Say my house burns down under mysterious circumstances (grease fire in the living room?), and police charge my neighbor with arson. It would look awfully suspicious if I then bankrolled my neighbor’s legal defense — it would appear as if we were colluding to burn down my house and collect the insurance money.

Speaking of insurance and the appearance of collusion: The US insurance industry recently joined the fossil-fuel industry in its fight to avoid being sued over the damage oil, gas and coal emissions have done to the planet. Given that insurers are supposedly among the world’s biggest sufferers of those same climate-fueled losses, this was a perplexing choice — until you think about why Big Insurance and Big Oil might be on the same team.

Late last month, three US insurance-industry trade groups, including the American Property Casualty Insurance Association (APCIA), filed a friend-of-the-court brief to the Supreme Court in defense of Exxon Mobil Corp. and Suncor Energy Inc. The companies want the high court to toss out a lawsuit brought against them by the county commissioners and city of Boulder, Colorado, which are seeking compensation for climate-related damage.

In their brief, the insurance groups echo Big Oil’s argument that the suit amounts to carbon-emissions regulation, something state and local governments shouldn’t do because that’s the federal government’s job. This argument is a logical flop because a) Boulder has no interest in regulating emissions, just getting some money to help with weather disasters; and b) the current federal government under President Donald Trump has declared that regulating emissions isn’t its job, either.

“One would think that for an industry that constantly complains about how climate change is hurting its business, it’d be in favor of regulation wherever it can get it,” Rick Morris, an insurance campaigner with the nonprofit group Public Citizen, told me. “Insurers should be the No. 1 champions of state-based climate regulation when federal regulation is failing.”

Instead, Morris noted, insurers have routinely sided with fossil-fuel companies in fighting state-level efforts to hold Big Oil accountable for cleaning up and preventing climate damage, from Hawaii to Connecticut. At least 10 states have sued the fossil-fuel industry, and at least a dozen have passed or are considering superfund bills that would tax the industry to help cover losses and build resilience.

In their brief, the insurance groups warn that letting just anybody sue fossil-fuel companies will sow chaos, rendering insurers unable to price the companies’ climate risks. That will make it harder to insure them, meaning (even more) exorbitant energy prices for the rest of us because the fossil-fuel industry will have to jack up prices to cover going about its business.

“Our amicus filing in Suncor should not be read as an alignment with, or endorsement of, the fossil fuel industry,” Joanna Coll, APCIA’s general counsel, said in a statement. “Our position is a legal one: Claims involving emissions require a uniform standard because emissions do not stop at state borders, and conflicting state-by-state liability rules would create uncertainty and inconsistent outcomes, rendering it difficult for insurance companies to assess and price risk.”

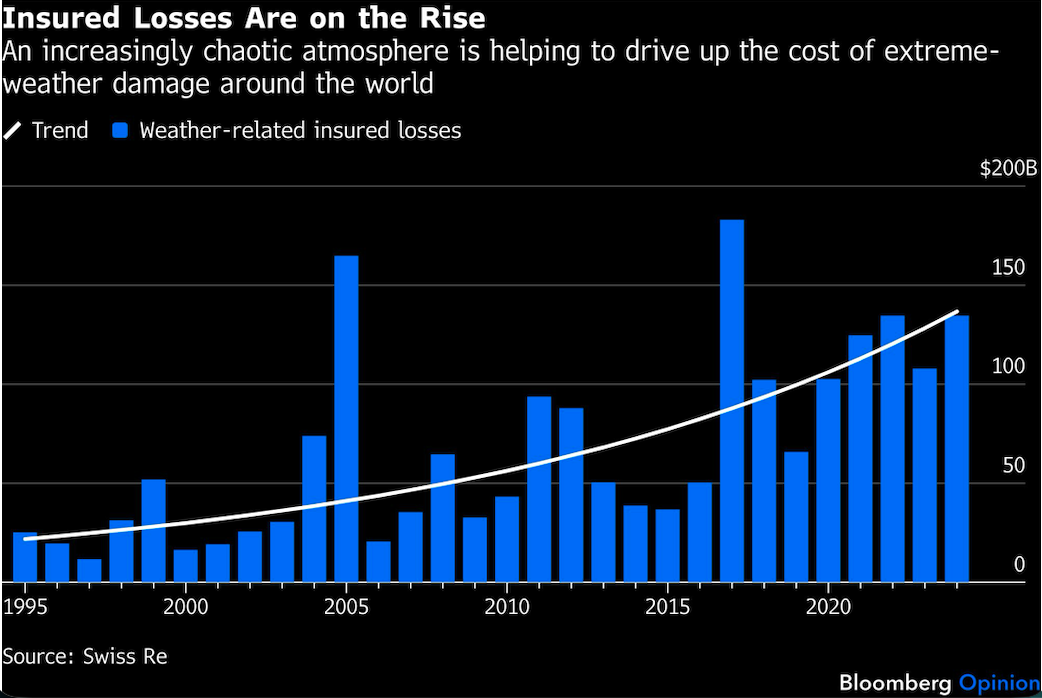

But would such an outcome really be so bad? Several insurance companies have already backed away from covering coal extraction and some oil and gas projects. They’ve been inspired in part by the natural disasters that now routinely inflict at least $100 billion in global insured losses every year, thanks largely to an atmosphere made hotter by burning fossil fuels. No argument in the insurers’ Supreme Court brief hints at any benefit worth $100 billion a year.

