IN THIS ISSUE:

1. Fed to Continue QE – Stocks & Bonds Plunge Anyway

2. Fed’s QE Has Raised, Not Lowered, Treasury Yields

3. FedZIRP, Not QE, is Causing Low Interest Rates

4. Surviving QE:How to Invest in Today’s Crazy Markets

Overview

Today I hope to dispel the myth that the Fed’s massive quantitative easing (QE) policy has driven long-term interest rates lower. I will argue that the opposite is true and demonstrate that the yield on the 10-year Treasury note has actuallyrisen during QE-1, QE-2 and QE-3. This flies in the face of most market commentators.

Before we get into that discussion, I will review the highlights of the Fed’s policy announcement last Wednesday and Chairman Bernanke’s press conference afterward. Obviously, the biggest news was the fact that the Fed decided to continue its $85 billion a month in purchases of bonds and mortgages at least until the end of the year. Many feared that the Fed would start “tapering” immediately.

You would have thought that the Fed’s decision to continue QE as is for at least the rest of the year would have been good news for stocks and bonds, but instead both markets cratered last week. So what is going on? Apparently, stocks and bonds are addicted to QE and want it to continue forever. In light of that, how should you position your portfolio now?

The extreme selloff in the markets in the days following the Fed’s decision last Wednesday has prompted many investors to bail out of stocks and bonds because of short-term emotions. I'll close today by revisiting the fact that we need to keep our emotions out of investment decisions, and why managing for “absolute returns” is a far more realistic approach. As a bonus, I'll also show you how to download your free copy of my Absolute Returns Special Report.

Fed To Continue QE – But Stocks & Bonds Plunge Anyway

Analysts around the world watched closely last Wednesday as the Fed Open Market Committee (FOMC) policy statement confirmed that QE-3 will continue for a while longer. As such, the Fed’s record balance sheet of $3.4 trillion will continue to rise rapidly. The FOMC also voted to keep the Fed Funds rate near zero at least through 2014.

The FOMC also revised upward its forecasts for the economy. The Committee sees growth in gross domestic product of 3% to 3.5% in 2014, up from a projected range of 2.9% to 3.4% in March. The Committee also revised its projected unemployment range to 6.5% - 6.8% by the end of 2014, better than its previous forecast of 6.8% to 7%.

During the press conference reporters pressed Bernanke hard to get a more specific timeline for ending QE, but as usual, he was very elusive. Bernanke hinted that the FOMC hopes the economy will be strong enough to start reducing monthly QE purchases by the end of the year, and hopefully end the program by mid-2014. That was the media’s main takeaway from the press conference – QE is ending. And the stock and bond markets tumbled!

However, my main takeaway from the press conference was something different. Early-on in his prepared remarks, Bernanke once again hinted that the Fed might elect to simply hold the Treasury bonds in its huge portfolio to maturity, rather than selling them back into the market at some point. Bernanke first floated this trial balloon when testifying before the House Financial Services Committee on February 27, when he stated:

“The one thing we could do differently is hold some of the securities a little longer… We could even let them just run off [mature].”

The fact that he again hinted at holding the Treasury bonds to maturity tells me that this is something the Fed is considering very seriously, especially since he was reading from a prepared script that, as always, was meticulously worded. Analysts have worried for the last several years that if the Fed decides to sell the trillions in Treasuries it holds, it would spike interest rates and throw the economy back into recession. It is looking increasingly likely that the Fed will just let those bonds mature.

The strangest thing about this is the fact that bonds and stocks both sold off hard on Wednesday afternoon and even worse on Thursday, even though Bernanke made it clear that the Fed is not ending QE anytime soon. And further that the Fed is still considering holding its Treasury bond portfolio to maturity.

Both of these developments should have been positive news for bonds, at the very least. Yet just about everything plunged in value – including precious metals and commodities – late Wednesday and again on Thursday and to a lesser extent since then. About the only thing that managed to rally after the press conference was the US dollar.

As noted above, the only thing the markets took from the FOMC policy statement and Bernanke’s press conference was that QE is ending. This despite Bernanke’s repeated statements that the Fed could doless OR more QE – depending solely on how the economy does going forward.

In my view, the stock and bond markets over-reacted to the Fed’s decision, especially since Bernanke repeatedly said it all depends on the economic data ahead.

