Has the Fat Lady Started to Sing on the Housing Market?

As decision makers we are continually looking for clues from economic activity in order to adjust portfolios. The beauty of following business cycle sequences is the value from anticipating financial market leadership changes. A major beneficiary of this four year old business recovery has been housing and housing related stocks.

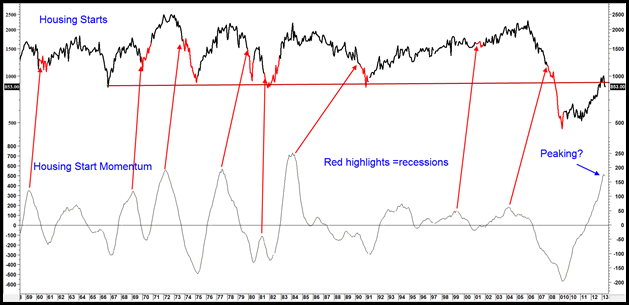

In recent days we have seen euphoria reign in the housing sector as sales and prices have both experienced new cyclical highs. I am not sure why, because prices, as monitored by the Case Shiller Composite 20 Index, are still down in excess of 25% from their 2006 peak. Moreover, the number of starts (see Chart 4) has “rebounded” sharply in the last few years but are currently at similar levels of previous cyclical lows set in 1966,1975,1980,1981 and 1991. Moreover the March 2013 recovery high of 1 million starts was less than half of the January 2006 peak at just under 2.3 million. House prices tend to be a lagging indicator and may continue to rise for a while, but there are good reasons for suspecting that starts and housing oriented equities may be in the process of peaking following several years of gains.

Housing Starts versus Interest Rates

Housing is arguably the most interest sensitive economic sector since the vast majority of houses are financed. Over the course of a number of years it is the major cost of owning a home for most people, so changes in the level of interest rates has a primary influence on the housing industry.

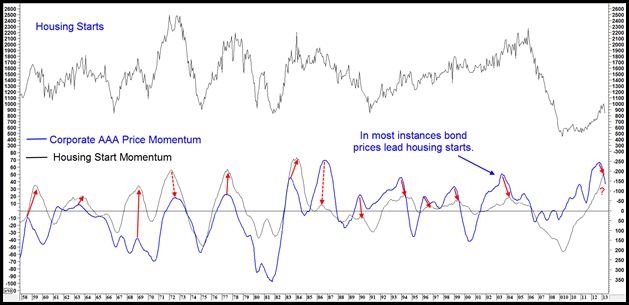

Chart 1 Housing Starts versus Bond Market Momentum

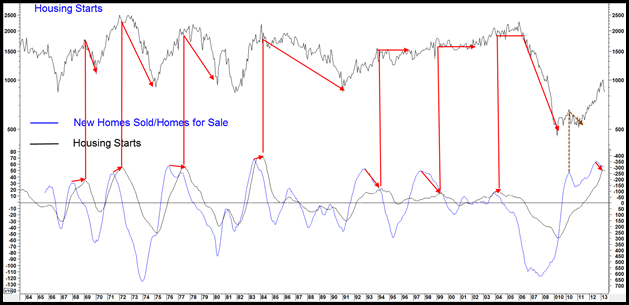

Chart 1 features housing starts in the top panel and their momentum in the bottom one. The blue line in the lower window is a momentum series for corporate bond prices. We could have substituted mortgage rates but the relationship between housing starts and Moody’s corporate AAA bond prices appears to be closer. In addition price history for corporate bonds is more extensive. The forward sloping solid arrows show that for the most part bond price momentum leads that for housing starts at cyclical peaks. The same is true for troughs but to simplify the chart those arrows have been omitted. The two dashed arrows indicate when starts led bond prices. The problem from a forecasting point of view is that the lead time and magnitude of the housing decline varies from cycle to cycle. The range has been from -4 months in 1986 to +8 months in 2004 for an average of just under +4 months. The latest interest rate momentum peak developed last October. That offers a tentative 5-month lead time if the recent March crest in the housing start momentum does turn out to be the peak. We also have to bear in mind that peaks in housing start momentum occasionally lead the actual numbers as the 1990-2004 period testifies. In the vast majority of situations though, this relationship is very close. It is also worth noting that even during the secular uptrend that developed between 1990 and 2004 peaks in housing start momentum nevertheless signaled the start of a 1-2-year sideways trend in starts. This fact can be appreciated from the horizontal red arrows flagging the peak in housing start momentum during this period (Chart 2).

