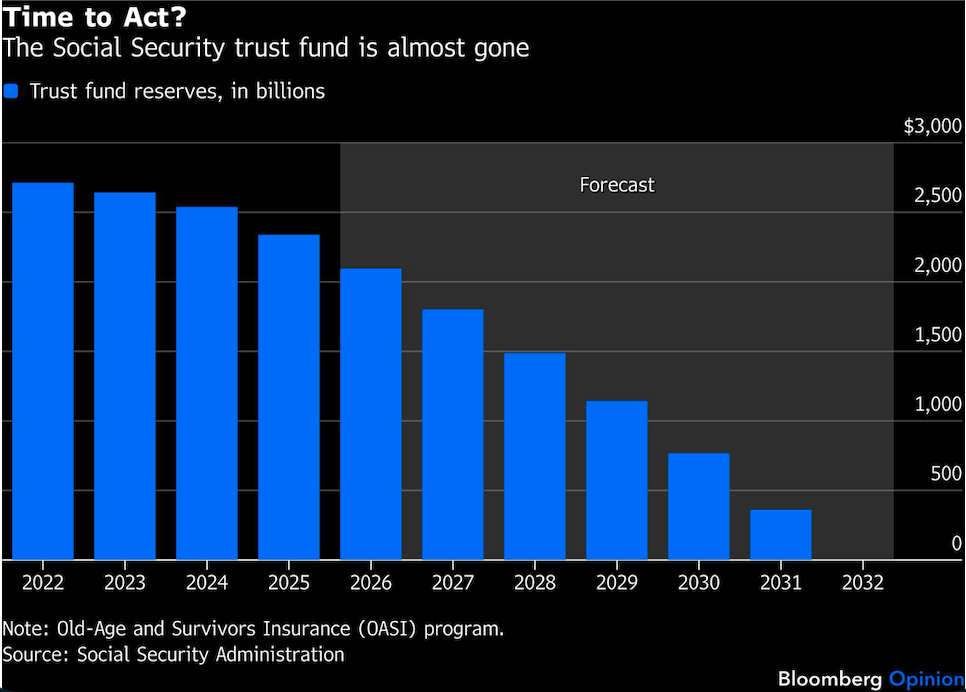

Social Security is now just six years away from insolvency, according to the latest annual assessment. Many in Congress might like to keep on ignoring the problem, as they have for years, but this won’t be an option much longer. Senators elected in November will see the system’s trust fund empty during their terms.

Maybe, just maybe, this is finally getting through. Senators Elizabeth Warren and Bernie Moreno — a Democrat and a Republican — have recently drawn attention to the issue. They propose applying the 12.4% payroll tax that funds the system to incomes above the current cap of $184,500.

By itself, this reform won’t suffice, but it’s good that they’re demanding action and even better that they’re working across the aisle. Bipartisan support for an effective solution needs to grow, and fast.

The new report predicts insolvency sooner than previously expected. The projected gap between pensions paid out and taxes received has grown, mainly thanks to declining fertility and lower immigration, hence fewer future workers and a smaller tax base. The tax cut for benefit recipients included in last year’s One Big Beautiful Bill Act didn’t help.

Once the deficit has drained the fund, the law requires that benefits equal revenue. If nothing is done, retirees can expect an automatic cut of 22%. Yet that wouldn’t be enough: Without further cuts or higher taxes, the deficit would reappear. Restoring the system to long-term solvency requires an even bigger drop in benefits or a much steeper tax increase than the one proposed by Warren and Moreno. Their plan would be quite a hike for the workers affected — but it would get the system only a little more than halfway to long-term solvency.

That’s the price of inaction. Any further delay will make finding the answer harder still.

Given the scale of the shortfall, a lasting remedy will have to include both targeted cuts in benefits and higher taxes on those who can most afford it. Here are the basic components: Reduce benefits for higher earners; raise the retirement age and link it to rising life expectancy; base cost-of-living increases on a more accurate measure of inflation (so-called chained CPI); tax benefits as though they were private pensions; apply the payroll tax to employer-provided health benefits; and, as the senators recommend, raise or eliminate the income cap on the payroll tax.

Any one of these alterations would be politically demanding, and a package involving all or most might seem downright impossible. But the only alternative is to abandon the system’s design altogether, by turning it into a welfare program supported by general revenue and ever-mounting public debt. That would not only invite eventual fiscal disaster, but it would also discard the idea that retirement benefits should be linked to taxes paid during one’s working years, and that those payments create an entitlement that people can trust. Most Americans value this notion and would hate to see it set aside.

To repair the current model, a comprehensive plan of reform is essential. And to repair it durably, as opposed to merely patching it up, Democrats and Republicans will need to work together. The country deserves a system that’s good for the coming decades, not just through the next election.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by The Editors