This is the third in a series of articles designed to find value in today’s stock market environment. However, it is the second of 10 articles covering the 10 major general sectors. In my first article, I laid the foundation that represents the two primary underlying ideas supporting the need to publish such a treatise. First and foremost, that it is not a stock market; rather it is a market of stocks. Second, that regardless of the level of the general market, there will always be overvalued, undervalued and fairly valued individual stocks to be found.

My second article wasFinding Great Value In The Energy Sector. As a refresher, my focus in this and all subsequent articles will be on identifying fairly valued dividend growth stocks within each of the 10 general sectors that can be utilized to fund and support retirement portfolios. Therefore, when I am finished, the individual investor interested in designing their own retirement portfolio should find an ample number of selections to properly diversify a dividend growth portfolio with.

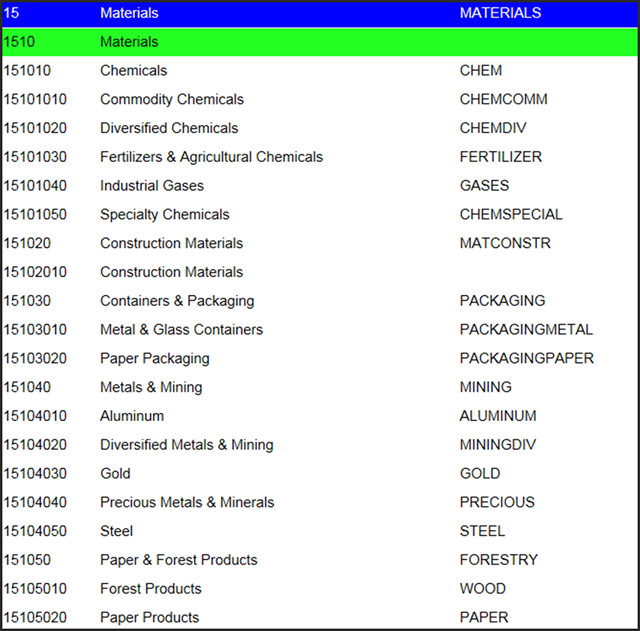

With the above second notion in mind, this article will look for undervalued and fairly valued individual companies within the general sector 15-Materials. Within this general sector, there are several subsectors which I list as follows:

My Selection Methodology

Before I go any further, an important disclosure is in order. I will produce a list of companies in this article (and all subsequent articles), that are names that I have hand-selected from a much larger universe. My selections were made by reviewing the individual earnings and price correlatedF.A.S.T. Graphs™on all appropriate companies that I identified within the sector. Some might say my method of identifying them was not very scientific, but I would counter that it was very thorough and comprehensive. On the other hand, I will admit to it being somewhat arbitrary and based on my own judgments.

Here is the basic method that I utilized. In order to find undervalued or fairly valued companies within the materials sector, I utilized the assistance of the F.A.S.T. Graphs™ screening tool in the following manner. First, I asked the screener to only look for companies within the sector 15-Materials. Then I asked to search for any company within the sector that had a current dividend yield of 1% or better. This is a slight deviation from my article on the energy sector, because I found it very difficult to find quality companies that I felt were in value within the materials sector that also had a dividend yield of 2% or better. Finally, I included ADRs and all companies listed on the Canadian stock exchanges.

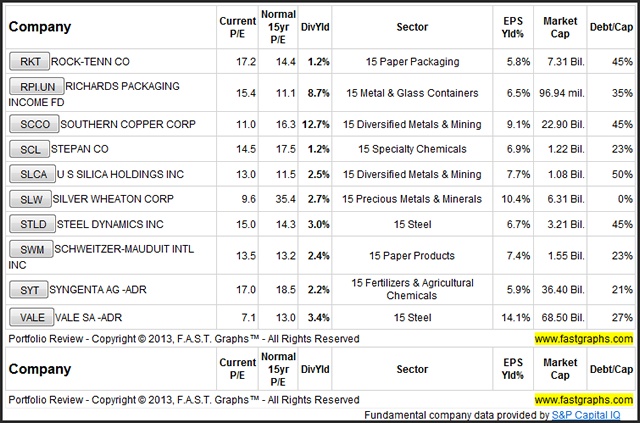

This produced a gross list of 179 individual companies. Then I created a personal portfolio comprised of these 179 individual companies and sorted them in alphabetical order. Next, I reviewed the individual graphs of each company and either rejected it or added it to my final list of potential candidates based on whether or not I felt it had an adequate history and a reasonable level of consistency within that history. But most importantly, I looked for companies that I felt were reasonably valued, or close to it today based on current earnings and expected future earnings growth (or FFO for partnerships and trusts). Then I broke my refined list into two categories:

1. Conservative Growth and Income – 23 companies made this list.

2. Aggressive Growth and Income - 40 companies made this list

Before I present each of these lists, and featured selections from each, it’s important that the reader understands that these are prescreened lists of potential candidates prior to the necessary morecomprehensive research effort. In other words, I am not recommending any of these stocks for current investment. Instead, I am recommending them as companies with historical records that appear reasonably valued, and therefore, worthy of investing the time and effort to take a closer look at. This was a challenge within the materials sector because of the cyclical nature of most of its constituents.

