Before analyzing a company for investment, it’s important to have a perspective on how well the business has performed. Because at the end of the day, if you are an investor, you are buying the business. The FAST Graphs™ presented with this article will focus first on the business behind the stock. The orange line on the graph plots earnings per share since 1999. A quick glance vividly reveals the historical operating record of the company.

Qualcomm Incorporated (QCOM) is the world leader in 3G, 4G and next-generation wireless technologies.

This article will reveal the business prospects of Qualcomm Inc through the lens of FAST Graphs – fundamentals analyzer software tool. Therefore, it is offered as the first step before a more comprehensive research effort. Our objective is to provide companies that have excellent historical records and appear reasonably priced based on past, present and future data and expectations.

A quick glance at the graph itself and the orange earnings justified valuation line will tell the readers volumes about how well the company has historically been managed and performed as an operating business. Simply put, the reader should ask whether this example is worthy of a greater investment of their time and effort based on the data as presented and organized. The FAST Graphs’ unique advantage is the graphical articulation of the price value proposition.

Earnings Determine Market Price: The following earnings and price correlated F.A.S.T. Graphs™ clearly illustrates the importance of earnings. The Earnings Growth Rate Line or True Worth™ Line (orange line with white triangles) is correlated with the historical stock price line. On graph after graph the lines will move in tandem. If the stock price strays away from the earnings line (over or under), inevitably it will come back to earnings.

Earnings & Price Correlated Fundamentals-at-a-Glance

A quick glance at the historical earnings and price correlated FAST Graphs™ on Qualcomm Inc shows a picture of undervaluation based upon the historical earnings growth rate of 27.6% and a current P/E of 15.6. Analysts are forecasting the earnings growth to continue at about 15%, and when you look at the forecasting graph below, the stock appears slightly overvalued (it’s inside of the value corridor of the five orange lines - based on future growth).

Qualcomm Inc: Historical Earnings, Price, Dividends and Normal P/E Since 1999

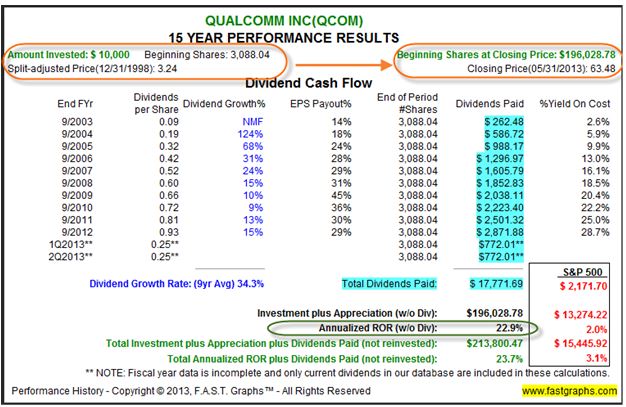

Performance Table Qualcomm Inc

The associated performance results with the earnings and price correlated graph, validates the principles regarding the two components of total return: capital appreciation and dividend income. Dividends are included in the total return calculation and are assumed paid, but not reinvested.

When presented separately like this, the additional rate of return a dividend paying stock produces for shareholders becomes undeniably evident. In addition to the 22.9% Annualized ROR (w/o Div) (green circle), long-term shareholders of Qualcomm Inc, assuming an initial investment of $10,000, would have received an additional $17,771.69 in total dividends paid (blue highlighting) that increased their Annualized ROR (w/o Div) from 22.9% to a Total Annualized ROR plus Dividends Paid of 23.7% versus 3.1% in the S&P 500.

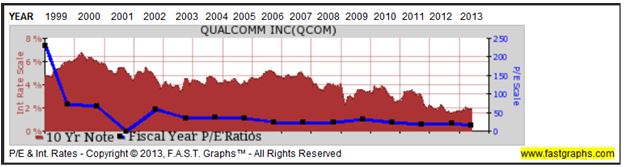

The following graph plots the historical P/E ratio (the dark blue line) in conjunction with 10-year Treasury note interest. Notice that the current price earnings ratio on this quality company is as low as it has been since 1999.

A further indication of valuation can be seen by examining a company’s current P/S ratio relative to its historical P/S ratio. The current P/S ratio for Qualcomm Inc is 5.06 which is historically low.

Looking to the Future

Extensive research has provided a preponderance of conclusive evidence that future long-term returns are a function of two critical determinants:

1. The rate of change (growth rate) of the company’s earnings

2. The price or valuation you pay to buy those earnings

Forecasting future earnings growth, bought at sound valuations, is the key to safe, sound and profitable performance.

The Estimated Earnings and Return Calculator Tool is a simple yet powerful resource that empowers the user to calculate and run various investing scenarios that generate precise rate of return potentialities. Thinking the investment through to its logical conclusion is an important component towards making sound and prudent commonsense investing decisions.

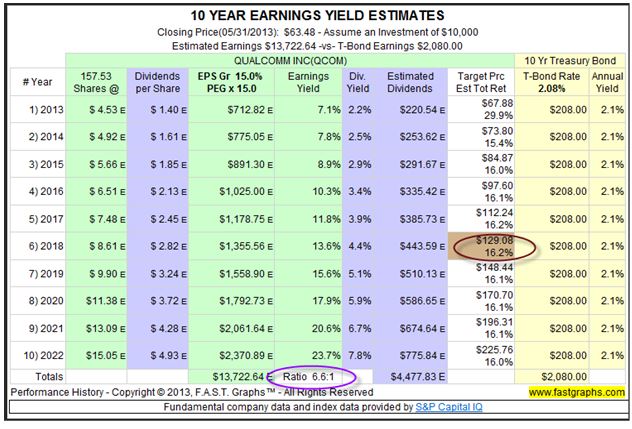

The consensus of 45 leading analysts reporting to Standard & Poor’s Capital IQ forecast Qualcomm Inc’s long-term earnings growth at 15%. Qualcomm Inc has no long-term debt of capital. Qualcomm Inc is currently trading at a P/E of 15.6, which is inside the value corridor (defined by the five orange lines) of a maximum P/E of 18. If the earnings materialize as forecast, based upon forecasted earnings growth of 15%, Qualcomm Inc’s share price would $129.08 at the end of 2018 (brown circle on EYE Chart), which would represent a 16.2% annual rate of total return which includes dividends paid (yellow highlighting).

Earnings Yield Estimates

Discounted Future Cash Flows: All companies derive their value from the future cash flows (earnings) they are capable of generating for their stakeholders over time. Therefore, because Earnings Determine Market Price in the long run, we expect the future earnings of a company to justify the price we pay.

Since all investments potentially compete with all other investments, it is useful to compare investing in any prospective company to that of a comparable investment in low risk Treasury bonds. Comparing an investment in Qualcomm Inc to an equal investment in 10-year Treasury bonds illustrates that Qualcomm Inc’s expected earnings would be 6.6 (purple circle) times that of the 10-year T-bond interest (see EYE chart below). This is the essence of the importance of proper valuation as a critical investing component.

Summary & Conclusions

This report presented essential “fundamentals at a glance” illustrating the past and present valuation based on earnings achievements as reported. Future forecasts for earnings growth are based on the consensus of leading analysts. Although with just a quick glance you can know a lot about the company, it’s imperative that the reader conducts their own due diligence in order to validate whether the consensus estimates seem reasonable or not.

Disclosure: Long QCOM at the time of writing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation. A comprehensive due diligence effort is recommended.

© F.A.S.T. Graphs