BHP Group Ltd. never seems to pick the right moment to sell its fossil fuel businesses.

Consider coking coal. The high-quality solid fuel used in steelmaking was for many years seen as a jewel in BHP’s crown. At the peak, its mines in the Bowen Basin of Australia’s Queensland state accounted for about a quarter of such coal traded by sea. It’s a relatively small, volatile business, but when supply and demand get out of line, the profits can be extraordinary. The last time prices spiked, in 2022, the world’s biggest miner sold more than $10 billion of the stuff at a 62% profit margin.1

That would have been a good moment to get out. Coking coal’s charms have since faded drastically. Chief Executive Officer Mike Henry, a veteran of BHP’s coal unit who always speaks highly of its potential, has been shrinking the business ever since taking over in 2020. Sales in the 12 months through June 30 came to just 17.8 million metric tons, about 41% of the figure in 2019. Further mines may have to close if current low prices persist and Queensland doesn’t cut royalty taxes, he warned in annual results last week.

Taxes aren’t sufficient to explain the problem.

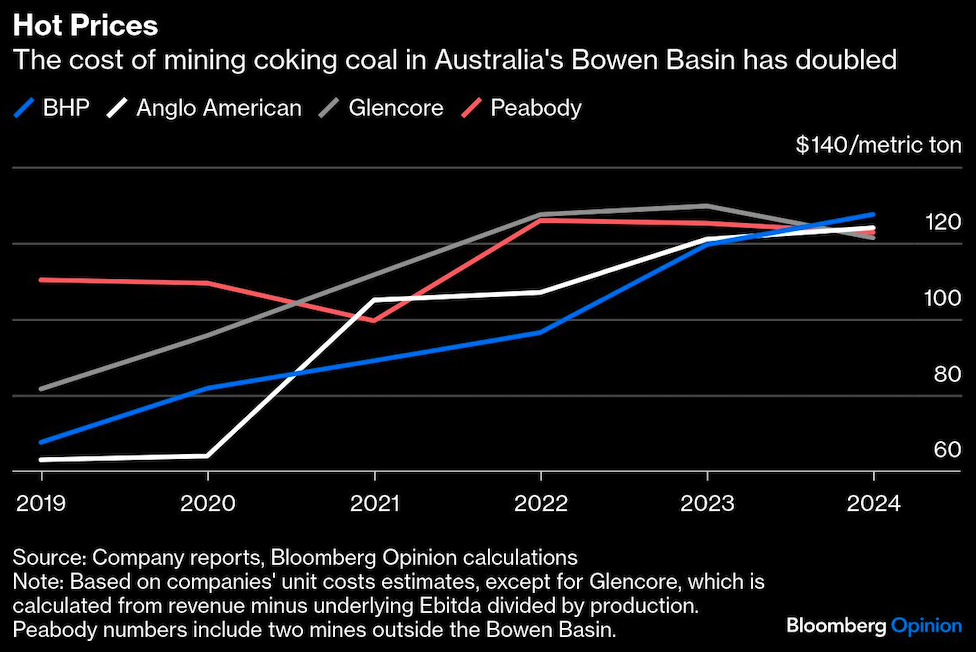

One factor is that it’s getting increasingly expensive to mine in the Bowen these days. Unit costs at the four big miners there have almost doubled over the past five years. Depreciation has increased just as dramatically. As open pits worked for more than 50 years (in BHP’s case) descend deeper and deeper into the ground, more earth needs to be moved, more diesel burned, and more dump trucks worn out to reach seams of coal and bring it back to the surface.

