General Electric Looks Like It's Becoming The Shareholder-Friendly Company It Once Was

General Electric (GE) was once revered as one of the bluest of all blue-chip companies in the world. During its glory days, GE was respected as an industrial conglomerate that manufactured some of the world’s best jet engines, locomotives, appliances and even the highly regarded General Electric light bulb. However, as best I can determine, the roots of General Electric’s ultimate demise were established in 1930 when the company, responding to the great depression, formed GE Finance in order to help their customers finance GE appliances over time.

Over the many decades since, GE Finance rapidly grew into GE Capital, the company’s largest, and for many years, their most profitable division. Essentially, General Electric morphed from being one of America’s great industrial companies into one of America’s largest diversified financial services companies. However, in addition to helping large customers finance their jet engines, locomotives and other General Electric products, General Electric became a major player is almost every aspect of financial lending from car loans to mortgages.

As a result, GE Capital generated approximately half of all General Electric profits for many years. But for all the success that GE Capital provided, it was simultaneously General Electric’s Achilles’ heel. The financial crisis that culminated into the great recession of 2008 brought the mighty General Electric literally to its knees. General Electric’s reentry into the home lending market in 2004, home lending’s heyday, hurled General Electric headfirst into the subprime lending crisis. The results were disastrous for the company’s profitability. This articlesummarizes the success, trials and tribulations of GE Capital.

In recent times, General Electric has been working hard as it attempts to unravel GE Capital. Yesterday’spress releasefrom General Electric provides continuing evidence that the company has repented from its past financial sins, and is working hard to bring the company back to its preeminence as a great American industrial manufacture and service provider. But perhaps more importantly, it may also offer evidence that the company is becoming more shareholder-friendly regarding how it plans on returning capital to shareholders.

General Electric - A Textbook Lesson In Stock Investing

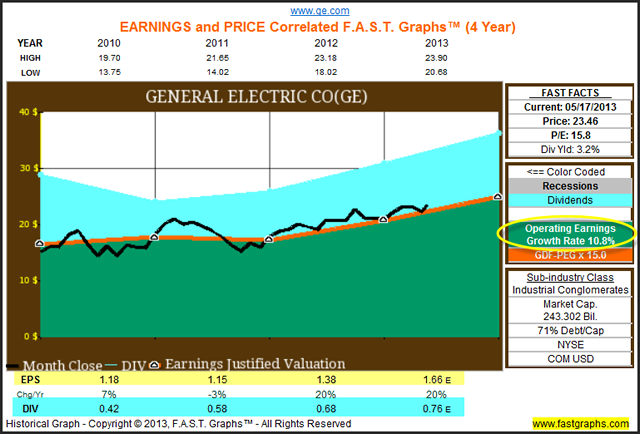

Personally, I believe that General Electric’s stock price trading history, relative to its operating earnings, over the last couple of decades should be a textbook case study in stock investing. Perhaps more than any other company that I have personally examined, General Electric’s historical stock price behavior provides many important investing lessons. The following 21-year (20 years of history and the current year we are in) earnings and price correlatedF.A.S.T. Graphs™on General Electric teaches several important lessons for investors.

For starters, we see a clear picture of the long-term importance of earnings as a driver of stock prices. But, although the long-term correlation between earnings (the orange line) and monthly closing stock prices (the black line) is undeniable, we also see a classic picture of market mispricing vividly exposed. Starting in late 1995, we see General Electric’s stock price disconnecting from its earnings justified valuation (the orange line) and becoming both dangerously and obviously overvalued.

As an interesting aside, this was occurring during the height of the Jack Welch era (Jack left in 2001). From calendar year 1995 to late 2000, it seemed as though neither General Electric nor Jack Welch could do anything wrong and GE’s stock price seemed to be in a never-ending upward trajectory. Certainly, fat profits from GE Capital were a contributing factor to the General Electric aura of those times. Then of course, two monumental occurrences happened almost simultaneously.

First, General Electric lost its iconic leader to retirement, and then came the 2001 recession. With General Electric’s stock priced to perfection, it had nowhere to go but down while new chairman Jeffrey Immelt could only helplessly watch it happen. It’s important to note that General Electric’s stock price was collapsing, even though the company continued to grow operating earnings at an above-average rate. Nevertheless, the headwinds of significant and dangerous overvaluation were simply too severe. I wrote extensively about this in July of 2011 in two articlesfound hereandpart 2 here.

However, once General Electric’s stock price returned to more fundamentally-justified levels, its stock price once again began advancing in conjunction with continued earnings growth that even began accelerating in 2004, coinciding with the company’s reemergence into the home lending mortgage market. And, as the graphic depicts, everything was fine and rosy until the subprime crisis led to the great recession of 2008. These two related catastrophic events turned GE Capital, General Electric’s now largest and most profitable division, into its worst nightmare. In 2008, thanks to the company’s exposure to the subprime market, earnings collapsed, and alas, stock price and dividends followed.

