IN THIS ISSUE:

1. Great Recession Followed by Grand Illusion

2. Stocks at Record Highs, But How About Consumers?

3. How Are Investors Doing in This Bull Market?

4. The Love Affair With Taxable Bonds Continues

Overview

We start today with an excellent editorial I read last week written by Mort Zuckerman, Editor-In-Chief of U.S. News & World Report.My goal every week is to do a lot of reading and summarize what I’ve learned in these pages week in and week out.

But every now and then I run across something so good that it just makes sense to reprint it in its entirety, even if it’s not my own work. Not many of my contemporaries are willing to do that, as they think it makes them look less scholarly. I don’t have that problem.

Following that, we’ll take a look at the stock markets now that the S&P 500 Index has finally reached a new record high. You would think that investors would be jubilant with stocks at new record highs, but consumer confidence is still in the tank. We’ll look at some of the reasons why.

Finally, we will revisit the public’s continued love affair with taxable bonds (including Treasury bonds). Despite the huge bull market in stocks, investors continue to pour money into bonds and bond mutual funds. I continue to maintain that long-only bonds are in for a bear market due to rising long-term interest rates.

QUOTE:

The Great Recession Has Been Followed by the Grand Illusion

by Mortimer Zuckerman

The Great Recession is an apt name for America's current stagnation, but the present phase might also be called the Grand Illusion—because the happy talk and statistics that go with it, especially regarding jobs, give a rosier picture than the facts justify.

The country isn't really advancing. By comparison with earlier recessions, it is going backward. Despite the most stimulative fiscal policy in American history and a trillion-dollar expansion to the money supply, the economy over the last three years has been declining. After 2.4% annual growth rates in gross domestic product in 2010 and 2011, the economy slowed to 1.5% growth in 2012. Cumulative growth for the past 12 quarters was just 6.3%, the slowest of all 11 recessions since World War II.

And last year's anemic growth looks likely to continue. Sequestration will take $600 billion of government expenditures out of the economy over the next 10 years, including $85 billion this year alone. The 2% increase in payroll taxes will hit about 160 million workers and drain $110 billion from their disposable incomes. The Obama health-care tax will be a drag of more than $30 billion. The recent 50-cent surge in gasoline prices represents another $65 billion drag on consumer cash flow.

February's headline unemployment rate was portrayed as 7.7%, down from 7.9% in January. The dip was accompanied by huzzahs in the news media claiming the improvement to be "outstanding" and "amazing." But if you account for the people who are excluded from that number—such as "discouraged workers" no longer looking for a job, involuntary part-time workers and others who are "marginally attached" to the labor force—then the real unemployment rate is somewhere between 14% and 15%.

Other numbers reported by the Bureau of Labor Statistics have deteriorated. The 236,000 net new jobs added to the economy in February is misleading—the gross number of new jobs included 340,000 in the part-time, low wage category. Many of the so-called net new jobs are second or third jobs going to people who are already working, rather than going to those who are unemployed.

The number of Americans unemployed for six months or longer went up by 89,000 in February to a total of 4.8 million. The average duration of unemployment rose to 36.9 weeks, up from 35.3 weeks in January. The labor-force participation rate, which measures the percentage of working-age people in the workforce, also dropped to 63.5%, the lowest in 30 years. The average workweek is a low 34.5 hours thanks to employers shortening workers' hours or asking employees to take unpaid leave.

Since World War II, it has typically taken 24 months to reach a new peak in employment after the onset of a recession. Yet the country is more than 60 months away from its previous high in 2007, and the economy is still down 3.2 million jobs from that year.

Just to absorb the workforce's new entrants, the U.S. economy needs to add 1.8 million to three million new jobs every year. At the current rate, it will be seven years before the jobs lost in the Great Recession are restored. Employers will need to make at least 300,000 hires every month to recover the ground that has been lost.

The job-training programs announced by the Obama administration in his State of the Union address are sensible, but they won't soon bridge the gap for workers with skills in science, technology, engineering and mathematics. Nor is there yet any reform of the patent system, which imposes long delays on innovators, inventors and entrepreneurs seeking approvals. It often takes two years to obtain the environmental health and safety permits to build a modern electronic plant, a lifetime in the tech world.