Chart 2 Housing Starts versus a Sales/Inventory Ratio of New Housing

The New Homes for Sale/New Homes Sold Ratio

Another leading indicator that has proved useful over the years is the momentum of the ratio between new homes sold and new homes for sale. It is compared to housing start momentum in the lower window of Chart 2. This sales/inventory relationship has a consistent lead over the actual start momentum. Even the mini pause that took place in 2010-2011 (flagged by the brown dashed arrow) was picked up by this series. The new homes sold/for sale ratio looks as though it topped out last September, which supports the view that housing starts may also be in the process of topping.

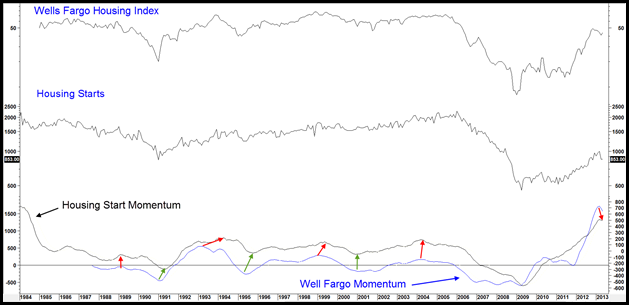

The Wells Fargo Housing Market Index (HMI)

Finally, each month Wells Fargo publishes an index of realtor sentiment. Historical data is fairly limited, only going back to the 1990’s. However, there does appear to be a good correlation between this series and housing starts themselves. This relationship is shown in Chart 3. Its momentum appears to lead, or at the very worst coincide with housing start momentum. The latest data suggests that this momentum series has topped out again. Each previous peak in the HMI momentum has been associated with a top in the housing start momentum and there is no reason to expect the current situation from being anything different.

Chart 3 Housing Starts versus the Wells Fargo Housing Market Index

If housing starts are in the process of peaking does that mean the recovery is over? Not really because housing is a very long leading indicator. In this respect the red highlights in Chart 4 indicate recessions. The arrows point up the lead time between the peak in housing start momentum and the onset of a recession. They vary of course, but the average is around two years. The range extends from 3-months in the true double dip recession of the early 1980’s to 75-months in 1989. It makes little sense to project the lead time of the current probable peak in housing starts to the onset of the next recession because of these inconsistent and wide ranging of historical variations.

Chart 4 Housing Starts and Housing Start Momentum

However, we can say two things. First, if our suspicion of a cyclical high in housing starts is valid it’s an initial signal that the business cycle has started to turn over. Think of an alarm clock set at 7:00 am to prepare us for a 10:00 am appointment. Second, since the current recovery has been sub-par, the lead time is more likely to be on the shorter side.

Our assumption is that the business cycle is nothing more than a set series of chronological sequences or events. In other words, from a forecasting point of view we need to focus on the trend of industrial commodity prices because they should be rising at this stage in the proceedings. If commodities firm up to any great degree from here, so will interest rates, the total effect being to suck out purchasing power and reversing the growth path to one of contraction. Alternatively, if commodity prices remain flat to down that will lessen or even reverse the current upward trajectory of bond yields and delay the next recession.

In any event if you hold homebuilder or other housing related equities it might be a good time to lighten up or place those stops a little closer. Evidence is building for a shift in leadership from interest sensitive sectors toward typical late cycle beneficiaries such as materials, energy, and industrial companies. Be on alert, for housing, the fat lady is on stage and could start to sing at any time.

© Pring Turner Capital Group