What’s good for the US dollar isn’t always good for US bonds — but investors are finding ways to work around it.

Even as the greenback draws support from a resilient American economy and renewed tensions in the Middle East, those same variables have pressured US Treasuries. Bond yields have remained elevated on concerns that strong growth and higher oil prices will stoke already-sticky inflation and prompt Federal Reserve interest-rate hikes.

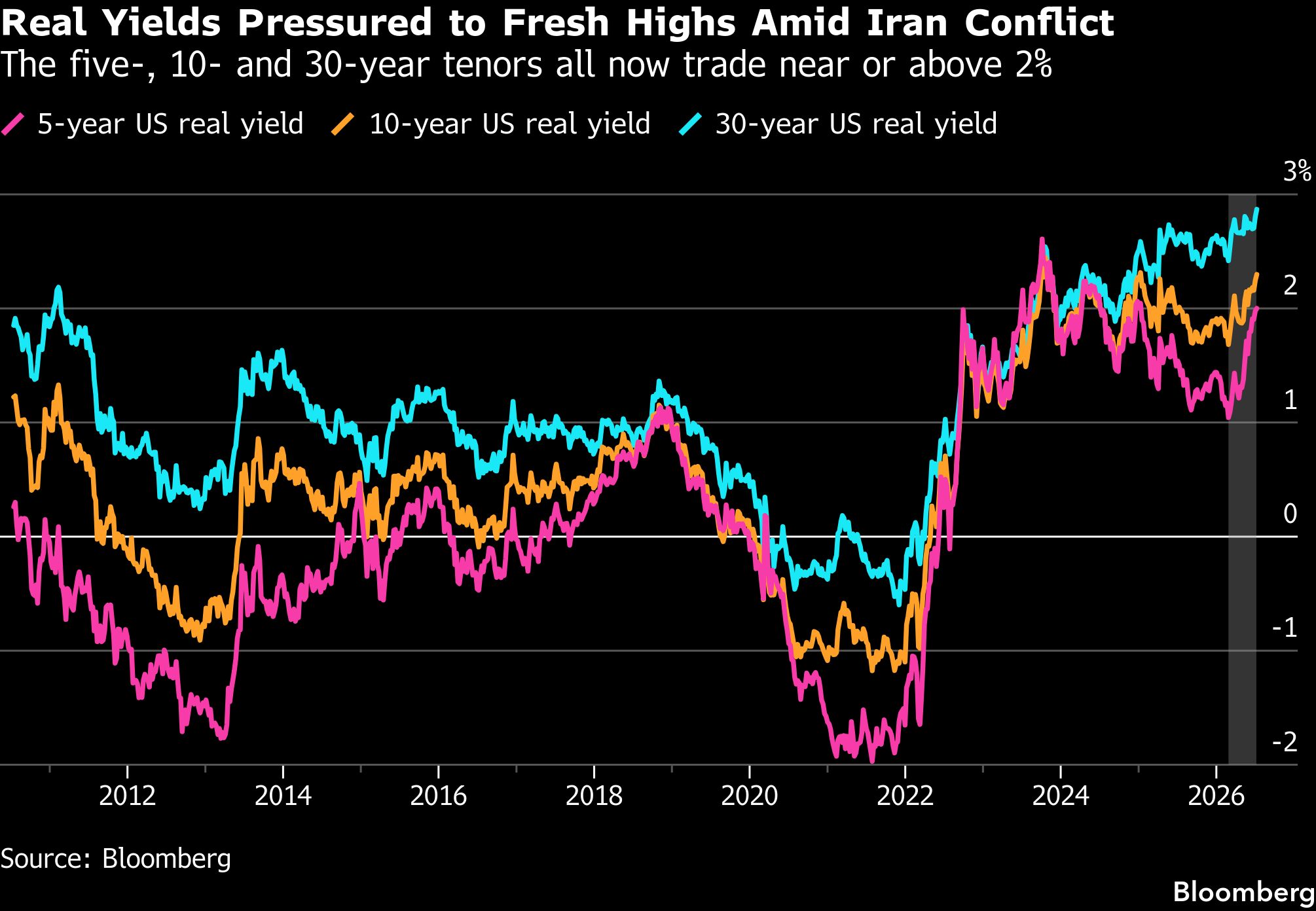

The outlook is most clearly reflected in a sharp rise in so-called real US yields, which strip out the effect of inflation on returns. The yield on inflation-adjusted, 10-year Treasuries last week climbed above 2.3%, its highest level in more than a year, as investors price in tighter Fed policy in the months ahead.