Big Oil’s climate risk may become more difficult for insurers to price, but there must be some level on the supply-demand chart where the fossil-fuel companies’ need for coverage will meet insurers’ need for certainty. And anything that makes pulling these pollutants out of the ground more expensive is a step toward replacing them with cleaner energy sources.

It also seems doubtful that fossil-fuel companies would let the lawsuit-chaos era last for very long. Likelier would be an industrywide settlement, like the one state attorneys general reached with Big Tobacco in 1998. That master agreement quickly took shape once the state lawsuits started piling up, as they’re starting to do for fossil fuels.

Such a deal would cost Big Oil billions of dollars, of course. That’s one reason it’s scrambling for immunity shields in Congress and at the Supreme Court. Its water carriers in Congress and think tanks are already attacking the authors of a coming report from the National Academies of Sciences, Engineering, and Medicine promising to tie climate damage even more specifically to fossil-fuel companies, Politico reported last week. The report will be a powerful weapon for plaintiffs’ lawyers. But a tobacco-style master settlement would at least provide the certainty insurance companies say they need.

But let’s assume, as I do, that Big Oil will eventually obtain legal immunity. It’s still worth exploring why Big Insurance would favor that outcome. Following the money offers some clues.

Many of these insurers earn steady income covering fossil-fuel projects. The world’s top 28 global property and casualty insurers collected $11.3 billion in such premiums in 2023, according a 2024 report by the Insure Our Future collaboration of nonprofits.

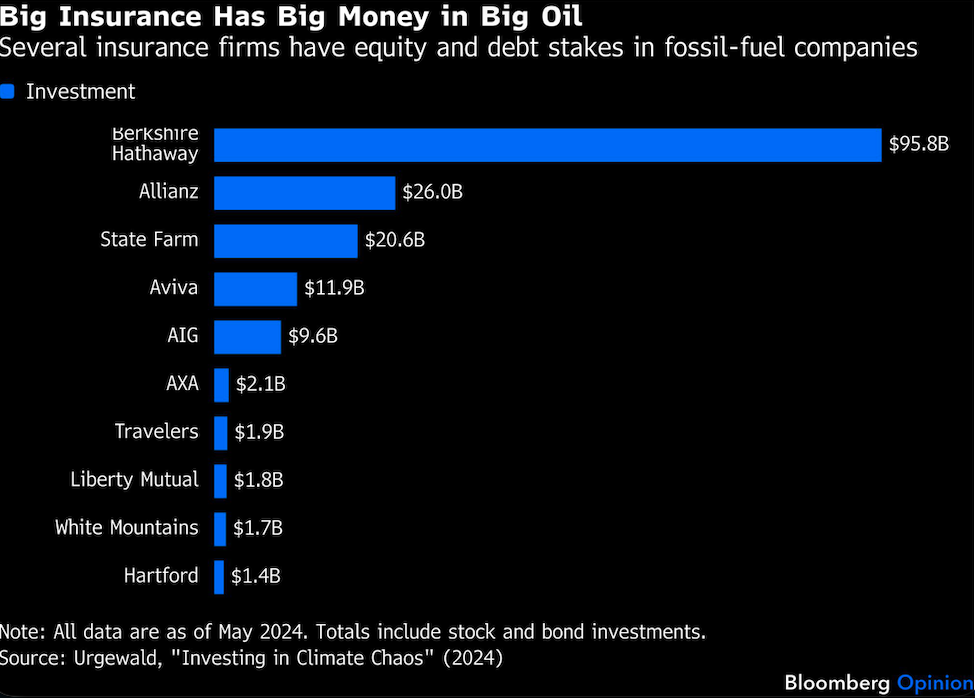

And the property and casualty insurance industry alone had $84 billion in fossil-fuel investments in 2023, according to a 2024 Wall Street Journal analysis. A database compiled in 2024 by Investing in Climate Chaos, a project of the German nonprofit Urgewald, found 20 large insurers exposed to weather damage had $180 billion invested in oil, gas and coal companies.

A top name on that list was State Farm, the biggest US home insurer, with an estimated $20.6 billion in fossil-fuel stocks and bonds as of 2024. Today, the company has $10 billion in oil-and-gas equity investments alone, or 5.7% of its portfolio, according to Bloomberg data. It’s a large investor in Exxon Mobil Corp. but has no stock in renewable energy. Last year, it earned $6.2 billion from investments compared with $1.5 billion from underwriting.

All along, State Farm has been retreating from California’s home-insurance market, saying it can’t take any more wildfire losses. Meanwhile, it and the other four-biggest US home insurers have steadily ratcheted up claim denials, which hit 44% last year, up from 36% a decade ago, the Journal reported recently. The highest percentage of denials was in disaster-prone Florida.

Add it all together, and it’s easy to suspect insurers are willing to accept a little climate chaos in exchange for the reliable income stream of fossil-fuel investments and underwriting, especially if they can find ways to avoid picking up the tab for that climate chaos.

How long that status quo can stay comfortable for insurers is the question. The income from fossil fuels will become less reliable the more voters connect the dots between oil and gas projects and the fact that they no longer have a roof.

Chubb Ltd., which grossed $745 million in fossil-fuel premiums in 2024 by one estimate, last year dropped coverage of the Calcasieu Pass LNG terminal in Louisiana. The reasons for Chubb’s withdrawal aren’t clear, but it followed months of protests that included a focus on insurers’ role in the project. It’s a reminder that you can profit from self-harm for only so long.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.