US banks seem likely to get the changes they want to an obscure but important rule known as the supplementary leverage ratio. The leading reform proposal should cut the capital that banks need for this measure and help make the Treasury market more resilient, but not lead to a giveaway of shareholder capital that could undermine their safety. For the financial system, that’s a win-and-not-lose outcome.

Treasury Secretary Scott Bessent has been pushing for this to be the first major financial reform since he took on the job. The Federal Reserve said on Tuesday that it will discuss the changes next week and hold an open meeting. Two main changes have been under discussion. The first is to take Treasuries out of tallies for the size of bank balance sheets, which would mean banks could lend to the government almost without using any equity. The second is to reduce the amount of capital banks need for their whole balance sheet, which would allow them to run a larger balance sheet for a wider variety of assets. The latter option is now the leading plan, Bloomberg News reported this week.

To understand how this helps the Treasury market but won’t mean a flood of bank share buybacks, we need to take a quick step back and look at the two lines of defense in bank capital. There are risk-based rules that measure assets according to how safe or dangerous they are. Under these, credit-card lending requires more capital than mortgages, for example. That’s the first line of defense. At the biggest US banks, between about 10% and nearly 14% of risk-weighted assets need to be backed by common equity.

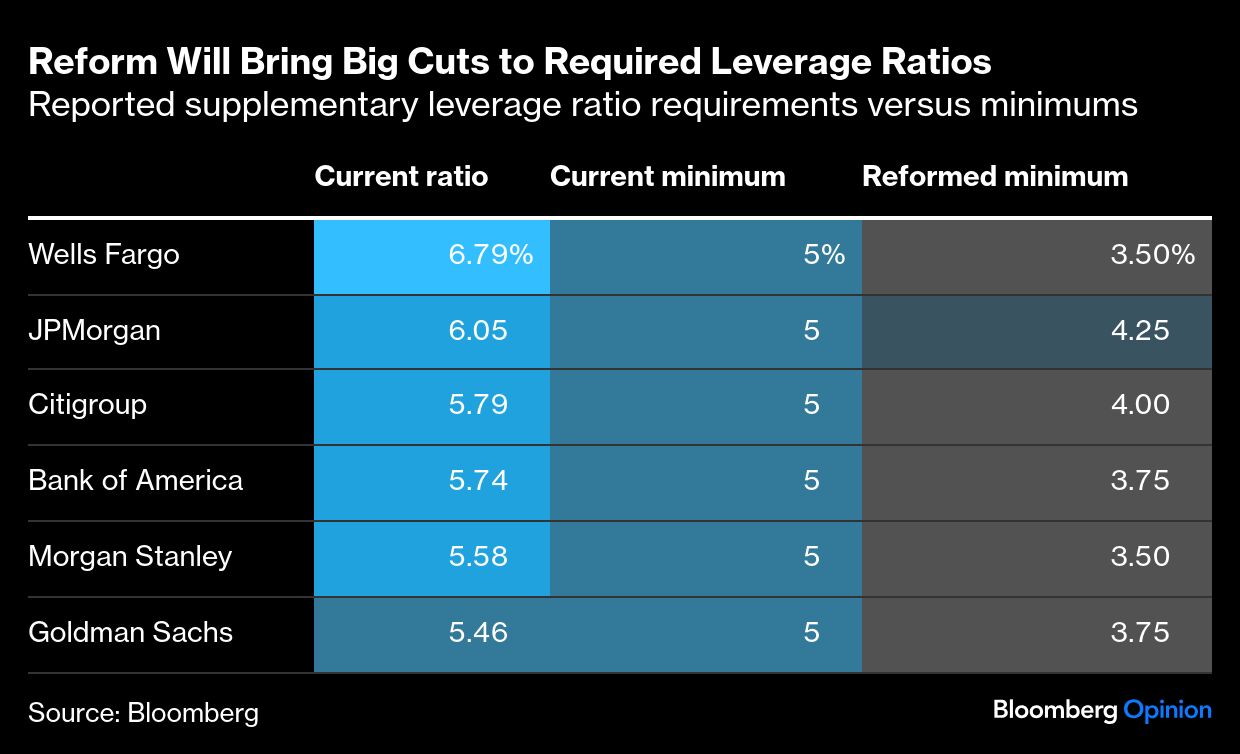

In contrast, the supplementary leverage ratio treats all exposures the same, so a dollar of credit-card loans counts the same as a dollar of mortgages or government debt. The biggest banks currently need equity and other tier one capital (typically preferred shares) of at least 5% of all assets measured in this simpler way. This is the second line of defense and the main reason it exists is just in case the more sophisticated risk-based measures turn out to be too clever for their own good and the banks become more highly leveraged – and riskier – than watchdogs intended.

America’s 5% leverage ratio is higher than in other markets. For big US banks, this second line of defense is much too close to the first. It constricts them too quickly when the Fed floods the financial system with cash, or when there’s a major selloff in Treasuries, like in early 2020 when both things happened. When banks suddenly need to take much more cash or low-risk government bonds onto their balance sheets, even briefly, it doesn’t hurt their primary capital ratios, but it can lead them to breach their leverage ratios. In other words, they get too big for the tier-one capital they have and have to stop trading or turn away depositors. When JPMorgan Chase & Co. got close to doing this in 2020, the Fed enacted a temporary exemption for cash and Treasuries to help the financial system cope.

