IN THIS ISSUE:

1.How Much Did the Economy Slow in the 4Q?

2.US Debt Crisis – I’ve Been Wrong For Years

3. BCA: Debt Supercycle Likely to End in 3-5 Years

4. Breakdown of the $16+ Trillion National Debt

5. TheDebt-to-GDP Ratio & Why It Matters

6. Interest on the National Debt is a Growing Problem

Overview

[ Editor’s Note : Last week’s E-Letter“Gun Control & How to Play Upcoming Debt Battles”was one of the most widely read articles I’ve written in years, maybe ever. It landed at #2 on the AdvisorPerspectives.com most read list. Obviously, these are very hot topics!]

I first began writing my “paper” newsletter in 1977. That was 35 years ago, and I’ve been writing it continuously ever since. In fact, there are still some clients and readers who receive my newsletter in paper form only. But over a decade ago, with the advent of the Internet, the transmission of my newsletters gradually shifted to the Worldwide Web.

Thanks to InvestorsInsight.com and other Internet publishers who picked me up, my weekly E-Letter is now opened bytens of thousands of people each week. My how things have changed! But in looking back at some of my earlier writings, one theme has continued throughout.

That theme has been my continued concern about the explosion in US DEBT.

Today, the national debt has mushroomed to almost $16.5 trillion. It has exploded by over 60% just since President Obama took office, when it was at $10 trillion. At the end of 2012, our national debt exceeded 100% of GDP (104%) for the first time since WWII. By the end of Obama’s second term, our national debt will top$20 trillion at the rate it’s growing.

We all know that at some point, this massive Ponzi scheme will come to an end. The only reason it has gotten to this point is because the US dollar is the world’s “reserve currency” which enables our government to print as much money as it wants. This will end only when foreign buyers of our debt decide to turn off the spigots. The only question is when.

Last week, one of the most respected research groups in the world predicted that the US likely has only 3-5 years before the wheels fall off and the world is thrust into a major financial crisis, possibly even a depression.

We’ll talk about all of these things as we go along today. But before we go there, let’s take a brief look at the economy before tomorrow’s advance (first) estimate of 4Q GDP.

How Much Did the Economy Slow in the 4Q?

The Commerce Department’s third and final estimate of 3Q GDP came in stronger than expected at 3.1% (annual rate). The report on December 20 said that the better than expected number was due primarily to consumer spending,private inventory investment, federal government spending and residential fixed investment.

There is a broad consensus that 4Q GDP was not nearly as strong. The pre-report consensus is for a rise of only 1.0%. The range is 0.5% to 2.6%. The report will be released tomorrow morning at 8:30 EST.

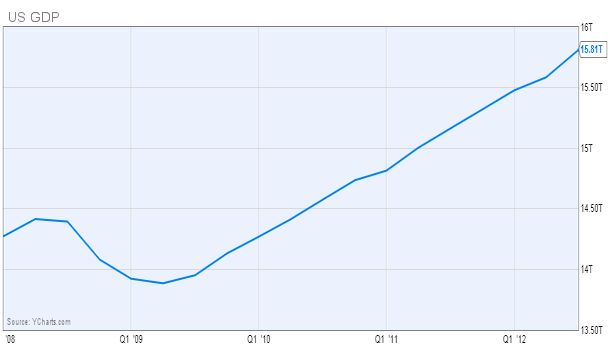

At mid-2012, Gross Domestic Product expanded to $15.81 trillion according to the Commerce Department. While the current recovery has been weak in comparison to previous post-recession expansions, the economy has added almost $2 trillion in GDP since early 2009. Of course, it should have been double that or more.

Consumer confidence dropped in January to its lowest level in more than a year as Americans were more pessimistic about the economic outlook and their financial prospects, according to the Conference Board report out this morning. The Consumer Confidence Index fell to 58.6 in January from an upwardly revised 66.7 in December – well below the pre-report consensus of 64-65. It was the lowest level since November 2011.

While economic reports have been mixed in the last few weeks, there has been continued good news from the housing sector. Sales of new homes last year were up almost 20% over 2011 according to HUD. Sales of existing homes were up 12.8% over 2011. Likewise, housing starts rose 12.1% in 2012.

The median sales price of existing homes rose to $176,600. That’s up 6.3% from 2011 prices. It was the largest annual increase in home prices since 2005. For all these reasons, homebuilder confidence is reportedly at a five-year high.

US Debt Crisis – I’ve Been Wrong For Years

If you had asked me 20 years ago if the US could survive as we know it with $5 trillion in debt, I would have said absolutely not. But we flew by $5 trillion in debt by the end of 1994. If you had asked me a decade ago if the US could survive with $10 trillion in debt, I would have said the same thing. But by the end of 2008, we topped $10 trillion. Now we’re at almost $16.5 trillion and rising rapidly.

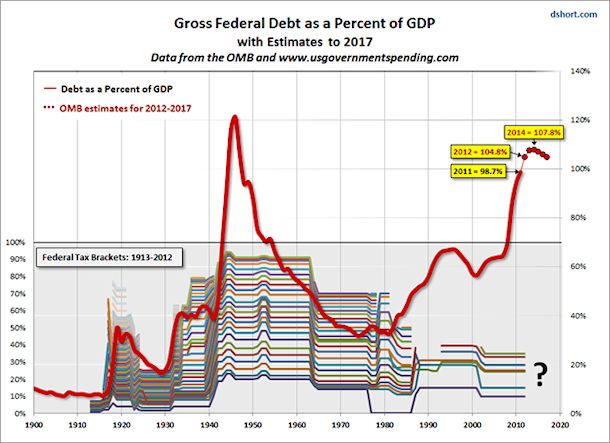

*Note that this chart is as of the 3Q of last year.

At the end of President Carter’s term in 1980, the national debt was $930 billion. At the time, I thought that was a lot. In 1981 under President Reagan, our national debt first topped $1 trillion. By the time Reagan left office, the debt had more than doubled to $2.69 trillion. Even though I voted for Reagan twice, I roundly criticized him more than once in my newsletter for deficit spending.

The point is, I, like many Americans, have been wrong in speculating about how much debt America could take on before it leads to a financial crisis. Now that the national debt is over $16 trillion and rising rapidly, some Americans now feel that we can borrow however much money we want, for however long we want. That is wrong!

BCA: Debt Supercycle Likely to End in 3-5 Years

Long-time clients and readers will remember The Bank Credit Analyst (BCA). BCA is one of the oldest investment research firms out there and is highly respected. Last week, a Special Report from BCA landed in my e-mail inbox. For many years, BCA has warned that the massive increase in US government debt – which they coined the “Debt Supercycle” – would have to come to an end at some point, and would probably end very ugly.

In their latest Special Report, the editors predict that the Debt Supercycle will come to an end in the nextfive years, maybe as soon asthree years.

The end of the Debt Supercycle would mean that it would become much more difficult for the US government to borrow money, if at all. Interest rates would soar and a new financial crisis would erupt. Worst case, the US would default on its debt.

At this point I trust that most of my clients and long-time readers have given up on any chance that Congress will balance the budget and stop the explosion in debt. Likewise, I think we know the financial markets are going to revolt at some point and it will be ugly, maybe very ugly.

At some point in the next few years, this massive build-up of debt is going to spark a new and likely significant round of inflation. This will send interest rates sharply higher. That will likely lead to another financial crisis that could make 2008 look tame.

Now we have BCA predicting that the crisis is likely coming in the next 3-5 years. The problem is, President Obama will be in office for the next four years, and it should be clear to all that he doesnot want to reduce the debt. If you saw the movie, 2016: Obama’s America, none of what has happened in the last four years should have come as a surprise to you. To this point, the 2016 documentary is dead-on.

With that warning delivered, let’s return to our discussion on the national debt.

Breakdown of the National Debt

The US national debt is the sum of all outstanding debt owed by the federal government. Over two-thirds is “public debt,” which is owed to the people (US and foreign), businesses and foreign governments who bought Treasury bills, notes and bonds. The public debt at the end of 2012 was apprx. $11.5 trillion.

The “non-public” debt is that which is held by government accounts, also known as “intra-governmental” debt, and includes non-marketable Treasury securities held in accounts administered by the federal government that are owed to program beneficiaries, such as the Social Security Trust Fund. The non-public debt at the end of 2012 was apprx. $5 trillion.

As of July 2012, $5.3 trillion (almost half) of the debt held by the public was owned by foreign investors, the largest of which are China and Japan at just over $1.1 trillion each. What happens if either or both decide to stop buying Treasury securities? More on that later.

The other largest foreign holders of US Treasury debt are the oil exporting countries at $267 billion, with Brazil next at $251 billion and the Caribbean Banking Centers at $240 billion, according to the Treasury Department. The next largest holders (in order) are Taiwan, Switzerland, Russia, United Kingdom, and Hong Kong, which own between $135-$191 billion each.

The US national debt is the largest in the world for a single country. (The combined EU debt is close, and sometimes greater.) How did it get so large? Purchasers of Treasury securities still reasonably expect the US economy to grow enough to pay them back. Also, because the US is the world’s largest importer, countries like China and Japancontinue to buy large quantities of our debt so we will continue to buy their exports.

Even before the financial crisis and recession, the US national debt grew 50% between 2000 and 2007, ballooning from around $6 trillion to over $9 trillion. The $700 billion bank bailout helped the debt grow to $10.5 trillion by December 2008. The debt is tracked by theNational Debt Clock.

The Debt-to-GDP Ratio & Why It Matters

The national debt level is often expressed as a percent of the total country’s economic production, or GDP, which was estimated at $15.8 trillion for calendar year 2012. With the national debt at $16.4 trillion, that means the debt-to-GDP ratio is now at 104.8%, up from 51% in 1988.

As you can see in the chart below, the US debt-to-GDP ratio has not been above 100% since World War II. Notice also the near vertical spike since 2009. Also notice that projections don’t show us falling below 100% anytime in the next five years! Remember these are the official projections of President Obama’s own Office of Management & Budget (OMB).

Let me caution that you will see similar graphs which show the debt-to-GDP ratio up to only 70-75% of GDP. In fact, most debt-to-GDP charts you see will include the lower numbers. Why is that? If you count only the debt held by the “public,” and not the total debt, you come up with a number of 73% as of the end of 2012. Yet this is very misleading.

Some justify ignoring the non-public internal trust fund debt because that’s money that “we owe to ourselves.” The misleading part is that we are now starting to convert these trust funds into actual payments for Social Security and Medicare beneficiaries. As we do so, these intra-governmental IOUs must be converted into publicly held debt. Eventually most or all of the non-public debt will have to be converted into actual Treasury notes and bonds that will have to be sold. So it is misleading tonot count it as part of the total debt.

The debt-to-GDP ratio is one of the indicators of the health of an economy. It is the amount of national debt of a country as a percentage of its Gross Domestic Product. A low debt-to-GDP ratio indicates an economy that produces a large number of goods and services and profits that are high enough to pay back debts. Governments aim for low debt-to-GDP ratios, but in most of the developed world, the ratios are rising at an alarming rate.

Interest on the National Debt is a Growing Problem

Total interest paid on the national debt was $359 billion in FY 2012 thanks to lower interest rates. In FY 2011, the interest was $454 billion, the highest ever. Not to oversimplify, but we’ve got ahuge problem on our hands long-term. We all know that interest rates have nowhere to go but up! When you combine rising interest rates with trillion-dollar deficits, the cost of servicing our debt is projected to skyrocket.

I’ve seen numerous projections that show the interest on the national debt topping $1 trillion a year if interest rates go back to normal levels.

Here’s another area where a word of caution is in order. Oftentimes, you’ll see the interest on the national debt referred to as the “net” interest. The argument here is that the interest paid on the roughly $5 trillion in non-public debt should not be counted since the government is essentially paying itself. Maybe so, but the interest is still paid.

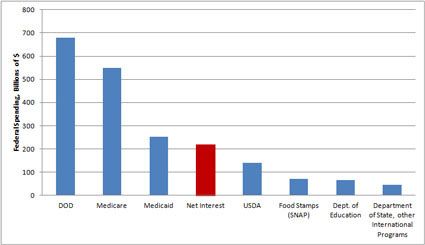

Here is just one example of using “net” interest that appeared in US News & World Report:

The writer uses net interest of $220 billion in the chart above. But we know that the total interest paid in FY2012 was $359 billion and $454 billion in FY2011. In both years, the interest paid was larger than any other government programs other than Medicare and the Defense Department.

The problem is that the interest paid to the Treasury should be going to the various Trust Funds that hold those Treasuries, not into the government’s coffers to be spent. Even the Treasury Department reports the total interest paid, as you can see atTreasuryDirect.gov, not the net. Nonetheless, you’ll see net interest figures more often than not.

Conclusions

The day is coming when the US has borrowed so much that buyers of our debt will begin to fear that they will not be paid back, and/or that they will be repaid with dollars that are worth substantially less. While I believe this outcome is inevitable at some point, investors – foreign and domestic – are still lined-up to buy our debt even though interest rates are at historical lows. At the very least, these buyers will at some point demand higher yields on their Treasury investments.

If it is the latter, there is some chance that it could be a reasonably orderly process, but I doubt it. Confidence in the “full faith and credit” of the United States could evaporate very quickly, and things could get ugly very quickly. Think Greece.

Best regards,

Gary D. Halbert

© Halbert Wealth Management