One notable group has been absent from the 2026 stock rally: the American tech giants that have charged a nearly four-year bull run.

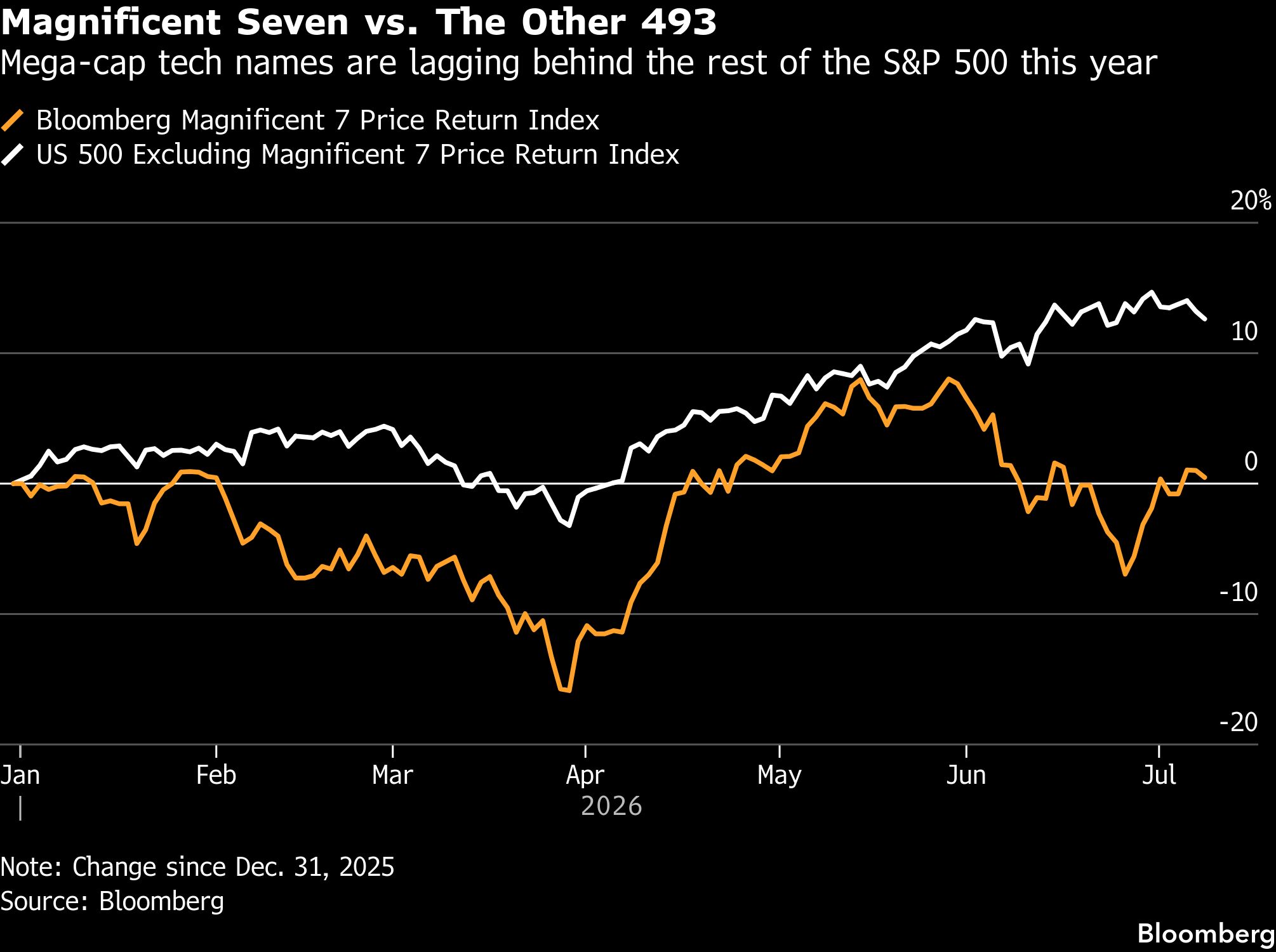

The Magnificent Seven Index, which includes companies like Nvidia Corp., Alphabet Inc. and Amazon.com Inc., has gone nowhere this year, even as the artificial-intelligence boom it’s bankrolling continued to propel other technology names. The group as a whole has trailed 300 stocks in the S&P 500 Index this year, including relative minnows like Dollar Tree Inc. and Hubbell Inc.