The six biggest US lenders currently must meet a minimum 5% ratio, comprising the 3% that all banks must hit plus a 2% surcharge for being systemically important. That systemic risk surcharge is a US invention, whereas under the reform plans banks would use the 3% base plus half of the systemic capital charge recommended under international standards. The difference would be considerable. Morgan Stanley and Wells Fargo & Co. would see their leverage ratios fall to just 3.5%, while at the top end, JPMorgan would have a 4.25% hurdle.

This wouldn’t lead to a wave of buybacks because all these banks would still be bound by their first lines of defense. At the low end, Wells Fargo would still have to meet its risk-based common equity ratio of 9.8%, while Goldman Sachs Group Inc., seen by regulators as the riskiest bank, would still have a 13.7% minimum risk-based ratio. (These numbers will change as they do every year when the Fed releases this year’s stress test results next Friday.)

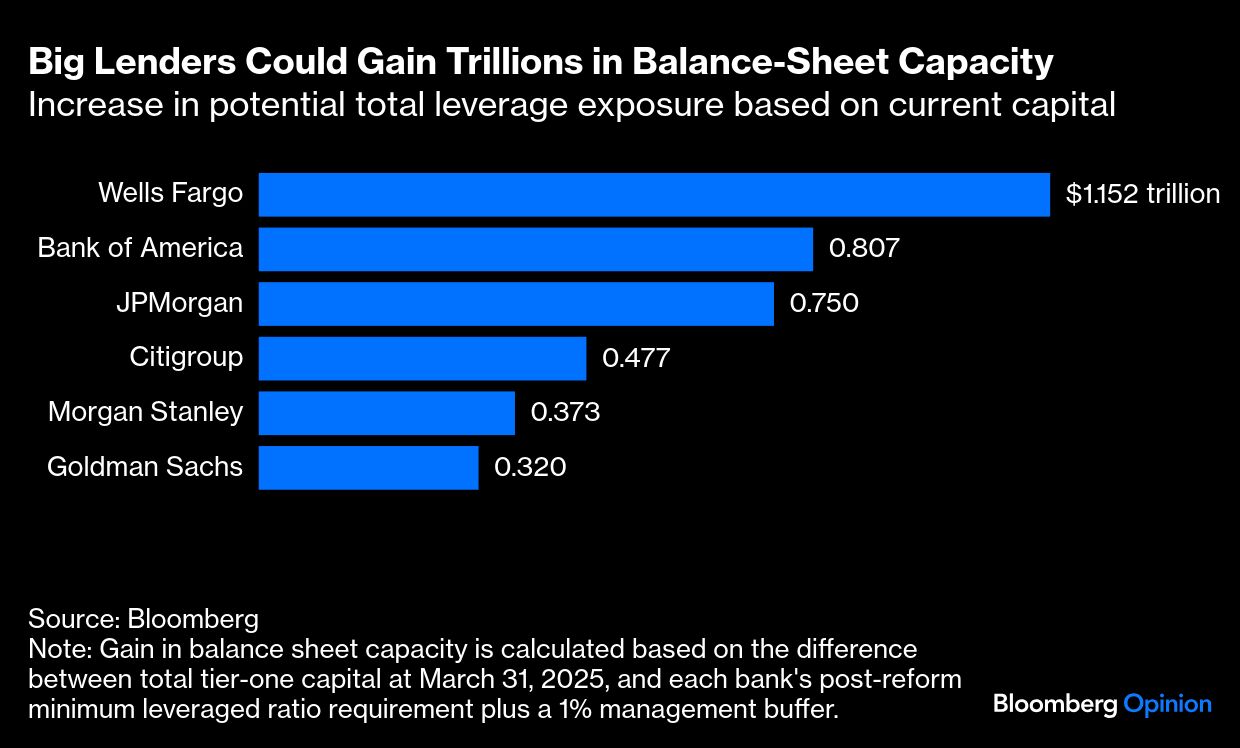

But reforming the leverage ratio will increase the amount of lower risk assets these banks can hold, theoretically by several trillion dollars, although they wouldn’t want or be able to max this out. That increases the capacity of lenders to absorb a future round of quantitative easing in a crisis, for example. It would improve the elasticity of their balance sheets, allowing them to expand and contract to take on spikes of activity in trading Treasuries, high-grade mortgage bonds and corporate debt. It would likely also boost the lending that investment banks can do for hedge funds where that financing is collateralized with shares or bonds that can be easily sold if the fund defaults.

But how much could be put toward buying more Treasuries as Bessent hopes? If banks used 1% of their extra balance sheet space for government bonds, that would mean about $40 billion of extra demand. If they used 5%, as analysts at Wells Fargo assume, that would mean almost $200 billion of extra demand.

However, banks already hold a lot of Treasuries. For example, Bank of America Corp., which would see one of the biggest nominal increases in balance sheet capacity with this reform, already holds about $760 billion of government and agency debt. There is risk related to interest-rate changes involved in these investments, which can be painful. Either it makes a bank’s capital more volatile if the bonds are marked to market, or it can leave the lender with large unrealized losses, which make investors nervous. If banks do take on more government debt, it would likely be much more in the form of short-term bills rather than multi-year bonds.

The $29 trillion Treasury market needs to be reliably tradeable. This debt doesn’t just fund America’s government, it has also become an important store of value and source of quick liquidity for investors, while providing the foundations for the vast world of shadow banking, which has become increasingly important in funding the wider US economy.

Supplementary leverage ratio reform – as niche as it sounds – looks a good step in protecting all of this. It doesn’t solve all the problems of fragility in Treasuries, or offer America a ticket to endless borrowing. But it makes a major crisis in government debt at least a little less likely.

Gain clarity on H1 & strategize for the remainder of the year. Register now for the Midyear Market Outlook Symposium on June 26 at 11 am ET.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.