The Dow Hits All-Time Highs, But The Truth Is It Remains Cheaply Valued

The Dow Jones industrial average sits above 15,000, an all-time high. But don’t be fooled, this doesn’t mean that stocks are expensive. I understand that it seems logical to assume that if the Dow Jones industrial average, what many believe to be the bellwether index of the stock market, is at an all-time high, then it must simultaneously be overvalued. Herein is the danger of relying on headlines and simple statistics.

This article intends to demonstrate that more than one third of the 30 Dow stocks (11) are undervalued, another 6 are fairly valued, another 6 fully valued, but not overly so, and finally, only 7 that could rightfully be classified as overvalued. In other words, the Dow Jones industrial average is rather cheap, even though it sits near an all-time high.

But as I often like to say, “The Angels are in the details.” The beauty of an index with only 30 constituents is that the details are relatively easy to review. What follows is a breakdown of the 30 Dow Jones industrials in order of valuation, lowest to highest. The 30 constituents will be organized according to the four categories depicted above: first the 11 that are undervalued, followed by 6 that are in value, followed by 6 more that are fully valued but not overly so, and finally by 7 that appear overvalued.

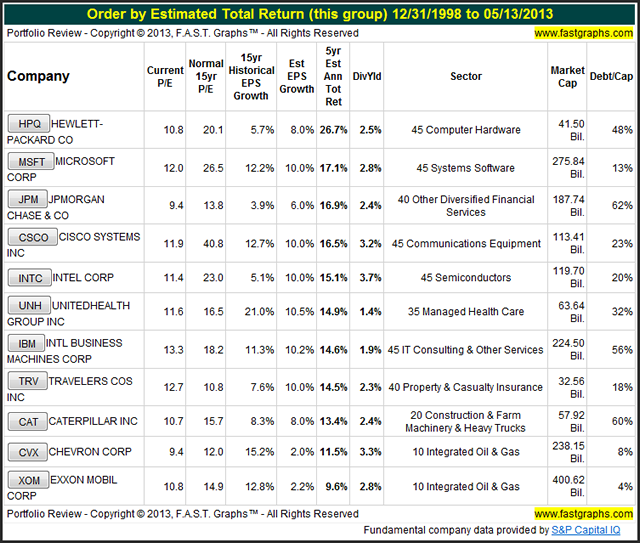

I will provide a “F.A.S.T. Graphs™portfolio review” for each category listing the current P/E ratio, the company’s historical normal PE, each company’s 15-year historical EPS growth rate, the consensus estimated 5-year growth rate, followed by the 5-year estimated annual total return based on those estimates, then the dividend yield, sector, market cap, and finally their debt/capital ratio.

Then I will provide a 15-year earnings and price correlatedF.A.S.T. Graphs™on each company. My objective is to provide the reader a greater insight into what the Dow Jones industrial average truly looks like relative to fair valuation over what they could obtain by simply reading provocative headlines.

In addition to a focus on the current valuation of this bellwether index, I hope that the reader walks away with a more comprehensive understanding of the nature of the 30 businesses that make up the Dow Jones industrial average. This large-cap index contains many types and categories of common stocks. It is comprised of growth stocks, dividend growth stocks, cyclical stocks, turnaround situations and everything in between.

Moreover, each constituent is a bellwether of its own respective industry in its own right. It all adds up to quite a feat for such a small number of companies. Nevertheless, this index has historically represented itself quite admirably as a proxy for the state of the market and the US economy at large. I am hopeful that the reader walks away with a much clearer perspective and opinion about the stock market, and stocks in general, as a result of reviewing the Dow Jones 30 industrial average, one company at a time.