The Materials Sector: General Characteristics and Considerations

The materials sector, also known as the basic materials sector, is generally comprised of companies in the development, processing or discovery of raw materials. This includes the mining and refining of metals, the production of chemicals and forestry products

As I researched individual companies in the materials sector, it became abundantly clear that many of the companies within this sector possessed very cyclical operating histories that were generated based on one of two important factors. First of all, many of the companies within the materials sector are cyclical because, by their very nature, they are very sensitive to the state of the general economy. Consequently, their long-term earnings histories tend to be very cyclical because their underlying businesses are very sensitive to economic weakness. Second, many of the companies in the materials sectors fortunes are tied directly to the underlying price movements of the specific commodities their businesses are centered around.

The basic nature of the companies in the materials sector is a fact that any prospective investor must always keep in mind. Consequently, when I was reviewing each of the companies in the materials sector they reminded me of one of my favorite Aesop’s fables about the scorpion and the frog as follows:

The Scorpion and the Frog

A scorpion and a frog meet on the bank of a stream and the scorpion asks the frog to carry him across on its back. The frog asks, "How do I know you won't sting me?" The scorpion says, "Because if I do, I will die too."

The frog is satisfied, and they set out, but in midstream, the scorpion stings the frog. The frog feels the onset of paralysis and starts to sink, knowing they both will drown, but has just enough time to gasp "Why?"

Replies the scorpion: "I am a scorpion, it is my nature to sting…"

Other important characteristics that go hand-in-hand with what I described above relate to the growth potential of companies in the materials sector. For the most part, cyclicality also brings about low average long-term growth rates. Therefore, generally speaking, the best and most well-known companies in the materials sector tend to have low to moderate historical earnings growth rates. However, as with any rule, there are always exceptions. Nevertheless, you have to look very hard at the materials sector to find any companies that could be classified as fast, or even above-average growth companies. But there are a few.

Conservative Growth and Income Featured Selections

Frankly, it was difficult to classify companies in the materials sector as either conservative or aggressive. Due to the cyclicality mentioned above, and/or since many of this sector’s companies future prospects are directly tied to the price of the underlying commodity, it was difficult for me to not think of all of them as aggressive. On the other hand, in spite of the cyclicality of their earnings, most of the companies on the conservative list have consistent long-term records of paying a dividend without cutting it during economic weakness. But at the same time, it’s hard to find any growth with their dividends either.

Perspectives on Valuation

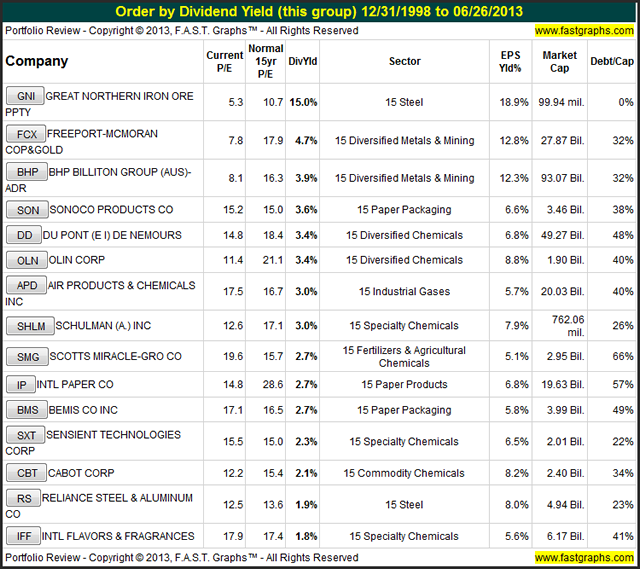

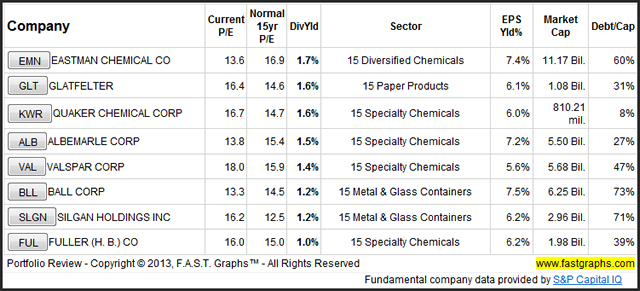

The following portfolio review lists the 23 conservative selections from the materials sector in order of dividend yield highest to lowest. Since as I previously mentioned, growth is hard to come by in this sector, stable dividends would tend to be an important component attracting investor interest. Consequently, even though all of these selections are also offered as appearing to be fairly valued, that doesn’t necessarily mean that they also represent good investments because of it. One of the benefits of reviewing this sector, is it gives me an opportunity to clarify an important principle regarding valuation and its relevance to return.

More simply stated, your future total returns are a function of both valuation and earnings growth. Consequently, it does not necessarily follow that simply because a company is technically trading at a sound valuation, that it can generate a high future return. Fair value represents the current soundness of your transaction based on the earnings yield that your purchase price corresponds to. Your future return, however, will be predicated on the future rate of growth of the earnings and dividends (if the company pays dividends). I have written a three-part series that elaborates more and these principles for any reader that is interested in a deeper understanding of these principles:

How to Know What Rate of Return to Expect from your Stocks: Part 1

How to Know What Rate of Return to Expect from your Stocks: Part 2

How to Forecast Future Stock Returns: Part 3

Featured Companies

In order to provide the reader with better insights into the opportunities for investment available in the materials sector, I feature the following companies from my so-called conservative list. Since a picture is worth 1000 words, I’m going to rely on the fundamentals analyzer software tool F.A.S.T. Graphs™ to illustrate the characteristics and types of companies available in this sector. Therefore, I ask that the reader spend some time looking over the graphs in order to see what each reveals about the company and the sector. However, I will provide brief commentary on each.