When employers can't expand or develop new lines because of the shortage of certain skills, the employment opportunities for the less skilled are also restricted. To help with this shortage, the administration's proposals for job-training programs do deserve support. The stress should be on vocational training, postsecondary education and every program that will broaden access to computer science and strengthen science, technology, engineering and math in high schools and at the university level.

But the payoffs from these programs are in the future, and it is vital today to increase the number of annual visas and grants of permanent residency status for foreigners skilled in science and technology. The current situation is preposterous: The brightest and best brains from all over the globe are attracted to American universities, but once they get their degrees America sends them packing. Keeping these foreigners out means they will compete against us in the industries that are growing here and around the world.

What the administration gives us is politics. What the country needs are constructive strategies free of ideology. But the risks of future economic shocks will multiply so long as we remain locked in a rancorous political culture with a leadership more inclined to public relations than hardheaded pragmatic recognition of what must be done to restore America's vitality.

END QUOTE

Stocks at Record Highs, But How About Consumers?

The Dow Jones Industrial Average hit a new record high on March 5 closing at 14,253.77, surpassing its previous record high of 14,164.53 in October 2007. It has since made several new record highs and is currently trading above 14,600. The DJIA is a narrow index made up of 30 large publicly-traded US companies.

The much broader S&P 500 Index lagged the Dow in the latest rally, and that worried a lot of traders and investors. However, the S&P 500 finally managed to close at a new record high last Thursday at 1,569.19 versus its previous record of 1,565.15 in early October 2007. Since then, the S&P 500 has moved in a trading range and is above 1,570 as this is written.

As I have discussed often in recent weeks, the stock markets have been buoyed by the Fed’s decision to continue buying $85 billion a month in Treasury and mortgage-backed securities indefinitely. The Fed’s decision was more than enough to override some disappointing economic news and even the financial crisis in Cyprus.

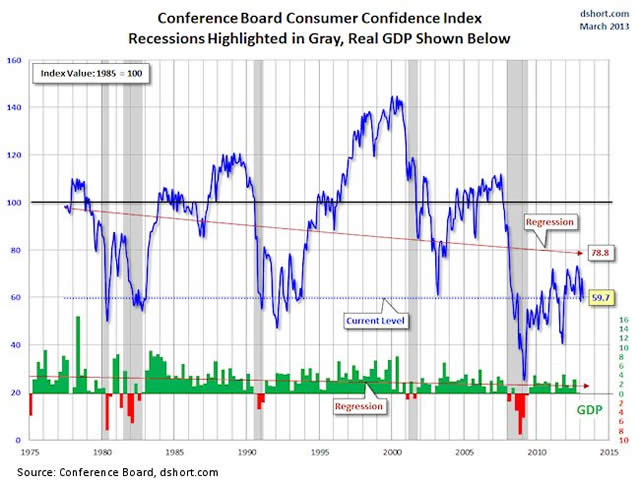

With the Dow and S&P at new record highs, one might assume that consumers and investors in general are jubilant. Let’s take a look. One way to gauge the public’s mood about the economy is the Consumer Confidence Index. The Index plunged in March to a reading of 59.7, down from a revised 68.0 in February and sharply lower than the pre-report consensus of 66.9.

But what is even more revealing about consumer confidence is where the Index stands relative to previous levels. Prior to the Great Recession of 2008-early 2009, the Consumer Confidence Index was well above 100 for the two years prior to the financial crisis. Prior to the recession of 2001, the Index was above 140. Take a look at the chart below.

As you can see, while the Consumer Confidence Index has recovered significantly from the Great Recession, it is still hovering near the lows of previous recessions despite the fact that we’re now over four years into this so-called “recovery.” This dovetails perfectly with Zuckerman’s analysis reprinted above.

How Are Investors Doing in This Bull Market?

Despite the Fed-driven bull market in stocks, investors in general haven’t done nearly as well as the markets. Vanguard, the world’s largest mutual fund company, reports that average 401(k) balances rose from $78,000 at the end of 2007 to $86,000 at the end of 2012. That’s an average return rate of just 2.3% (net of contributions) as compared to around 5% for the Dow and the S&P 500.