Dow Jones Industrial Average Constituents Undervalued

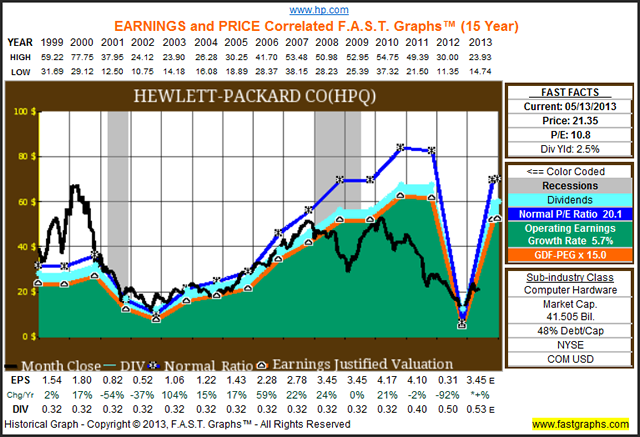

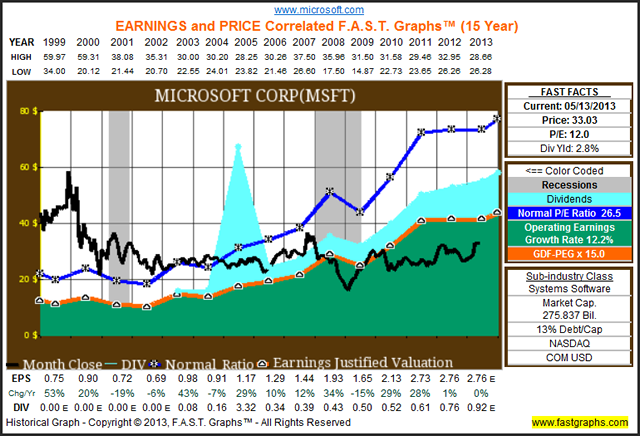

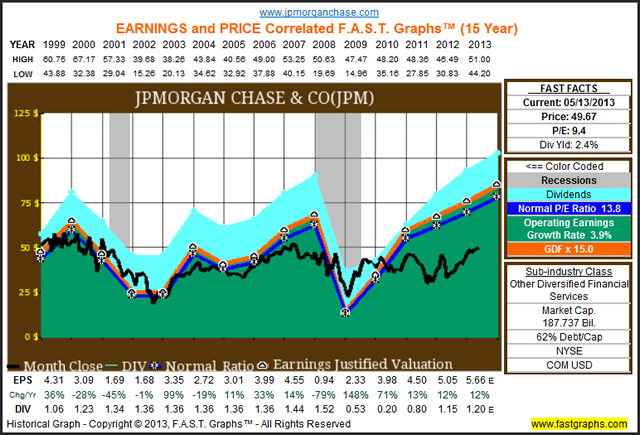

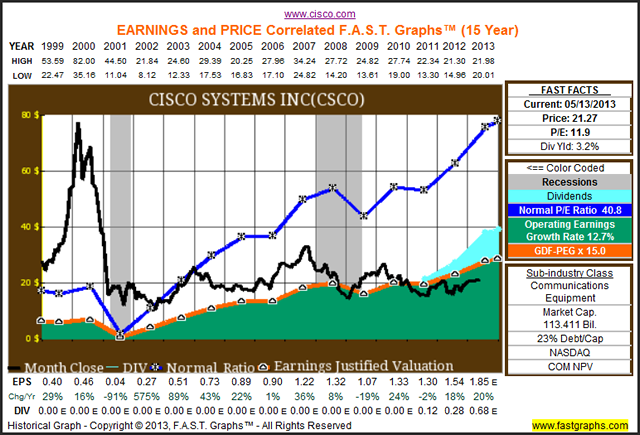

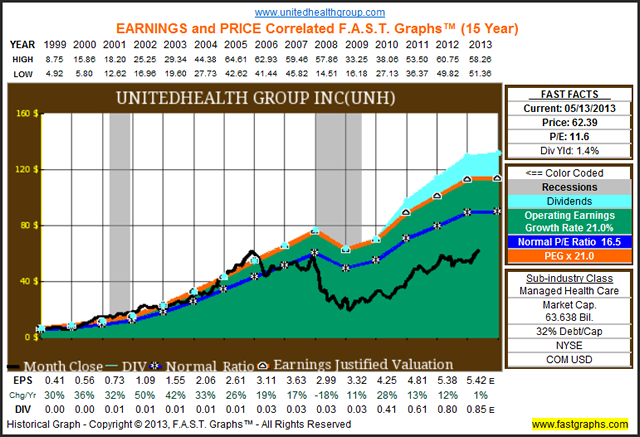

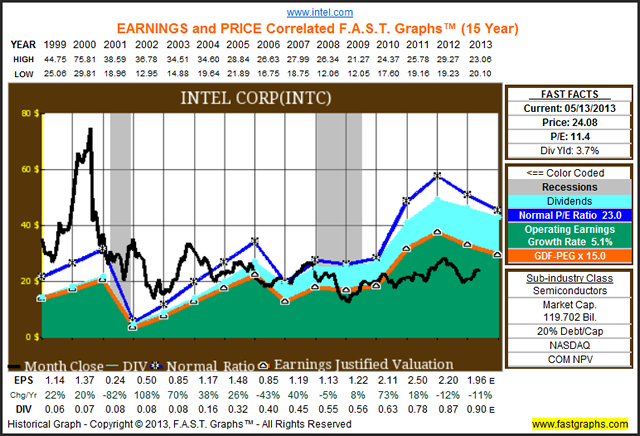

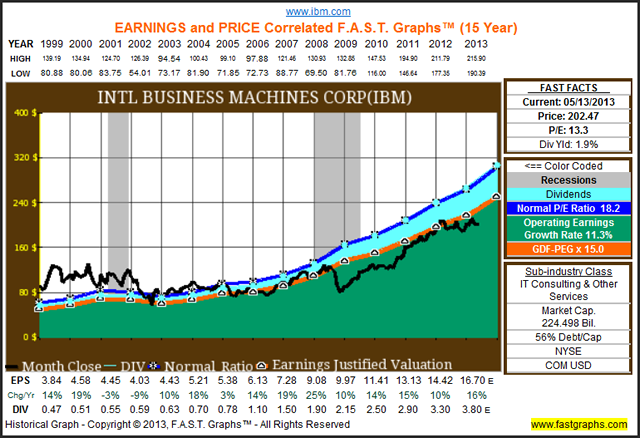

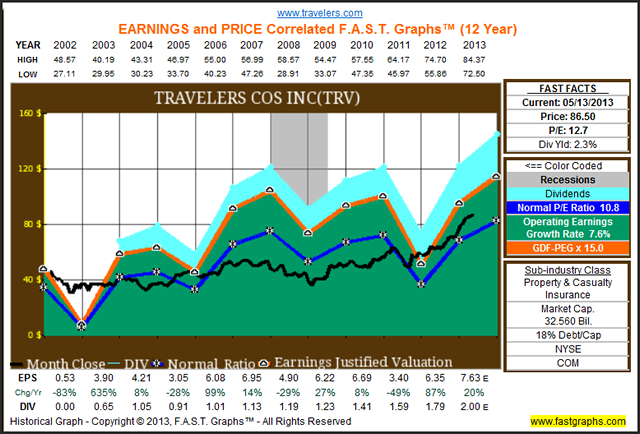

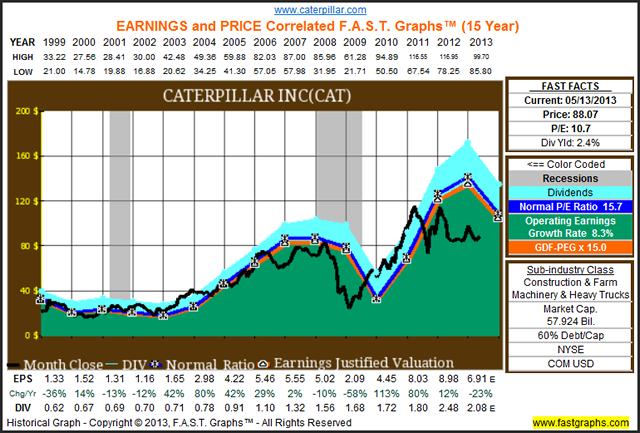

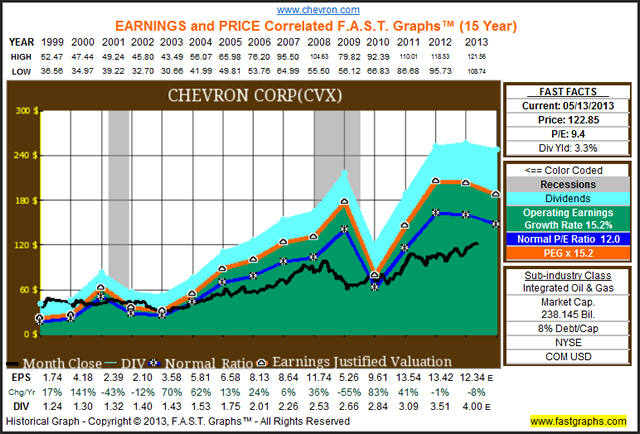

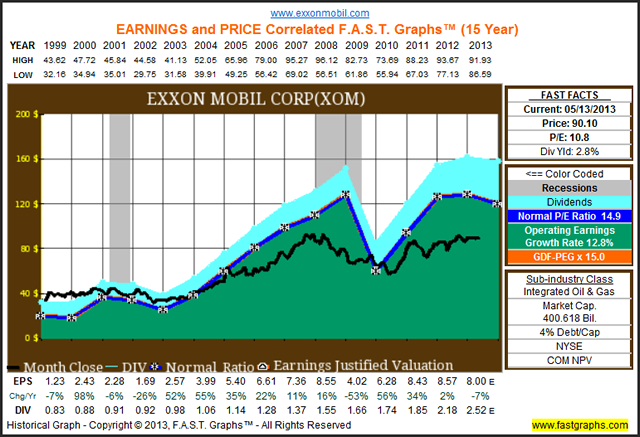

As I previously indicated, there are 11 of the 30 Dow Jones stocks that appear to be undervalued even after the recent market run-up. What comes next is first a portfolio review of these 11 companies, followed by an individual earnings and price correlated F.A.S.T. Graphs™ on each. The reader should note that each of these individual earnings and price correlated historical graphs contain a forecast for the current fiscal year’s earnings. This will be marked by a capital “E” for estimate next to the dollar amount of earnings forecast for the next fiscal year listed at the bottom of the graph.