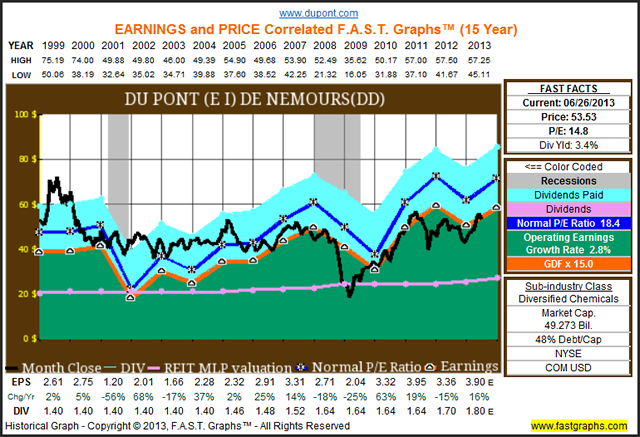

DuPont (DD)

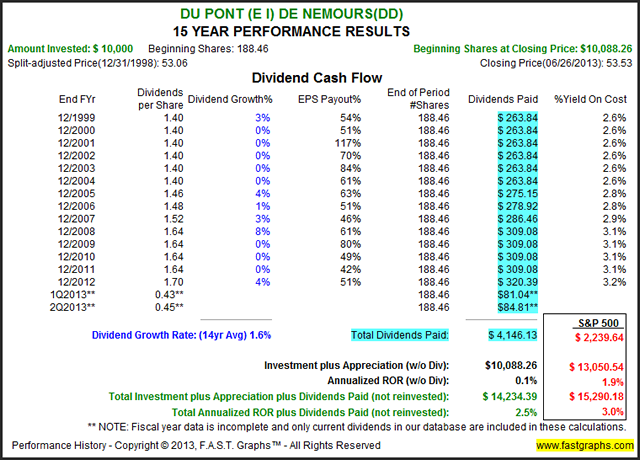

DuPont is a very well-known company in the materials sector. As you can see by looking at the orange earnings justified valuation line, the company’s earnings are very cyclical, and highly sensitive to recessions. Correspondingly, the long-term average growth rate at 2.8% is also very low. However, as we see by the pink line plotting dividends, DuPont’s dividend record is consistent, but not great relative to growth.

When reviewing the performance results associated with the above graph, the reader’s key focus should be on the appreciation component, or lack thereof. A high beginning valuation coupled with a low rate of cyclical growth produced scant capital gains. Moreover, the dividend was quite consistent, but since dividends are functionally related to earnings, average growth was also very low.

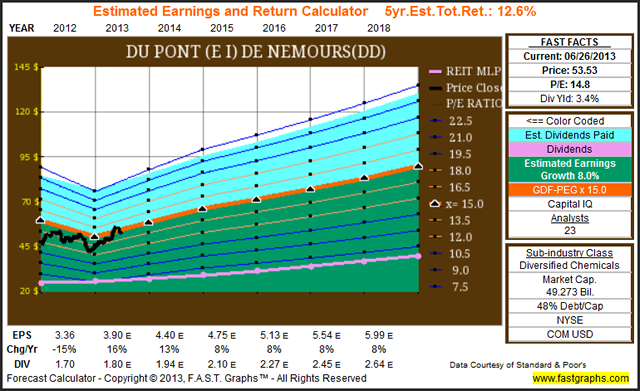

I have often written in the past that the key to long-term investment success is forecasting future earnings as correctly as humanly possible. The following estimated earnings and return calculator is based on the consensus of leading analysts reporting to Standard & Poor’s Capital IQ. Based on their consensus estimates, the calculations would theoretically be true. However, by referring back to the company’s historical operating history, it brings the consistency portrayed with this graph under question. In other words, I find it hard to believe that the future can look as smooth as this graph depicts.

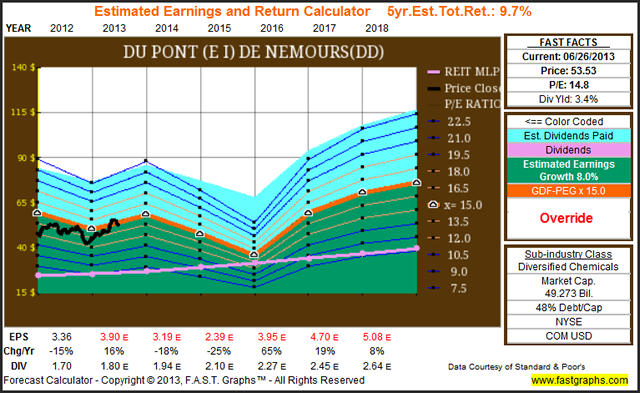

Therefore, utilizing the override feature of the F.A.S.T. Graphs™ “Estimated Earnings and Return Calculator,” I created the following hypothetical calculations. I simply took the operating history of the previous six years, and utilized them as a template with which to forecast what the future might more realistically look like for DuPont. Although these numbers are completely hypothetical, I believe that these potential future results, or something close to them, might be a more reasonable forecast. I repeat, these results are based on attempting to emulate their historical pattern, and not on any deep analysis of each of the future year’s earnings.

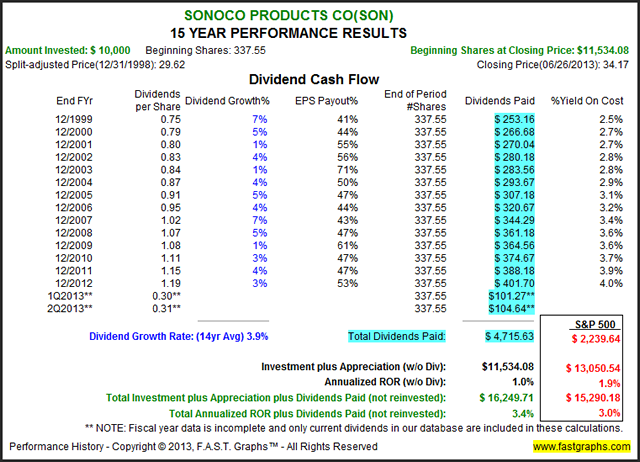

Sunoco Products Company (SON)

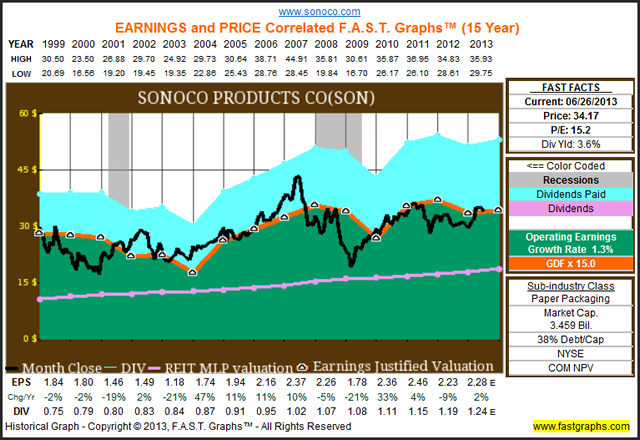

I chose my second example, Sunoco Products Company, because I felt it really illustrates the long-term earnings and price relationship, and how fair value represents soundness, but not necessarily a great return. Sunoco Products’ stock price clearly tracks earnings, and whenever the price deviates from earnings over or under, it quickly returns to the orange earnings justified valuation line. Importantly, the company was reasonably valued at the start of this time period as well as at the end. What’s more, we see a second example where bouts of cyclicality did not impact a steady record of increasing dividends.

The following performance results associated with the above graph on Sunoco Products shows that performance is functionally related to earnings growth. Sunoco Products only generated a 1.3% earnings growth rate, which produced a similar 1% capital appreciation rate. Dividends contributed the majority of the return for shareholders of this company, which increased the total annualized rate of return to a respectable 3.4% per annum. Remember, the company was at fair value at both the beginning and the end of this specific time period measured.

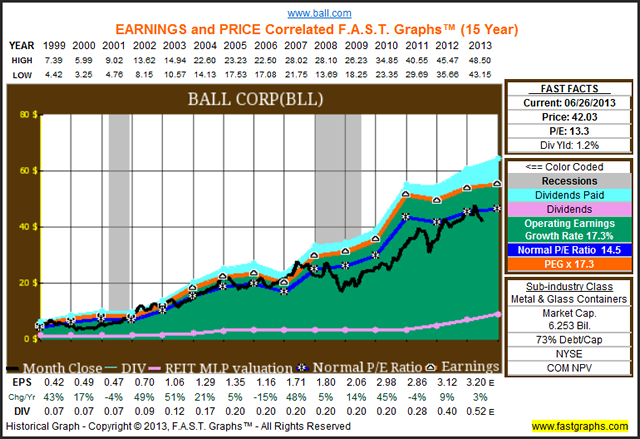

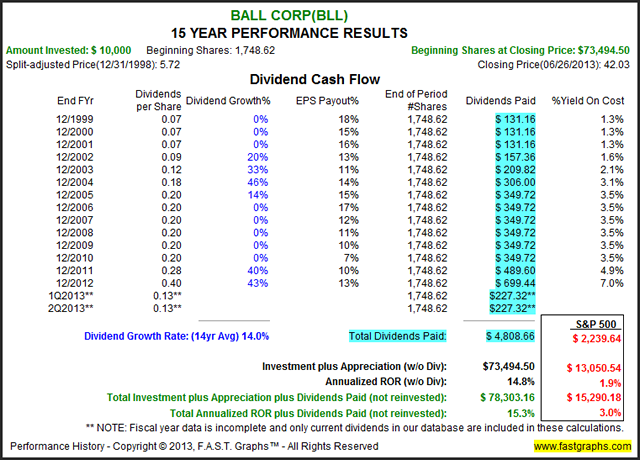

Ball Corp (BLL)

I offer Ball Corp. as an example of a high-quality materials company that has achieved a significant above-average rate of earnings growth rate of 17.3%. Although we still see some cyclicality with this blue-chip of the materials sector, its average long-term growth rate is extraordinary. However, I also point the reader’s attention to the 73% debt to capital found in the FAST FACTS tables to the right of the graph.

The long-term performance associated with Ball Corp. once again illustrates that long-term return is a function of valuation and earnings growth. Ball Corp. started out fairly valued, is currently undervalued, but is growing earnings at 17.3% per annum. Nevertheless, capital appreciation of 14.8% per annum closely correlates to the company’s earnings growth adjusted for current undervaluation. This example also corroborates the underlying thesis of this series of articles that “it is a market of stocks not a stock market.”