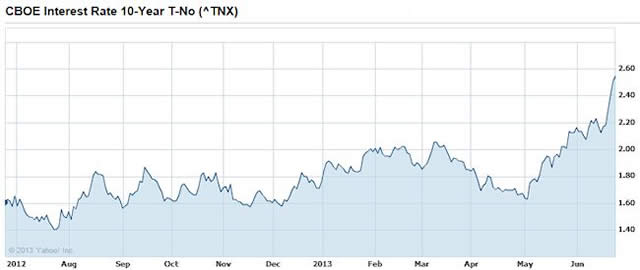

Fed’s QE Has Raised, Not Lowered, Treasury Yields

According to Bernanke, the three rounds of quantitative easing were designed to lower interest rates and stimulate the economy, and most market analysts believe they have worked at least to some degree. Indeed the Fed Funds rate has been near zero since late 2008. But when it comes to longer-term bonds, a strong argument can be made that QE has actually caused yields torise.

Let’s look at the three rounds of QE and what effect they had on 10-year Treasury notes. Each round of QE included large Fed purchases of government debt and mortgage-backed securities (MBS). Hat tip to Forbes writer Richard Salsman who crunched the interest data below.

QE-1 was formally adopted in March 2009, when the US 10-year T-note yield was 2.53%, but by the end of QE-1 in March 2010, the yield had moved up to 3.83%, for a rise of 130 basis points (over 50% higher).

When the Fed launched QE-2 in November 2010, the T-note yield was 2.62%, but it rose to 3.16% when QE-2 was ended in June 2011 – a rise of more than 50 basis points.

QE-3 began at the end of 2012 with the Fed buying $45 billion a month in 30-year T-bonds and $40 billion in MBS. When QE-3 began late last year, the T-note yield was 1.76%, but it was up to 2.38% before the FOMC decision on Wednesday– and since then to 2.60% today.

Now consider the interim periods since 2009, when QE was absent. Commentators would probably surmise that the 10-year T-note yield must have jumped in such periods. Not so. In fact, the yield decreased. In the period between QE-1 and QE-2 (March 2010 to November 2010) the T-note yield declined 0.57 basis points, and in the period between QE-2 and QE-3 (June 2011 and December 2012) it declined by 140 basis points.

Maybe this explains why T-note and T-bond yields went up sharply last Wednesday when the Fed announced that it will continue QE-3, most likely until the end of this year. If the Fed was really planning to end QE-3 now, Treasury yields would likely be moving down already.

Some analysts fear that QE will be inflationary down the road and cite that as the reason long rates have moved up during each round of Fed bond buying. However, one of the Fed’s favorite gauges of inflation – CPI minus food and energy – rose only 1.1% in the 12 months ended April 30. That matches the smallest 12-month gain since records started in 1960.

With inflation well below the Fed’s 2% long-run goal and the unemployment rate at 7.6%, the Fed is falling short of its dual mandate to ensure stable prices and maximum employment. This, too, is another indictment of QE.

ZIRP, Not QE, Causing Low Interest Rates

The Fed’s zero interest rate policy – “ZIRP” – is the main factor that has driven interest rates so low in recent years. The Fed Funds rate has been mostly below 0.25% since early 2009. Bernanke said last Wednesday that the Fed intends to keep it in that range until the end of 2014, unless the economy heats up considerably.

ZIRP invites bond traders to profit by borrowing cheaply in the short-term and investing in longer-term debt at higher yields. It’s also possible for central banks to depress bond yields this way. But what we need to remember is that prolonged ZIRP also causes stagnation in economic investment and growth.

The potential for a serious bust in T-notes and bonds (steadily rising yields) comes less from the end of QE-3, and more from the potential end of ZIRP. But when might that happen? Japan has retained its ZIRP for many years longer than it initially intended. The same could be true here as well. On the other hand, the hawks on the FOMC could prevail in the months ahead and do away with ZIRP after Bernanke steps down next January.

The futures markets offer reasonably reliable estimates of future Fed policy, and today futures are pricing in a Fed Funds rate around 0.21% a year from now and about 0.58% two years from now (June 2015). Although markets expect a resumption of Fed rate-hiking at some point, they suggest the new rate, when it comes to pass, won’t be significantly higher from today’s rate. It’s not as though markets expect the Fed to re-establish a funds rate of 2-3% anytime soon.

Surviving QE: How to Invest in Today’s Crazy Markets

If there’s any takeaway from today’s discussion regarding the Fed, it’s that investors have been at the whim of forces outside of normal market behavior. Sure, we all know that news can sometimes move the stock and bond markets, but intervention by a quasi-governmental entity like the Fed is a different story. Investors don’t know what to do and there’s no advisor on the planet that can accurately predict what will occur in the markets over the short-term (despite what they may claim).