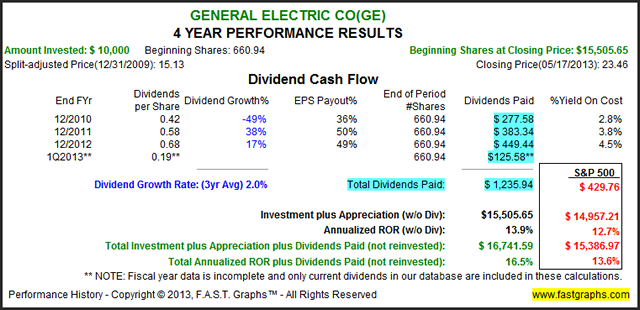

I find it very interesting to review General Electric’s track record over this storied two decade time period. In spite of all that happened, to include massive overvaluation, perhaps ill deserved profit growth, and two recessions, the once mighty General Electric fought the S&P 500 to a draw. Capital appreciation, (annualized rate of return) came in at about 1% less than the S&P 500; however, significantly greater dividend generation overcame the shortfall. Consequently, long-term shareholders in General Electric earned a total return with dividends paid, but not reinvested, that was just a few decimal points greater than the S&P 500.

Has a New and Improved General Electric Emerged?

Since the beginning of calendar year 2010, General Electric has been looking like the General Electric of old. Earnings growth has been steadily advancing, averaging 20% growth in fiscal 2012, and General Electric is expected to add another 20% growth for fiscal 2013. General Electric’s stock price has been tracking earnings growth and the company is once again firmly back on the steadily increasing dividend train. Moreover, as I will elaborate on later, General Electric is pledging a strong commitment to maintaining a generous dividend policy now and into the future.

Both General Electric the stock, and General Electric the company have been performing well since the beginning of calendar year 2010. Everything is growing steadily, the stock seems fairly valued, and the above-average and growing dividend yield is both enhancing returns and reducing risk.

A Thesis for Continued Growth

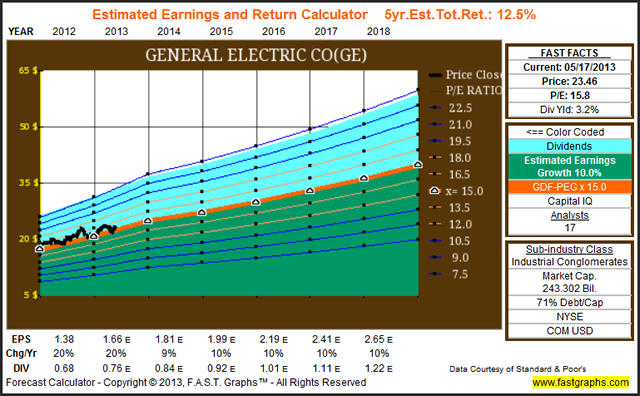

As a starting point, the consensus of 17 analysts reporting to Standard & Poor’s Capital IQ expect General Electric to grow earnings per share by 20% this fiscal year, followed by the 5-year 10% average growth rate going forward. These numbers appear reasonable and even conservative, for reasons I will elaborate on later. The following estimated earnings and return calculator indicates that General Electric is very attractively valued based on those estimates. Furthermore, the Value Line investment survey forecasts both earnings and dividends to grow at an average rate of 13% out to calendar year 2018.

In their April 24, 2012 earnings call transcript, Jeffrey R. Immelt – Chairman and Chief Executive Officer laid out the following summary of General Electric’s growth initiatives:

“Today with a $100 billion in revenue and 15% margins, we’re the largest and most profitable infrastructure company in the world, selling in more than a 160 countries. We put about 6% of our revenue back into R&D. We invest some $10 billion to launch products and build global capability and we’re big financial service players with an emphasis on specialty finance for small and medium sized business.”

He then went on to corroborate General Electric’s plan to revamp and hopefully reinvigorate GE Capital, their largest division:

“we want to continue to run off our non-core assets in GE Capital, make the non-core assets smaller and invest in our mid-market leasing and lending business, and the team exceeded all of there targets, and number five we want to have good year on balanced capital allocation, returning cash back to you, back to our shareholders, we had a good year with a mix about $5 billion of buyback, and $7 billion dividend, so $12 billion back to shareholders.”

Although as I previously mentioned, it was GE Capital that caused the company to falter during the subprime crisis, it was also GE Capital that was a major contributor to their profitability during their Golden years. I believe that management now understands both the relevance of GE Capital’s role in the company’s future as well as its appropriate areas of focus. Consequently, I believe the company’s current focus on middle market commercial and industrial loans and equipment leasing will better support GE’s other important divisions in the future, thereby once again becoming an important contributor to the company’s long-term profitability and growth. In the worst-case scenario, I believe that the future unraveling of non-core GE Capital assets will provide an important source of capital that the company can redeploy into shareholder-friendly actions such as bolt on acquisitions, share buybacks and perhaps most importantly, increasing its dividend.