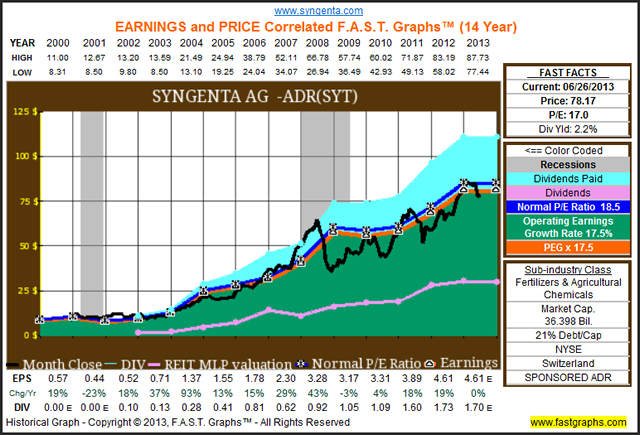

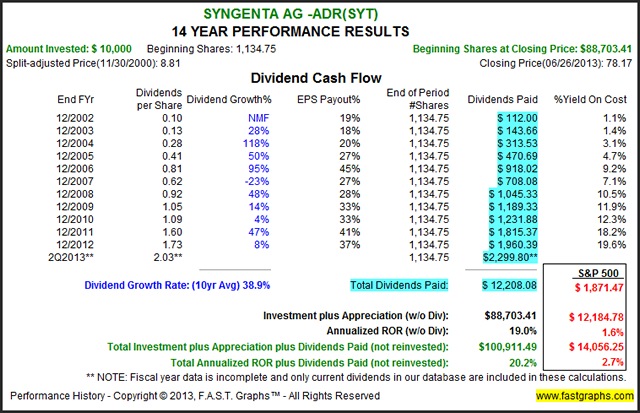

Syngenta AG – ADR (SYT)

The following graphs on Syngenta AG present a second example, similar to Ball Corporation above, that validates the truth that there are a few exciting companies available for investment in the materials sector. I will let the earnings and price correlated graph and the performance table speak for themselves.

Aggressive Growth and Income Featured Selections

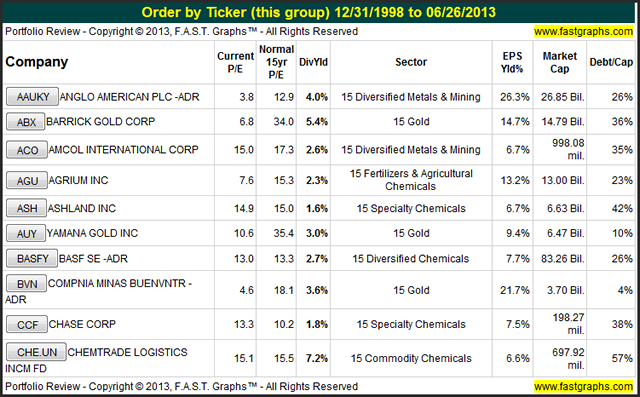

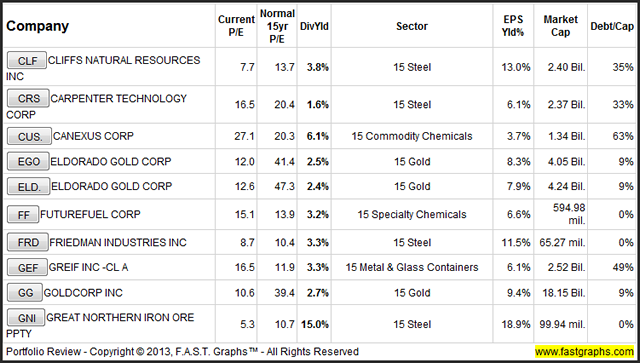

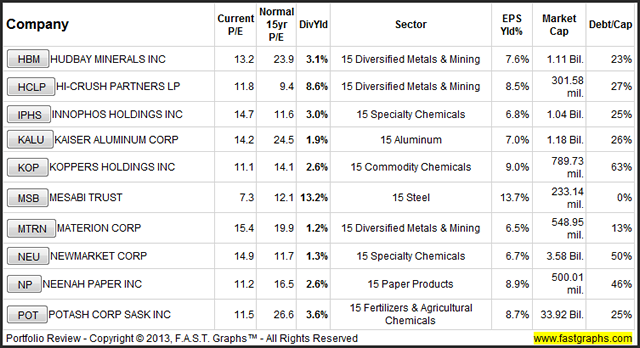

I identified 40 what I have classified as aggressive growth and income selections within the materials sector. However, the primary basis from which I presented this list on was valuation. There are some good dividend stocks here, and even some total return growth oriented selections. However, I caution that the reader not be disappointed, because there are some very spicy selections amongst this group.

You will find some with incredibly volatile operating histories that were included as speculations, primarily due to extremely low current valuations. In other words, low valuation was their salient feature. There are also several that have solid and even some with spectacular earnings growth rates. You will also find many different market caps, from very small to very big. In other words, there is no consistent thesis for investment amongst this group. Instead, I believe they represent an eclectic grouping of very aggressive selections. The only consistency amongst all these companies, is that they all appear undervalued and some even extremely so.

Featured Aggressive Growth and Income Selections

A discussion of investment opportunities within the materials sector would not be complete without a look at gold and silver companies. Both of these precious metal commodities have generated significant investor fervor in recent years. With both gold and silver, we saw an extended period of time where prices rose to stratospheric levels, and more recently, advocates have watched in abject horror as prices of both gold and silver have literally collapsed. Moreover, although I do not consider myself an expert in trading commodities or precious metals, I do believe I have something to offer in regards to investing in companies whose businesses are based on them.

Therefore, my first two featured companies under my aggressive growth and income section of this article on the materials sector will examine Silver Wheaton Corp. and Gold Corp. I want to once again remind the reader that these featured companies are not recommendations for investment. Instead, they are presented because of the principles and investing lessons that I believe their examination reveals.

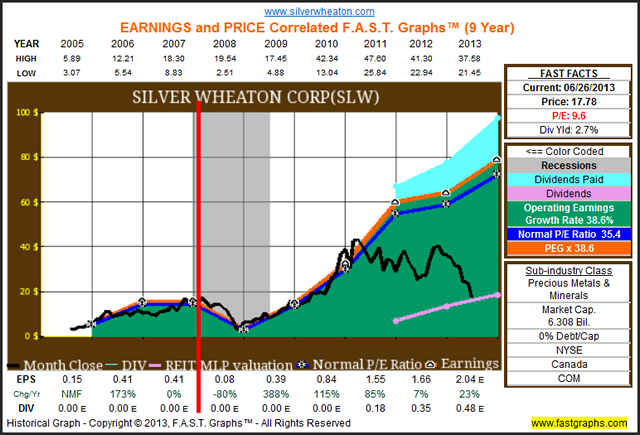

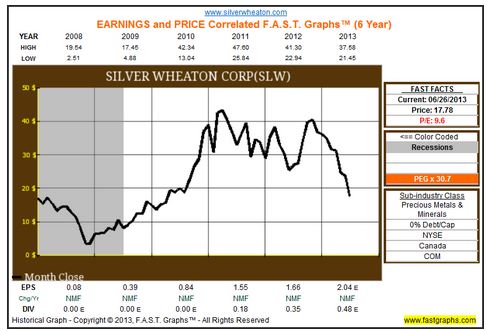

Silver Wheaton Corp. (SLW)

The following earnings and price correlated graph on Silver Wheaton Corp. since the company went public in 2005, reveals some interesting aspects. For starters, Silver Wheaton generates most of its revenues from silver sales. However, the company does not own or operate mines, but instead buys the base metals from companies that do. Consequently, prospects for profits and growth are highly dependent, but not totally, on the price of silver.

With the above said, the earnings and price correlated graph on Silver Wheaton reveals some fascinating correlations and relationships. For starters, we see that price almost perfectly tracked earnings from the company’s inception up through calendar year 2011. But here’s where it gets interesting, and perhaps even confusing. Earnings in 2011 and 2012 were strong, but silver prices fell precipitously since the beginning of 2011.

On the other hand, as I will soon reveal, Silver Wheaton’s stock price since 2008 has almost perfectly correlated with the price action of silver. This begs the question as to how the company’s profits have continued to grow in spite of falling silver prices. At this point, I do not have the answer, because I have not conducted comprehensive due diligence on this company. However, I would never invest in Silver Wheaton unless I was able to resolve the answer to this important question with a high degree of confidence that I understood why earnings have continued to advance.

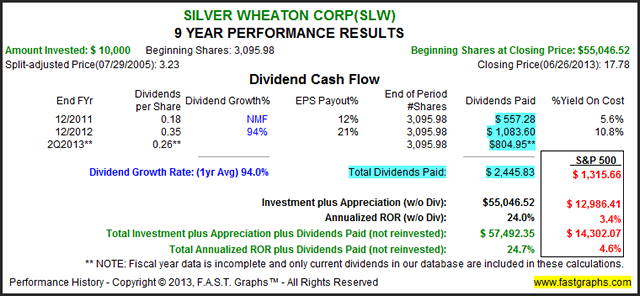

Regardless of Silver Wheaton’s current low valuation long-term shareholders have been lavishly rewarded. Therefore, if this company is truly as inexpensive as it currently looks, long-term returns could be exceptional. On the basis of extremely low valuation, this certainly seems like a worthy candidate for a deeper look.

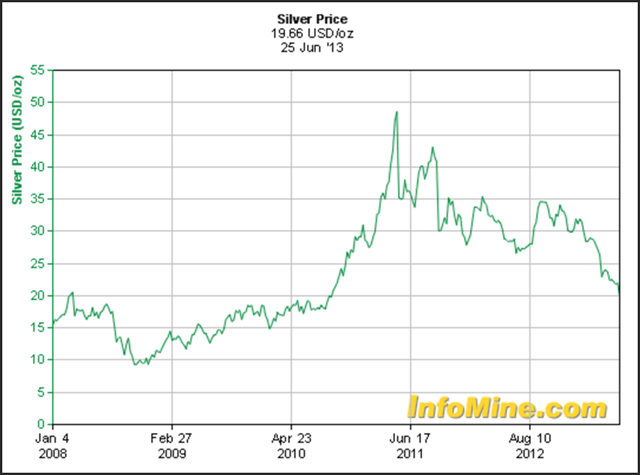

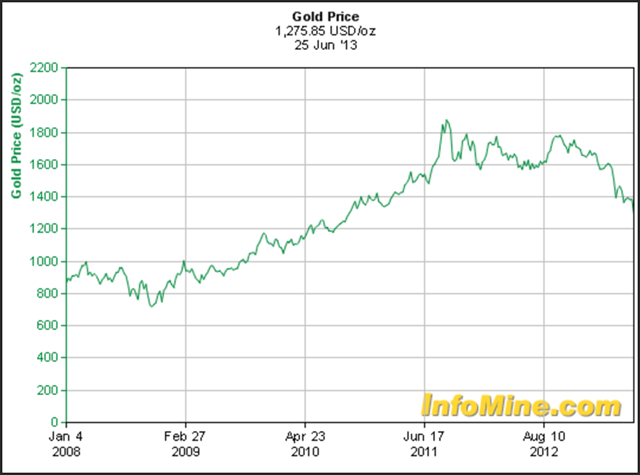

Stock Price Correlated to Precious Metals Prices (gold and silver)

