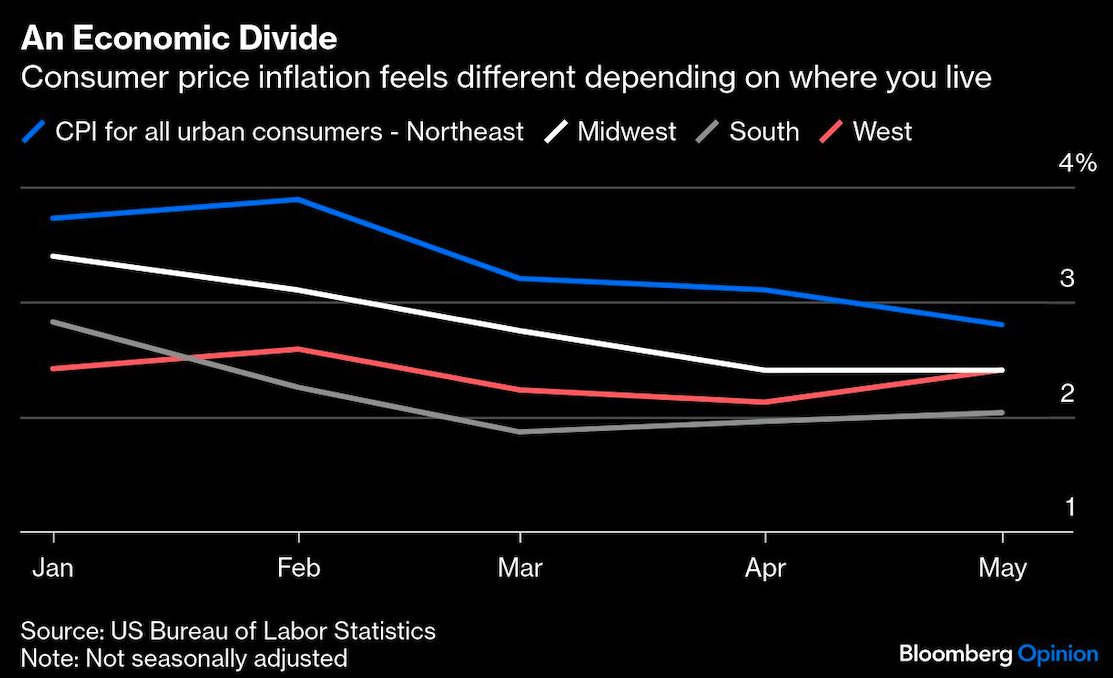

US economic data continue to send mixed signals, keeping uncertainty high on interest rate cuts from the Federal Reserve later this year. This cautious policy stance is likely appropriate in the Northeast and Midwest, where inflation remains elevated, in part due to the continued increase in home values. It will, however, be painful for the South, where price gains have slowed and risks to the economy from a housing slump are intensifying.

Nationally, inflation is higher than the Fed’s 2% target primarily due to the lagged impact of house price gains from the early 2020s still working their way through the economy. Excluding housing, the Consumer Price Index rose 1.5% in May from a year earlier, similar to levels experienced in the late 2010s when rates were much lower and inflation wasn’t a concern for policymakers or the general public.

The challenge for the Fed is that troublesome housing inflation is concentrated in the Northeast and Midwest, both regions that don’t build much for structural and regulatory reasons. Meanwhile, in the rest of the county, the housing parts of the economy — home prices, construction activity and related employment — are sliding deeper into downturns. This is particularly true in states such as Texas and Florida, where pandemic-era booms in real estate and interstate migration have become slumps.

Across the South, headline CPI rose 2% in May from a year earlier, compared with 2.8% in the Northeast and 2.4% in the Midwest. In Dallas, where home prices are basically flat year-over-year, shelter inflation growth has dropped to 1.6% after peaking north of 10% in 2023. This has pulled headline inflation down to just 0.6%.

Housing is a big part of the sluggishness across the South. At the end of May 2025, Texas, Florida and Tennessee were among 10 states with housing inventory levels higher than in May 2019, according to ResiClub, a housing analytics site. (The Western states of Arizona, Colorado and Washington are also struggling in this regard.) That’s putting pressure on prices; nationally, 14 of 20 metros tracked by the S&P CoreLogic Case-Shiller home price indices showed declines in March from the previous month.

These softness should continue as resale inventory climbs across the country, led by the Southern states. What lies ahead is a painful period of price discovery for sellers who need to move for life or financial reasons at a time when housing affordability is substantially worse than it was in the late 2010s and mortgage rates have been sticky around 7%.

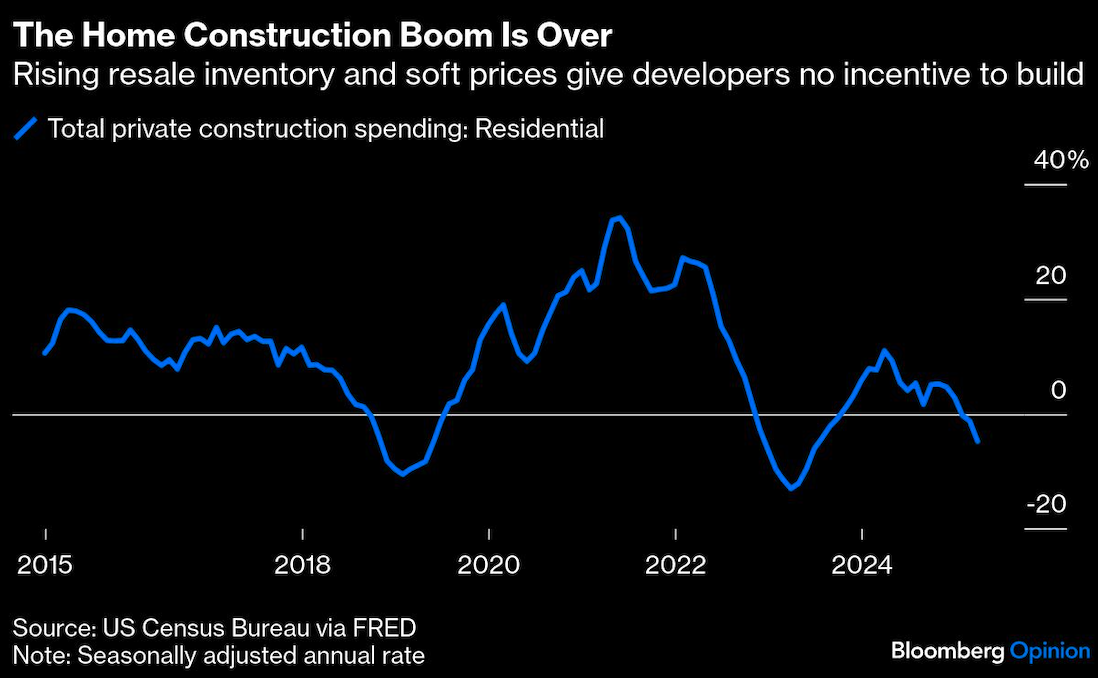

The weakness in southern housing markets has been a theme for a few years, but for a while it didn’t translate into price declines because low inventory and the mortgage lock-in effect kept transactions to a minimum, supporting the illusion that prices were stable. Developers, offering mortgage buydowns, stepped in to provide homes that the resale market could not, boosting construction activity.

That trend has now run its course with homebuilders tapping the brakes on residential construction spending, which is now declining on a year-over-year basis. Employment in the sector fell in May from a year earlier for the first time since mid-2020.

A broader downturn in the region’s housing markets will weigh on household balance sheets and consumer psychology. There doesn’t need to be a 2008-type housing bust for falling residential construction activity and employment along with declining home prices and poor affordability to lead to broader economic problems.

For all the talk that tax cuts and deregulation in Washington will boost economic growth, it’s worth noting the regional impact that the reconciliation bill working its way through Congress will have. Increasing the state and local tax deduction will benefit residents of high-tax states such as New York, New Jersey and California to the tune of hundreds of billions of dollars, but do much less for southern states with low or no state income tax. Meanwhile, the South, which received a chunk of electric vehicle, battery and other projects kickstarted by the Inflation Reduction Act, is now likely to bear the brunt of downsizing and cancellations as Congress moves to gut the legislation’s green investment tax credits. Simultaneously, the White House’s stepped-up efforts to increase deportations and crack down on illegal immigration will hurt economic activity in states near the border with Mexico.

I worry that in the two and a half years following the Fed’s aggressive interest rate increases, starting mid-2022, we saw something akin to the economy holding its breath after policymakers sucked the oxygen out of the room. Would-be home sellers stayed on the sidelines, holding on to their cheap mortgages and helping homebuilders for a while. Real estate professionals encouraged buyers to “date the rate, marry the house” assuming that the opportunity to refinance into a lower mortgage rate would soon emerge. The rest of the economy had other sources of momentum ranging from pandemic-era stimulus to green investments.

Now, trends in inventory, home prices and construction activity suggest the laws of gravity are at work. And it’s happening at a time when the other sources of strength for the economy have faded, with green investment growth decelerating and governments looking to cut costs. Investments in artificial intelligence, though, remain a bright spot.

The risk is that the housing market weakness in the South doesn’t stay contained, and we get a repeat of 2021 in reverse. Back then, housing inflation that started in places such as Florida and Texas evolved into a national problem by the Spring of 2022. At the time, policymakers were focused on supply chain issues. Today, they are monitoring the uncertainties related to trade and fiscal policies, when it’s this slow-moving housing downturn that’s becoming a bigger risk in many parts of the country.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Bloomberg News provided this article. For more articles like this please visit

bloomberg.com.