According to Morningstar, General Electric is a diversified manufacturer organized into four major segments: technology infrastructure, energy infrastructure, home and business services, and of course capital services. Although this article has thus far primarily focused on the capital services segment, Morningstar believes that General Electric will emerge as a leader in the power infrastructure market which will be the backbone for the firm’s future growth.

Additionally, healthcare and aviation are both large and important core divisions for the company. For example, an article published in December of 2012 in VOX byMarco AnnunziataChief Economist and Executive Director of Global Market Insight, General Electric Co had the following to say about General Electric’s contribution to these important industries and vital segments of General Electric:

“ The next wave of innovation

This scepticism might be premature. In a recent report (Annunziata and Evans 2012), my co-author Peter Evans and I have looked at the productivity-enhancing potential of the ‘industrial internet’, a network that binds together intelligent machines, software analytics and people. The declining cost of instrumentation is beginning to enable a much wider use of sensors in machines ranging from jet engines to power generation turbines to medical devices. Software analytics can then leverage the enormous amount of data generated in order to optimise the performance of individual machines, fleets and networks. This means, for example, having a better insight in the performance of a jet engine and being able to anticipate mechanical failures so that maintenance can be performed in a pre-emptive way, minimising the delays that occur when the problem emerges shortly before take-off. It means being able to track the exact location of medical devices in a hospital and whether they are in use or idle, so that patient admissions and medical procedures can be scheduled more efficiently, yielding better health outcomes to more patients at lower cost.

The potential benefits are sizeable. Just a 1% gain in fuel efficiency over fifteen years would yield $30 billion in savings in aviation and $66 billion in the power generation industry, while a 1% efficiency gain would yield $63 billion in the healthcare industry and $27 billion in the rail industry. Our study focuses on the sectors where General Electric has a strong presence, because those are the sectors we know best and where we are seeing these gains materialise. But the industrial internet has the potential to impact a much wider range of industries, as well as services.”

The following slides from General Electric’s recent shareholder meeting highlight many of the growth initiatives and drivers that GE sees in their future. The first slide talks about what the company accomplished in 2012:

This next slide illustrates the company’s commitment to a more vigorous shareholder-friendly capital allocation that I spoke about earlier. Dividends are clearly their number one priority, followed by buybacks and strategic acquisitions. Consequently, General Electric is committed to rewarding shareholders with cash, while simultaneously capitalizing their future growth.

Additionally, General Electric is clearly committed to continuous investments in research and development into their industrial segments. Consequently, I have great confidence in their ability to maintain a competitive posture in their newly focused but legacy industrial segments. I believe that General Electric is positioning itself to be a leader in every market it competes in.

Because General Electric serves customers in over 160 countries throughout the world, soft economies in Europe and the United States are being overcome by strong growth in emerging markets throughout the world. In short, General Electric has numerous opportunities to fuel future growth throughout the world.

Summary and Conclusions

When Jeffery Immelt first took the reins of General Electric, I believe he was dealt a very difficult hand. Accordingly, General Electric the stock has not been a stellar performer under his leadership. When a common stock is a poor performer, it is not uncommon for investors to vilify the CEO. I discussed this in great detail in part two of my two-part series on General Electric (links provided above). Frankly, I believe it took many years to solve some of the enormous problems that General Electric faced when Jeffery Immelt took charge. Therefore, I feel that General Electric’s performance since calendar year 2010 more accurately reflects his leadership and skill as a CEO. At least I’m now willing to give him the benefit of the doubt.

Although General Electric Corp has certainly faced many trials and tribulations over the last 15 years, the company’s legacy for providing quality products to its customers goes back more than 100 years. Taken from the first page of the company’s history, the following establishes the company’s legacy starting in 1878:

“From the invention of the first practical incandescent light bulb to building America’s first Central Power Station, the GE tradition of life-changing innovations was underway. With power and light, GE provided the basis of modern life, quickly redefining everything from the length of the day to our knowledge of the human body through the development of the first X-ray machine.”

From these early beginnings, General Electric has evolved into one of the largest industrial and financial service companies in the entire world. Today the company engages in power generation, water processing, medical imaging, aircraft engines, household appliances and much much more. Perhaps the company lost its footing a little bit over the past couple of decades, but they appear to have learned their lessons well. The company seems to be back on track toward earning back the reputation they once had as one of the world’s bluest of all blue-chip companies. I feel that they’re up to the task, and that their current valuation and dividend yield provide retired investors seeking income a great opportunity. As Mahatma Gandhi so eloquently put it “The weak can never forgive. Forgiveness is the attribute of the strong.“ Perhaps in this case forgiveness might also be very profitable.

Disclosure: Long GE at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs