IN THIS ISSUE:

1. WSJ: “Markets and Memory Banks”

2. Bonds – A “Fire Sale” Sooner Or Later

3. You Need to Protect Yourself From the Bond Bear

Overview

The Halberts are out of town celebrating our son’s graduation from college on the sunny beaches of southern Florida. In place of my usual writing, I have chosen to reprint an excellent article from The Wall Street Journal’s Jason Zweig on investor behavior.

The WSJ writer keys in on a new investor survey from BlackRock, one of the largest money management firms in the world (almost $4 trillion in customer assets). BlackRock surveyed investors that have at least $50,000 in investable assets. The findings are almost sure to surprise you.

In short, investors are shunning stocks and clinging to bonds, even though a large majority worry about rising interest rates. In fact, inflows to taxable bond funds and ETFs continue to be strong even though interest rates remain at or near historical lows. We’ve seen this movie before and it doesn’t end pretty!

Everyone who invests should read this article. I have interspersed some comments of my own within the article.

QUOTE:

Markets and Memory Banks

By Jason Zweig

For years on end, pundits have been predicting the collapse of the bond market, and recently such calls havereached a crescendo– with bond kingBill Grossof Pimco being the latest to sound the death knell.

But investors show almost no inclination to avoid the impending doom: A new survey of investors by BlackRock, Inc. found that 57% are “worried about rising interest rates” and 53% think bonds are riskier today than a decade ago. Yet fewer than 7% said that “identifying the bond investments that are right for you” would be a major focus for them over the coming year – and 60% said they wouldn’t focus on it at all.

[GDH : This confirms what I’ve been saying since late last summer – that investors continue to herd into bonds and bond funds as if long-term interest rates are going to zero or below. As noted above, 60% of bond investors don’t think much at all about their bond investments, even though almost that many say they are worried about rising interest rates. What gives?

You might want to look at theBlackRock surveyreferenced above. There are a lot more interesting stats on investor thinking and behavior than noted above.]

Meanwhile, even as the stock market has shot almost straight up for the past four years, investors appear to be turning their backs on equities. The proportion of Americans who will admit to owning stocks has sunk to 52%, down from 65% in 2007, according toa new Gallup survey.

[GDH : Obviously, the financial crisis and the severe bear market of late 2007-early 2009 drove millions of Americans out of stocks, and many have never returned. Sadly, many missed the most powerful bull market ever.]

In short, investors are the prisoners of their past.

As the late investment strategist Peter Bernstein liked to say,markets have memory banks. What investors expect is shaped by what they experience.

Bernstein was fond of pointing out that in 1958, when the yield on stocks fell below bond yields for the first time, Wall Street’s wise men predicted that it couldn’t possibly last. There was nothing else in their memory banks to draw on. For decades – centuries, in fact – stocks had always yielded more than bonds. So the reversal had to be temporary, they argued. But it wasn’t: Bonds went on to out-yield stocksfor another half-century, to Bernstein’s bemusement.

By the same token, many investors – individuals and professionals alike – in the late 1990s had never experienced a protracted bear market in stocks. It was easy for them to imagine the future as an endless stream of double-digit gains. Never having seen even conservative stocks lose much money,they were eager [to] buy Internet stocks at any price.

Today, however, so many have been burned by bad markets that nearly 40% of U.S. investorsbelieve they don’t need to own stocksto meet their long-term investing goals, according to another recent survey, from Franklin Templeton; 57% of younger investors felt that way.

[GDH : This is simply stunning! It is a testament to a generation of investors who were repeatedly told by Wall Street that “buy-and-hold” was the Holy Grail. As I wrote in myMay 14 E-Letter, most investors simply do not have the willpower to ride out bear-market losses of 40% or 50%. It is really sad to see that 57% of younger investors have apparently decided never to invest in stocks. Where else will they go? Bonds? Good luck with buy-and-hold bonds!]

And for all the chatter about the recovery in the housing market, Americans aren’t exactly finding it hard to curb their enthusiasm about real estate. Earlier this month,a survey of 1,000 people byFannie Maefound that 51% - that’s right, half of them! – think that home prices will go up in the next 12 months.

Today’s bond investors have lived through more than three decades in which bonds almost never went down. So, even though everyone talks about the coming bear market in bonds, most people can’t imagine how painful it could be, warns David Allison, a partner at Allison Investment Management in Wrightsville Beach, N.C.

That’s true not just for individual investors but for professionals as well: The average age of a portfolio manager, according to the CFA Institute, is 43 – meaning that the last bear market in bonds ended when the typical portfolio manager was around 10 years old.

For today’s stock investors, the reverse is true. The past 13 years have been gut-wrenching, with the Standard & Poor’s 500-stock index collapsing 38% between 2000 and 2002, then roaring up until 2007, then losing half its value between 2007 and 2009, then bouncing back again. No wondernearly a third of investorsthink the stock market went down last year, even though the S&P 500 gained 16% in 2012.

[GDH : You might want to click on the link just above and look at what investor perceptions of stock market performance have been the last few years. When you open the link, be sure to click on the “Click to View” button to take you to the second, and most revealing chart. It shows you the percentages of investors who believe the stock market hasgone down in each of the last four years. This is unbelievable!]

This phenomenon isn’t unique to our time; investors have always been captive to their memory banks.