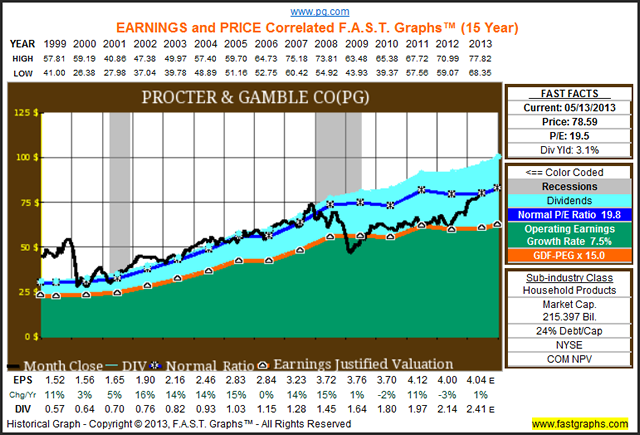

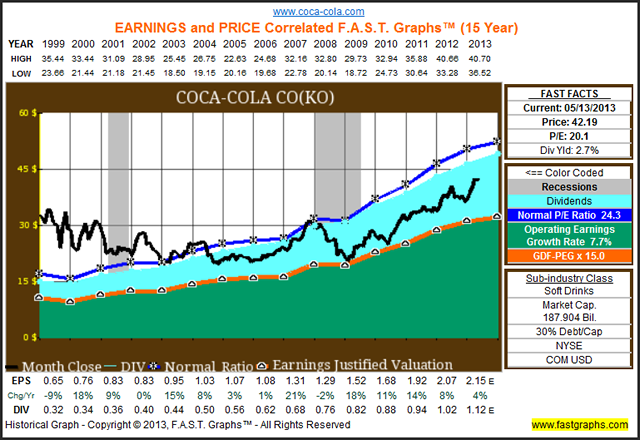

When reviewing the individual graphs, the orange line represents a metaphor of fair value based on widely-accepted formulas for valuing a business. Notice how the monthly closing stock price (the black line on the graph) tracks the orange earnings justified valuation line on each individual constituent’s graph. Even the most cyclical of the Dow stocks will show a high correlation between the company’s stock price and its earnings over time. Whether the earnings go up, down or sideways, stock price will follow. Moreover, when price and earnings become disconnected, notice how they inevitably move back into alignment with each other.

Hewlett-Packard Co (HPQ)

Microsoft Corp (MSFT)

JP Morgan Chase & Co (JPM)

Cisco Systems Inc (CSCO)

United Health Group Inc (UNH)

Intel Corp (INTC)

International Business Machines Corp (IBM)

Travelers (TRV)

Caterpillar Inc (CAT)

Chevron Corp (CVX)

Exxon Mobil (XOM)

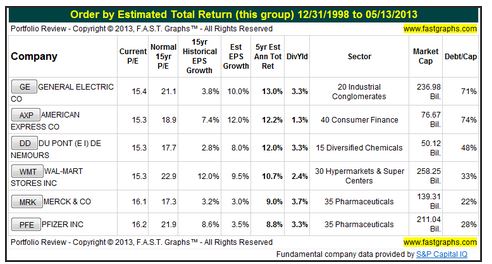

Dow Jones Industrial Average Constituents In-Value

This next set of six Dow constituents are all trading at theoretical fair value bringing the total to 17, or more than half of the 30 Dow Jones industrials that are either undervalued or fairly valued. The following portfolio review, and all subsequent portfolio reviews are presented with the same information as we saw with our 11 undervalued Dow constituents.

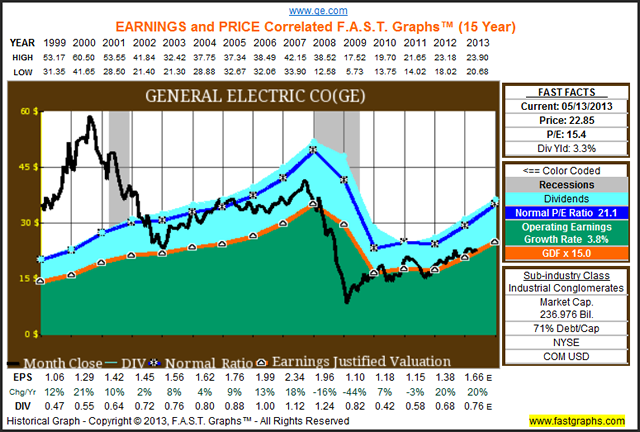

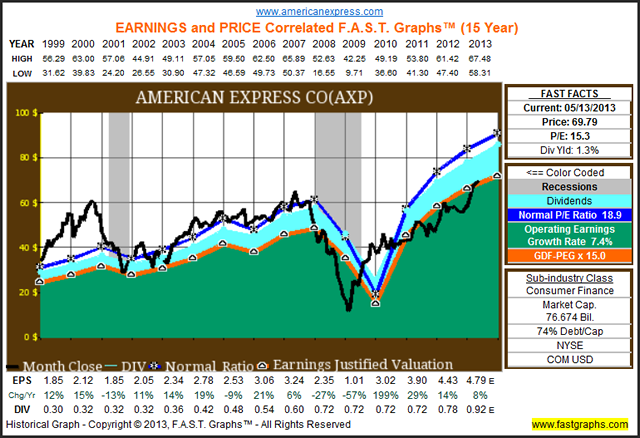

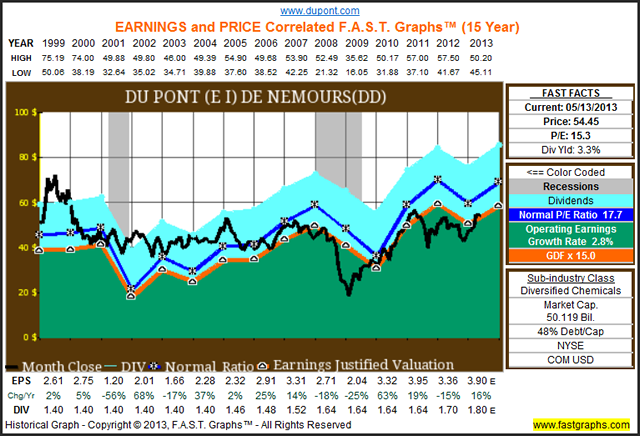

Once again, when reviewing the individual graphs, the orange line represents a metaphor of fair value based on widely-accepted formulas for valuing a business. Notice how the monthly closing stock price (the black line on the graph) tracks the orange earnings justified valuation line on each individual constituent’s graph. Even the most cyclical of the Dow stocks will show a high correlation between the company’s stock price and its earnings over time. Whether the earnings go up, down or sideways, stock price will follow. Moreover, when price and earnings become disconnected, notice how they inevitably move back into alignment with each other.

