Consider the humble bank note. Wrinkled and torn as it may be, it’s the only government-issued legal tender — the only direct obligation of a central bank — to which most people have access. It’s foundational to the many forms of private money, such as bank deposits and Venmo balances, that now dominate daily commerce. Their value ultimately depends on the ability, if necessary, to convert them into cold, hard cash.

What to do, then, when finance goes digital? The European Central Bank is aiming to be among the first of its peers to fully address the question. It’s an experiment worth watching closely.

For several years, the ECB has been preparing to issue what it calls the digital euro. Like a bank note, it would be central bank money, transferable by its holder to anyone at will, with no verification of sufficient funds required. Unlike a bank note, it could reside on a smartphone and travel like a text message, reaching Budapest from Brussels in an instant. If the European Parliament approves, the first transactions could happen before the end of the decade.

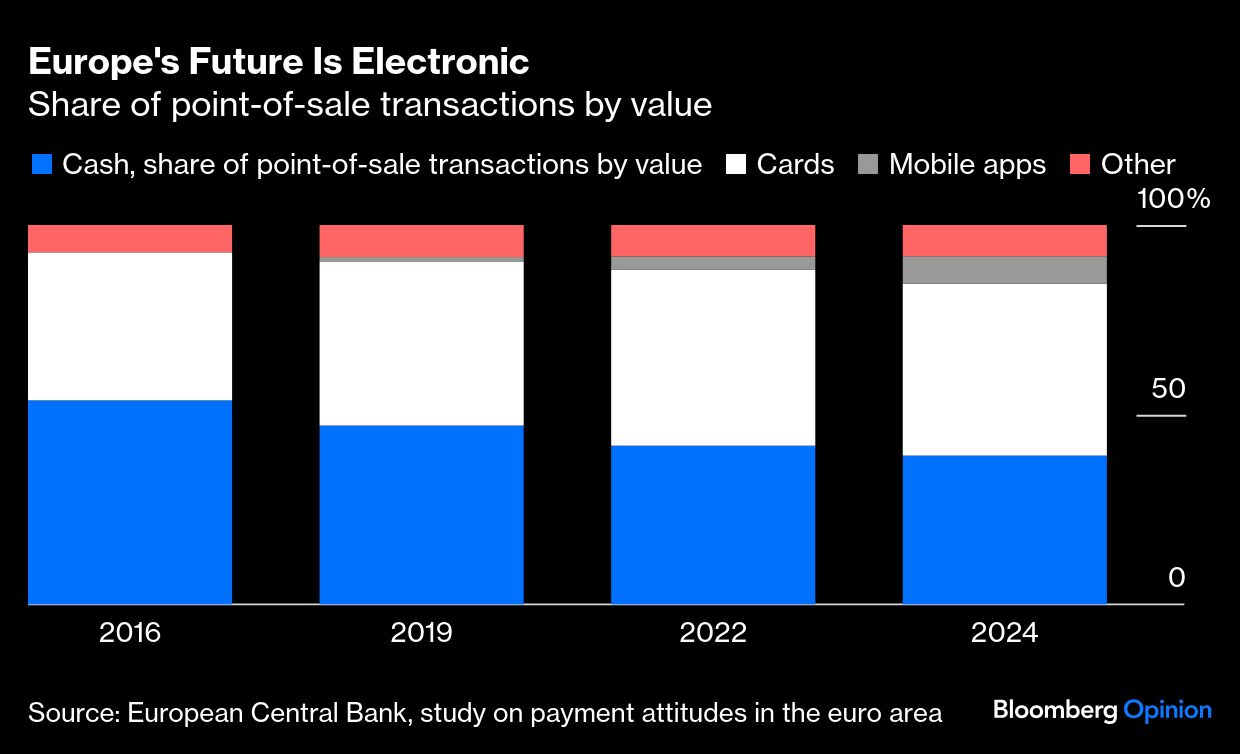

Europeans might reasonably ask why they need such an innovation. After all, they’ve long been able to send bank deposits to one another in a matter of seconds. They can buy everything from clothes to ice cream using the likes of Visa and Mastercard. The ECB estimates that such cards accounted for 45% of point-of-sale purchases (by value) in 2024. Cash accounted for 39%, down from 54% in 2016, as an increasing share of companies chose not to bother with it.

So why not just let private money take over? Attractive as the idea sounds, it presents serious risks. Deposits are obligations of banks, which may be too fragile to be reliable stewards of the currency — as the runs on Silicon Valley Bank in 2023 and Greek banks in the 2010s amply demonstrated. Relying on US-headquartered institutions such as Visa Inc. and Mastercard Inc. may present legal or political risks. If people struggled to use private euros and couldn’t get their hands on euros issued by the central bank, they could lose confidence in the currency. If they turned to alternatives such as dollar-denominated stablecoins, the ECB could lose control over monetary policy in the euro area.