I offer the next two graphs to illustrate the almost uncanny and perfect correlation between the price of Silver Wheaton’s stock to the price of silver. The first graph plots the price of silver since early 2004. The next graph plots price only for Silver Wheaton over approximately the exact same time period (note this price only graph corresponds to Silver Wheaton’s stock price to the right of the red vertical line on the previous graph). My point being that since early 2008, Silver Wheaton’s stock price has deviated from its theoretically earnings justified levels, and instead has almost perfectly tracked the price of silver since 2008.

Therefore, do I believe the company with its excellent operating history and its strong forecasts, or do I turn my attention solely to what might happen with the price of silver? These are questions that I suggest a prospective investor must answer successfully.

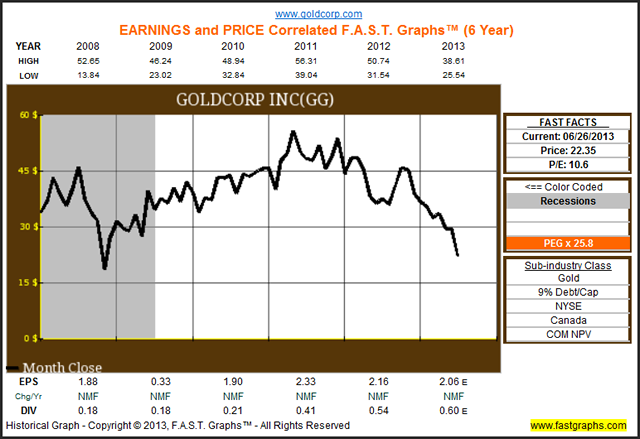

The following two graphs provide a similar analysis of GoldCorp. Inc.’s stock price since early 2008 and correlates them with the price of gold. As we did with Silver Wheaton above, we see an uncanny correlation between GoldCorp’s stock price and the price of gold itself.

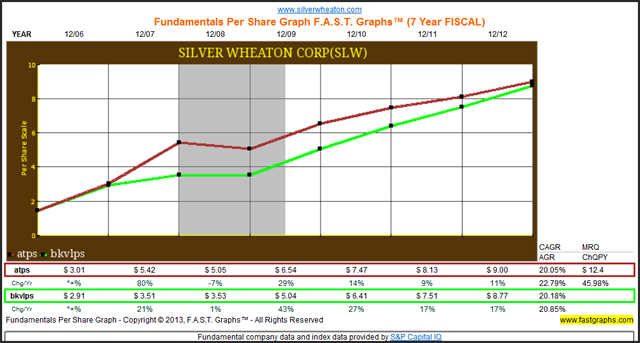

Assets and Book Value Per Share

Before I leave these precious metal examples, I offer the following graph that plots Silver Wheaton’s total assets per share divided by common shares outstanding (atps) and its book value per share (bkvlps). What I feel these graphs indicate is that Silver Wheaton possesses a lot of natural leverage that might indicate strong future profitability if silver prices (and gold to a lesser extent), were to rise again.

Additional Featured Companies In The Materials Sector

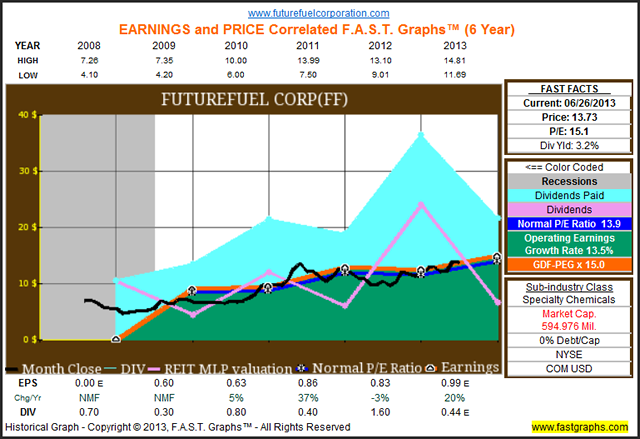

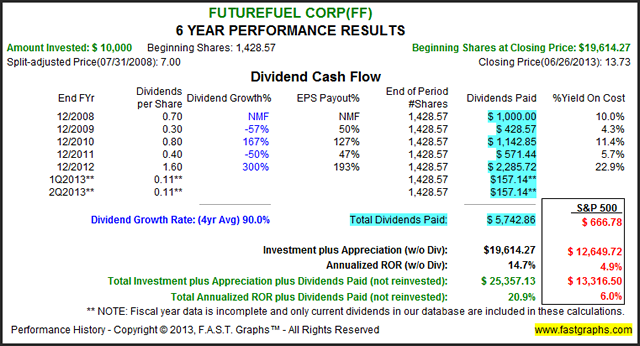

I will close this article by featuring two additional companies. The first one is Future Fuel Corp. (FF) that I feel is both interesting and unique at the same time within this sector.

Future Fuel Corp.