However, in contrast to what we saw with our first 11 undervalued examples where the black monthly closing price was below the orange earnings justified valuation line, with this set of 6 fairly valued companies we see the price approximately touching the orange line indicating fair value. On the other hand, the concept of fair value means different things for the individual companies in this subset.

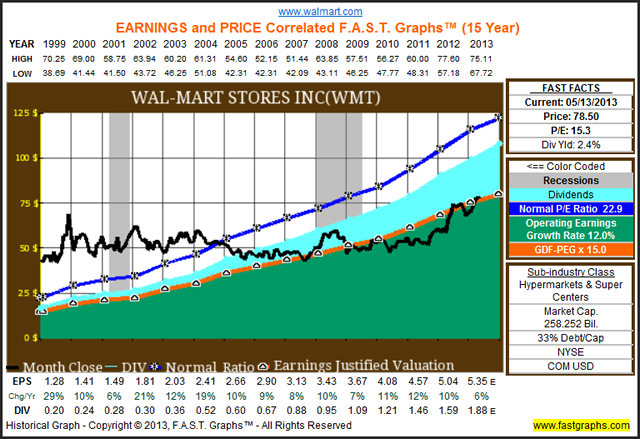

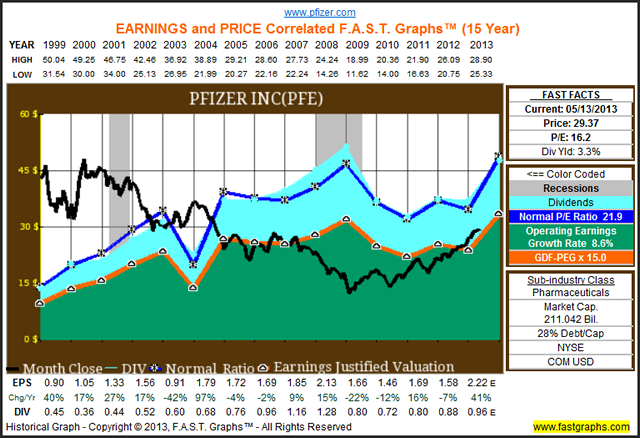

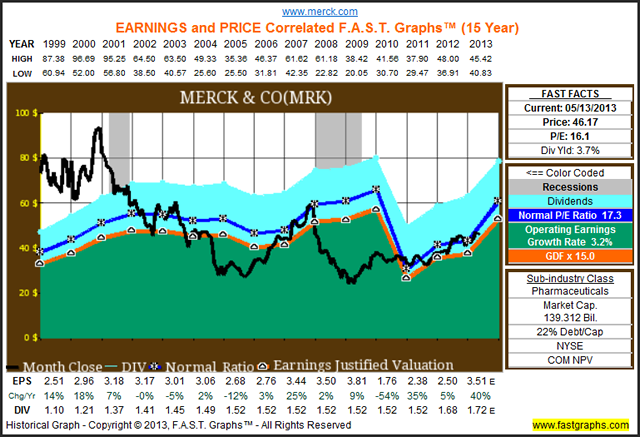

For example, today’s fair value for General Electric (GE) is based on a resetting of earnings growth created by the great recession caused by the financial crisis of which General Electric was a major player in. In the case of DuPont (DD), we see earnings growth that has been both highly cyclical, yet flat. American Express (AXP) shows a strong recovery in earnings while Walmart’s (WMT) stock price has been tracking earnings justified levels after experiencing a significantly long period of overvaluation. In the case of the two big pharma’s, Pfizer (PFE) and Merck (MRK), both appear fairly valued based on expected earnings acceleration for fiscal 2013.

General Electric Co

American Express Co

DuPont

Wal-Mart Stores Inc

Pfizer Inc

Merck & Co

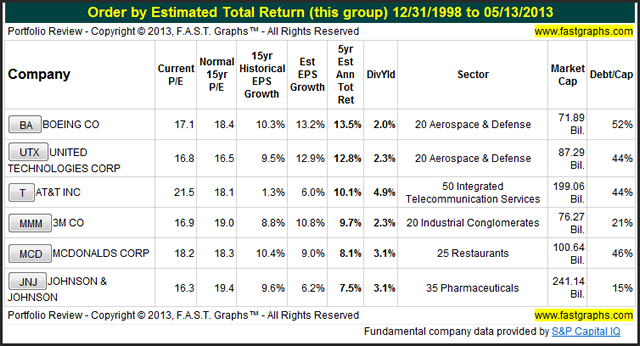

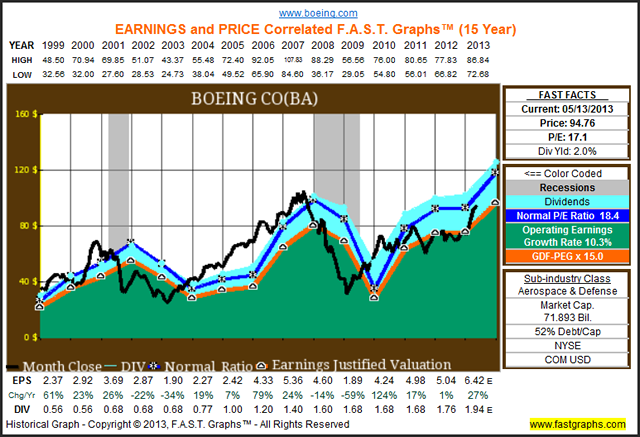

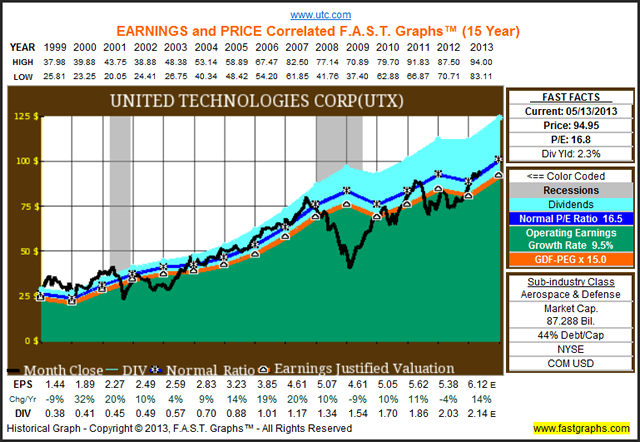

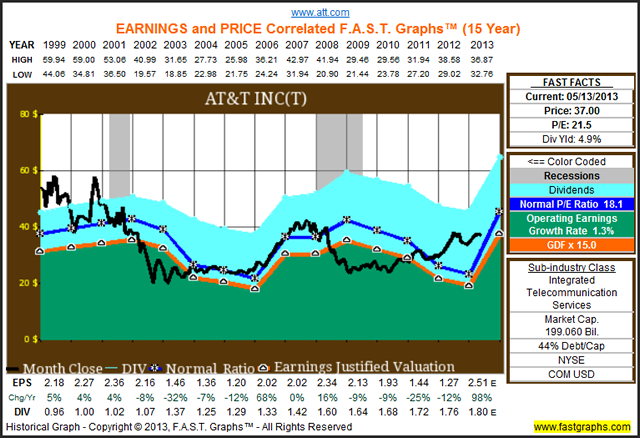

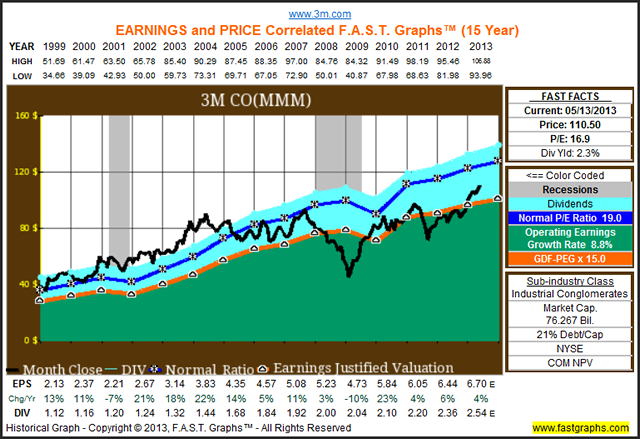

Dow Jones Industrial Average Constituents Fully Valued

There are an additional 6 of the 30 Dow Jones industrial average constituents that I would call fully valued, but not dangerously overvalued. In other words, although the stocks are not cheap, they are far removed from bubble territory.

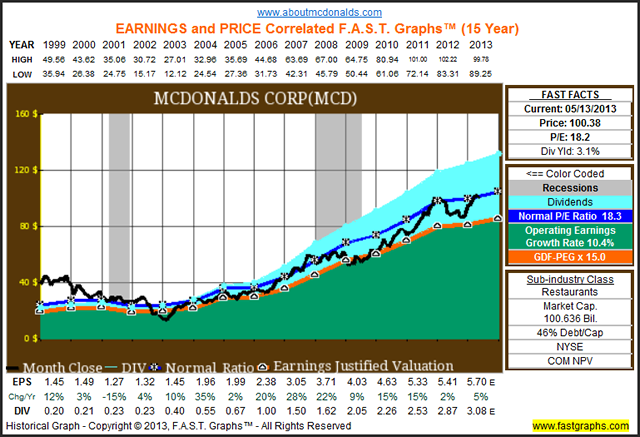

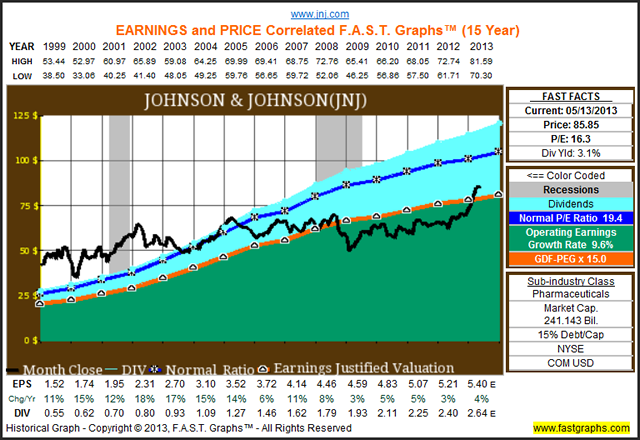

Once again, when reviewing the individual graphs, the orange line represents a metaphor of fair value based on widely-accepted formulas for valuing a business. Notice how the monthly closing stock price (the black line on the graph) tracks the orange earnings justified valuation line on each individual constituent’s graph. Even the most cyclical of the Dow stocks will show a high correlation between the company’s stock price and its earnings over time. Whether the earnings go up, down or sideways, stock price will follow. Moreover, when price and earnings become disconnected, notice how they inevitably move back into alignment with each other.