“The reason real yields are where they are today is straightforward,” said Brendan Murphy, head of fixed income for North America at Insight Investment, which manages about $836 billion in assets globally. “The Fed has turned more hawkish, economic data has remained resilient and inflation has stayed elevated.”

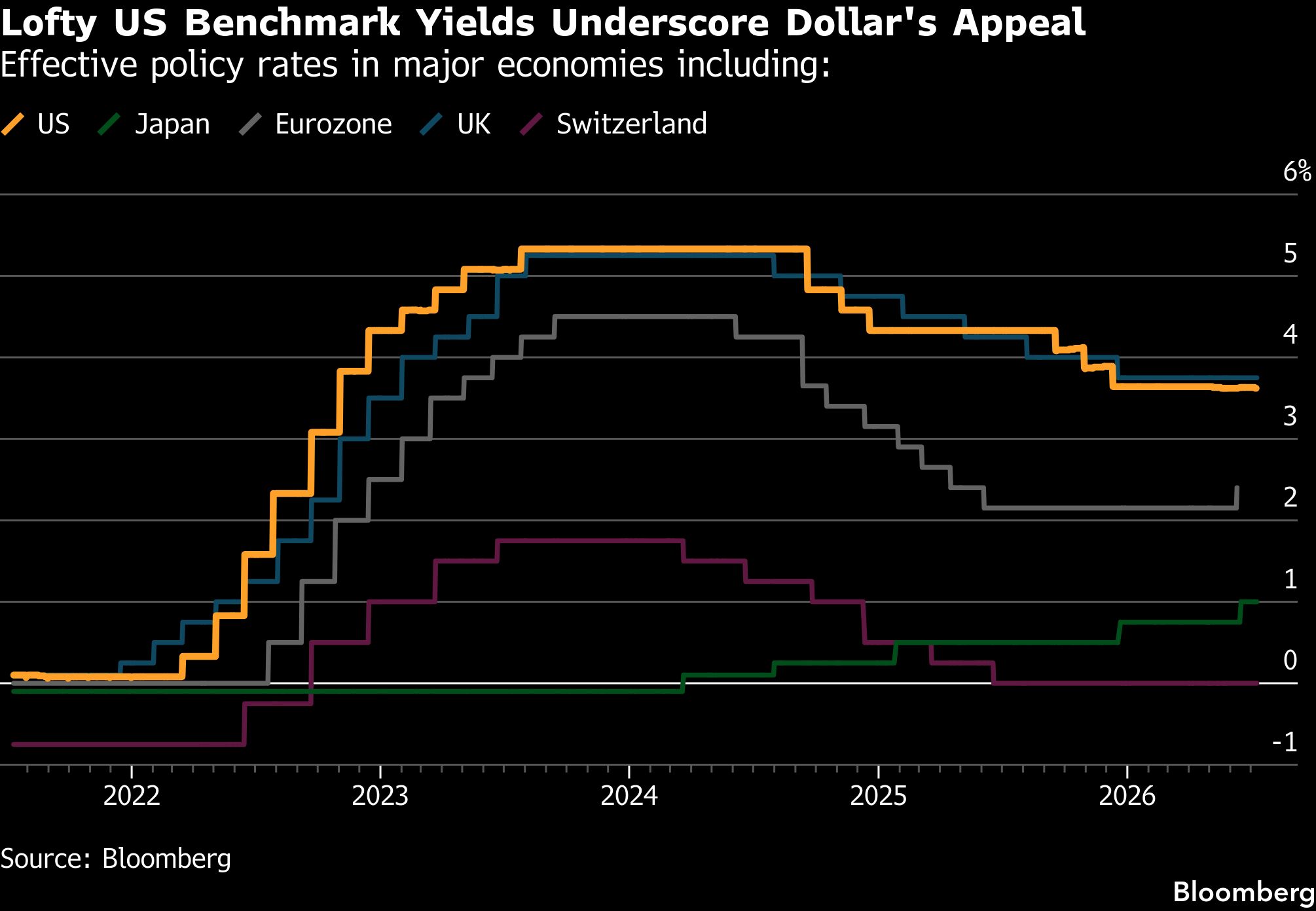

For investors, this creates a conundrum. While the rise in real yields relative to those in other major markets makes dollar-denominated assets more attractive to global investors, investing in inflation-sensitive US bonds leaves investors vulnerable to losses. Some, however, are finding ways to thread the needle.

Adam Coons, chief investment officer at Winthrop Capital Management, which manages more than $3.9 billion, says he is long the dollar, but less positive on longer-term US bonds that will get hit the most should the US economy continue to outperform the rest of the world and fuel inflation. He’s funding the firm’s long dollar exposures by selling the euro and yen, currencies that offer less attractive all-in yields.

“The dollar is currently enjoying the best of both worlds. It offers high yield and superior economic growth,” Coons said. He’s wagering that longer-term bonds in the UK and Europe will perform better than their US counterparts.

