support retirement portfolios. Therefore, when I am finished, the individual investor interested in designing their own retirement portfolio should find an ample number of selections to properly diversify a dividend growth portfolio with.

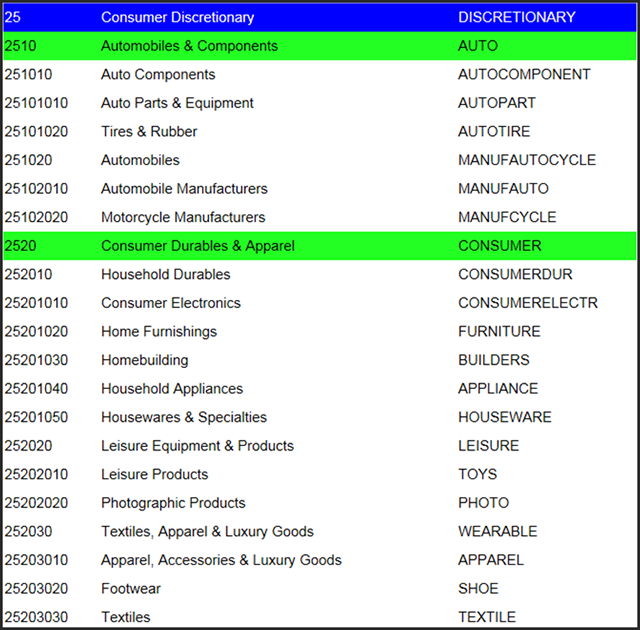

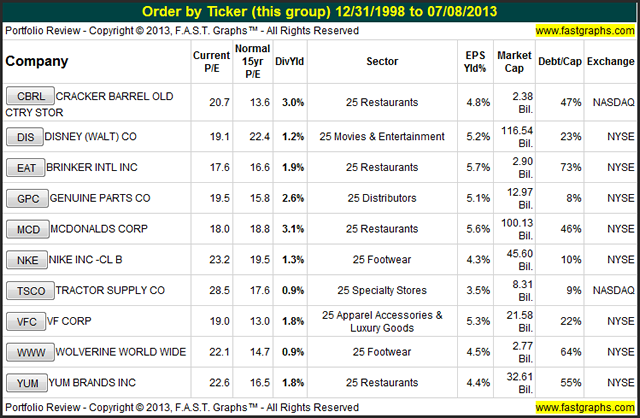

This article will look for undervalued and fairly valued individual companies within the general sector 25-Consumer Discretionary. Within this general sector, there are several subsectors which I list as follows:

