Water utilities are selling bonds at a record pace to upgrade aging pipes and meet tougher regulations as they prepare for a potential pullback in federal funding.

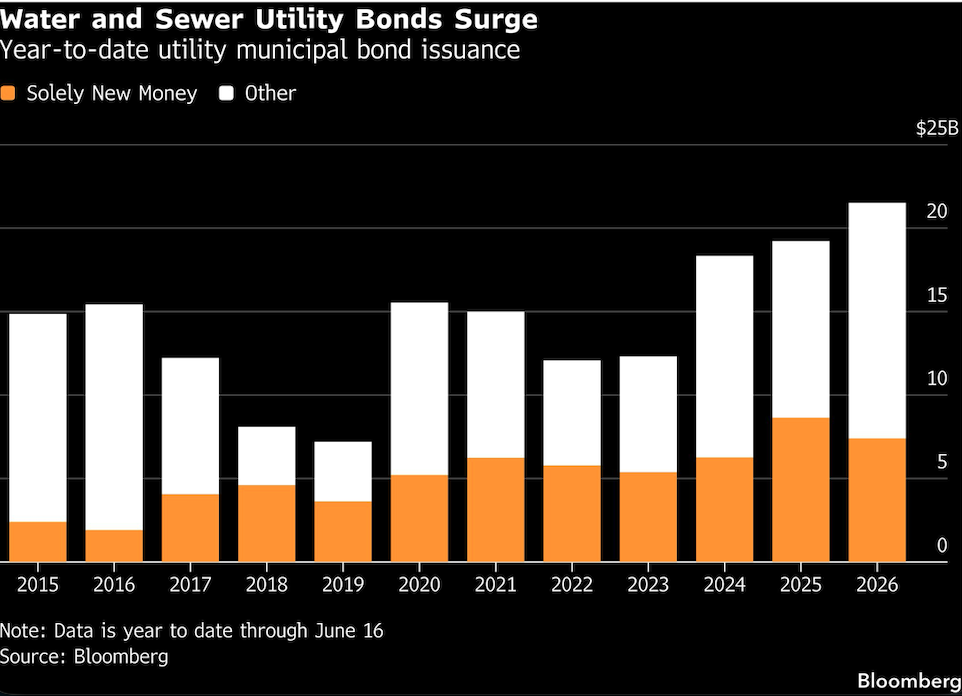

More than $21 billion of water and sewer bonds have been sold so far in 2026, the most compared to the same period since 2015, according to data compiled by Bloomberg. Borrowers in New York, California and Texas have made the biggest contribution.

Utilities need to nearly triple the pace of capital improvements over the next 25 years to meet drinking water infrastructure needs, according to a March report from the American Water Works Association, which represents more than 4,300 utilities.

“You have a combination of issuers needing to replace and renew aging infrastructure, and the needs to finance new development to support growth,” Ajay Thomas, head of public finance at FHN Financial, said in an interview. The proliferation of data centers being built to power the artificial intelligence boom will spur debate on how to manage demand, he said.

Higher regulatory demands and climate resilience needs are also “driving additional issuance,” said Sarah Sullivant, sector lead for local governments at S&P Global Ratings. She added that the risk of lower federal funding is pushing more utilities to tap the municipal bond market.

The Trump administration’s fiscal 2027 budget proposes sharp cuts to water infrastructure funding, including the clean water and drinking water state revolving funds, which provide low-cost financing to communities.

Sullivant also flagged broader drivers, like inflation driving up construction costs, which are “particularly pronounced in the water sewer sector because of the significant infrastructure backlog.”

Sustained Growth

In some states, water-related issuance has swelled from nearly zero to hundreds of millions of dollars. Illinois issued over $1 billion last year, up from a low of about $16 million in 2021. This year, the state has sold over $940 million worth of such bonds.

Given the need for maintenance across the country, water and sewer utilities will be a sustained source of issuance growth in the muni market, said Kimberly Olsan, senior portfolio manager at Newsquare Capital. Issuance of new money in 2026 — rather than refinancing deals — is running slightly behind the pace of last year’s record.

“Supply will continue to grow to a larger extent than others,” Olsan said.

Last month in Texas, strong demand for water funding caused the state’s flagship water financing program to hit its capacity limit the first time. There were $4.2 billion worth of project requests vying for a pool of nearly $2 billion, so the State Water Implementation Fund for Texas had to turn away 13 applications.

Some water and sewer issuers also may be tapping into higher interest from investors trying to diversify beyond general obligation muni bonds, FHN’s Thomas said. Looking ahead, demand from data centers will also be a factor, he said.

Building out new capacity to meet the substantial needs of such facilities in the US could cost at least $10 billion through 2030, researchers including those at the University of California-Riverside and California Institute of Technology wrote in a March report.

“Data centers are absolutely part of the conversation and a matter of the policy and resource implications,” Thomas said.