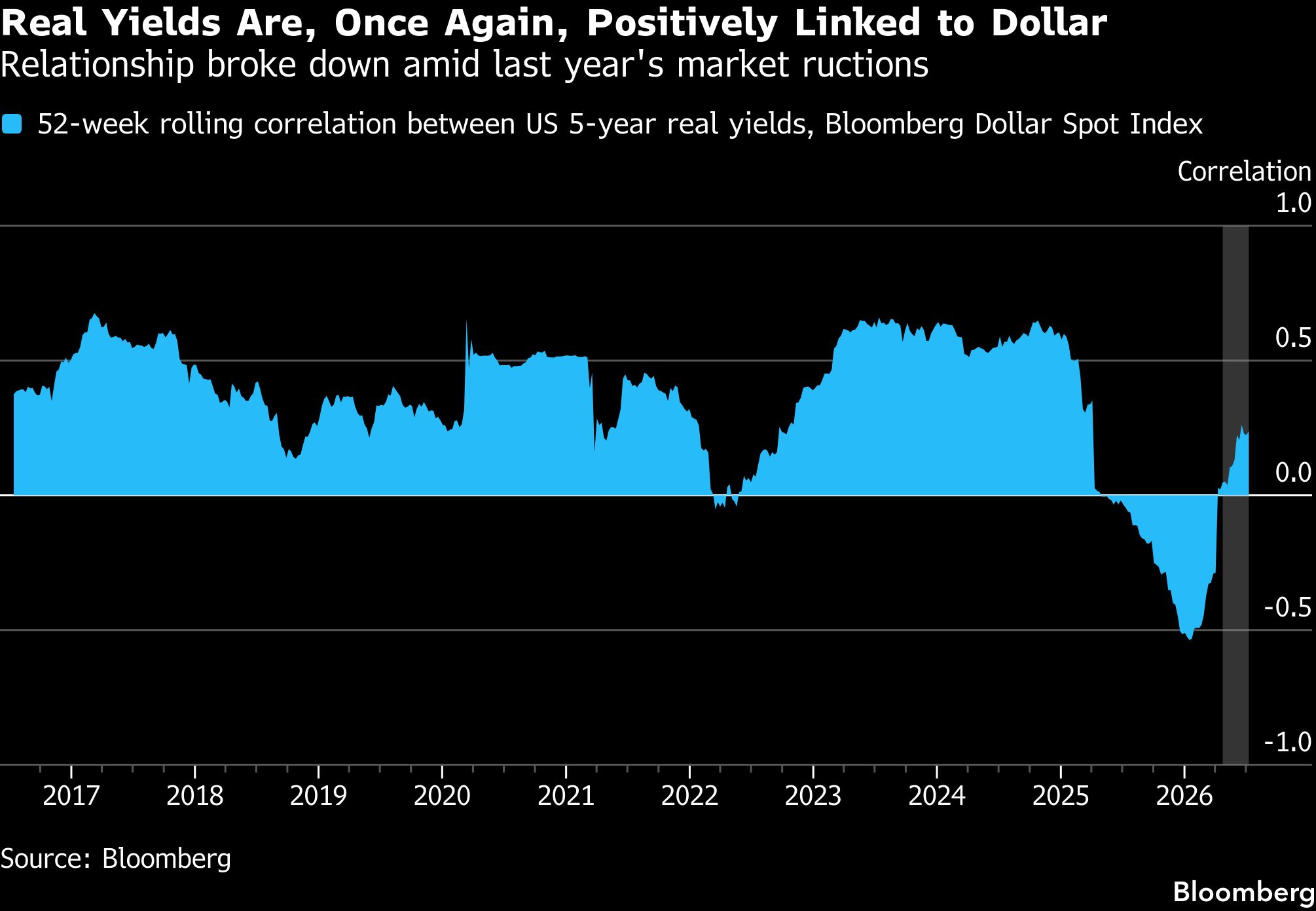

The greenback has historically tracked US real yields closely. That relationship fractured last year as the Trump administration’s trade war shook confidence in US assets, but it has since re-emerged, putting the Fed’s rate outlook — especially relative to major peers — back at the center of the dollar’s trajectory.

The Bloomberg Dollar Spot Index held firm last week, not far from its highs for the year, as fresh doubts emerged around peace prospects between the US and Iran. The gauge was steady on Monday.

The yield on policy-sensitive two-year Treasury notes rose 7 basis points to 4.21% last week — also near its year-to-date high, and remained around that level at the start of the new week. Over the weekend, the US and Iran traded strikes, while Washington and Tehran issued conflicting declarations over whether the Strait of Hormuz remains open to shipping.

At Brandywine Global Investment Management, portfolio manager Jack McIntyre argues the dollar’s recent strength is justified as markets price in a more hawkish Fed and holds an underweight position in Treasuries, in large part because of the robust US economy.

Speculative traders are now the most bullish on the greenback since 2015 and hold more than $40 billion in long dollar derivatives positions, according to Commodity Futures Trading Commission data for the week ended July 7.

This week, traders will scrutinize key readings on US consumer and wholesale prices in June. They will be the last inflation prints before Fed officials led by Chairman Kevin Warsh meet later this month, providing important clues for investors assessing the outlook for rates.