My Selection Methodology

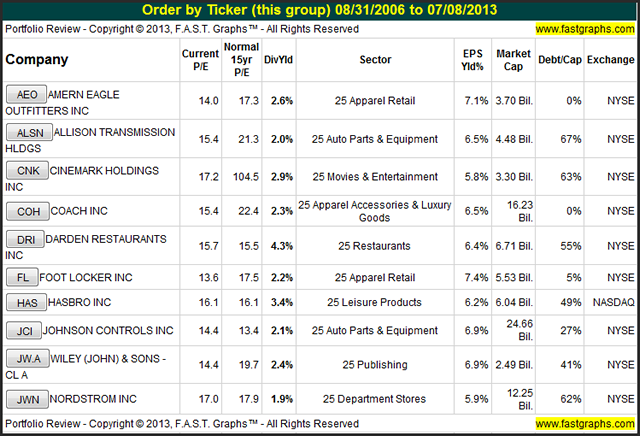

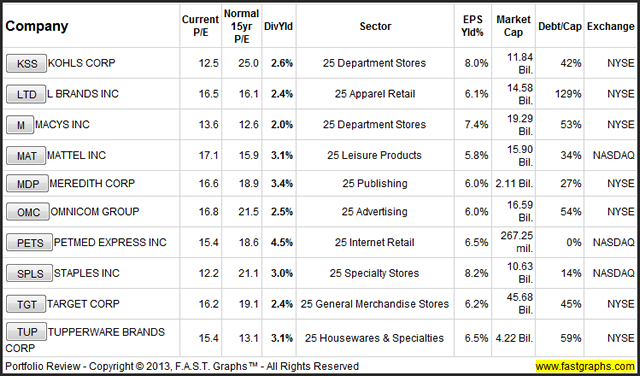

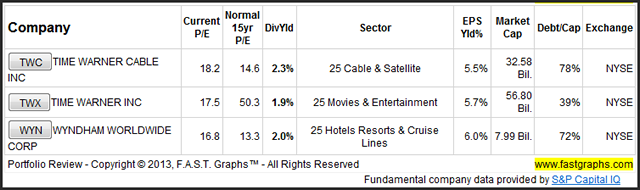

Although I utilized the same selection methodology with this sector as I did with my four previous articles, my results were rather disappointing. What I discovered was that most of my favorite Consumer Discretionary companies were overvalued today. Apparently, the recent run-up in the stock market in general, has driven the valuations of what I considered to be the best-of-breed Consumer Discretionary companies to lofty and overvalued levels. Therefore, with this article I’m going to change my approach a little bit. What follows is a list of 23 Consumer Discretionary companies that I believe possess the characteristics that I personally favor in a dividend growth stock.

The primary characteristics I favor are a consistent historical record of above-average growth of both earnings and dividends, coupled with a valuation worthy of further scrutiny. To me, the idea of the dividend growth stock, especially one worthy of consideration into a retirement portfolio, needs to meet stringent hurdles of quality, predictability and stability. I believe the following list of Consumer Discretionary companies meet most of those criteria close enough to be worthy of additional due diligence.

However, I’m not going to feature any of the companies on this list. Instead, I plan to later take advantage of the opportunity to present an important investment lesson that the Consumer Discretionary sector currently offers by looking at my favorite Consumer Discretionary companies that alas, are overvalued. I believe this will help the dividend growth investor desirous of funding their retirement portfolios more than simply providing a list of good buy candidates.

My Top 10 Best-of-Breed Consumer Discretionary Stocks Are Overvalued

As I reviewed the Consumer Discretionary sector looking for dividend growth stocks that can be purchased at sound valuations, I quickly became very disappointed. Much to my chagrin, I discovered that my very most favorite stocks in this sector have become overvalued during the recent stock market run-up. The following is my top 10 list of favorite companies in the Consumer Discretionary sector that I would like to own if only I could buy them at fair value. But unfortunately, that is not the case at the moment.

The Dangers and Problems of Overvaluation

Perhaps the greatest danger of an overvalued stock is that it often attracts the most investor interest at precisely the time when it is a risky and dangerous investment. The problem is that many investors become interested in the stock solely based on its recent price history. If the stock has been recently rising, the greed factor kicks in, and people want to invest because they don’t want to miss future gains. Consequently, the demand to own a stock is often the highest when its investment merit is the lowest. Within this discussion, there are also lessons to be learned about the dangers of evaluating stocks based on price alone, and/or statistics alone.

The above principle is what inspired Warren Buffett to state: “Youcan’t buy what’s popular and expect to do well.” In other words, the bargains are found in the unpopular stocks, and that is where investors should look for new purchases.

Cracker Barrel Old Country Store (CBRL)

As I will soon illustrate, Cracker Barrel Old Country Store is a terrific company, with a great operating history and a tremendous track record of rewarding its shareholders. A $10,000 investment in Cracker Barrel on December 31, 1998 would have grown to $42,607.60, additionally; shareholders would have received $3,403 in total dividend income. An equal investment on the same day in the S&P 500 turned an equivalent $10,000 investment into only $13,283.58, and total dividends were only $2,138. Furthermore, Cracker Barrel today offers an above-market dividend yield of 3%. These statistics alone are enough to attract many people into investing in this company.

But those numbers are nothing compared to more recent history for Cracker Barrel. Since the beginning of 2012, Cracker Barrel has provided shareholders capital appreciation of 56.6% per annum, and when you add in dividends, the total annual return balloons to 59.3%. This magnificent annual total return occurred during a time when the S&P 500 averaged a very attractive 18.8% capital appreciation.