Future Fuel Corp., from their website: “FutureFuel develops, manufactures, and markets products within two segments: Chemicals andBiofuels. The Chemicals segment is comprised of two components:Custom ManufacturingandPerformance Chemicals. Performance Chemicals includes our own branded line of specialty chemical products.”

Future Fuel is a relatively young company with a good record of growing earnings, and a history of paying special dividends along the way. Consequently, I felt this young company was worthy of mention in this article.

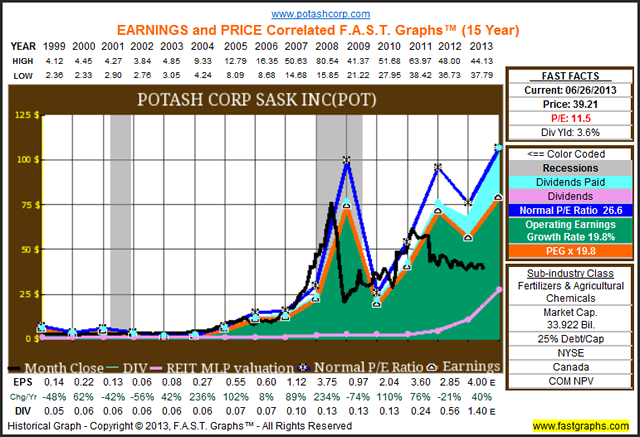

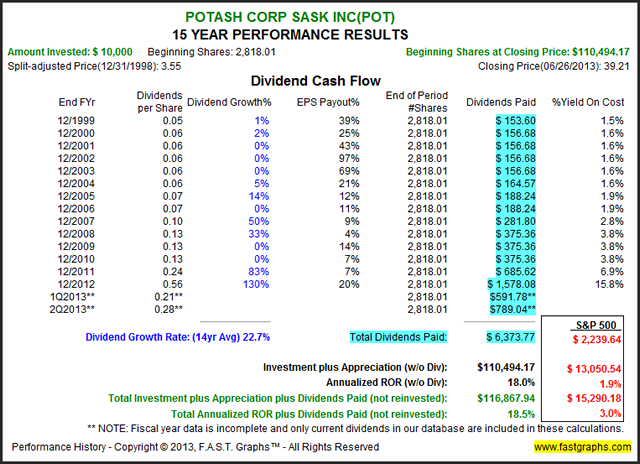

Potash Corp (POT)

My second example is Potash Corp, a fertilizers and agricultural company that is as basic to the materials sector as you can get. You can see that this company is somewhat of an enigma for investors to analyze. First of all, its average long-term growth of earnings is very high, but with extreme bouts of cyclicality. Recently the company has increased its payout ratio and offers an attractive 3.6% current dividend yield.

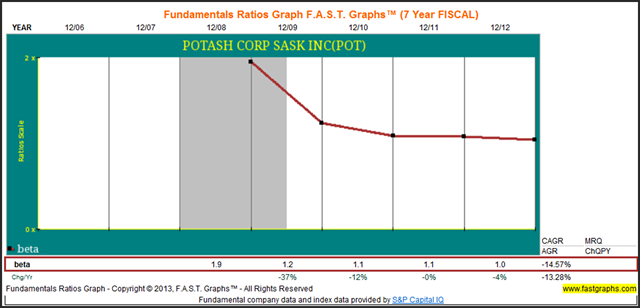

Potash Corp’s 5-Year Historical Beta

In spite of the cyclical nature of Potash Corp’s operating history, its long-term performance has been exceptional. Both dividend income and capital appreciation have greatly exceeded the average company as represented by the S&P 500. However, investors might consider the cyclical nature of the company as well as its high beta. However, as the following graph depicts, the beta on Potash has steadily fallen over the past five years from 1.9 to currently a market neutral 1.

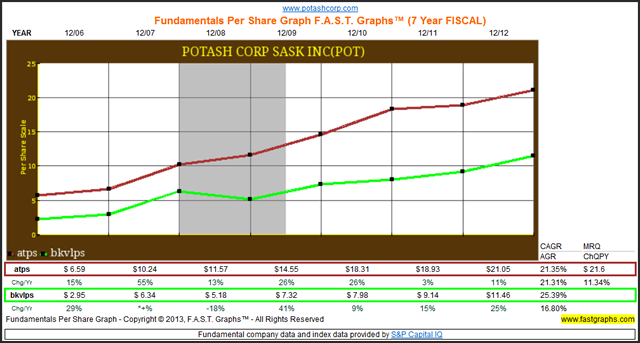

When evaluating Potash based on asset growth per share (atps) and book value per share (bkvlps), we see steady growth and very little cyclicality. Consequently, today’s low valuation may represent an excellent opportunity for aggressive investors to acquire Potash Corp.

Assets and Book Value Per Share

Summary and Conclusions

Companies in the materials sector can best be thought of as cyclical companies and/or commodity based companies. Consequently, as it relates to valuation, companies in the materials sector are often dependent on the price movement of a macro variable of either the price of the underlying commodity, or the health of the underlying economy. Since both of these macro events move in cycles, correctly predicting future cash flows and earnings can be a difficult task. On the other hand, as it relates to the dividend growth investor, they might take solace in the fact that in spite of their cyclical natures, most companies in the materials sector have consistent records of steady and growing dividends.

This is the third in a series of articles looking for value amongst the various sectors. The next sector covered in this series will look for value in the sector 20-Industrials.

Disclaimer: No positions at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs