Most people are looking to the politicians in Washington to reign in the deficit by bringing spending under control. Based on their record this optimism seems severely misplaced. Nevertheless, the technical position of the bond market is suggesting that a more disciplined and powerful force is waiting in the wings. After a long 31-year vacation it may be time for the bond vigilantes (skeptical global bond investors who vote with their money) to return to town. The President has said a deal over the debt ceiling is non- negotiable but the non-partisan bond vigilantes may have a different view.

To set the scene, the average secular or very long-term trend in bond yields since the mid-nineteenth century has averaged 27-years. The current downtrend for yields (bull market for bond prices) that began in 1981 is now close to 32-years in length. Based on historical precedent it is certainly due for a reversal. A secular trend is like an ocean tanker since they both require a lot of effort and time to reverse.

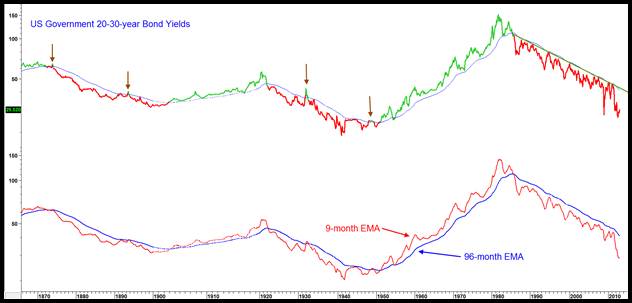

Chart 1 US Government 20-20-year Yields 1865-2013

As a result it often takes several years or more before it is evident that a new secular trend is underway.

A useful approach for spotting such reversals is to observe when the 9-month EMA of government 30-year yields crosses above and below its 96-month average. Since data on the 30-year yield has a limited historical record the series plotted in Chart 1 has been spliced with several others in order to obtain some historical perspective. The green highlights indicate bullish periods and red bearish ones. Not surprisingly there have been some whipsaws in this 150-year history and they are flagged with the small brown arrows. By and large though, the system has worked well, experiencing its last false signal in the 1940’s.

Trendline violations (see Chart 4) have also been helpful in identifying reversals. Sometimes good reversal signals are difficult to spot but the current downtrend is blessed in that regard since a significant long-term trendline is intersecting with the 96-month EMA. That reinforces their roles as a resistance barrier. Bottom line, when the yield eventually pushes through this resistance area the signal will likely be a reliable one. The odds of that happening in the next few months are low because the 9-month EMA is still falling, and after all we are dealing with a secular reversal which takes time.

Nevertheless, there are some tentative signs that the secular trend may be reversing. That’s because such turning points are often characterized by extreme swings in certain momentum indicators as the prevailing trend literally blows itself out. The theory of contrary opinion tells us that when the crowd reaches an extreme prevailing wisdom has been fully discounted and its time to look for alternative scenarios to justify a reversal in trend. Well, it is an established fact that momentum indicators reflect sentiment, ergo we can use momentum indicators to help us identify when the crowd has reached an extreme.

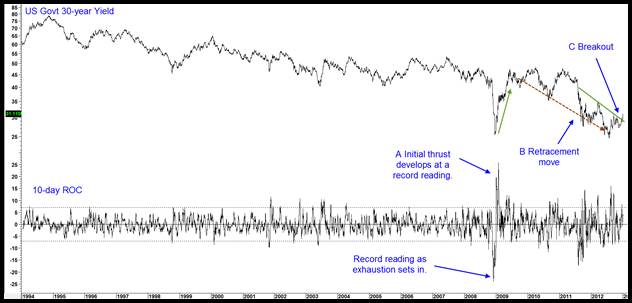

Chart 2 US Government 30-year Yield and a 10-day ROC

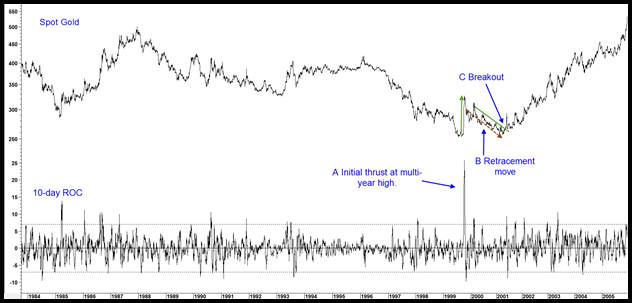

Chart 2 compares the progress of the 30-year yield to a 10-day rate-of-change (ROC). It is evident that the ROC fell to a record low reading in 2008 as the price trend totally exhausted itself. Then begins a series of A, B C steps. A was an initial thrust to a multi-year high, in this case a record. B, a retracement move, as market participants re-visit their bearish emotions. Finally, C offered confirmation with a breakout by the price above a down trendline connecting the peaks of the last phase of the retracement move. Chart 3 shows that this was very similar to the reversal in the 1980-99 secular decline in the gold price.

Though the final low was not associated with a multi-year selling climax, the remaining A,B and C steps developed right on cue.

Chart 3 Spot Gold and a 10-day ROC

Chart 4 US Government 20-30-year Yields 1865-2013

Supplementary evidence is presented in Chart 4, where the 12-month ROC swung from a multi-century oversold to a multi-century overbought reading in the 2008-9 period. Note how the trendlines were very useful and reliable in identifying previous secular trend reversals. That secular down trendline stands just over 4.25%. Incidentally, the 1932 low in US equity prices was signaled in a similar way with a 12-month ROC, which swung from -65% in July 1932 to +128% in June 1933. Neither of those numbers has been ever been seen again in 200-years of US stock market history.

These are strong signs of a secular reversal but not enough to come to a beyond reasonable doubt conclusion. For that we require a series of rising peaks and troughs, secular trendline violations and a 96-month EMA crossover.

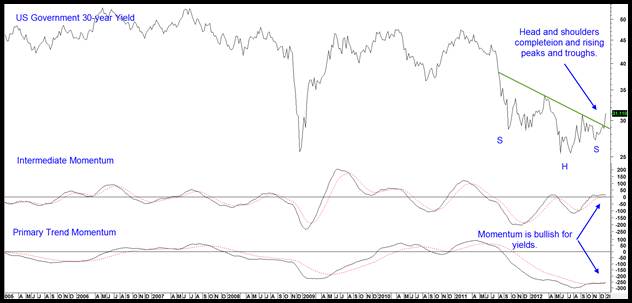

Chart 5 US Government 30-year Yield and Two Momentum Indicators

All secular uptrends begin with their first primary or business cycle associated bull market, and there is substantial evidence that one in yields (bearish for bond prices) is already underway.

In that respect Chart 5 shows that the 30-year Yield has just completed what is known to market technicians as a reverse head and shoulders pattern (These formations are defined as a final low separated by two higher lows followed by a breakout above the trendline joining their rally highs.) In addition the Friday January 4 closing took the yield above its previous rally high thereby setting up a series of rising peaks and troughs, another plus. Finally, the primary trend momentum, in the bottom panel, has just triggered a buy signal by rallying above its 26-week EMA. Its intermediate counterpart is also positive and neither are overextended. It’s not evident from this chart which has a limited history, but primary trend momentum in this instance reversed from a record oversold condition, thereby providing another sign that the secular trend may be reversing.

Regardless of whether that’s the case or not there is strong evidence that the primary trend has already reversed. In addition long-term momentum for industrial commodities has started to reverse to the upside, serving as an inflationary warning and another argument for higher yields. The CRB Spot Raw Industrials and ECRI JOC Industrial Products Indexes have both moved above their 12-month moving averages. In short, there are strong indications that the current business cycle has moved to a stage that is consistent with inflationary pressures and that’s not good news for bond prices.

Chart 6 World Bond Index *(BWX*3 +AGG)

Rising bond yields and falling prices is not likely to be limited to the US as Chart 6, shows that my World Bond Index (constructed from a weighted average of the BWX (Barclays International Treasury Bond ETF) and the AGG(i-Shares Total US Bond Market ETF) has just ruptured a 12-year up trendline. To me that signals that bond vigilantism is likely to be an international movement.

The global financial system has experienced four years of unprecedented central bank balance sheet expansion and record budget deficits. These policies have been carried out to what would previously have been considered unthinkable extremes. Now the global economy is set to expand again and the technical position of the credit markets has started to deteriorate in a major way. As a consequence the fiscally irresponsible chickens may well be coming home to roost. Politicians in the US may think that the next couple of months will be business as usual as they take their time discussing budgetary excesses.

However, being the lagging indicators that politicians are, there is no realization yet that the real negotiations will involve a much tougher partner. The return to town of Mr. Market and his band of bond vigilantes may very well force fiscal discipline sooner rather than later.

Martin Pring is Chairman of Pring Turner Capital and investment strategist for the Pring Turner Business Cycle ETF ( symbol DBIZ).

© Pring Turner Capital Group