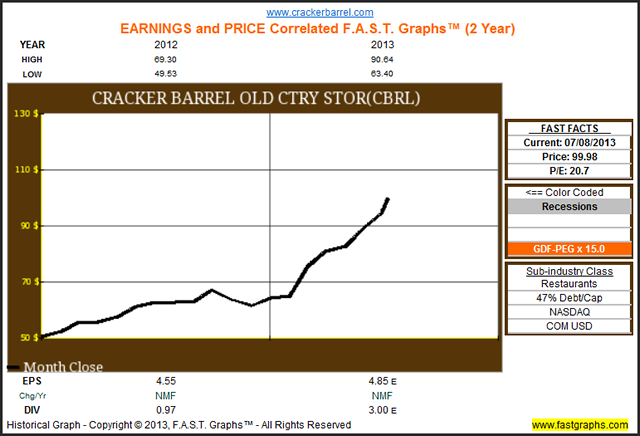

The following price only graph for Cracker Barrel since the beginning of 2012 shows how enticing Cracker Barrel’s stock price recently has been. Unfortunately, most investors only have “price only” graphs at their disposal. In a moment, I will show what a great disadvantage this can be.

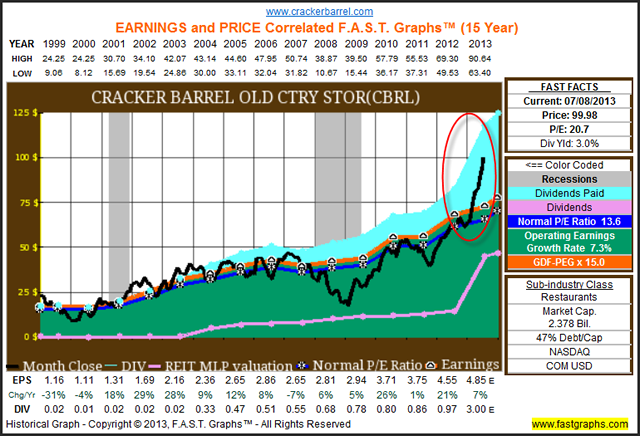

The following earnings and price correlated F.A.S.T. Graphs™illustrates the great disadvantage with “price only” graphs. When you look at stock price (the black line) in correlation to earnings (the orange line), you immediately discover that Cracker Barrel’s stock price crossed over the fair valuation line (the orange line) on approximately February 2013. Subsequently, the price has now risen to one of the highest valuations (current blended P/E ratio of 20.6) that Cracker Barrel has ever traded at. Since a picture is worth 1000 words, the graphic speaks for itself. Although Cracker Barrel’s stock price has on occasion risen above the orange fair value line in the past, it is never risen to this extreme before.

Another fact that this graph reveals relates to possible excuses or rationalizations as to why investors might currently be behaving this way. The pink line on the graph plots dividends per share, and here we see that Cracker Barrel’s payout ratio has recently exploded. To clarify my point, the green shaded area below the pink line represents the portion of earnings paid out to shareholders, a.k.a. the payout ratio. Cracker Barrel’s recent announcement in their third quarter fiscal year-end report that they raised their dividend by 50% to $.75 per share has apparently created some investor excitement. Déjà vu - irrational exuberance anyone?

Consequently, Cracker Barrel could be a poster child for those who now believe that the overall market has become overvalued because of the recent surge in stock price. As this series of articles has been attempting to point out, the overall market does not appear to be overvalued, but there are individual companies that are. Cracker Barrel represents one of those companies, in my opinion.

Interestingly, it’s amazing the difference a few months can make. Here is a link to an articleposted by my associates at F.A.S.T. Graphs™ on October 19, 2012 when Cracker Barrel had an appropriate current P/E ratio of 14.6 and a market price of $66.98. Moreover, on October 19, 2012 Cracker Barrel’s valuation most importantly provided potential investors an earnings yield of 7%. In contrast, Cracker Barrel’s earnings yield today is only a sub optimal 4.9%.