Investors will also focus on Warsh’s first Congressional testimony as Fed chairman, expected on Tuesday.

Swaps traders now price almost 40 basis points of Fed tightening by December, up from about 15 basis points in early June. Economists surveyed by Bloomberg expect headline CPI as well as the core figure, which excludes food and energy, to have cooled slightly from May on a year-over-year basis, with both still running well above the Fed’s 2% target

Not all investment houses are convinced the Fed needs to hike rates before the end of the year, in large part because the jobs backdrop isn’t as solid as it was even six months ago.

“Growth has been strong, but we think the labor market is telling a more nuanced story,” said Insight Investment’s Murphy. “The path of least resistance is for policymakers to remain on hold, and we think real yields have likely already seen their highs.”

There’s also the risk, as described by George Goncalves at MUFG Securities, that rising real yields and a stronger dollar are already tightening financial conditions — in effect, hiking borrowing costs without the Fed having to move itself.

Major financial firms, Bank of America Corp among them, are nonetheless sticking with their expectation that a hawkish Fed and sticky real yields will bolster the dollar in the months ahead.

A team at the firm including Michalis Rousakis and Claudio Piron recently upgraded their forecasts for the greenback into the third quarter. On Friday, they noted that “resilient growth is likely to keep US real rates elevated” and recommend traders buy the US currency versus lower-yielding peers.