Markets are always changing — and sometimes the rules of finance do, too. I believe markets are efficient, which means my investment portfolio is pretty much all index funds. My enthusiasm for indexing is based on evidence from the Before Times, when the question of a corporation’s index-worthiness was straightforward. Now there is debate over that question, which raises another one: Are we all active investors now?

First, an important distinction: Believing markets are efficient doesn’t require believing that prices are always “correct.” The efficient-markets hypothesis is just that markets are pretty decent at incorporating information into prices, or better than any alternative.

For this reason, it is very hard to consistently beat the market by picking stocks. Instead, investors should buy passive funds that simply follow an index, like the S&P 500 or the Nasdaq 100. These collections of stocks represent the market as a whole. There are many economic research papers showing that owning all the stocks, based on their size, means less risk and typically higher returns than picking individual stocks. There are no special skills involved, so investors needn’t pay for market research.

Passive investment funds offer diversification for a low price because they follow their benchmark index as closely as possible. But the question of which companies are included in an index is becoming more complicated. It’s not just the biggest ones. In fact, the S&P 500 was never just the biggest companies — as a recent paper points out, only 380 of the 500 largest US companies are in the S&P.

There are standards other than size, though until recently they did not seem important. The S&P 500 won’t include SpaceX for at least a year, for example, and may never, because the company doesn’t meet the index’s requirements for profitability. There are costs to this judgment. The paper estimates the S&P will have a lower Sharpe ratio — a measure of the return of an investment compared to its risk — than if it tracked the biggest 500 companies. These decisions about what to include in an index are becoming more meaningful as markets change.

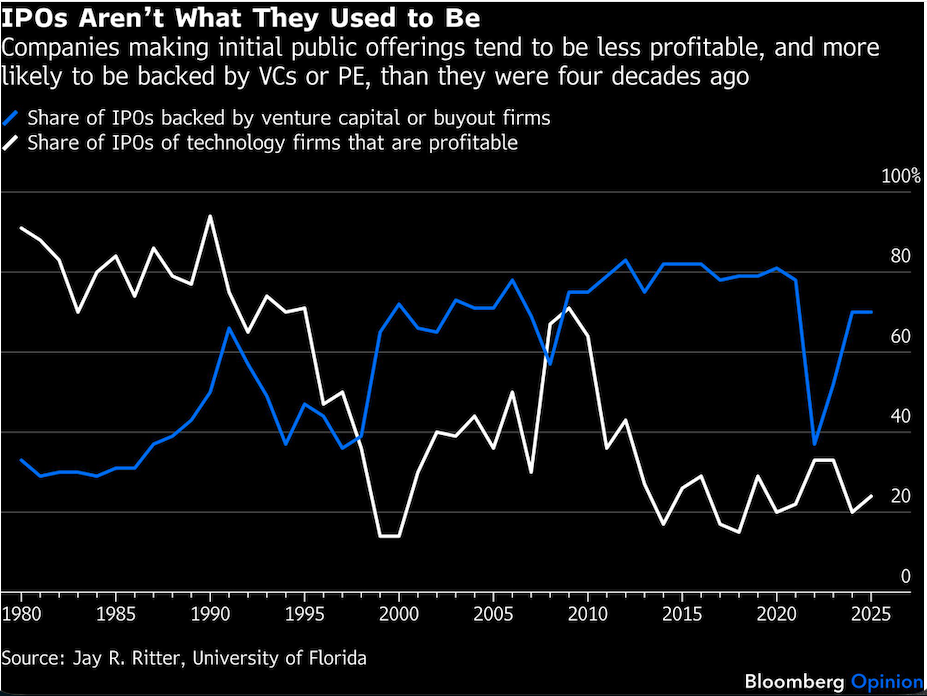

For one, the market has become more concentrated, with a few stocks that are in a similar industry. That means less diversification. For another, firms are going public later and — especially if they were backed by private equity — are bigger and less likely to be profitable when they do.

Since 1980, the median age of a firm at an IPO has doubled, from 6 years old to 12. In 1980, 91% of tech firms that made IPOs were profitable, compared to only 24% in 2025. Finally, in the 1980s the market capitalization of a company on the first closing day of its IPO was typically $20 million to $40 million; in the last few years it has been $100 billion to $400 billion.

These are all good reasons to exercise a little judgment. Older companies that are more valuable yet less profitable could be included in large indices before they are tested in public markets and benefit from all the information priced in. Unlike the S&P, for example, the Nasdaq allowed SpaceX to join the index its first week. As Stanford finance professor Hanno Lustig argues, this effectively imposes a cost to investors, because many firms IPO at a high price, but lose value over the following days as markets price them more accurately. Private investors don’t always care about profitability — they just want to see growth. Public investors, meanwhile, eventually want to see some cash flow.

So far this week, SpaceX shares have been rising, making the S&P’s decision look bad. But it can take at least a year for public markets to price in information, and many big IPO values don’t hold up: On average, three years after their first day of trading, IPOs trade 25% lower. If an index includes a new stock, it probably overpaid for it.

That leaves passive funds with an incentive to deviate from the index, or indices with an incentive to adopt new standards for inclusion. In either case, more judgement will be necessary, which will require more research and talent — and, presumably, more fees. Granted, those fees would still be lower than the ones investors pay for active managers, whose judgment may not be much better. So for now, I am sticking with index funds, even if they’re not so passive anymore.