Evaluating Cracker Barrel Utilizing Additional Fundamental Metrics

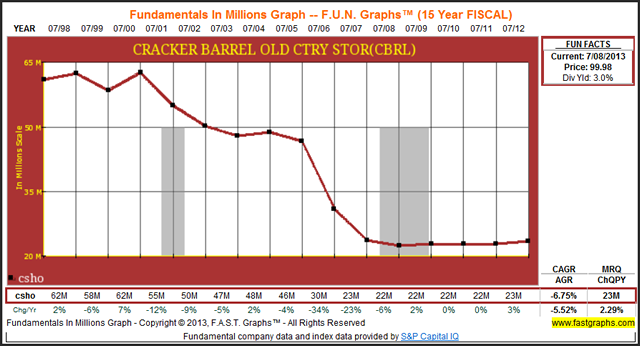

Let’s turn to FUN Graphs (fundamental underlying numbers) to further illustrate how raw statistics can mislead prospective investors. In addition to raising their dividend by 50%, the following graphic reporting common shares outstanding shows that Cracker Barrel has cut their share count from 62 million shares to 23 million shares in their most recent quarter (MRQ). Rising dividends and share buybacks are widely-accepted as shareholder-friendly behavior, which can be very attractive to prospective investors.

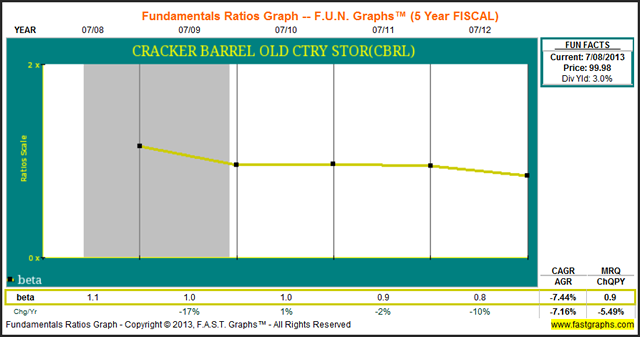

Beta is widely accepted as a measurement of risk by many stock market pundits. A high Beta implies higher risk, and a low Beta implies lower risk. More precisely, Beta is a measurement of volatility relative to the market, and a Beta of one is considered neutral. The following graph shows that Cracker Barrel’s Beta has fallen from 1.1 in fiscal 2009 to a Beta of .8 in fiscal 2012, and in its most recent quarter (MRQ) their Beta is .09. Consequently, just as Cracker Barrel’s stock price has risen to unjustifiable fundamental levels based on earnings, their Beta has steadily fallen, indicating that Cracker Barrel’s stock is less risky today than it was in 2009, 2010 and most of 2011. I believe that common sense indicates otherwise.

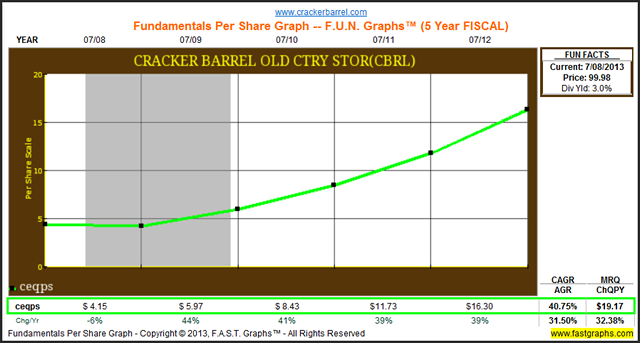

Common equity per share (ceqps) or book value is another major fundamental that many investors and pundits rely on to gauge the investment merit of a given company. Clearly, Cracker Barrel’s book value per share has grown from $4.15 per share by fiscal year-end 2008 to over $19.17 per share during the most recent quarter (MRQ). Therefore, we have another statistic arguing in favor of investing in this quality Consumer Discretionary in the restaurant subsector. We discover a book value that is growing at a compounded annual growth rate (CAGR) of 40.75% since the beginning of fiscal year 2008.

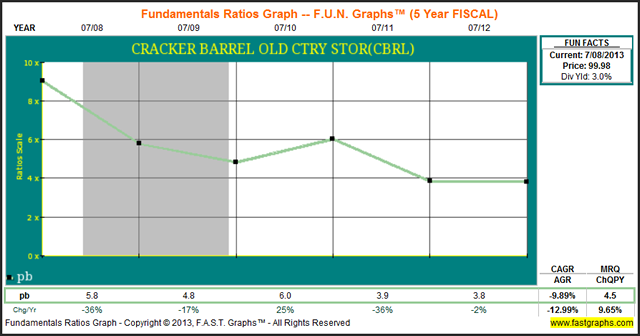

Next let’s look at another popular valuation measurement that many investors and pundits like to utilize, price-to-book value (pb). Here we discover that Cracker Barrel, in spite of its highest P/E ratio in recent years, is simultaneously available at one of its lowest price-to-book values. Cracker Barrel’s fiscal year-end 2012 price-to-book value (pb) of 5.8 is much higher than its most recent quarter price-to-book value of 4.5. This would imply the Cracker Barrel is trading at one of its best valuations in recent history based solely on price-to-book value.

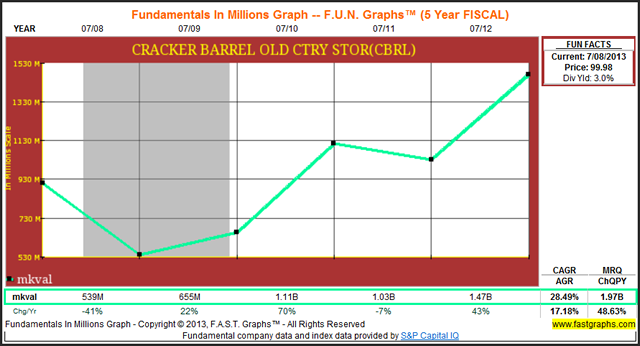

Moreover, a quick peek at Cracker Barrel’s market value over the same timeframe shows that a market value of $1.97 billion at its most recent quarter was its highest ever. However, since Cracker Barrel’s stock price has continued to advance since its most recent quarter, its current market value is now $2.36 billion (see earnings and price correlated F.A.S.T. Graphs™ above). Consequently, I would argue that Cracker Barrel’s highest market value ever in contrast to a low price-to-book value raises a red flag. In other words, further scrutiny is in order.

The point of the above exercise thus far is to illustrate how dangerous it can be to evaluate a business relying on any single widely-accepted statistic and/or fundamental metric in a vacuum. The majority of the fundamentals I covered above would indicate that Cracker Barrel is an extremely high-quality company that’s firing on all cylinders. My point being, that the performance of Cracker Barrel’s operations have been exemplary and I believe there is little argument about that.

However, from a shareholder’s point of view, when you measure price to the bottom line (earnings), we discover a clear picture of overvaluation. It is only through the combination of these clear correlations and functional relationships between the company’s earnings and price that we get a clearer picture of current value. And that picture says that Cracker Barrel is overpriced today. On the other hand, all of these other important fundamental measurements tell us that if we can ever find Cracker Barrel at a fair price based on earnings, that we should jump on it. I can tell a similar story with all of my top 10 overvalued favorite companies listed above.

Summary and Conclusions

When looking for value for the dividend growth investor within the Consumer Discretionary sector, I found very little to be excited about. Although I did provide a list of potential candidates that I felt were in value, my very best choices I feel are overvalued today, with some more than others. For example, I would see McDonald’s as fully valued today whereas Cracker Barrel I have argued is significantly overvalued. My point being, that there are degrees of overvaluation. Nevertheless, I do believe that most of the best choices in the Consumer Discretionary sector as listed above are worth waiting for, but not worth investing in today.

This is the fifth in a series of articles looking for quality dividend growth stocks at sound value amongst the various sectors. The next sector covered in this series will look for value in the sector 30-Consumer Staples.

Disclosure: No position at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs