What do one of the largest private-school operators in the UK, a Spanish waste management company and a European fast food franchise of Burger King have in common? Their private equity owners are readying sales that don’t need debt underwriters.

PE firms including Cinven, Platinum Equity and Jacobs Holding have inserted provisions into debt agreements this year that are alarming bankers who stand to lose out on some of the most profitable fees on Wall Street. These portability clauses allow private equity firms to buy and sell companies without fresh borrowings — and they’re appearing with increasing regularity in refinancings on both sides of the Atlantic.

“As it catches on in loan docs, it raises a difficult quandary for banks who will lose out on the lucrative fees that come with underwriting financing in the LBO market,” said Sabrina Fox of Fox Legal Training, a leveraged finance expert.

The deals are wrong-footing bankers waiting for a revival in acquisitions, where they might earn 2% to 3% in fees on buyout funding, up to $15 million on a $500 million deal. With portability eating into their potential profits, they have less to look forward to from a much-heralded return to deal-making.

Cognita, an education business that could be worth as much as €6 billion ($7 billion) and is entertaining bids from Blackstone Inc. and CVC Capital Partners Plc, has got its acquisition financing all lined up. It repriced and upsized existing euro and dollar loans this month, a transaction that included a portability provision that will cover at least €1.9 billion-equivalent of borrowings related to its sale by Swiss investment firm Jacobs Holding.

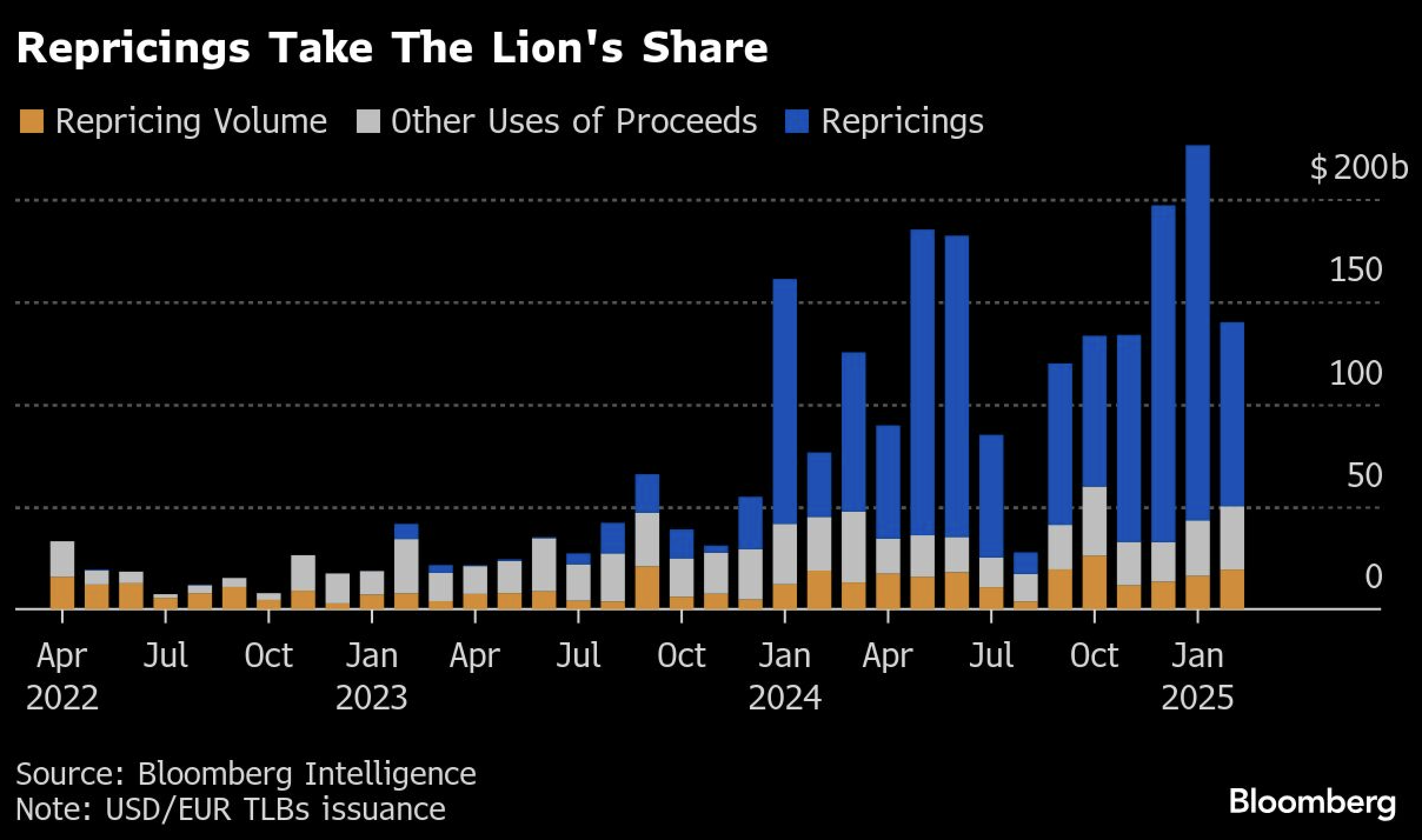

Compared with what the banks could make handling a multi-billion-euro acquisition financing, the fee on the repricing, led by Goldman Sachs Group Inc., would be negligible. Competition for business is so rife that some banks have been willing to arrange repricing deals for free; in Europe they usually pay anywhere between €100,000 to €500,000.

A representative with Cognita declined to comment, as did a representative for Goldman Sachs.

Traditionally, private equity firms buy companies with a mix of their own equity and underwritten debt from banks, which is then sold onto institutional investors. Down the road, when PE owners look to exit their investments, a change of control triggers a repayment of the loans and the start of a new debt-raising and fee-generating cycle all over again.

Portability has interrupted that cycle, and upended the relationship that’s come to define private equity firms and their bankers.

For the PE firms, it’s easier to draw bidders if funding is already in place. That’s especially true as acquisition plans can come apart under trade headlines, and signs grow that the inflationary impact of tariffs are creeping into consumer price inflation.

Spanish sanitation firm Urbaser SA, which is owned by private equity firm Platinum Equity, put a lengthy sales process on ice earlier this year. Later, it raised €2.3 billion from a debt deal that partly paid its owners dividends and also locked in a portability clause. Though Urbaser is no longer officially soliciting bids, offers can still come in, and the funding is an extra enticement to potential buyers.

“Portability is being requested on a number of opportunistic financings and can make a target more attractive to bidders when it comes to an M&A process,” said Jeremy Duffy, a partner at law firm White & Case LLP who advises on leveraged finance.

Bankers worry that portability is a scourge spreading quickly through the buyout industry, after catching on in bond markets and private credit.

Cinven-backed Restaurant Brands Europe, PAI Partners-backed Infra Group and Ardian-backed Cerelia have all added portability to opportunistic refinancings, according to people familiar with knowledge of the deals who asked not to be identified when discussing private transactions. They say more deals with portability are in the pipeline.

Representatives for Cinven, PAI and Ardian declined to comment. Representatives for Platinum Equity and Jacobs Holding didn’t respond to a request for comment.

PE firms, once they have the option of portable financing in place, can also choose not to use it but instead squeeze underwriters pledging new financings. The option acts like a safety net to reduce the risk of a new loan and drive down its pricing and fees.

Don’t Know, Don’t Like

Investors are also worried. They’re trying to add restrictions to portability to protect themselves from lending to a company that could end up being owned by a firm they don’t know or don’t like.

They’ve asked private equity owners to stick to approved buyers identified on “white lists,” according to people with knowledge of the matter.

Yet these sprawling lists give only the illusion of exclusivity — more than 160 funds were named as approved buyers of Cognita — making them all but meaningless.

In the bond market, where the practice is more prevalent, investors have pushed back with some success. Rocket Software dropped a proposed portable structure on a bond last year at the urging of prospective investors, according to people with knowledge of the matter. A representative for Rocket Software didn’t respond to a request for comment.

In Europe, firms are acceding to some demands from investors regarding the size of the new buyer, the timeframe around a sale, ratings and leverage levels, according to people with knowledge of discussions.

Investors are seeking to limit the use of portability to once during the lifetime of a financing agreement and asking that the option expires after two to three years.

“Investors have never liked it,” Fox said. “Given the value of the option for sponsors, however, it is a trend that’s unlikely to reverse given that they remain in the driver’s seat when it comes to terms.”

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.

Read more articles by Claire Ruckin, Reshmi Basu