So what is the best advice for an investor in today’s uncertain markets? I can tell you in one short sentence: Take your eyes off of the short-term.

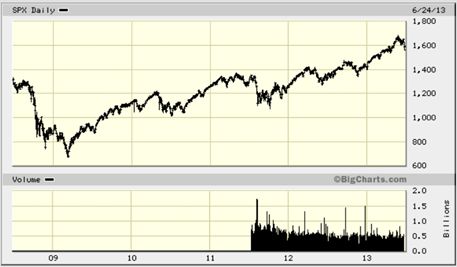

Let’s take the last several years for example. Over that time, we’ve had two previous quantitative easing programs begin and end, each with its own short-term market mayhem. We’ve also weathered a European sovereign debt crisis (remember that?), a Libor rate-fixing conspiracy and countless interpretations of what the market thought Ben Bernanke said, or didn’t say. Each of these events also coincided with its own short-term pullback in the stock market.

Yet what has been the general direction of the S&P 500 Index since the 2009 lows? As the graph below shows, it’s been an upward trend, as a general rule:

Unfortunately, many investors focused only on the short-term negative events and missed out on the overall longer-term upward trend. There’s a behavioral finance term for this type of activity, but let’s just call it “being human.”

Unfortunately, many investors focused only on the short-term negative events and missed out on the overall longer-term upward trend. There’s a behavioral finance term for this type of activity, but let’s just call it “being human.”

It’s just human nature for short-term events and expectations to have a greater effect than long-term issues. That means we often put off long-term planning in favor of short-term gratification. If that were not the case, lots more Baby Boomers would have saved enough for retirement rather than consuming all of their income over the years.

So, is the answer to have an investment plan that consists of “set it and forget it?” No, although the fat cats on Wall Street would love for you to think that way. It’s in their best interests for you to stay invested at all times, so they champion asset allocation programs that passively buy and hold a group of stocks, bonds, mutual funds and/or ETFs and let the chips fall where they may.

Since the general direction of the market has been upward over extended periods of time, should you just buy the latest buy-and-hold allocation and forget about it? Actually, that would probably work IF you could forget about it. The problem is another nasty human trait called emotions.

Most of us have an emotional trigger beyond which we can no longer remain invested. For some, this means they cannot tolerate any losses, so they accept the low returns offered by CDs and fixed annuities in exchange for safety of principal. At the other end of the spectrum are speculators who can theoretically lose an amount greater than their original investments. Think venture financing, options and futures.

The rest of us occupy that middle ground where some loss is OK, but too much is intolerable. At the point where emotions take over, investments are liquidated in order to stop the pain of loss. Since the stock and bond markets can have wild swings, losing as much as 50% or more of their value, the result is that many investors end up buying high and selling low – just the opposite of the desired outcome.

Given the above discussion about how we as humans tend to put too much stock in the short- term concerns and our emotions often rule our investment decisions, what’s the solution? I have two words for you: Absolute Returns.

“Absolute returns” refer to investment strategies that seek to produce consistently positive returns without regard to the performance of the stock and bond market indexes. Think of it this way – when you planned for your future financial goals, you probably determined an average return that you’d need to earn on your investments, year-in and year-out, to reach your goals. That, in a nutshell, becomes your absolute return target.

When using absolute return strategies, the short-term performance of stock and bond market indexes becomes irrelevant. This, in turn, allows you to invest in such a way as to avoid taking too much risk. After all, investing in such a way as to “beat the market” has left many investors short of their investment goals because it usually requires investing in more aggressive strategies with the potential to boost the returns.

Best of all, using an absolute return target allows you to periodically check your progress based on your real-life needs rather than some artificial index of stocks or bonds. It also helps keep your emotions in check since a good absolute return strategy will incorporate risk management techniques to keep your emotions at bay.

Obama’s Nuke Reduction Offer is Very Bad For America

Speaking in Berlin on June 19, President Obama publicly offered to reduce our long-range nuclear weapons by one-third if Russia would do the same. Initially Russian President Putin rejected the idea, but later he made a counter offer. Both sides would reduce long-range nukes by one-third, but in addition the US would remove all 180 tactical missiles that are placed in Europe. That would leave Europe defenseless.

The question is, would Obama agree to such an offer? I would think not,

but Obama desperately wants another nuclear reduction on his legacy.

Wishing you a great summer,

Gary D. Halbert

© Halbert Wealth Management