In these six moderately overvalued or fully valued examples the reader should notice that the black monthly closing stock price line is moderately above the orange earnings justified valuation line. However, only United Technologies Corp (UTX) and AT&T (T) are experiencing a stock price that is above their historical normal P/E ratio (the blue line on the graph). Consequently, I see this group of stocks as expensive, but not dangerously overvalued.

Boeing Co (BA)

United Technologies Corp (UTX)

AT&T Inc

3M Co (MMM)

McDonald’s Corp (MCD)

Johnson & Johnson (JNJ)

Dow Jones Industrial Average Constituents Overvalued

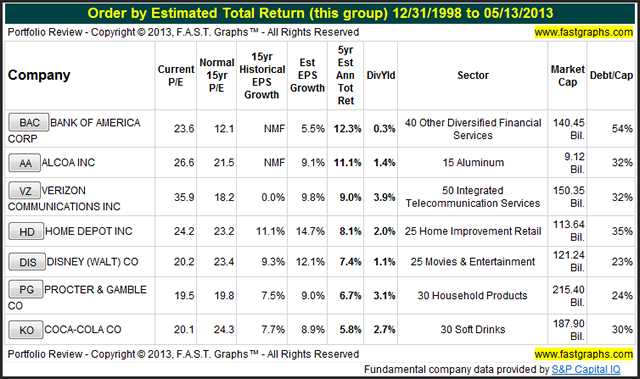

This final group of seven Dow Jones industrial average constituents I consider as being improperly valued by the marketplace. Consequently, the label “overvalued” does not precisely fit in all cases.

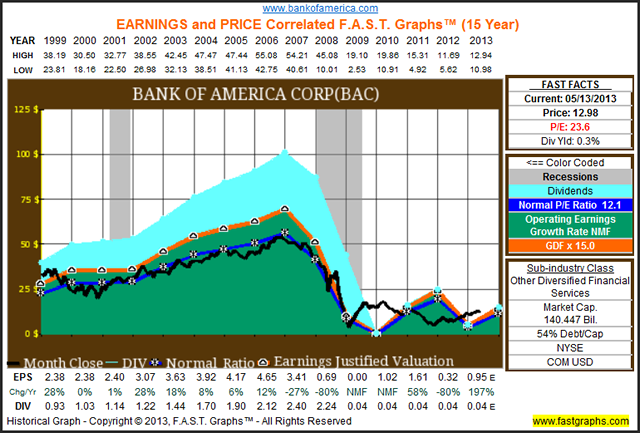

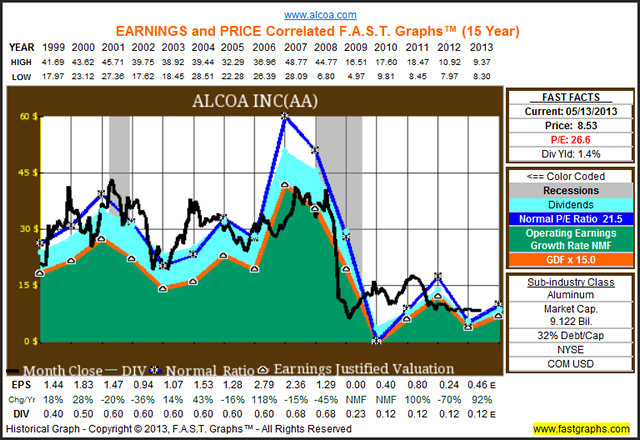

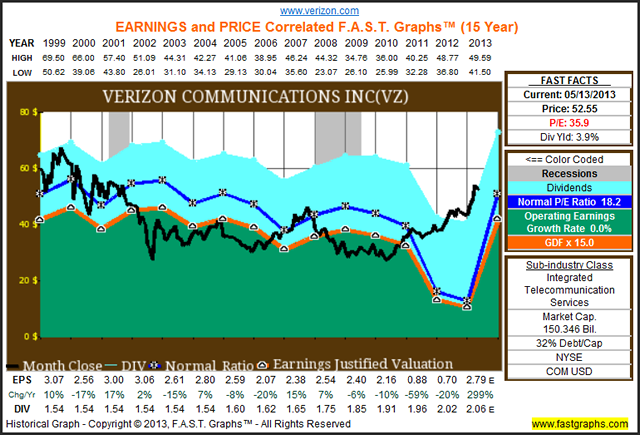

To clarify, as you review the individual graphs on each, notice that Bank of America (BAC), Alcoa Inc (AA) and Verizon Communications Inc (VZ) are all carrying high P/E ratios because of weak recent earnings. However, since each of these companies is expected to have a strong recovery of earnings in fiscal 2013, it could be argued that they are not overvalued at all. Therefore, these three names could theoretically be counted as reasonably priced Dow Jones industrial average constituents.