The shift is vexing Wall Street forecasters, who had counted on the group, which makes up a third of the S&P 500, when they forecast that the benchmark would finish the year at 7,824.09 points, on average. If the current trend of tech titans sitting idle continues, the remainder of the S&P 500 would need to rally 6.8% by late December, on top of 13% that group has already gained this year, for that target to become a reality.

“From here, I think it would be hard for the S&P to keep powering forward without participation from the Mag 7, specifically because so many sectors that have run up significantly, like energy for example, are subject to some downdraft too,” said Alonso Munoz, chief investment officer at Hamilton Capital Partners. “These names, the Mag 7, have a significant impact on the indexes being up or down.”

The Magnificent Seven cohort, the defining trade of most of the past decade, has lost its appeal this year as attention shifted to the biggest beneficiaries of the wave of cash dedicated to building out AI. Chipmakers have become the preferred way to play the technology, pushing the Philadelphia Stock Exchange Semiconductor Index up 78% this year, compared with a 0.5% gain in the Bloomberg Magnificent 7 Price Return Index.

That puts year-end targets at risk. Strategists on average expect the S&P 500 to finish 2026 at 7,824.09, implying an upside of almost 5% from Wednesday’s close. The views of the likes of Ed Yardeni and Oppenheimer’s John Stoltzfus are even rosier, and suggest that the 500-member gauge will eclipse 8,000 before January.

Should the Magnificent Seven group continue to advance at a snail’s pace, the burden falls on the remaining 493 stocks to carry the load. The non-Magnificent Seven stocks would have to rally 6.8% in order to reach the average year-end target, according to Bloomberg’s estimates.

In the past two weeks, market watchers at Morgan Stanley, Goldman Sachs Group Inc. and JPMorgan Chase & Co. have said the group’s underperformance, relative to chipmakers and the broader market overall, has gone too far.

For Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management, now is the time to revisit the Magnificent Seven for potential opportunities as semiconductors are “meaningfully overbought.”

“Acceleration of backlogged order books and expanding pricing power among semiconductor makers and ‘memory’ suppliers have been eye-popping, but we don’t think they’re sustainable,” Shalett wrote in a note published on Tuesday. “This is not a call on the cycle’s end, but it is a call to rebuild diversified exposure to potential AI build-out winners, re-embracing some of the hyperscalers.”

Bloomberg’s gauge for the Magnificent Seven lost 1.9% in the first half of 2026, compared with a 9.3% gain in the S&P 500. The 11 percentage-point spread is the group’s second-worst start to a year ever relative to the broader equity gauge.

The selloff has boosted the appeal of the cohort’s price-to-earnings multiples, which have dropped to 23.9 from 32.6 in late October. The Magnificent Seven Index’s valuations sat 2.4 points higher than those of the S&P 500 last month, near the lowest premium ever, data compiled by Bloomberg show.

While the green light is being given for a return to the Magnificent Seven, some believe the S&P 500 does not even need their participation to reach the average year-end target.

Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute, is not sure an improvement in the Magnificent Seven is necessary for the broader gauge to rise. He points to the performance of the S&P 500 excluding the seven mega-capitalization names: they’re currently up 13% year to date.

The S&P 500 “could potentially get there with the rest of the names,” said Melissa Brown, head of investment decision research at SimCorp, when discussing whether the gauge could reach 7,824.09 points by the year’s end. “But given the lower weights, they’d have to have bigger returns to get the whole index up that much.”

Rich Privorotsky, partner at Goldman Sachs Group Inc., is among those seeing an opportunity in the group. Privorotsky is extremely bullish on AI, but “much less convinced” the market is backing the right parts of the value chain. In fact, once scarcity disappears, owning an AI platform will be better, he added.

As Privorotsky puts it: hyperscalers “own the toll road, not just the car.”