Many of us know “depression babies” – perhaps our parents or grandparents – who grew up during the Great Depression and whose behavior has been shaped by that experience for the rest of their lives. They don’t just tend to pinch pennies tighter than younger people do. Depression babies also are less willing to take financial risks in general, invest less of their money in stocks and have lower expectations of future stock returns than younger people do.

In its1948 Survey of Consumer Finances, the Federal Reserve asked approximately 3,500 Americans this question:

“Suppose a man decides not to spend his money. He can either put it in a bank or in bonds or he can invest it. What do you think would be the wisest thing for him to do with the money nowadays – put it in the bank, buy savings bonds with it, invest it in real estate, or buy common stock with it? Why do you make that choice?”

Mind you, this was nearly two decades after the Crash of 1929 and the onset of the Great Depression. Still, the wounds were salty and raw. Fully 34% of Americans said they wouldn’t put money into real estate because prices were “too high” and “capital loss [was] expected”; another 12% called buying a home “not safe, a gamble.” Only 9% were in favor of investing in real estate at all – but that towered over the paltry 5% who were willing to invest their savings in the stock market.

Note, too, that this kind of broad public loathing for an asset class is just what it takes to generate a high future return. Over the next decade, home prices went up by a cumulative total of roughly 12% after inflation, according to data from Yale University economist Robert Shiller; stocks gained an annual average of 14% after inflation.

Joachim Klement, chief investment officer at Wellershoff & Partners in Zurich, has argued that your attitude toward financial risk is shaped largely by the market returns you experience between the ages of 18 and 25, which he calls “the formative years” for investors.

[GDH : I question the conclusion drawn above by Mr. Klement because numerous studies show that most people ages 18-25 do not do much investing. They don’t make that much money in those early years and are busy accumulating household items, new cars, paying off college loans and building a family.]

The younger you are, the fewer experiences you have had time to deposit in your memory bank. So you will pay more attention to whatever has happened lately and, naturally, expect the future to resemble the recent past – the only history you have lived through.Research by Stefan Nagel, an economist at Stanford University, suggests that someone who is 30 years old places nearly twice the subjective weight on recent data as does someone who is 50 – and nearly three times as much as someone who is 70.

Bond investors who are over the age of, say, 55 know firsthand that bonds don’t always generate positive returns. When the bond market does finally tank, these are the people who will be in a position to buy from panicking younger investors who have never experienced such pain.

Sooner or later, older investors may well get the chance to benefit from buying bonds at the fire sale of a lifetime.

END QUOTE

Bonds – A “Fire Sale” Sooner Or Later

I obviously agree with the conclusions drawn by the WSJ writer above. Interest rates will go back to normal sooner or later, and that will mean a bear market for bonds. In August of last year, I wrote a Special Report entitled:How to Avoid theBURSTING of the Bond Market Bubble. Other than updating the various statistics and performance numbers for the passage of time, everything I wrote in the Special Report, I would stand by today.

Admittedly, I was early in forecasting the bursting of the bond bubble – that’s not surprising. But the case is still solid, especially since the bubble has continued to inflate since then. However, most investors (as confirmed by the BlackRock survey) are not worried about their bond holdings. As noted above, most apparently believe that bond yields are going lower still.

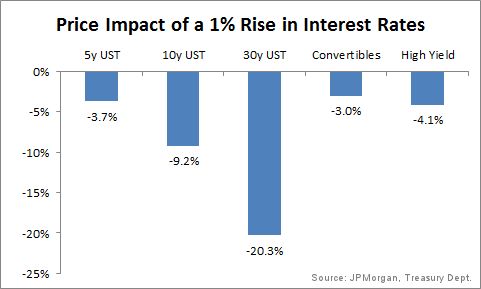

But give me your attention and let’s see what could happen to bond prices if there is merely a 1% rise in interest rates:

Take a moment to think about this chart and let it soak in, especially if you own long-term Treasury bonds! A mere 1% rise in long-term interest rates can result in a 20+% drop in 30-year Treasury bonds and a similar loss for Treasury bond mutual funds and ETFs.

If you are overweight in long bonds, as so many investors are today, I highly recommend that you consider ourLegacy Long/Short Multi-Index Portfolio, which is a team of three of our recommended professional money managers. This portfolio has the ability to “short ” long bonds should interest rates start to trend higher.

Click on the link above to see the performance of this portfolio. I trust you will be impressed! (As always, past performance is no guarantee of future results.)

Wishing you protection against the coming bond bear,

Gary D. Halbert

Forecasts & Trends E-Letter is published by ProFutures, Inc. Gary D. Halbert is the president and CEO of ProFutures, Inc. and is the editor of this publication. Information contained herein is taken from sources believed to be reliable but cannot be guaranteed as to its accuracy. Opinions and recommendations herein generally reflect the judgement of Gary D. Halbert, Mike Posey (or another named author) and may change at any time without written notice. Market opinions contained herein are intended as general observations and are not intended as specific investment advice. Readers are urged to check with their investment counselors before making any investment decisions. This electronic newsletter does not constitute an offer of sale of any securities. Gary D. Halbert, ProFutures, Inc., and its affiliated companies, its officers, directors and/or employees may or may not have investments in markets or programs mentioned herein. Past results are not necessarily indicative of future results. Reprinting for family or friends is allowed with proper credit. However, republishing (written or electronically) in its entirety or through the use of extensive quotes is prohibited without prior written consent.

© Halbert Wealth Management