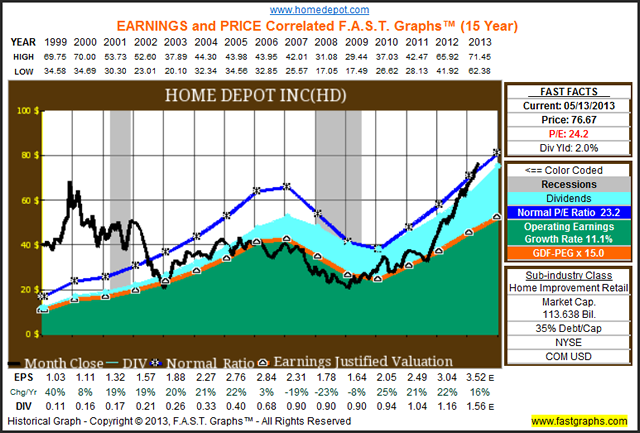

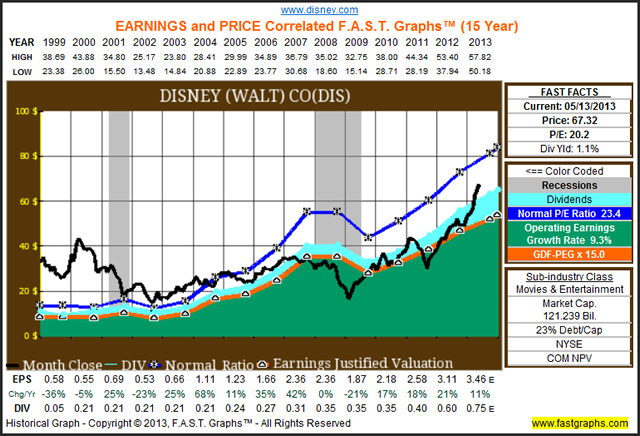

In contrast, I would argue that both Home Depot (HD) and Walt Disney (DIS) are overvalued under the strictest definitions of overvaluation. Therefore, I would suggest the risk of investing in them at current levels is high, especially over the short-to-intermediate run.

Finally, Procter & Gamble (PG) and Coca-Cola (KO) are two high-quality blue-chip dividend paying stalwarts with a legacy of being awarded a quality premium valuation by the market. Consequently, a case could be made that both of these stocks are reasonably valued today, at least on a historical basis, if not a pure earnings yield basis.

Bank of America Corp

Alcoa Inc

Verizon Communications Inc

Home Depot Inc

Disney (Walt) Co

Procter & Gamble Co

Coca-Cola Co

Summary and Conclusions

It is true that the Dow Jones industrial average is trading within an all-time high territory. However, I do not believe that it’s true that the Dow Jones industrial average is therefore overvalued. Instead, I believe a closer analysis indicates that the Dow Jones industrial average may have a lot more room to run. In truth, valuing a market, or for that matter an individual stock is not just about whether it’s trading at or near an all-time high.

By examining each of the individual Dow Jones industrial average constituents, it becomes clear that this is a multifaceted, and one could even say eclectic group, of companies. Some of the Dow stocks such as Boeing, Alcoa, Travelers and DuPont have long legacies of cyclicality. The communications constituents AT&T and Verizon have been in a continuous downtrend for many years. Big Pharma, Merck and Pfizer, have also been very weak over the past decade or so.

Home Depot and Walt Disney have shown a susceptibility to the great recession, but otherwise have good records of historical growth. Blue-chip stalwarts United Technologies, Procter & Gamble, Johnson & Johnson, McDonald’s Corp, Coca-Cola and 3M have been steady Eddie blue-chip dividend growth stocks. The companies with a financial legacy, General Electric, American Express, JP Morgan, and Bank of America, once all consistent above-average growth stocks saw their earnings and values decimated by the financial crisis-induced great recession.

For the most part the technology components, Cisco Systems Inc., Intel Corp and Microsoft, have suffered from significant overvaluation during the technology bubble which culminated in calendar year 2000, but have subsequently come back into fair value. Wal-Mart is a non-technology stalwart that has suffered from the same overvaluation issues during the irrational exuberance period. IBM has been a great growth story, and Hewlett-Packard is attempting to recover from a series of mishaps.

Energy constituents Chevron and Exxon have a long history of market undervaluation, as does the healthcare constituent United health Group. Finally, Caterpillar is a semi-cyclical that appears very undervalued currently.

The bottom line is that the Dow Jones industrial average is made up of 30 very diverse companies. The purpose of this article was to cast a light upon just how very different each of these companies were, and to illustrate that the Dow Jones industrial average is far from being in bubble territory. Personally, I believe there is a great deal more insight in reviewing these companies as individual entities than there is in thinking about them as the market in the general sense.

Disclosure: Long HD, PG, KO, HPQ, MSFT, CSCO, INTC, CAT, CVX, GE, PFE, BA, UTX and MCD at the time of writing.

Disclaimer:The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

© F.A.S.T. Graphs