Keep in mind that the 401(k) accounts researched by Vanguard were fully invested over the last five years. That was certainly not the case with millions of individual investors who bailed out of the stock markets, in part or in full, during the recession and financial crisis.

The Investment Company Institute that tracks mutual fund inflows and outflows reported that stock mutual funds had huge redemptions in 2008 and 2009. This pattern of outflows continued in 2010 and even beyond. In fact, ICI reports that there were net outflows from domestic equity mutual funds in 21 of 24 months in 2011 and 2012.

Net inflows to equity mutual funds didn’t turn positive until January of this year. These data prove that millions of investors missed all or most of the bull market in stocks that began in early 2009. Likewise, many are only getting back onboard now with the Dow and S&P 500 at all-time record highs… Selling low and buying high.

One last point on the recent ICI fund flow data: We don’t have all the data for March yet, but one point jumps out at us for January and February. Investors going back into stock funds this year are clearly favoring global funds over domestic funds by a wide margin.

Finally, not only have millions of investors missed out on most or all of the bull market in stocks over the last four years, they have also seen their returns on CDs and most other fixed-income investments implode. According to Bankrate.com, the average interest on savings was 5.3% in October 2007 as compared to only 1% or less today.

The sharp reversal in interest rates has significantly cut the buying power of retirees and anyone else dependent on a fixed income. This is yet another reason why this economic recovery is so disappointing.

The Love Affair With Treasury Bonds Continues

While we’re on the subject of ICI mutual fund flow data, let’s turn our eyes to the bond market once again. If you recall, I turned bearish on taxable bonds (including Treasury bonds) late last summer. In August, I released my Special Report:How to Avoid the Bursting of the Bond Bubble.

In late July of last year, the yield on 30-year Treasury bonds fell below 2½% for the first time ever. In fact, the yield fell to a record low of 2.44% on July 25 last year. That wee little voice in the back of my head was screaming: Who in their right mind would loan the US government money for 30 years at less than 2½%?

You can see in the chart below that bond yields bottomed in late July and have been rising ever since. You can see the uptick in the yield from the low of 2.44% to a high of 3.25% earlier this month. That’s an increase of 33%! That means 30-year Treasury bond prices have been hit hard in recent months, although the yield has backed off a bit over the last few weeks.

As you know, when bond yields rise, the prices of those bonds decline, and vice-versa. As you also know, bond yields have been falling ever since interest rates peaked in 1981, and bond prices have risen accordingly for over 30 years. Treasury bonds have been one of the best investments out there for a generation.

As a result, millions of investors are overloaded in bonds and bond mutual funds today. Many of those same investors only invested in the last couple of years – AFTER interest rates had fallen to near historical lows. They will be in big trouble if long-term interest rates continue to rise.

Despite the fact that taxable bond funds (including Treasury bond funds) have incurred some losses since the market top in late July, tens of billions of dollars continue to gush into these funds. According to ICI, taxable bond funds saw net inflows averaging $21 billion a month in 2012. Another $26 billion was invested in January of this year.

There were those who speculated late last year and earlier this year that the increased inflows to equity funds were coming largely from the bond market. Yet as noted above, a lot of new money is still flowing into taxable bond funds. So while the bond bubble is leaking a little air, it hasn’t burst yet! But that day may be coming soon.

As I discussedlast week, the Fed is hinting that it may start scaling back its $45 billion a month in Treasury bond purchases, perhaps before the end of the year. It is reported that the Fed has been buying almost 80% of all the Treasury bonds issued by the government. Thus, it will almost certainly be negative for bond prices when the Fed scales back its record purchases.

The only way I can see bond yields trending lower again is if there is another major financial crisis in Europe. In the wake of the crisis in Cyprus, some fear that a similar fate will hit major banks in Spain, Italy and perhaps other countries in southern Europe. Currently, it doesn’t look like that will happen. But if it does, that would increase demand for US Treasuries as a safe haven.

Otherwise, I believe that US long-term interest rates will continue to move higher, and that is bearish for taxable bonds. If you are overweight in long-only taxable bonds, including Treasury bonds, I recommend that you take some profits and lighten up.

Wishing you profits,

Gary D. Halbert

© Halbert Wealth Management