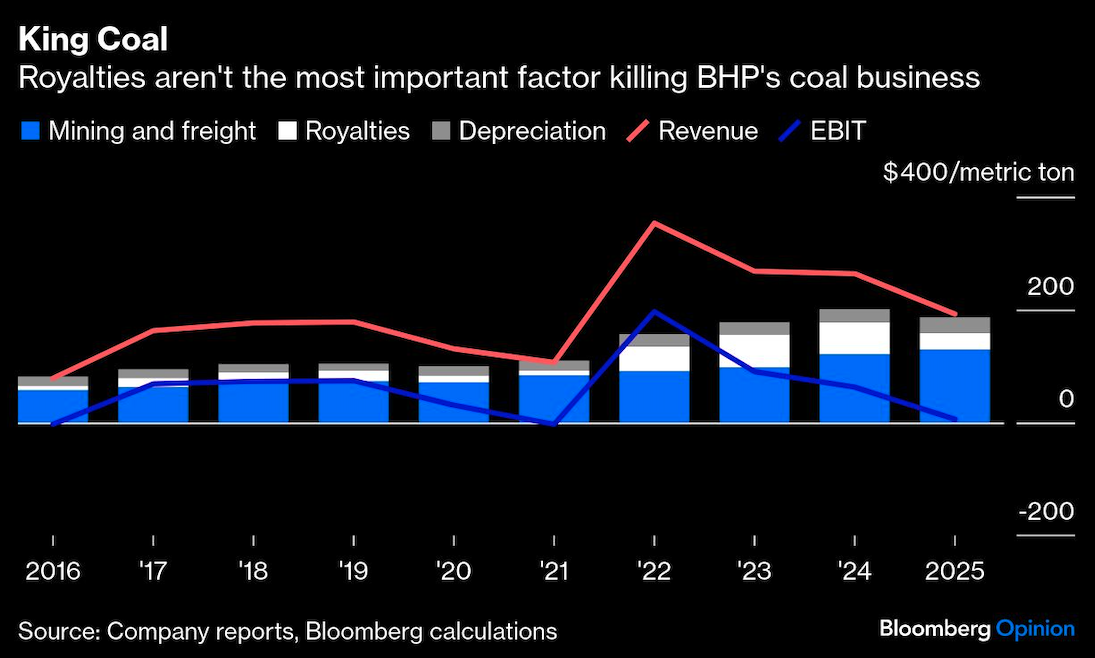

Last year, BHP spent $157 per metric ton on mining, freight and depreciation alone. With royalties of $30 per ton and coking coal fetching $194 per ton, that left the business looking marginal at best. Earnings before interest and tax were just $101 million. Peabody’s Energy Corp.’s decision last week to walk away from a promised $3.8 billion takeover of Anglo American Plc’s Bowen Basin pits, which have been plagued by operational problems in recent years, is emblematic of the darkening outlook for the region.2

In many ways, Queensland’s mines are victims of their own dominance. When coking coal prices spike, it’s generally because the Bowen has been hit by record rainfall, starving a global export market which gets about half its product from the basin. That’s the time when BHP and its rivals most want to make money — but they rarely can, because their own pits are underwater.

Queensland’s royalty regime is so annoying to the Bowen’s miners because they do best in the aftermath of such crises. With rates that escalate as coal prices rise, the new system introduced in 2022 sharply reduces the super-profits they count on to see them through the lean years.

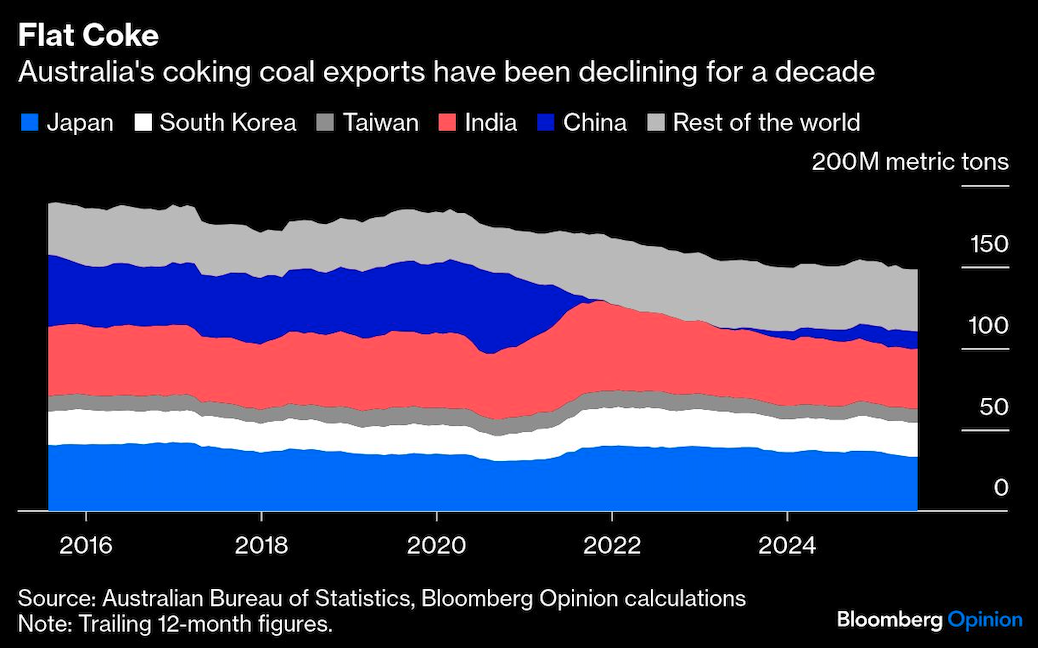

The bigger problem, however, is simply that coking coal is looking more and more like a declining market. China can produce enough for its own steel industry domestically, and has even been exporting cargoes of late. India, held out for years as the great hope of the industry, also may not be coming to the rescue.

Unlike China, which has depended heavily on blast furnaces and pig iron to make its steel, India favors a variety of alternative routes that eschew coking coal — from electric furnaces fed by recycled scrap, to direct-reduced iron, which can make use of abundant domestic lower-grade coal instead. On a trailing 12-month basis, India’s imports of Australian coking coal peaked back in 2021, and have since fallen by more than a third. Steel production over the same period has risen by nearly 40%.

There’s no other sizeable growth market emerging. Global pig iron production has already peaked and will fall 20% by 2050 as scrap and direct-reduced iron edge out blast furnaces, Li Jiang, chief analyst of the world’s biggest steel producer Baoshan Iron & Steel Co., argued recently. More than half of steel capacity under development consists of coal-free electric furnaces, and India has only started construction on a fraction of the blast furnaces it has promised to build, Global Energy Monitor, a pro-transition group, wrote in May.

Incoming BHP chief executives typically start the job by getting rid of coal mines their predecessors clung on to for too long. One of Henry’s first moves in 2020 was to sell off lower-grade pits that the former boss Andrew Mackenzie had cherished. Mackenzie, in turn, began work in 2013 by spinning off underperforming South African and Australian mines as South32 Ltd. With another change of leadership soon pending, the last vestiges of BHP’s once-mighty coal business may now be living on borrowed time.

1. Based on earnings before interest, tax, depreciation and amortization.

2. Peabody blamed Anglo's latest mine fire, in March, for changing the financial logic of the deal.

Prepare your bond portfolio for changing market conditions. Register today for the Fixed Income Symposium on Sept. 18, 2025, 11AM ET / 8AM PT.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by David Fickling